The BoE’s FLS delusion

The Bank of England reported yesterday the latest statistics of one of its flagship measures, the Funding for Lending Scheme. Unsurprisingly, they are disappointing. No, more than that actually: the FLS has been pretty much useless.

When launched mid-2012, the FLS was supposed to offer cheap funding to British banks in exchange for increased business and mortgage lending (though originally, authorities strongly emphasised SMEs in their PR as you can imagine) in order to ‘stimulate the economy’. The only effect of the scheme was to boost… mortgage lending.

The BoE, unhappy, decided to refocus the scheme on businesses (including SMEs) only, in November last year. Well, as I predicted, it was evidently a great success: in Q114, net lending to businesses was –GBP2.7bn and net lending to SMEs was –GBP700m. Since the inception of the scheme, business lending has pretty much constantly fallen (see chart below).

According to the FT:

Figures from the British Bankers’ Association showed net lending to companies fell by £2.3bn in April to £275bn, the biggest monthly decline since last July.

The BoE argues that we don’t know what would have happened without the scheme. Perhaps lending would have fallen even more? That’s a poor argument for a scheme that was supposed to boost lending, not merely reduce its fall. Not even all large UK banks participated in the scheme (HSBC and Santander didn’t). Moreover, some banks withdrew only modest amounts because they could already access cheaper financial markets by issuing covered bonds and other secured funding instruments, or, if they couldn’t, used the FLS to pay off existing wholesale funding rather than increase lending… The FLS funding that did end up being used to lend was effective in boosting… the mortgage lending supply.

The UK government has also ‘urged’ banks to extend more credit to SMEs. Still, nothing is happening and nobody seems to understand why. For sure, low demand for credit plays a role as businesses rebuild their balance sheet following the pre-crisis binge. Still, nobody seems to understand the role played by current regulatory measures. Central bankers are supposed to understand the banking system. The fact that they seem so oblivious to such concepts is worrying.

On the one hand, you have politicians, regulators and central bankers trying to push bankers to lend to SMEs, which often represent relatively high credit risk. On the other hand, the same politicians, regulators and central bankers are asking the banks to… derisk their business model and increase their capitalisation. You can’t be more contradictory.

The problem is: regulation reflects the derisking point of view. Basel rules require banks to increase their capital buffer relatively to the riskiness of their loan book; riskiness measures (= risk-weighted assets) which are also derived from criteria defined by Basel (and ‘validated’ by local regulators when banks are on an IRB basis, i.e. use their own internal models).

Those criteria require banks to hold much more capital against SME exposures than against mortgage ones. Banks that focus on SMEs end up squeezed: risk-adjusted SME lending return is not enough to generate the RoE that covers the cost of capital on a thicker equity base. Banks’ best option is to reduce interest income but reduce proportionally more their capital base to generate higher RoEs. Apart from lending to sovereigns and sovereign-linked entities, the main way they can currently do that is to lend… secured on retail properties…

(I have already described here how this process creates misallocation of capital and possibly business cycles)

As such, it is unsurprising that mortgage lending never turned negative in the UK (even a single month) throughout the crisis. Even credit card exposures haven’t been cut by banks, as their risk-adjusted returns were more beneficial for their RoE than SMEs’. Furthermore, alternative lenders, who are not subject to those capital requirements, actually see demand for credit by SMEs increase (see also here).

Let’s get back to the 29th of November 2013. At that time, after it was announced that the FLS would be modified, I declared:

RWAs are still in place! Mortgage and household lending will still attract most of lending volume as it is more profitable from a capital point of view.

Well…

As long as those Basel rules, which have been at the root of most real estate cycles around the world since the 1980s, aren’t changed, SMEs are in for a hard time. And economic growth too in turn. Secular stagnation they said?

PS: this topic could easily be linked to my previous one on intragroup funding and regulators “killing banking for nothing”. Speaking of the ‘death of banking’, Izabella Kaminska managed to launch a new series on this very subject without ever saying a word about regulation, which is the single largest driver behind financial innovations and reshaped business models. I sincerely applaud the feat.

PPS: The FT reported how far regulators (here the FCA) are willing to go to reshape banking according to their ideal: equity research in the UK is in for a pretty hard time. This is silly. Let investors decide which researchers they wish to remunerate. Oversight of the financial sector is transforming into paternalism, if not outright regulatory threats and uncertainty.

PPS: I wish to thank Lars Christensen who mentioned my blog yesterday and had some very nice comments about it.

News digest: Scotland, CoCos and electronic trading

Sam Bowman had a very good piece on the Adam Smith Institute blog about Scotland setting up a pound Sterling-based free banking system unilaterally (yeah I know I keep mentioning this blog now, but activity there seems to have been picking up recently). It draws on George Selgin’s post and is a very good read. One particular point was more than very interesting in the context of my own blog (emphasis added):

George Selgin has pointed to research by the Federal Reserve Bank of Atlanta about the Latin American countries that unilaterally use the dollar. Because these countries – Panama, Ecuador and El Salvador – lack a Lender of Last Resort, their banking systems have had to be far more prudent and cautious than most of their neighbours.

Panama, which has used the US Dollar for one hundred years, is the most useful example because it is a relatively rich and stable country. A recent IMF report said that:

“By not having a central bank, Panama lacks both a traditional lender of last resort and a mechanism to mitigate systemic liquidity shortages. The authorities emphasized that these features had contributed to the strength and resilience of the system, which relies on banks holding high levels of liquidity beyond the prudential requirement of 30 percent of short-term deposits.”

Panama also lacks any bank reserve requirement rules or deposit insurance. Despite or, more likely, because of these factors, the World Economic Forum’s Global Competitiveness Report ranks Panama seventh in the world for the soundness of its banks.

I don’t think I have anything to add…

SNL reported yesterday that Germany’s laws seem to make the issuance of contingent convertible bonds (CoCos) almost pointless. This is a vivid reminder of my previous post, which highlighted some of the ‘good’ principles of financial regulation and which advocated stable, simple and clear rules, a position I have had since I’ve opened this blog. All authorities and regulators try to push banks (including German banks) to boost their capital level, which are deemed too low by international standards. CoCos, which are bonds that convert into equity if the bank’s regulatory capital ratio gets below a certain threshold, are a useful tool for banks (as it allows them to prevent shareholder dilution by issuing equity) and investors (whose demand is strong as those bonds pay higher coupon rates). Yet lawmakers, who love to bash banks for their low level of capitalisation, seem to be in no hurry to provide a clear framework that would allow to partially solve the very problems they point at in the first place… This is a very obvious example of regime uncertainty. As one lawyer declared:

One thing is clear: Nothing is clear

Bloomberg reports that FX traders are facing ‘extinction’ due to the switch to electronic trading. In fact, this has been ongoing for now several years, with asset classes moving one after another towards electronic platforms. Electronic trading now represents 66% of all FX transactions (vs. 20% in 2001). Traditional traders are going to become increasingly scarce and replaced by IT specialists that set and programme those machines. Overall, this should also mean less staff and a lower cost base for banks that are still plagued by too high cost/income ratios. Part of this shift is due to regulation, which makes it even more expensive to trade some of those products. This only reinforces my belief that regulation is historically one of the primary drivers of financial innovation, from money market funds to P2P lending…

Bundesbank’s Dombret has strange free market principles

Andreas Dombret, member of the executive board of the Bundesbank, made two very similar speeches last week (The State as a Banker? and Striving to achieve stability – regulations and markets in the light of the crisis). When I started to read them, I was delighted. Take a look:

If one were to ask the question whether or not the market economy merits our trust, another question has to be added immediately: “Does the state merit our trust?”

[…]

Sometimes it seems as if we are witnessing a transformation of values and a redefinition of fundamental concepts. The close connection between risk-taking and liability, which is an important element of a market economy, has weakened.

Conservative and risk-averse business models have become somewhat old-fashioned. If the state is bearing a significant part of the losses in the case of a default of a bank, banks are encouraged to take on more risks.

[…]

[High bonuses and short-termism] are the result of violated market principles and blurred lines between the state and the banks. They are not the result of a well-designed market economy but rather indicative of deformed economies. However, the market economy stands accused of these faults.

Brilliant. I was just about to become a Dombret fan when…I read the rest:

In my view, the solution is to be found in returning the state to its role of providing a framework in which the private sector can operate. This means a return to the role the founding fathers of the social market economy had in mind.

They knew that good banking regulation is a key element of a well-designed framework for a well-functioning banking industry and a proper market economy in general.

[…]

This is where good bank capitalisation comes into play. It is the other side of the coin. Good regulation should directly address the key problem. If the system is too fragile, an important and direct measure to reduce fragility is to have enough capital.

[…]

Good capitalisation will have the positive side effect of reducing many of the wrong incentives and distortions created by taxpayers’ implicit guarantees and therefore making the bail-in threat more credible ex ante.

And from the second article:

In view of all this, I believe that two elements will be especially important in making banks more stable: capital and liquidity. Deficits in both of these things were factors which contributed significantly to the financial crisis. The state can bring in regulation to address these deficits, and has done so very successfully.

And on shadow banking:

In terms of financial stability, the crux of the matter is that these entities can cause similar risks to banks but are not subject to bank regulation.And the shadow banking system can certainly generate systemic risks which pose a threat to the entire financial system.

Much the same applies to insurance companies. Although they aren’t a direct component of the shadow banking system, they can also be a source of systemic risk. All of this makes it appropriate to extend the reach of regulation.

Sorry but I will postpone joining the fan club…

Mr. Dombret correctly identifies the issue with the financial system: too much state involvement. What is his solution? More state involvement. It is hard to believe that one person could come up with the exact same solution that had not worked in the past. Were the banks not already subject to capital requirements before the crisis? Even if not ‘high’ enough they were still higher than no capital requirement at all. So in theory they should have at least mitigated the crisis. But the crisis was the worst one since 1929, and much worse than previous ones during which there were no capital requirements. Efficient regulation indeed…

Like 95% of regulators, he makes such mistakes because of his (voluntary?) ignorance of banking history. A quick look at a few books or papers such as this one, comparing US and Canadian banking systems historically, would have shown him that Canadian banks were more leveraged than US banks on average since the early 19th century, yet experienced a lot fewer bank failures. There is clearly so much more at play than capital buffers in banking crises…

Moreover, he views formerly ‘low’ capital requirements as a justification for bankers to take on more risks to generate high return on equity. This doesn’t make sense. For one thing, the higher the capital requirements the higher the risks that need to be taken on to generate the same RoE. It also encourages gaming the rules. This is what is currently happening, as banks are magically managing to reduce their risk-weighted assets so that their regulatory-defined capital ratios look healthier without having to increase their capital.

Mr. Dombret starts by seriously questioning the state’s ability to manage the system and highlights the very harmful and distortive effects of state regulation to eventually… back further and deeper state regulation.

A question Mr. Dombret: what are we going to do following the next crisis? Continue down the same road?

Can please someone remind Mr. Dombret of what a free market economy, which he seems to cherish, means?

Picture: Marius Becker

Risk-weighted assets and capital manipulations

As some of you might have noticed, the Bank of International Settlements published yesterday the final version of the Basel III leverage ratio (official report can be found here). This ratio is a measure of the capitalisation of a bank for regulatory purposes. I have already mentioned a few times those capital ratios. Since the first Basel regulations were introduced, capital ratios were based on risk-weighted assets (RWAs). Some of you might already be aware of my ‘love’ of RWAs… The leverage ratio, on the other hand, gets rid of RWAs.

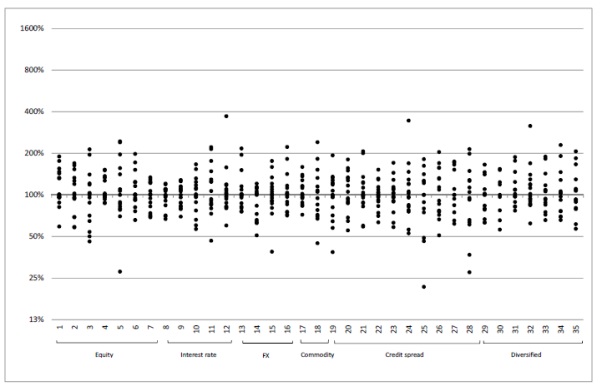

I am not going to speak about the leverage ratio here. But about other two other related BIS studies that, in a way, legitimate the use of unweighted capital ratios. In January 2013, the BIS published a first analysis of market RWAs. They tried to estimate the variability of risk-weights associated to equivalent securities across banks. The BIS provided 26 portfolios of financial securities to 16 different banks and asked them to risk-weigh them according to their internal models. The results were shocking (but not surprising).

Banks mostly assess market risks using statistical Value-at-Risk models. The graph below shows the dispersion of the results provided by the banks’ VaR models. The results are normalised so that the median result is centred on 100%.

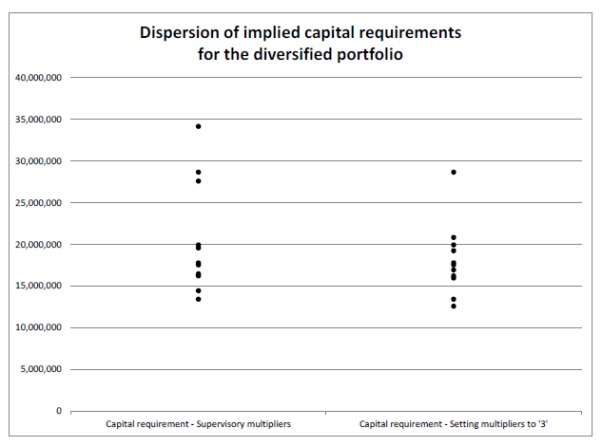

The dispersion is huge. Some banks judged portfolio 14 as being around 1000% riskier than the median bank’s perception of it (and I am not even talking about the most conservative one). Some comfort could be taken from the diversified portfolios (25 and 26), which are closer to real life portfolios. Nonetheless, even in those, variations are large enough to undermine the credibility of the risk-weights applied to them. The chart below demonstrates the capital requirements (in Euros) implied from the VaR results above for portfolio 25. Some banks would put aside more than twice the amount of capital than others would, for the same portfolio of securities.

The BIS believed at that time that different local regulatory requirements were partially responsible for the results (such as some banks following Basel 2.5 and others Basel 2. I’m going to skip the details but Basel 2.5 pushes market RWAs up).

The BIS eventually published its final study on market RWA at the end of December. This time, all banks had implemented Basel 2.5. So most of the observed variation could only come from the banks’ internal model differences. What did they find?

Not much difference. Variations were still huge. The resulting implied capital requirements (in thousands of Euros) for portfolios 29 and 30 were as follows:

Clearly, RWAs are unreliable. This questions the very utility of RWA-based regulatory capital ratios. How can one actually trust two different banks both reporting 10% Tier 1 ratios? One of them might in reality hold twice as little capital as the other one for what is actually the same risk level. Banks can easily game the system. Moreover, the FT was reporting yesterday that some banks were starting to report RoRWA (return on RWAs) instead of more traditional return on equity or return on assets. But those measures suffer from the exact same defects. While an unweighted leverage ratio is clearly not perfect, RWAs introduce far too much information distortion and even potentially exacerbate the business cycle. Time to get rid of them.

News digest (Libor 1.7bn fine, banks’ poor IT systems, banking, telco, IT, retailing convergence…)

Again this week, so many things happening that I can’t spend much time commenting on each and I have to make choices!

George Osborne, UK’s Chancellor of the Exchequer, is about to announce a tax-free treatment for P2P lending, which could be included in individual Isa accounts. This is a good thing. Nothing much more to say…

The Bank of England is thinking of asking UK-based banks to provide regulatory capital ratios calculated using standard risk-weights as defined by Basel’s Standardised method. These ratios would not replace those banks’ main capital ratios as currently calculated (under the IRB method) but would ‘complement’ them. It’s a good idea and we may well end up having a few surprises…

The EU has fined some of the large global banks as part of the Libor rate-rigging. Banks will have to pay EUR1.7bn. This isn’t that significant given what JPMorgan has paid so far in fines in the US… I stopped counting and I may well be wrong but I think they paid around USD$15bn so far this year. Surely this should make me doubt about the ability of laissez-faire to regulate banks? Not really. First, we are not in a laissez-faire environment. Second, laissez-faire does not mean laissez-faire fraudulent activities. It means laissez-faire people to negotiate their own contracts and agreements. When those contracts are not respected, when there is fraud, punishment should ensue. Laissez-faire is completely in favour of the rule of law. Moreover in a real free-market environment, it is likely that most fraudulent banks would already be out of business…

Something I know from experience: many banks have really poor IT systems and poorly-designed databases. This week, Royal Bank of Scotland’s customers could not access their accounts anymore for a whole day (and pretty busy shopping day on top of that). Its CEO acknowledged that the bank will have to invest… GBP1bn in its IT systems. That’s a massive bill. It shows how outdated its IT systems must have been. It is scary to see that some banks (nop, no name), whether small, medium-sized or massively massive have such poorly-designed systems that they cannot adequately track simple data such as their exposures and the level of provisioning against them by industrial sector or geographical area for example. This is the result of years, if not decades, of underinvestment in IT. This is also why start-up banks are usually much more efficient: they have top-notch IT. For large banks, no surprise, trading systems have been upgraded at a much faster pace than commercial and retail banking ones. Banks are currently plagued by their high cost base. But more efficient IT systems would have helped maintain their costs lower while improving internal productivity.

Moreover, banks are also under threat from new financial actors, and possibly future data-heavy entrants such as Google and Amazon. Those firms have great IT systems: it is their core business. What if they entered the banking business? It’s what Spain’s BBVA’s CEO asked in the FT this week. Indeed, banks are now closing branches one by one as customers move online or mobile. It also means that new entrants possibly wouldn’t need any branch network altogether and could offer more efficient services to customers, using their huge data centres and cloud computing capabilities. A quick visit to the annual Barcamp Bank ‘unconference’ shows how many people are currently working on new customer-friendly and efficient banking API and other systems. We’ve already seen the ‘convergence’ of IT, telecoms and media. Are we about to witness a banking, IT, telecom, retailing, online search and payment convergence?

Are synthetic CDOs making a comeback? Well, issuance volume is still pretty low… Unless low interest rates start over-boosting this market too?

Finally, Columbia University’s Charles Calomiris has his own take on Admati and Hellwig’s recommendations and rejects some of their claims (such as the fact that higher equity levels would not impair lending, a claim that I have already made here, although my reasoning was different). He also favours rising banks’ equity requirements though.

Banks’ RWAs as a source of malinvestments – A graphical experiment

Today is going to be experimental and theoretical. I have already outlined the principles behind the RWA-based variation of the Austrian Business Cycle Theory (ABCT), which was followed by a quick clarification. I am now attempting to come up with a graphical representation to illustrate its mechanism. In order to do that, I am going to use Roger Garrison’s capital structure-based macroeconomics representations used in his book Time and Money: The Macroeconomics of Capital Structure. I am not saying that what I am about to describe is 100% right. Remember that this remains an experiment that I just wrote down over those last few days and that needs a lot more development. There may well also be other ways of depicting the impacts that Basel regulation’s RWAs have on the capital structure and malinvestments. Completely different analytical frameworks might also do. Comments and suggestions are welcome.

This is what Garrison’s representation of the macroeconomics of capital structure looks like:

It is composed of three elements:

- Bottom right: this is the traditional market for loanable funds, where the supply and demand for loanable funds cross at the natural rate of interest. It represents economic agents’ intertemporal preferences: the higher they value future goods over present goods, the more they save and the lower the interest rate. The x-axis represents the quantity of savings supplied (and investments) and the y-axis represents the interest rate.

- Top right: this is the production-possibility frontier (PPF). In Garrison’s chart, it represents the sustainable trade-off between consumption and gross investment. Only movements along the frontier are sustainable and supposed to reflect economic agents’ preferences. Positive net investments and technological shocks expand the frontier as the economy becomes more productive.

- Top left: this is the Hayekian triangle. It represents the various stages of production (each adding to output) within an industry. See details below:

I don’t have time to come back to the original ABCT and those willing to find out more about it can find plenty of examples online. Today I wish only to try to understand the impact of regulatory-defined risk-weighted assets on this structure. Ironically, it becomes necessary to disaggregate the Austrian capital-based framework to understand the mechanics and distortions leading to a likely banking crisis. In everything that follows, and unlike in the original Austrian theory, we exclude central banks from the picture (i.e. no monetary injection). We instead focus only on monetary redistribution. The story outlined below does not explain the financial crisis by itself. Rather, it outlines a regulatory mechanism that exacerbated the crisis.

I don’t have time to come back to the original ABCT and those willing to find out more about it can find plenty of examples online. Today I wish only to try to understand the impact of regulatory-defined risk-weighted assets on this structure. Ironically, it becomes necessary to disaggregate the Austrian capital-based framework to understand the mechanics and distortions leading to a likely banking crisis. In everything that follows, and unlike in the original Austrian theory, we exclude central banks from the picture (i.e. no monetary injection). We instead focus only on monetary redistribution. The story outlined below does not explain the financial crisis by itself. Rather, it outlines a regulatory mechanism that exacerbated the crisis.

Let’s take a simple example that I have already used earlier. Only two types of lending exist: SME lending and mortgage/real estate lending. Basel regulations force banks to use more capital when lending to SME and as a result, bankers are incentivised to maximise ROE through artificially increasing mortgage lending and artificially restricting SME lending, as described in my first post on the topic.

In equilibrium and in a completely free-market world with no positive net investment, the economy looks like Garrison’s chart above. However, bankers don’t charge the Wicksellian natural rate of interest to all customers: they add a risk premium to the natural rate (effectively a ‘risk-free’ rate) to reflect the risk inherent to each asset class and customer. Those various rates of interest do reflect an equilibrium (‘natural’) state, which factors in the free markets’ perception of risk. Because lending to SME is riskier than mortgage lending, we end up with:

natural (risk free) rate < mortgage rate (natural rate + mortgage risk premium) < SME rate (natural rate + SME risk premium)

What RWAs do is to impose a certain perception of risk for accounting purposes, distorting the normal channelling of loanable funds and therefore each asset class’ respective ‘natural’ rate of interest. Unfortunately, depicting all demand and supply curves, their respective interest rates and the changes when Basel-defined RWAs are applied would be extremely messy in a single chart. We’re going to illustrate each asset class separately with their respective demand and supply curve. Let’s start with mortgage (real estate) lending:

Given the incentives they have to channel lending towards capital-optimising asset classes, bankers artificially increase the supply of loanable funds to all real estate activities, pushing the rate of interest below the natural rate of the sector. As the actual total supply of loanable funds does not change, returns on savings remain the same. In our PPF, this pushes resources towards real estate. Any other industry would interpret the lowered rate of interest as a shift in people’s intertemporal preferences towards the future and increase long-term investments at the expense of short-term production. Indeed, long-term housing projects are started. This is represented by the thin dotted red triangle.

Given the incentives they have to channel lending towards capital-optimising asset classes, bankers artificially increase the supply of loanable funds to all real estate activities, pushing the rate of interest below the natural rate of the sector. As the actual total supply of loanable funds does not change, returns on savings remain the same. In our PPF, this pushes resources towards real estate. Any other industry would interpret the lowered rate of interest as a shift in people’s intertemporal preferences towards the future and increase long-term investments at the expense of short-term production. Indeed, long-term housing projects are started. This is represented by the thin dotted red triangle.

However, the short-term housing supply is inelastic and cannot be reduced. The resulting real estate structure of production is the plain red triangle. Nonetheless, real estate developers have been tricked by the reduced interest rate and the long-term housing projects they started do not match economic agents’ future demand. Meanwhile, savers, adequately rewarded for their savings, do not draw down on them (or don’t have to), but are instead incentivised to leverage as they (indirectly) see profit opportunities from the differential between the natural and the artificially reduced rate. Leverage effectively becomes a function of the interest rate differential:

The increased leverage boosts the demand for existing real estate, bidding up prices, starting a self-reinforcing trend based on expected further price increases. We end up in a temporary situation of both short-term ‘overconsumption’ of real estate and its associated goods, and long-term overinvestments (malinvestments). This situation is depicted by the thick dotted red triangle and represents an unsustainable state beyond the PPF.

On the other hand, bankers artificially restrict the supply of loanable funds to SME, pushing the rate of interest above the natural rate. Tricked by a higher rate of interest, SMEs are led to believe that consumers now value more highly present goods over future goods (as they ‘apparently’ now save less of their income). They temporarily reduce interest rate-sensitive long-term investments to increase the production of late stages consumer goods. This results in an overproduction of consumer goods relative to economic agents’ underlying present demand. Nonetheless, wealth effects from the real estate boom temporarily boost consumption, maintaining prices level. Overconsumption of present goods could also eventually appear if and when savers start leveraging their consumption through low-rate mortgages, as house prices seem to keep increasing. In the long-run, SMEs’ investments aren’t sufficient to satisfy economic agents’ future demand of consumer goods.

With leverage increasing and the economy producing beyond its PPF, the situation is unsustainable. As increasingly more people pile in real estate, demand for real estate loanable funds increases, pushing up the interest rate of the sector. Interest payments – which had taken an increasingly large share of disposable income in line with growing leverage – rise, putting pressure on households’ finances. The economy reaches a Minsky moment and real estate prices start coming down. Real estate developers, who had launched long-term housing projects tricked by the low rates, find out that these are malinvestments that either cannot find buyers or are lacking the financial resources to be completed. Bankruptcies increase among over-leveraged households and companies. Banks start experiencing losses, contract lending and money supply as a result, whereas savers’ demand for money increases. The economy is in monetary disequilibrium. Welcome to the financial crisis designed in the Swiss city of Basel.

This all remains very theoretical and I’ll try to dig up some empirical evidences in another post. Nonetheless, the story seems to match relatively well what happened in some countries during the crisis. Soon after Basel regulations were implemented, household leverage in Spain or Ireland took off and came along with increasing house prices and retail sales, which both collapsed once the crisis struck. Under this framework, the artificially restricted supply of loanable funds to SME and the consequent reduction in long-term investments could also partly explain the rich world manufacturing problems. However, I presented a very simple template. As I mentioned in a previous post, securitisation and other banking regulations (liquidity…) blur the whole picture, and central banks can remain the primary channel through which interest rates are distorted.

RWA-based ABCT Series:

- Banks’ risk-weighted assets as a source of malinvestments, booms and busts

- Banks’ RWAs as a source of malinvestments – Update

- Banks’ RWAs as a source of malinvestments – A graphical experiment

- Banks’ RWAs as a source of malinvestments – Some recent empirical evidence

- A new regulatory-driven housing bubble?

Banks’ RWAs as a source of malinvestments – Update

Following a couple of comments I received on my RWA-based Austrian business cycle theory (ABCT) post, I’d like to clarify a few points:

- In the original ABCT, one cannot figure out where malinvestments will appear following an increase in the money supply not matched by an increase in the demand for money, apart from the fact that they are likely to be in producer goods industries rather than in consumer goods industries, due to the artificial lengthening of the structure of production. The mechanism involved is the Cantillon effect: the first firms to receive the new money will see their purchasing/investing power increase at the expense of the rest. We cannot really foresee where the new spending/investments will be directed though but what is certain is that the original structure of relative prices between goods in the economy will be modified as a result.

- In the RWA-based theory the Cantillon effect is ‘limited’: new funds are effectively channelled towards a few specific sectors that benefit from regulatory advantages (lower capital requirements for banks). It is thus possible to foresee which sectors could boom first and where some of the malinvestments could emerge. This does not mean that all malinvestments will show up in those sectors. Other related sectors could also boom as a result. And the increasing wealth effects of the people concerned could also reflect on unrelated sectors…

- Securitisation also makes it a lot more difficult to follow the channelling effect: asset-backed securities were lowly weighted under Basel 2 (under both Standardised and IRB methods) if they obtained a good credit rating. As a result, some corporate lending got a boost from the measure and this would typically replicate the exact process of the original ABCT. Risk-weights were tightened under latest Basel rules though.

- In the RWA-based ABCT, there is no increase in the money supply as assumption. Interest rates are lowered for some sectors (increasing related prices) and raised for others (depressing related prices) as a result of funding rebalancing through banks’ optimisation of capital. Consequences could be less catastrophic than an actual increase in money supply though (although I have no evidence of that). But there is always increase in the money supply at the same time anyway! 🙂

Today in an SNL article (membership required), I found out that the UK government is becoming increasingly frustrated about the lack of SME lending in the country. Hold your breath:

After years of frustration in its attempts to induce banks to extend more credit to small and medium-sized enterprises, the U.K. government has reached the perhaps surprising conclusion that bankers may simply lack the skills they need to lend.

RWAs? Capital requirements guys? No? It must be the skills! To be so clueless is both sad and hilarious.

RWA-based ABCT Series:

- Banks’ risk-weighted assets as a source of malinvestments, booms and busts

- Banks’ RWAs as a source of malinvestments – Update

- Banks’ RWAs as a source of malinvestments – A graphical experiment

- Banks’ RWAs as a source of malinvestments – Some recent empirical evidence

- A new regulatory-driven housing bubble?

Banks’ risk-weighted assets as a source of malinvestments, booms and busts

Here I’m going to argue that Basel-defined risk-weighted assets, a key component of banking regulation, may be partly responsible for recent business cycles.

Readers might have already noticed my aversion to risk-weighted assets (RWAs), which I view as abominations for various reasons. They are defined by Basel accords and used in regulatory capital ratios. Basel I (published in 1988 and enforced from 1992) had fixed weights by asset class. For example, corporate loans and mortgages would be weighted respectively 100% and 50%, whereas OECD sovereign debt would be weighted 0%. If a bank had USD100bn of total assets, applying risk-weights could, depending on the lending mix of the bank, lead to total RWAs of anything between USD20bn to USD90bn. Regulators would then take the capital of the bank as defined by Basel (‘Tier 1’ capital, total capital…) and calculate the regulatory capital ratio of the bank: Tier 1 capital/RWAs. Basel regulation required this ratio to be above 4%.

Basel II (published in 2004 and progressively implemented afterwards) introduced some flexibility: the ‘Standardised method’ was similar to Basel I’s fixed weights with more granularity (due to the reliance on external credit ratings), while the various ‘Internal Ratings Based’ methods allowed banks to calculate their own risk-weight based on their internal risk management models (‘certified’ by regulators…).

This system is perverse. Banks are profit-maximising institutions that answer to their shareholders. Shareholders on the other hand have a minimal threshold under which they would not invest in a company: the cost of capital, or required return on capital. As a result, return on equity (ROE) has to at least cover the cost of capital. If it doesn’t, economic losses ensue and investors would have been better off investing in lower yielding but lower risk assets in the first place. But Basel accords basically dictate banks how much capital they need to hold. Therefore banks have an incentive in trying to ‘manage’ capital in order to boost ROE. Under Basel, this means pilling in some particular asset classes.

Let’s make very rough calculations to illustrate the point under a Basel II Standardised approach: a pure commercial bank (i.e. no trading activity) has a choice between lending to SMEs (option 1) or to individuals purchasing homes (option 2). The bank has EUR1bn in Tier 1 capital available and wishes to maximise returns while keeping to the minimum of 4% Tier 1 ratio. We also assume that external funding (deposits, wholesale…) is available and that the marginal increase in interest expense is always lower than the marginal increase in interest income.

- Option 1: Given the 100% risk-weight on SME lending, the bank could lend EUR25bn (25bn x 100% x 4% = 1bn), at an interest rate of 7% (say), equalling EUR1.75bn in interest income.

- Option 2: Mortgage lending, at a 35% risk-weight, allows the same bank to lend a total of EUR71.4bn (71.4bn x 35% x 4% = 1bn) for EUR1bn in capital, at an interest rate of 3% (say), equalling EUR2.14bn in interest income.

The bank is clearly incentivised to invest its funding base in mortgages to maximise returns. In practice, large banks that are under the IRB method can push mortgage risk-weights to as low as barely above 10%, and corporate risk-weights to below 50%. As a result, banks are involuntarily pushed by regulators to game RWAs. The lower RWAs, the lower capital the bank needs, the higher its ROE and the happier the regulators. Banks call this ‘capital optimisation’.

Consequently, does it come as a surprise that low-risk weighted asset classes were exactly the ones experiencing bubbles in pre-crisis years? Oh sorry, you don’t know which asset classes were lowly rated… Here they are: real estate, securitisation, OECD sovereign debt. Yep, that’s right. Regulatory incentives that create crises. And the new Basel III regime does pretty much nothing to change the incentivised economic distortions introduced by its predecessors.

Yesterday, Fitch, the rating agency, published a study of lending and RWAs among Europe’s largest banks (press release is available here, full report here but requires free subscription). And, what a surprise, corporate lending is going…down, while mortgage lending and credit exposures to sovereigns are going…up (see charts below). The trend is even exacerbated as banks are under pressure from regulators to boost regulatory capitalisation and from shareholders to improve ROE. And this study only covers IRB banks. My guess is that the situation is even more extreme for Standardised method banks that cannot lower their RWAs.

The ‘funny’ thing is: not a single regulator or central banker seems to get it. As a result, we keep seeing ill-founded central banks schemes aiming at giving SME lending a boost, like the Funding for Lending Scheme launched by the Bank of England in 2012, which provided banks with cheap funding. Yes, you guessed it: SME lending continued its downward trend and the scheme provided mortgage lending a boost.

Should the situation ‘only’ prevent corporates to borrow funds, bad economic consequences would follow but remain limited. Economic growth would suffer but no particular crisis would ensue. The problem is: Basel and RWAs force a massive misallocation of capital towards a few asset classes, resulting in bubbles and large economic crises when the crash occurs.

The Mises and Hayek Austrian business cycle theory emphasises the distortion in the structure of relative prices that emanates from central banks lowering the nominal interest rate below the natural rate of interest as represented by economic agents’ intertemporal preferences, resulting in monetary disequilibrium (excess supply of money). The consequent increase in money supply flows in the economy through one (or a few) entry points, increasing the demand in those sectors, pushing up their prices and artificially (and unsustainably) increasing their return on investment.

I argue here that due to Basel’s RWAs distortions, central banks could even be excluded from the picture altogether: banks are naturally incentivised to channel funds towards particular sectors at the expense of others. Correspondingly, the supply of loanable funds increases above equilibrium in the favoured sectors (hence lowering the nominal interest rate and bringing about an unsustainable boom) but reduces in the disfavoured ones. There can be no aggregate overinvestment during the process, but bad investments (i.e. malinvestments) are undertaken: the investment mix changes as a result of an incentivised flow of lending, rather than as a result of economic agents’ present and future demand. Eventually, the mismatch between expected demand and actual demand appears, malinvestments are revealed, losses materialise and the economy crashes. Central banks inflation worsen the process through the mechanism described by the Austrians.

I am not sure that regulators had in mind a process to facilitate boom and bust cycles when they designed Basel rules. The result is quite ‘ironic’ though: regulations developed to enhance the stability of the financial sector end up being one of the very sources of its instability.

RWA-based ABCT Series:

- Banks’ risk-weighted assets as a source of malinvestments, booms and busts

- Banks’ RWAs as a source of malinvestments – Update

- Banks’ RWAs as a source of malinvestments – A graphical experiment

- Banks’ RWAs as a source of malinvestments – Some recent empirical evidence

- A new regulatory-driven housing bubble?

Co-operative Bank’s new ownership ‘tragedy’ is rather a good thing

For those of you who don’t live in the UK, the Co-operative Bank has been struggling with a large GBP1.5bn capital shortfall (vs. a capital base of GBP1.6bn) since early summer due to losses on its loan book (most of them emanating from the takeover of Britannia Building Society in 2009, a struggling mutual mortgage bank). Moody’s, the rating agency, even downgraded it by six notches all of a sudden. The Co-operative Bank was a subsidiary of the Co-operative Group, a mutual company that owns multiple businesses.

I said ‘was’ because…it won’t be anymore. And it’s apparently causing some headaches.

Mutual companies are owned by their members (who are some of their customers), and not by external shareholders. This was the case of both Britannia’s and Co-op’s equity capital (indirectly through the Co-op Group). However, due to their very nature, mutuals’ ability to raise capital is limited. Consequently, they raise complementary capital from external investors in order to grow. In the case of Co-op, its equity capital was complemented by some sort of hybrid capital: GBP60m of preference shares owned by retail investors and around GBP1.1bn of subordinated debt, which happened to be partly held by…hedge funds. Both counted towards the total regulatory capital ratio of the bank, as defined by Basel accords. Ranking of the capital structure in case of bankruptcy of the bank was as follows: after depositors and other senior creditors, subordinated creditors had the second claims on the liquidated assets of the bank, followed by preference shares-holders and members.

Following several months of negotiations that saw creditors threatening to block a deal under which they would take a loss on their investments, a deal was finally reached a few days ago: a conversion of their bonds into new equity. As a result, 70% of the capital of the bank will be owned by institutional investors, among which several hedge funds (representing around 30/40%). The Co-op Group (and hence members) will retain a 30% stake in the bank. It obviously sounds quite ironic to see a mutual company owned by vulture capitalists… It also looks quite ironic to see the failure of the now all-powerful UK regulators: they never spotted the problems at Co-op Bank, all their proposed solutions collapsed once after the other, and the agreed deal was reached in a perfect free-market type agreement without their intervention…

Many people around me and in the media have raised concerns that the new hedge funds ownership was a bad thing due to the short-term view of their investment strategy. Those fears are misplaced. Hedge funds and private equity firms indeed invest for the short-term. As far as I’m aware, there aren’t many studies analysing the impacts of hedge funds on the performance of the firms in which they own a stake. This recent one found that activist hedge funds actually improved future performances! There are many more studies on the long-term effects of short-term private equity investments. It was actually the topic of my Masters’ research dissertation. The academic research was clear: private equity-owned firms suffered over the short-term through tough restructuring processes (involving job losses and pressure on salaries), but over the longer-term performed better than their peers and actually even hired more people…

Is this surprising? No. We really need to keep emotions aside and think about the underlying reasons for all this. What is the hedge fund’s goal? To maximise profits. What is the time frame? Usually quite short-term (= a few years). How can the fund exit the investment? By selling the company to external investors. Here we go. This is key. Do you think that funds would be able to maximise the selling price if external investors viewed the company as unlikely to perform well over time? Of course not. Prices are derived from future discounted cash flows. The more likely the company is to perform well after the sale, the higher the price the hedge (or private equity) fund can extract from it. As a result, it is not in the interest of the fund to seek “short-term gains at the expense of the future”.

Of course, this does not mean that no failure ever happens. Some funds also acquire companies to dismantle them. Which does not necessarily imply that they are evil. Some companies actually represent net economic losses to society with no prospect of improvements. Those companies should disappear and capital reallocated to more efficient ones. Funds that dismantle companies usually do it as there is no other way to realise profits. Some funds also fail in restructuring firms, or overload them with debt. But when the companies fail, funds also make massive losses that threaten their own existence. It is in the interest of both to succeed.

Co-op Bank’s former CEO declared that the restructuring process was a ‘tragedy’, that hedge funds were ‘maximising profits’ and were ‘unethical’. I would like to ask: what is actually a tragedy? Is mismanaging an institution leading to bankruptcy and potential losses for ordinary individuals that ethical? What about mis-selling financial products to naïve customers on top of that? Wouldn’t it be better to have a well-performing bank that generates economic profits? Are low profits, losses and waste of capital a way of proving that a company is behaving well? Or is a company more useful for human and social advancement if it actually delivers economic benefit and creates additional capital? Some people have serious rethinking to do.

There is no real need to worry about hedge funds owning a large stake in Co-operative Bank. Co-op may well at last become an asset to society instead of a liability. Its new hedge fund owners also seem to understand that to maximise the value of the brand, ethics must remain a focus, whatever that means. But if eventually Co-op does not survive, it may also well be because it couldn’t be saved in the first place.

Update: I don’t know how I originally missed the senior creditors but I did… Depositors aren’t the only senior creditors and this is now corrected

How increasing banks’ capital reduces lending

This is a controversial topic. Since the beginning of the financial crisis, there hasn’t been a single week without someone calling for increased banks’ capitalisation. What does it mean in practice?

Banks fund their loans and investments through several main channels: customer deposits (retail and corporate), interbank deposits, short and long-term wholesale borrowings, and equity. Equity represents around 3 to 7% of banks’ funding structure in developed-markets, i.e. equity funds 3 to 7% of the bank’s loans and investments. This has led many to say that banks are ‘over-leveraged’, as the rest of the funding structure is effectively debt, under one form or another. Under current and future Basel 3 rules, banks are also allowed to count some form of loss-absorbing hybrid debt and preference shares as complementary capital, on top of shareholders’ equity. This ‘Tier 1’ capital should reach 6% of risk-weighted assets (not of total assets, see my previous post) by 2019 (up from 4.5% previously).

Many people think it is not enough. In the UK, Sir John Vickers proposed that equity should fund 20% of the banks RWAs (up from the 10% he recommended with his Independent Commission on Banking). In the US, calls for higher capital requirements are also very common (see here, here, here). Most of them point to the fact that banks’ equity level used to be much higher in the past than it is now. I’ll come back to this claim and many others on capital in another post.

Today I only want to address the main claim backing the ‘more equity is always better’ argument: that increasing equity (or more generally, regulatory capital) does not negatively impact the banking sector’s lending ability. Research by Anat Admati and Martin Hellwig has provided the main intellectual foundation to proponents of increased capital requirements (see also their now famous book, The Bankers’ New Clothes, which has received positive comments from regulators and most of the financial media, and which I’ve read and will try to review when I have the time). Their argument about capitalisation looks convincing and has not really been challenged so far on theoretical grounds: capital does not represent money set aside for safety which could otherwise be used to lend, as some foolish bankers would like us to believe. Why? Because equity is also already used to lend. Therefore, we can increase equity and lending will not be constrained as a result. They are right (as highlighted at the beginning of my post). However, they are also wrong.

Let me take a very simple financial system, only comprising banks as financial intermediaries. Here are my assumptions:

– High-powered money supply (money base) M0 is fixed and there is no physical cash

– M1: money supply following deposit expansion through the money multiplier

– Reserve requirements (RR): 10% of deposits (even though in most developed countries this figure is closer to 1 or 2% or even non-existent nowadays)

Before considering two different scenarios, let’s remember that we live in a fractional reserve banking world. When you deposit money in a bank, the bank lends out a portion of it to other people (or invests it in securities). Effectively, the bank never has all of its depositors’ money at the same time. However, deposits are still considered as part of the money supply. Why? Think about your own reaction when you put money in a bank: you consider money as yours and redeemable on demand. So you hold your physical cash balances at a minimum, considering that you can go get the rest of your money whenever you want anyway. And your consumption pattern reflects your whole money holding (cash on hand and deposits), not only the cash that you have in your wallet.

As a result the money multiplier applies, according to reserve requirements. What is it? In such a system, banks can effectively lend out multiple times the funds that have originally been deposited, as long as they keep enough of them to satisfy daily withdrawal. As such, banks create money (through new deposits). In a world with 10% reserve requirements, the money multiplier is 1/RR = 1/0.1 = 10, meaning the banking system can potentially multiply the original deposit base up to 10 times through lending.

This is where things differ regarding equity. Equity is not a deposit. It is not subject to reserve requirements (and hence to the money multiplier). Once you’ve invested in a bank’s equity, you don’t consider this money as yours anymore (you only have a claim on it that cannot be used for anything else). The only thing you can do is sell your stake at some point in the future to generate cash. As such, equity funding is a kind of 100%-reserve banking system, i.e. equity transfers money instead of creating it. A banking system 100%-funded through equity would be similar to a 100%-reserve banking system, with banks essentially becoming some sort of mutual funds (and deposits not being used at all for investments).

Alright. Now let’s now see what happens if banks’ capital requirements is 10% of their assets. Ex-post, after applying the deposit multiplier (when the system if ‘fully loaded’), M1 should be comprised of 10% of equity and 90% of deposits. Consequently, to figure out the original ability of the system to lend and create extra-deposit, we need to work backward in order to find out the ex-ante money supply structure. Rebasing the 10%/90% M1 structure gives a 53%/47% M0 structure after dividing the deposit base by the deposit multiplier, equivalent to M0 = 19% of M1. It also means that the system’s fully-loaded state (M1, after monetary expansion through fractional reserve lending) represents 526% of the original money supply M0.

What if banks’ capital requirements are raised to 20% of their assets? Ex-post, after applying the deposit multiplier, M1 should be comprised of 20% of equity and 80% of deposits. The 20%/80% M1 structure gives a 71%/29% M0 structure once divided by the deposit multiplier, equivalent to M0 = 28% of M1. It also means that the fully-loaded state (M1) represents 357% of the original money supply M0.

Clearly, increasing capital requirements led to a lower potential money supply as banks were not able to lend as much as before as a larger part of the money supply was not subject to fractional reserves anymore. Admittedly, this is a very simple scenario that might not accurately reflect the effects of the various near-moneys and injection of reserves by central banks of the real world. However, it does show that Admati and Hellwig’s claim is not that simple and straightforward. They also never explain how capital requirements can be smoothly increased. In real life, the transition process can be quite painful as we witness every day at the moment (banks cutting lending in order not to issue new equity, etc).

Don’t get me wrong though. I am in favour of banks holding more equity. But I don’t want to force them to do so. There are various historical reasons that explain why equity as a percentage of assets is low nowadays, and most of them are due to….the influence of government’s policies. Surprising heh?

Recent Comments