The inherent contradiction of regulation exposed (again)

A few weeks ago, Reuters reported that a new research report (I can’t seem to find the original paper, which is still a work in progress) published by two German academics (Wolfgang Gick and Thilo Pausch) recommended that bank supervisors “withhold some information when they publish stress test results to prevent both bank runs and excessive risk taking by lenders”.

I have pointed out multiple times that this was an intrinsic problem to bank regulation, and that Bagehot had correctly identified the issue already in his time. Our societies have, since then, tried to conveniently forget Bagehot’s wise remarks.

Reuters continues:

If depositors know from the watchdog that banks are in trouble, they will withdraw their cash, threatening lenders’ survival and causing the panic the supervisor is trying to avoid, the paper said.

Exactly. And wholesale markets are even more at risk. The authors then recommend that “the amount of information disclosed by supervisors should decrease the more vulnerable the banking sector is expected to be.” Is this going to correct the problem? Evidently not. As the public starts to understand that ‘less information about a given bank’ equals ‘riskier bank’, withholding information from the public domain will become self-defeating.

The authors also correctly highlight that

giving banks a clean bill of health also carries risks, according to Gick and Pausch, by encouraging depositors to leave their money in banks. That would undermine market discipline and lead lenders to take excessive risks, they wrote.

In the end, whatever regulators do, negative consequences follow.

Another contradiction was exposed last month when Ewald Nowotny, Governor of the Austrian central bank, warned that proposed changes to the Basel regulatory regime were “dangerous” because borrowing “could become harder for SMEs.” He added that the revised Basel framework had “a sort of bias against bank lending”, and that “banking regulators should analyze the combined effect on the real economy of the multitude of rules that are due to come into force.”

He is both right and wrong. Wrong because the Basel rules have not been loose for corporate lending since Basel was put in place in the 1980s. It’s precisely the opposite. Rules were stricter than for many other lending types, such as real estate lending, leading to the great credit distortion we have experienced over the past couple of decades, and the slow recovery as corporations were starved of credit (see many many of my previous blog posts for details).

But he’s right that the revised Basel framework will perhaps exacerbate this situation by widening the spread between the capital cost of SME lending and that of real estate lending.

This is where the great contradiction lies. Nowotny is one of the first top regulators to underline a part of the credit allocation distortion. Yet most regulators believe that higher capital costs are justified on the basis that SME/corporate lending is inherently riskier. They never admit that the Basel framework played a major role in creating the great real estate credit bubble that led to the crisis. They constantly, and stubbornly, deny that Basel’s risk-weights could have any impact on the credit supply (and hence the sectorial interest rate). Yet, they contradict themselves when, at the same time, they consider lowering those same risk-weights on a number of products (such as securitisations) to boost…their supply and demand!

Let me get this straight: risk-weights are an instance of price control (in this case, capital cost control). And economic theory clearly demonstrates that price controls are both inefficient and leads to economic distortions. You can’t stabilise the financial system using price control tools, and then blame financial institutions and economic agents for rationally reacting to your measures. You just can’t.

Update: I originally used the term ‘price-fixing’ above. I then thought ‘price control’ was more appropriate, so I modified the post.

The Economist’s flawed logic

The Economist this week accused global banks of being “badly managed and unrewarding” (also see its second, more comprehensive article here). It is true that banks have been hit by the crisis and the following regulatory outburst. But the logic underpinning the two articles of the newspaper in this week’s edition is badly flawed and only seems to demonstrate the paper’s bias against banks.

The newspaper admits that

on paper global banks make sense. They provide the plumbing that allows multinationals to move cash, manage risk and finance trade around the world. Since the modern era of globalisation began in the mid-1990s, many banks have found the idea of spanning the world deeply alluring.

Indeed. Global banks evolved from a need: the need to maintain a single (or just a few) banking relationship throughout the world. Globalisation of trade and capital flows inherently implies the globalisation of banking. The current de-globalisation trend that we witness among Western banks is dangerous as this will not help corporations grow their business and hence generate growth.

However, the Economist’s bias appears in that it does not distinguish between banks that are truly global and the rest, and between banks that suffered from the crisis, and the rest. Comparing HSBC, Standard Chartered and Citi with the likes of RBS or Societe Generale doesn’t make much sense. Some have a truly global presence in both retail and investment banking operations, while others only have representative offices or limited product ranges. They do not have the same business models and, despite this, all struggle to generate meaningful RoEs. Moreover, tiny to medium-sized domestic banks also struggle to generate RoEs that cover their cost of capital. Accusing global banks of underperformance thus makes no sense. Identifying some banks that perform relatively well because they focus on regulatory-advantaged businesses such as mortgage lending is irrelevant.

The Economist also targets both banks that needed bailouts and others that did survive the crisis with limited damages. That bailouts mostly involved banks that were not global and that some global banks indeed were saved by their diversified operations doesn’t seem to have rung a bell at the newspaper.

This is unfortunate, as The Economist does acknowledge the impact of regulatory changes:

The wave of regulation since the financial crisis is partly to blame. Regulators rightly decided not to break up global banks after the financial crisis in 2007-08 even though Citi and RBS needed a full-scale bail-out. Break-ups would have greatly multiplied the number of too-big-to-fail banks to keep an eye on. Instead, therefore, supervisors regulated them more tightly—together JPMorgan Chase, Citi, Deutsche and HSBC carry 92% more capital than they did in 2007. Global banks will probably end up having to carry about a third more capital than their domestic-only peers because, if they fail, the fallout would be so great. National regulators want banks’ local operations to be ring-fenced, undoing efficiency gains. The cost of sticking to all the new rules is vast. HSBC spent $2.4 billion on compliance in 2014, up by about half compared with a year earlier. A discussion of capital requirements in Citi’s latest regulatory filing takes up 17 riveting pages.

Indeed. Though regulation isn’t ‘partly’ to blame. It is the primary factor (along with low interest rates) driving the underperformance of banks of all sizes and shapes. The Economist itself several times attacked current regulatory reforms as being unnecessarily costly (see here and here). It now seems to have forgotten and ‘mismanagement’ has become to culprit. For any other industry, The Economist would have blamed regulatory overreach for the industry’s poor performance, in turn pleading for growth-liberating liberalisation. But not for banking. The Economist still hasn’t come to terms with the fact that banks were not the origin, but only the tool, that led to the financial crisis, and as a result remains a ‘classical liberal’ newspaper only when it wants to.

Liquidity and collateral are two sides of the same coin

I recently wrote a piece listing all the current regulatory constraints that arise from banking regulation and which weigh on liquidity. Unfortunately, there is more. As Singh explained in this FT article (as well as in many of his research papers), monetary policy, and in particular quantitative easing, can have serious repercussions on market liquidity:

From a financial lubrication angle, markets need both good collateral and money for smooth market functioning and, ultimately, financial stability. Having a ready supply of good collateral like US Treasuries or German Bunds also helps in reallocating the not-so-good collateral.

QE that isolates good collateral from the wider market reduces financial lubrication. Its substitute, money that shows up as excess reserves, is basically contained in a closed circuit system built to avoid inflation by introducing “interest on excess reserves”.

Indeed, the combination of QE and Basel rules effectively drives so-called ‘high-quality assets’ out of the market by ‘siloing’ them in various places (central banks’ and banks’ balance sheets, clearinhouses’ margins…). This is what many have dubbed ‘scarcity of good collateral’. (I personally think that Singh is wrong to call all highly rated and liquid assets ‘collateral’. When the Fed buys Treasuries, it doesn’t purchase collateral. It purchases an asset that could potentially be used as collateral. Yet, Singh just uses the word ‘collateral’ in every single circumstance. Semantics I know, but the distinction is important I believe)

The potential solution? Governments could issue more debt, meaning more indebtedness. Not certain this is a good one, especially as increased indebtedness would at some point cause the quality of the asset to decline… (reducing the maturity of existing issues could potentially ease liquidity constraints, but the effect is going to be limited)

JP Koning once declared that he didn’t understand how such ‘collateral shortage’ could even happen. Any asset could serve as collateral, with bigger haircut applied to riskier asset to offset potential market value fluctuations. He is fundamentally right. In a free market, there is no real reason why such shortage should ever appear.

Unfortunately, we do not live in a fully free market, and financial regulations institutionalised the use of certain classes of assets as collateral for certain transactions and increased the required associated haircut (for example, see here for OTC derivatives, see here for shadow banking transactions). Many transactions are also pushed towards central clearing at clearinghouses, which often require posting more (standardised) collateral, hence reducing supply by placing high-quality assets in a silo.

Cash, which can also be used as collateral, is itself siloed at the central bank level because of interest on excess reserves*.

As a result of those new rules, the latest ISDA survey tells us that:

Estimated total collateral in circulation related to non-cleared OTC derivatives has decreased 14%, from $3.7 trillion at the end of 2012 to $3.2 trillion at the end of 2013 as a consequence of mandatory clearing.

Regulations have created a lot of ‘know unknowns’. How the entanglement of all those rules will unravel in a crisis will be ‘interesting’ to follow.

* I know that those reserves don’t usually leave the central bank (unless withdrawn by depositors). But when banks expand their loan book, reserves that were previously in excess suddenly become ‘required’ (unless there is no reserve requirement of course).

Vincent points at the new Fatal Conceit

William Vincent, a veteran bank equity analyst, published a very good piece on the SNL website (gated unfortunately).

This is Vincent:

To most people in and around the banking industry, the term Basel III probably means a revised set of capital ratios, building on the two earlier, and failed, Basel structures. They are right, of course. But Basel III means a great deal more. When all of its measures are taken into account, it is clear that regulators are not just introducing another capital ratio regime. They are fundamentally altering how banks are controlled and run.

They are, in short, removing banks’ freedom, within limits, to run themselves as they and their shareholders see fit. In the pursuit of reducing the risk of another global banking crisis, they are tearing up a system that took centuries of trial and error to produce, replacing it with a set of rigid rules that will, in effect, mean that banks’ management will run their institutions on behalf of regulators, not the owners of the business.

To which he adds:

This in itself raises an interesting question: why should regulators be better placed to assess risk than the people who actually do it for a living?

Thumbs up.

Perhaps it is time we raise funds through Kickstarter to send thousands of copies of Hayek’s The Fatal Conceit to regulators?

In defence of the leverage ratio

Regular readers know that I blame risk-based capital requirements for many of the ills of our current banking system. Before the introduction of Basel regulations, banks’ capital level used to be assessed using more standard and simple leverage ratios (equity or capital/total assets). Those ratios have mostly disappeared since the end of the 1980s but Basel 3 is now re-introducing its own version (Tier 1 capital/total exposures).

While I believe there should not be any regulatory minimum capital requirement, I also do believe that, if regulators had to pick one main measure of capitalisation, it should be a standard leverage ratio. All RWA-based ratios should be scrapped.

A new study just added to the growing body of evidence that leverage ratios perform better than RWA-based ones as predictor of banks’ riskiness. Andrew Haldane, from the BoE, has been a long-time supporter of leverage ratios. Admati and Hellwig also backed non-risk weighted ratios. Another paper recently suggested that there was nothing in the literature that justified the level of risk-weights.

Still, most economists, central bankers and regulators consider leverage ratios as mere backstops to complement the more ‘scientific’ (read, more complex, as there is no science behind risk-weights) Basel RWA-based ratios. See this speech from Andreas Dombret, which sums up most criticisms towards simple leverage ratios:

Yet a leverage ratio would also create the wrong incentives. If banks had to hold the same percentage of capital against all assets, any institution wanting to maximise its profits would probably invest in high-risk assets, as they produce particularly high returns. This would eradicate the corrective influence of capital cover in reducing risk.

Unfortunately, Mr. Dombret and many others are very misinformed.

A leverage ratio would not incentivise banks to leverage up to the allowed limit. Under Basel’s RWA framework, no banks operated with the bare regulatory minimum. Critics forget that different banks have different risk aversion and different risk/reward profiles. Some banks generate relatively low RoEs in return for lower level of risk. Others are willing to take on more risks to generate higher margins and higher RoEs. Banks are not uniform.

Banks would not necessarily pile into the riskiest assets under a leverage ratio either. The answer to this is the same as above. Banks have different cultures and different risk/return profiles to offer to investors. There is no reason why all banks would suddenly lend to the riskiest borrowers to improve their earnings. Such criticism could also easily apply to Basel capital ratios: why didn’t all banks follow the same investment strategy? Critics forget that banks do not try to maximise their profits. They try to maximise their risk-adjusted profits. Finally, such argument only demonstrates its proponents’ ignorance of banking history, as if all banks had always been investing in the riskiest assets in the 300 years before Basel introduced those risk-weights.

RWA-based capital ratios are very patronising: because the riskiness of the assets is already embedded within the ratio, banks are effectively telling markets how risky they are. This became overly sarcastic with Basel 2, which allowed large banks to calculate their own risk-weights (i.e. the so-called ‘internal rating based’ method). It has been proved that, for a given portfolio of assets, risk-weights were considerably varying across banks (see here and here). Given the same balance sheet, one bank could, say, report a 10% Tier 1 ratio, and another one, 14%, implying massive variations in RWA density (RWAs/total assets). A given bank could also change its RWA calculation model (and hence its RWA density) in between two reporting periods, making a mockery of period to period comparison. Of course, all this is approved by regulators. Consequently RWA-based capital ratios became essentially meaningless.

As a result, a leverage ratio would provide a ‘purer’ measure of capitalisation that markets could then compare with their own assessment of banks’ balance sheet riskiness.

Scrapping RWA-based capital ratios would also provide major economic benefits. As regularly argued on this blog, RWA-incentivised regulatory arbitrage has been hugely damaging for the economy and is in large part responsible for the recent internationally-coordinated housing bubbles and ‘secular’ low level of business lending. Getting rid of such regulatory ratio would benefit us all by removing an indicator that has big distortionary effects on the economy.

Of course, there are still a few issues, though they remain relatively minor. The main one is that differences in accounting standards across jurisdictions do not lead to the same leverage ratios (i.e. US GAAP banks have much less restrictions to net their derivative positions than IFRS ones). But those accounting issues can easily be corrected if necessary for international comparison. The second one is what definition of capital to use: common equity? Tier 1 capital? Another problem is the fact that very low risk banks, which don’t need much capital, would also get penalised. In the end, it’s likely that any regulatory ratio will prove distortive in a way or another. Why not scrap them all and let the market do its job?

Chart: Guardian

Chinese regulation, the European way

Some European banking regulators are currently considering the implementation of a sovereign bond exposure cap of 25% of capital to any one sovereign. Their goal is to break the link between sovereigns and banks. I think they don’t really know what they are doing.

European sovereign bond markets are distorted in all possible ways:

- The Basel banking regulation framework has been awarding 0% risk-weight to OECD sovereign debt since the 1980s, meaning purchasing such asset does not require any capital. Recent rules haven’t changed anything to this.

- On the contrary, Basel 3 introduces a liquidity ratio (LCR) basically requiring banks to hold even more sovereign debt on their balance sheet (as part of so-called highly-liquid ‘Level 1 assets’).

- Meanwhile, the ECB, as well as the BoE, have been trying to revive business lending (which suffers from the opposite problem: high risk-weights) by launching cheap funding programmes (LTRO, TLTRO, FLS…). Banks drawn on those facilities to invest in… more 0% weighted sovereign debt, and earn capital-free interest income. We call this the ‘carry trade’.

- Furthermore, investors (including banks) have started seeing peripheral European debt as virtually risk-free thanks to the ECB pledge that it would do whatever it takes to prevent defaults in those countries.

There you are: had European regulators wanted to reinforce the link between sovereigns and banks, they wouldn’t have been more successful. Their usual talk of breaking the link between banks and sovereigns has been completely undermined by their own actions.

The easy solution would have been to scrap risk-weights (or at least increase them on sovereign bonds). But this was too simple, so European policymakers decided to go the Chinese way: never scrap a bad rule; design a new one to fix it; and another one to fix the previous one that fixed the original one.

The new 25% cap would only add further distortion: while Basel’s risk-weights do not differentiate between Portuguese and German bonds, the 25% rule doesn’t either. But, you would retort, this isn’t the point: the point is to limit the exposure to any single sovereign. I agree that diversification is usually a good thing. But 1. lack of diversification has been encouraged by policymakers’ own decisions, and 2. forcing banks to diversify away from the safest sovereigns just for the sake of diversifying may well put many banks’ balance sheet more at risk.

Finally, Fitch estimates at EUR1.1Trn the amount of debt that would need to be offloaded. This is very likely to affect markets and could result in banks taking serious one-off hits on their available-for-sale and marked-to-market bond portfolios, resulting in weaker capital positions. This could also raise overall interest rates, in particular in riskier (and weaker) European countries. Fitch believes banks could rebalance into Level 1-elligible covered bonds. Maybe, but this would only introduce even more distortions in the market by artificially raising the demand for their underlying assets, and this would encumber banks’ balance sheets even further, creating other sorts of risks.

Why pick a simple solution when you can do it the Chinese way?

Photo: picture-alliance / dpa through www.dw.de

The Economist on mobile payments and market liquidity

The Economist recently published an article on mobile payment, which is suspicious of its success to say the least:

The fragmentation [of mobile payment systems] confuses merchants and consumers, who have yet to see what is in it for them. From their perspective, the current system works well. Swiping a credit card is not much harder than tapping a phone. Nor is it too risky, especially in America, since credit cards are protected against fraud. Upgrading to a new system is a hassle. Merchants have to install new terminals. Consumers need to store their card details on their phones, but still carry their cards around, since most stores are not yet properly equipped.

I believe the newspaper is too pessimistic. Yes, swapping credit cards is easy. But then it involves signing a bill (not the fastest and most modern system ever) and the card can be replicated. Hence why most of the rest of the developed world has moved to a ‘chip and pin’ form of card payment, which is only slightly more burdensome (and not very fast either). The US is also taking the same direction.

Most people who have recently swapped their ‘chip and pin’ card for a contactless one can witness how convenient and quick the new system is. Yet, they also believed that the previous system “worked well”. Following the same argument, it would have been hard to convince people to switch to cards since carrying cash also “worked well” (ok, it’s not as strong an argument). Switching to smartphone-based contactless payment would make the system as fast, yet reduce the number of cards and devices one carries.

The Economist continues:

But even Apple’s magic may not be enough to make mobile payments fly. It is not clear how merchants will benefit from Apple’s new ecosystem: it does not offer them lower fees for processing payments or useful data about their customers, as CurrentC does. As a result, they may refuse to sign up for Apple Pay or discourage its use.

Yet, as described above, speed is mobile payment’s major asset. Any retailer regularly experiencing long queues is likely to lose customers. Contactless cards already speed up the checkout process considerably. Unfortunately, they are usually capped to pay small amounts (GBP20 in the UK). Contactless mobile payment/NFC systems would remove that cap.

In another article, The Economist once again highlights its ambivalent stance towards regulation:

But the illiquidity problem will still be there when the next crisis occurs. In a sense, it is a problem caused by regulators; they wanted banks to be less exposed to the vicissitudes of markets. But you cannot make risk disappear altogether; you can only shift it to another place. Get ready for more moments of sheer market terror.

The article refers to the recent market turbulence and points to regulatory requirements that have made lack of liquidity a rather new problem:

Due to new regulatory restrictions and capital rules that make bond-trading less profitable, banks have cut back their inventories to the level of 2002, even though the value of bonds outstanding has doubled since then (see chart).

That is a problem when trading surges, as it did between October 10th and 16th, when volumes rose by 67%. “Credit is not a continuously priced market,” says Richard Ryan of M&G Investments, a fund manager. “When a bond price falls from 100 to 90, it won’t do so smoothly, but in big drops.”

This is correct. Market-making (mostly fixed income) is becoming trickier because harsher capital requirements make it more expensive to carry a large inventory of bonds through three channels: 1. deleveraging, as banks are pushed towards higher regulatory capital ratios (and as the new leverage ratio is introduced), 2. credit risk, as credit risk-weights are on upward trend, 3. market risk, as holding larger inventories penalise banks through higher market RWAs than before. I may write a whole post on this topic soon.

But the newspaper forgets liquidity requirements: banks are required to hold enough very liquid assets on their balance sheet (‘liquidity coverage ratio’). Given the combination of leverage and liquidity constraints, banks have to sacrifice other asset classes: the riskier bonds. This leads to the following very good chart, from a Citigroup report and reported by Felix Salmon at Reuters:

This has been an issue with The Economist since the start of the crisis: the same newspaper declares that banks needs to be regulated and safer and complains about the negative effects of regulation at the same time. Perhaps time to be less contradictory?

PS: The ECB published its stress test results yesterday. I won’t comment on them. I just thought the AQR was an interesting exercise, but its consequences must be carefully weighted and it is crucial not to over-interpret them (I’ve already written about the danger of ‘harmonizing’ assessments across multiple jurisdictions and cultures).

ECB policies: from flop to flop… to flop?

Even central bankers seem to be acknowledging that their measures aren’t necessarily effective…

ECB’s Benoit Coeuré made some interesting comments on negative deposit rates in a speech early September. Surprisingly, he and I agree on several points he makes on the mechanics of negative rates (he and I usually have opposite views). Which is odd. Given the very cautious tone of his speech, why is he even supporting ECB policies?

Here is Coeuré:

Will the transmission of lower short-term rates to a lower cost of credit for the real economy be as smooth? While bank lending rates have come down in the past in line with lower policy rates, there is a limit to how cheap bank lending can be. The mark-up that banks add to the cost of obtaining funding from the central bank compensates for credit risk, term premia and the cost of originating, screening and monitoring loans. The need for such compensation does not necessarily fall when policy rates are lowered. If anything, a central bank lowers rates when the economy needs stimulus, which is precisely when it is difficult for banks to find good loan making opportunities. It remains to be seen whether and to what extent the recent monetary policy accommodation translates into cheaper bank lending.

This is a point I’ve made many times when referring to margin compression: banks are limited in their ability to lower the interest rate they charge customers as, absent any other revenue sources, their net interest income necessarily need to cover their operating costs (at least; as in reality it needs to be higher to cover their cost of capital in the long run). Banks’ only solution to lower rates is to charge customers more for complimentary products (it has been reported that this is in effect what has been happening in the US recently).

Negative rates are similar to a tax on excess reserves, which evidently doesn’t make it easier for a bank to improve its profitability, and as a result its internal capital generation. And Coeuré agrees:

A negative deposit rate can, however, also have adverse consequences. For a start, it imposes a cost on banks with excess reserves and could therefore reduce their profitability. Note, however, that this applies to any reduction of the deposit rate and not just to those that make the rate negative. For sure, lower bank profitability could hamper economic recovery, especially in times when banks have to deleverage owning to stricter regulation and enhanced market scrutiny. But whether bank profitability really falls when policy rates are lowered depends more generally on the slope of the yield curve (as banks’ funding costs may also fall), on banks’ investment policies (as there is scope for them to diversify their cash investment both along the curve and across the credit universe) and on factors driving non-interest income.

Coeuré clearly understands the issue: central banks are making it difficult for banks to grow their capital base, while regulators (often the same central bankers) are asking banks to improve their capitalisation as fast as possible. Still, he supports the policy…

Other regulators are aware of the problem, and not all are happy about it… Andrew Bailey, from the Bank of England’s PRA, said last week that regulatory agencies should co-ordinate:

I am trying to build capital in firms, and it is draining out down the other side.

This says it all.

Meanwhile, and as I expected, the ECB’s TLTRO is unlikely to have much effect on the Eurozone economy… Banks only took up EUR83m of TLTRO money, much below what the central bank expected. It is also likely that a large share of this take up will only be used for temporary liquidity purposes, or even for temporary profitability boosting effects (through the carry trade, by purchasing capital requirement-free sovereign debt), until banks have to pay it off after two years (as required by the ECB, and without penalty, if they don’t lend the money to businesses).

Fitch also commented negatively on TLTRO, with an unsurprising title: “TLTROs Unlikely to Kick-Start Lending in Southern Europe”.

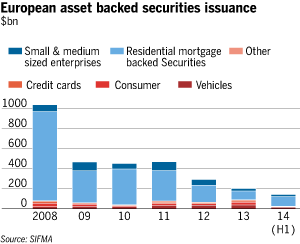

Finally, the ECB also announced its intention to purchase asset-backed securities (which effectively represents a version of QE). While we don’t know the details yet, the scheme has fundamentally a higher probability to have an effect on banks’ behaviour. There is a catch though: ABS issuance volume has been more than subdued in Europe since the crisis struck (see chart below, from the FT). The ECB might struggle to buy the quantity of assets it wishes. Perhaps this is why central bankers started to encourage European banks to issue such structured products, just a few years after blaming banks for using such products.

Oh, actually, there is another catch. ABSs are usually designed in tranches. Equity and mezzanine tranches absorb losses first and are more lowly rated than senior tranches, which usually benefit from a high rating. Consequently, equity and mezzanine tranches are capital intensive (their regulatory risk-weight is higher), whereas senior tranches aren’t. To help banks consolidate their regulatory capital ratios and prevent them from deleveraging, the ECB needs to buy the riskier tranches. But political constraints may prevent it to do so… Will this new ECB scheme also fail? As long as central bankers (and politicians) continue to push for schemes and policies without properly understanding their effects on banks’ internal ‘mechanics’, they will be doomed to fail.

PS: I have been busy recently so few updates. I have a number of posts in the pipeline… I just need to find the time to write them!

New research at last asks the right questions on RWAs

A new piece of research by the US Treasury Department’s Office of Financial Research has started questioning the use and definitions of Basel regulations’ risk-weighted assets (RWAs), which they view as a “rather curious scheme”… RWAs are critical in the Basel framework as they have been underlying regulatory capital ratios since the introduction of Basel 1 back in 1988. Readers of this blog know that I blame RWAs for being a major factor in the economic distortions and resources misallocation that directly led to the crisis (reduction in business lending, jump in real estate lending, securitizations and sovereign lending…) (see also here… and everywhere on this blog).

The authors’ thesis is similar to mine (emphasis added):

This is a rather curious scheme, if we consider that risk is not ordinarily considered additive. One might construe the additive formulation as conservative, but capital requirements affect which assets a bank chooses to hold, so the choice of risk weights affects a bank’s asset mix and not just the overall risk of its portfolio. A risk-weighting scheme may be conservative in its effect on overall risk and yet introduce unintended distortions in the levels of different kinds of lending activities. […]

For our investigation, we take a risk-weighting scheme to have two primary interlinked objectives: to limit the overall risk in a bank portfolio and to do so without an unintended distortion of the mix of assets held by the bank. The first of these objectives is common to all capital regulation, but the second is specific to a risk-weighting scheme because risk weights implicitly assign prices (in terms of additional capital) to asset categories and thus inevitably create incentives for banks to choose some assets over others.

They add that the literature supporting the use (and validating the level) of risk-weights is rather thin, unlike the literature on the nature of banks’ capital (the so-called ‘Tiers’), which has been the focus of most new regulatory measures while RWAs have remained pretty much unchanged.

They propose to tie risk-weights to asset profitability and develop a mathematical framework to help regulators to do so (as they are unlikely to obtain enough information to accurately set their level). This is interesting, but I’d rather get rid of risk-weights altogether: market actors can already assess banks’ profitability vs. asset mix risk and invest accordingly. There is also another issue with such a scheme: assets that do not appear profitable (and hence risky) at first do not necessarily mean they are not, as secured real estate markets demonstrated over the last decade. Moreover, ‘riskier’ business lending rates are currently lower than ‘safer’ mortgage lending ones. Profitability of riskier assets is sometimes subdued, either for relationship purposes (in order to generate revenues elsewhere), and/or if lending terms/collateral nature/haircuts are deemed reasonable. I have to admit that I did not have the time to read their mathematical description in depth and I might be missing something.

Meanwhile, the BoE’s Funding for Lending Scheme still struggles to revive lending to UK businesses. As policy-makers are unlikely to read this blog, perhaps this new research will help?

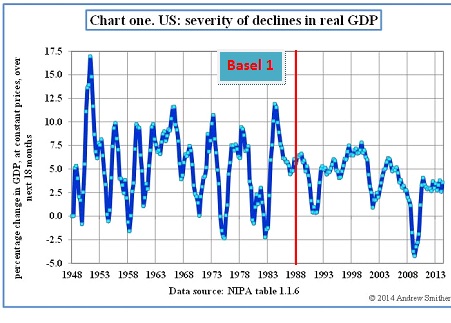

PS: I extracted the following chart from an FT blog post published yesterday and added Basel 1 to it (which introduced risk-weights and led to a decline in business lending). US real GDP growth seems to start declining exactly when business lending falls below trend (compare with second chart):

Secular stagnation: factoring in banking regulation

David Beckworth wrote a good post on the secular stagnation hypothesis, highlighting the problem with the interpretation of the natural rate by secular stagnation theorists. This is Beckworth:

First, real interest rates adjusted for the risk premium have not been in a secular decline. Everyone from Larry Summers to Paul Krugman to Olivier Blanchard ignore this point in the book. They all claim that real interest rates have been trending down for decades. The editors of the book, Coen Teulings and Richard Baldwin, even claim that this development is the ‘prima facie’ evidence for secular stagnation. What they are doing wrong is only subtracting expected inflation from the observed nominal interest rate. They also need to subtract the risk premium to get the natural interest rate, the interest rate at the heart of the story. For it is the natural interest rate that is affected by expected growth of technology and the labor force.

He is right. But I believe there is more to the story.

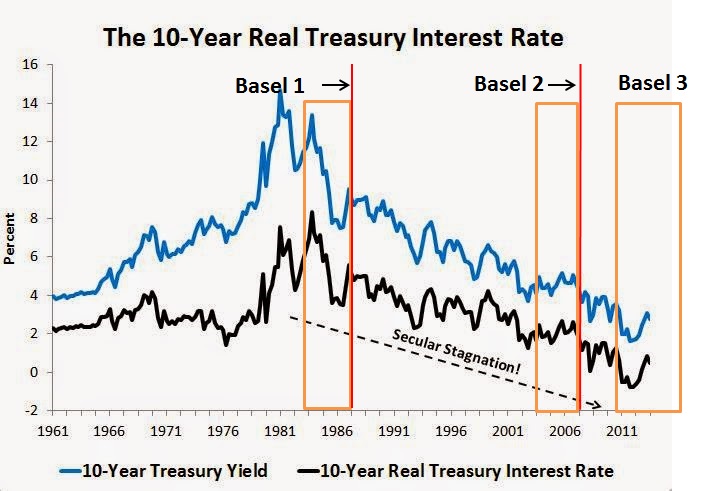

This is Beckworth’s chart highlighting the apparent secular decline in interest rates as believed by secular stagnation adherents. I added to it Basel 1, Basel 2 and Basel 3 introductions (red lines) and discussions (orange area) (unlike in Europe, only a few US banks had implemented Basel 2 when the crisis started):

What is striking is the fact that Treasury yields started declining exactly when Basel 1 was being discussed and implemented. There is a clear reason for this: Basel introduced risk-weighted assets, and government securities were awarded a 0% risk-weight, meaning banks could purchase them and hold no capital against them. As I have described before, banks were then incentivised to pile in such assets to maximise RoE, as a quick risk-adjusted return on capital calculation demonstrates. Basel 1 also introduced risk-weights for other asset classes such as business and mortgage lending. Structural changes in lending* and government securities markets occurred directly post-Basel. I believe this is no coincidence.

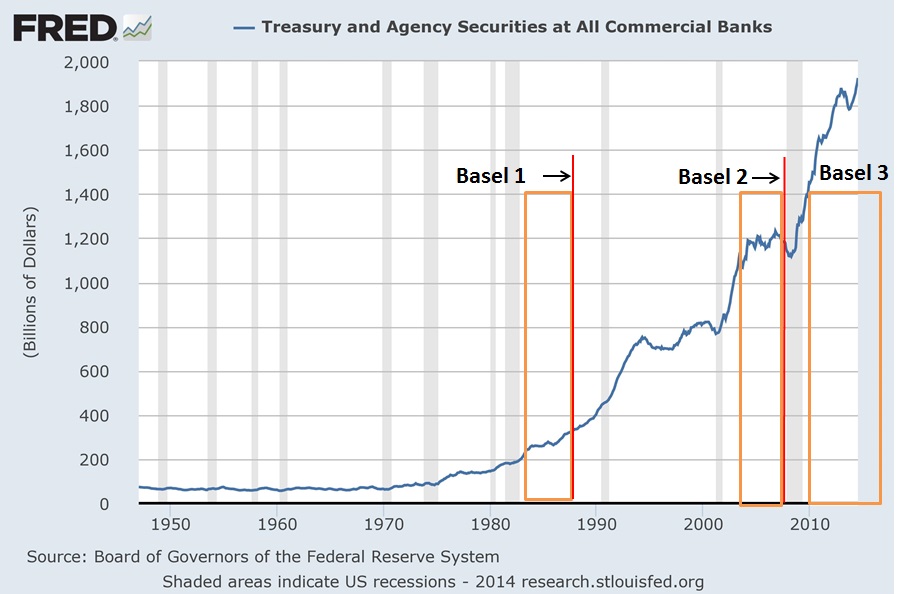

Take a look at the following chart. Until the 1980s, the volume of US government securities on US banks’ balance sheet was pretty much constant. Everything changed from the 1980s onward:

As a share of banks’ total assets (see chart below), US government securities literally spiked after Basel 1 was introduced, only to decline (as a share of total assets) as banks started piling in other assets that benefited from generous capital treatments such as securitisations and insured mortgages (though this doesn’t mean demand faded as banks balance sheets grew quickly over the period, just that demand for other assets was even stronger). Post-crisis, Basel 3 renewed the demand for US sovereign debt as it 1. modified the capital treatment of some previously lowly-weighted assets and 2. introduced minimum liquidity requirements (LCR) as well as margins and collateral requirements that require the use of high-quality liquid assets such as Treasuries.

We identify the same pattern as a share of total securities on US banks’ balance sheet**:

The demand for Treasuries also boomed throughout the financial sector due to those margin/collateral/liquidity requirements that apply (mostly post-Basel 3), not only to commercial banks, but also to broker dealers and investment managers:

All those regulations evidently artificially increase demand for US government-linked securities, pushing their yields down.

But I guess you’re going to tell me that Beckworth’s adjusted risk-free Treasury yield was actually stable over the whole period (chart below). Actually, unlike what Beckworth claims, it does look like there is a slight decline since the end of the 1980s. Moreover, ups and downs almost exactly coincide with banks decreasing/increasing their relative holdings of Treasuries (see above, third chart). Finally, there is also another option: that the natural (risk-free) rate of interest’s trajectory was in fact upward, which would be hidden by financial regulations’ artificially-created demand…

However, this analysis is incomplete: it does not account for foreign banks’ demand for Treasuries, which is also a widely-held asset as part of banks’ liquidity buffers (and in particular when their own sovereign fails…). I unfortunately don’t have access to such data.

In the end, the use of Treasury yield (even adjusted) as an estimate of the natural rate of interest is unreliable given the numerous microeconomic variables that distort its level.

* See this chart from one of my previous posts:

** Post-WW2’s very high figures (close to 100%) reflect the low level of corporate securities issued following the Great Depression and WW2, the high issuance volume of US sovereign debt to fund the war, as well as restrictions on banks’ securities holding to facilitate such wartime issuances.

Recent Comments