Macro-pru, regulation, rule of law and public choice theory

Another rule of law-related post. It might be the anniversary of the Magna Carta that brought this topic back in fashion. Consider it as a follow-up post to my Hayekian legal principles post of a couple of weeks ago.

John Cochrane has a very long post on the rule of law on his blog (which could have been an academic article as the pdf version is 18-page long) titled The Rule of Law in the Regulatory State.

His vision is a little gloomy, but spot on I believe:

This rule of law always has been in danger. But today, the danger is not the tyranny of kings, which motivated the Magna Carta. It is not the tyranny of the majority, which motivated the bill of rights. The threat to freedom and rule of law today comes from the regulatory state. The power of the regulatory state has grown tremendously, and without many of the checks and balances of actual law. We can await ever greater expansion of its political misuse, or we recognize the danger ahead of time and build those checks and balances now.

He believes the rise of the regulatory state does not fit the standard definitions of socialism, regulatory capture or crony capitalism. He believes that we are

headed for an economic system in which many industries have a handful of large, cartelized businesses— think 6 big banks, 5 big health insurance companies, 4 big energy companies, and so on. Sure, they are protected from competition. But the price of protection is that the businesses support the regulator and administration politically, and does their bidding. If the government wants them to hire, or build factory in unprofitable place, they do it. The benefit of cooperation is a good living and a quiet life. The cost of stepping out of line is personal and business ruin, meted out frequently. That’s neither capture nor cronyism.

He thinks the term ‘bureaucratic tyranny’ could be appropriate to describe the situation, and that it is the ‘greatest danger’ to our political freedom. That is, opposing or speaking out against a regulatory agency, a politician or a bureaucrat might prevent you from obtaining the required regulatory approval to run your business.

He takes what seems to be a Public Choice view when he states that “the regulatory state is an ideal tool for the entrenchment of political power was surely not missed by its architects.”

While his post covers all sorts of industries, and while his definition of the rule of law (and its difference with mere legality) isn’t as comprehensive as Hayek’s, it remains pretty interesting. He actually has a lot to say on the current state of banking and financial regulation:

The result [of Dodd-Frank] is immense discretion, both by accident and by design. There is no way one can just read the regulations and know which activities are allowed. Each big bank now has dozens to hundreds of regulators permanently embedded at that bank. The regulators must give their ok on every major decision of the banks.

While he says that, for now, Fed staff involved in bank stress tests are mostly honest people, he is wondering how long it will take before the Fed (pushed by politicians or not) stop resisting the temptation to punish particular banks by designing stress tests (whose methodology is undisclosed) to exploit their weaknesses.

While Cochrane laments the rise of discretionary ruling and its consequences on freedom, The Economist also just published a warning, albeit a less-than-passionate one. Since the crisis, The Economist has always taken a somewhat ambivalent, if not completely contradictory double-stance (for instance, it takes position against rules in monetary policy in the same weekly issue). Here again, the newspaper believes that the crisis made new rules ‘inevitable’, because taxpayers ‘need protection from the risks of failure’. And that, as a result, regulators needed ‘flexible’ rules (MC Klein made a similar point some time ago – see my rebuttal here).

By and large, The Economist has approved that sort of rulemaking, as well as the use of macro-prudential policies (something I have regularly criticised on this blog). Nevertheless, the newspaper also complains about abuse of discretionary decision-making and the effect of regulatory regime uncertainty (a term originally coined by Robert Higgs). It doesn’t seem to have realised that the nature of what it was requesting (i.e. respect of the rule of law and control of the industry and of the monetary system by regulatory agencies) was by nature antithetical. Cochrane’s fears (as well as mine) thus seem justified if such a classical liberal newspaper cannot even realise this simple fact.

Public Choice theory could be used as a strong rebuttal to the regulatory discretion rationale. As Salter points out in a remarkable paper titled The Imprudence of Macroprudential Policy, the economic and political science behind discretionary macro-pru policies taken by bureaucratic agencies suffers from major flaws that regulators or academics haven’t even tried to address.

He highlights the fact that, as Mises and Hayek had already mentioned decades ago during the socialist calculation debate, regulatory agencies lack the information signalling system to figure out what the ‘right’ market price should be and hence act in the dark, possibly making the situation even worse* (and empirical evidences do show that it doesn’t work), and that the assumption of the macro-pru literature that capitalist (and financial) systems are inherently unstable is at best unproven. A typical example is Basel’s capital requirements: as I have long argued on this blog, RWAs incentivise the allocation of credit towards asset classes that regulators deem safe. The fact that they are aware of the allocative power that they have is clearly illustrated by the recent news that EU regulators would lower capital requirements on asset-backed securities to persuade insurance firms to invest in them! Yet they continue to blame banks for over-lending for real estate purposes and not enough ‘to the real economy’. Go figure.

Worse, Salter continues, macro-pru regulation (and his critique also applies to all other regulatory agencies) assumes away all Public Choice-related issues, taking for granted omniscient regulators always acting in the ‘public interest’. Yet proponents of strong regulatory agencies seem to ignore (voluntarily or not – rather voluntarily if we believe Cochrane) that regulatory agencies themselves can fall prey to the private interests of regulators, whether those are power, money, job… If not directly to the regulators, regulatory agencies can fall prey to voters’ irrationality, as Caplan would argue (but also Mises and Bastiat), leading elected politicians to put in place regulators executing the irrational wishes of the voters. The resulting naïve line of thought of the macro-pru and regulatory oversight school is dangerous and goes against the body of knowledge that Western civilization has accumulated since the Enlightenment period.

And such occurrences are not only present in the minds of Public Choice theorists. They are happening now. The case of the head of the British Financial Conduct Authority directly comes to mind: whether or not one agreed with his “shoot first, ask questions later” method (and many didn’t), he was removed from office by the new UK government as he didn’t fit in the new political ‘strategy’.

What can we do? Cochrane proposes a Magna Carta for the regulatory state, in order to introduce the checks and balances that are currently lacking in our system (for instance, appeals are often made with the same regulatory agency that took the decision in the first place). Buchanan would certainly argue for a similar constitutional solution that would attempt a return to the ‘meta-legal’ principles of the rule of law described by Hayek, with an independent judiciary as the main arbitrator.

The wider public certainly isn’t ready to accept such changes given its negative opinion of particular industries (they’d rather see more regulatory oversight). Consequently, the only way to convince them that constitutional constraints on regulatory agencies are necessary seems to me to remind them that regulatory discretion negatively affects them as well (and day-to-day examples of incomprehensible regulatory decisions abound). If broad principles can be agreed upon from the day-to-day experience of millions of people, they should apply more broadly to all types of sectors. As Salter concludes for macro-prudential policies (although it applies to any regulatory agency):

Market stability is ultimately to be found in institutions, not interventions. Institutions that are robust to information and incentive imperfections must be at the heart of the search for stable and well-functioning markets. Robust monetary institutions themselves depend on adherence to the rule of law and the protection of private property rights, which are the cornerstone of any well-functioning market order. Since macroprudential policy relies on unjustifiably heroic assumptions concerning the information and incentives facing private and public agents, its solutions are fragile by construction.

*Cowen and Tabarrok take another angle here by arguing that the problem of ‘asymmetric information’, which underlies most regulatory thinking, almost no longer exists in the information/internet age.

I’d rather not have a fox as bank regulator

We can sometimes read stupefying things on the internet. I almost fell off my chair yesterday when I read MC Klein’s latest banking piece on FT Alphaville. He suggests that the right way to regulate banks might well be to be “crazy like a fox”…

Throughout his ‘surprising’ post, he writes things like:

While simple rules about capital and short-term debt still have tremendous appeal, there is value in having a regulatory regime that is onerous precisely because of its complexity and its unpredictability.

And

As Matt Yglesias notes, the value of having lots of pointless but annoying rules is that they distract the bank lobbyists from the really important stuff. The swap pushout was the first in what is hopefully a long line of defence. We’re tempted to say that crafty policymakers should immediately propose several new and even more annoying rules for the banks.

Fortunately, regulators have other means of harassing their adversaries, hopefully keeping them busy enough to avoid exploiting the system too much.

Andrew Haldane must be having a heart attack right now.

This goes against some of the most basic economic principles, and against the very thing that allows any business to exist and thrive in the first place: the rule of law.

Let’s start with Matt Yglesias’ post. Perhaps not surprising for someone who once wrote that Dodd-Frank was an ‘achievement’ that created a ‘safer banking system’, Yglesias again proves that he has a very low understanding of how banking works. CDS contacts have apparently become ‘custom swaps’ that are used to “bet on the potential bankruptcy of a given country or company or the failure of a new financial product.” Hedging anyone? Insurance that can protect even the most vanilla-like institutions against some specific default risks? No, this is just an evil Wall Street speculative tool. Nevermind that some CDS are traded on behalf of clients, and banks’ positions taken to offset customers’ needs. Nevermind that siloing banking activities/liquidity/capital across different entities of a same banking group actually decrease the safety of the system (see also here).

Despite this rather limited knowledge of the industry, Klein builds on Yglesias’ reasoning: any repealed rule should be replaced by many pointless ones to distract lobbyists.

Now, I am still trying to understand the logic behind constantly adding red tape for no reason rather than judging rules and bureaucracy on their actual value-added and efficiency. Here again, nevermind that countries with the least efficient and most numerous rules are the least business-friendly, and that too much red tape and regulatory uncertainty is around the top issue for most US businesses at the moment. No, banking is (apparently) different.

Let me suggest that a few years working for a bank would probably help dispel some of those myths. That, lobbyists aren’t that dumb, and that, if they attack some specific rules, it is surely that these would be harmful for the banks (and indeed, both Yglesias and Klein are plain wrong in considering this CDS rule ‘pointless’). That the 30,000-page rulebook that Dodd-Frank created might not fully facilitate banking processes and lending. That, by constantly changing the rules as Klein suggests, banks might well be tempted to move away from any risky activity that might end up being considered unlawful at some point in the future, hurting risky lending in the process (i.e. usually SME lending, as if it were not already low enough) with all the associated potential economic consequences.

Banks have been closing entire lines of business, de-globalising, preventing international payments to go through, harming international trade and economic activity. The multiplication of rules could, not only lead to resource misallocation, but also to increased management time. Management time that would be better spent on analysing and controlling the business than on bureaucratic, ‘pointless’, but dangerous (because of potential fines) rules. Unexpected consequences if you like. Still, it looks acceptable for Klein.

This is exactly why avoiding regulatory uncertainty and discretionary policies, and applying a predictable set of rules (i.e. rule of law), is so crucial in facilitating business and economic development.

As Kevin Dowd clearly illustrates in a very good recent paper:

One has to understand that the banks have no defense against this regulatory onslaught. There are so many tens or hundreds of thousands or maybe millions of rules that no one can even read them all, let alone comply with them all: even with armies of corporate lawyers to assist you, there are just too many, and they contradict each other, often at the most fundamental level. For example, the main intent of the Privacy Act was to promote privacy, but the main impact of the USA PATRIOT Act was to eviscerate it. This state of lawlessness gives ample scope for regulators to pursue their own or the government’s agendas while allowing defendants no effective legal recourse. One also has to bear in mind the extraordinary criminal penalties to which senior bank officers are exposed. Government officials can then pick and choose which rules to apply and can always find technical infringements if they look for them; they can then legally blackmail bankers without ever being held to account themselves. The result is the suspension of the rule of law and a state of affairs reminiscent of the reign of Charles I, Star Chamber and all. Any doubt about this matter must surely have been settled with the Dodd-Frank Act, which doled out extralegal powers like confetti and allows the government to do anything it wishes with the banking system.

A perfect example of this governmental lawlessness was the “Uncle Scam” settlement in October 2013 of a case against JP Morgan Chase, in which the bank agreed to pay a $13billion fine relating to some real estate investments. This was the biggest ever payout asked of a single company by the government, and it didn’t even protect the bank against the possibility of additional criminal prosecutions. What is astonishing is that some 80 percent of the banks’ RMBS had been acquired at the request of the federal government when it bought Bear Stearns and WaMu in 2008, and now the bank was being punished for having them. Leaving aside its inherent unpleasantness, this act of government plunder sets a very bad precedent: going forward, no sane bank will now buy a failing competitor without forcing it through Chapter 11. It’s one thing to face an acquired institution’s own problems, but it is quite another to face looting from the government for cooperating with the government itself.

The argument’s logic is also very weak. If rules are believed to let excessive risks “fall through the cracks”, then they should never be adopted in the first place. Why even adopting rules which we already know create systemic risks? If regulators really believe those rules will cover most (or all) risks, there is no point in planning to replace them with other rules, just for the sake of changing the rules, as the new ones are likely to be less effective. Otherwise those new, more effective, rules are the ones that should have been implemented in the first place. The whole logic of the argument just doesn’t hold*.

What about the practicality of ever changing the regulatory framework? Here again the argument fails. There aren’t hundreds of derivative settlement options and assets acceptable as collateral or as liquidity buffer. While the theory sounds nice in FT Alphaville’s columns, it is simply not possible to implement in practice.

The financial imbalances that led to our previous crisis, for a large part, originated in the most complex banking rule set devised in history, compounded by politically-incentivised housing agendas (along with misguided monetary policy and accounting rules). Klein’s (and Yglesias’) failure is to ignore this and assume that more, and tighter, rules are more effective. Moreover, regulators’ failure to foresee crises has probably been a constant throughout history. Yet, Klein backs an ever-more complex and constantly-changing regulatory framework at the discretion of those same regulators.

Calomiris and Nissim, two academics that know and understand a thing or two about banking, declared that:

We worry that regulatory uncertainty – and especially the persistent waves of political attacks on global universal banks – is taking a toll.

It is important to recognize that bank stockholders are not alone in suffering from the low stock prices that result from these attacks. The supply of bank loans, and banks’ ability to provide other crucial financial services in support of economic growth, reflect the risk-bearing capacity of banks, which is directly related to market valuations of bank franchises. If banks’ earnings get little respect from the market, banks’ abilities to help the economy grow will be commensurately hobbled.

Even The Economist, which has been a supporter of banking regulatory reform over the past few years, is against regulatory discretion and is well-aware of regulators’ weaknesses (emphasis mine):

Attracting the capital that will make banking safer will be hard, with profit forecasts so anaemic. However it will also be made unnecessarily difficult by capricious behaviour from the very watchdogs who are ordering banks to raise the funds.

One problem is the endless tinkering with the rules. For all Mr Carney’s talk of finishing the job, global regulators have yet to set the minimum level for several of their new capital requirements. National regulators are just as bad. No bank can be certain how much capital it will need in a few years’ time. Pension funds and insurance companies rightly fret that even a tiny tweak in any of the new regulatory tests is enough to send a bank’s share price plummeting (or, less often, rocketing). […]

Banks can hardly be surprised that regulators have rewritten the rule-book and then thrown it at them. But, for the health of the system, the rules need to be predictable, transparent and consistent. Incredibly, the regulations emanating from America’s Dodd-Frank financial reforms are still being written, more than four years after the law was passed. Europe is scarcely better. Impose demanding capital rules, but stop adding more red tape: that should be the mantra of bank regulators just about everywhere.

The worst is: Klein does identify some of the problems with our current regulatory regime, which is easily gameable because of its complexity. In terms of regulation and forecasting, simple rules and models have always performed better (see some of the links above). But instead of stepping back and getting back to simpler, less distortive, rules, his policy of choice seems to be more bank-bashing, never-ending regulatory regime uncertainty, more complexity, the possible paralysis of bank lending and the build-up of risk within the more opaque shadow banking system. I guess it’s going to be a real success.

* He could reply that the very purpose of ‘pointless’ rules is that they have no real impact on anything. Let me clarify something: all rules have an impact, whether it is small, big, negative, positive, or both (and again, the CDS rule was far from pointless). He could also reply that changing the rules limit the gameability of the system. But this makes little sense, as ‘pointless’ rules changes would probably not prevent the accumulation of risk anyway and, even for ‘non-pointless’ rules, there are only a few available options as described above (changing capital requirements by 1% up or down, including or excluding A+ rated bonds as LCR-compliant, increasing/decreasing haircut requirements by 5%, and so forth, really would have very little impact on gameability or stability).

Breaking banks won’t help economic recovery

In contrast with the bank-bashing environment of the post-crisis period, voices are increasingly being raised to moderate regulatory, political and judiciary risks on the banking system.

Last week, Gillian Tett wrote an article in the FT tittled “Regulatory revenge risks scaring investors away”. She says:

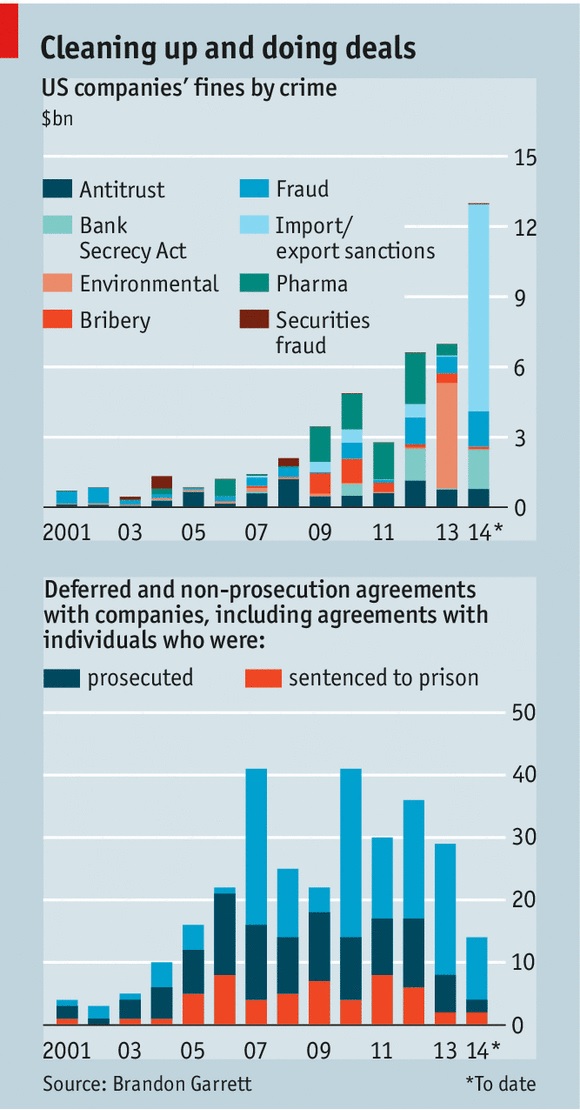

Last month [Roger McCornick’s] project team published its second report on post-crisis penalties, which showed that by late 2013 the top 10 banks had paid an astonishing £100bn in fines since 2008, for misbehaviour such as money laundering, rate-rigging, sanctions-busting and mis-selling subprime mortgages and bonds during the credit bubble. Bank of America headed this league of shame: it had paid £39bn by the end of 2013 for its transgressions. When the 2014 data are compiled, the total penalties will probably have risen towards £200bn.

She argues that “legal risk is now replacing credit risk.” This is a key issue. Banks have already been hit hard by new regulatory requirements, which sometimes require a fundamental restructuring of their business model. The consequences of this framework shift is that profitability, and hence internal capital generation, remain subdued, weakening the system as a whole. Banks now reporting double digit RoEs are more the exceptions than the rule. Moreover, low profitability also reduces the banks’ ability to generate capital externally (i.e. capital raising) because they do not cover their cost of capital. This scares investors away, as they have access to better risk-adjusted investment opportunities elsewhere.

The enormous amounts raised through litigation procedures make such a situation even worse. Admittedly, banks that purposely bypassed laws or committed frauds should be punished. But, as The Economist argues this week in a series of articles called “The criminalisation of American business” (see follow-up article here), the “legal system has become an extortion racket”, whose “most destructive part of it all is the secrecy and opacity” as “the public never finds out the full facts of the case” and “since the cases never go to court, precedent is not established, so it is unclear what exactly is illegal”:

This undermines the predictability and clarity that serve as the foundations for the rule of law, and risks the prospect of a selective—and potentially corrupt—system of justice in which everybody is guilty of something and punishment is determined by political deals. America can hardly tut-tut at the way China’s justice system applies the law to companies in such an arbitrary manner when at times it seems almost as bad itself.

Estimates of capital shortfall at European banks vary between EUR84bn and as much as EUR300bn (another firm, PwC, estimates the shortfall at EUR280bn). Compare those amounts with the hundreds of billions Euros paid or about to be paid by banks as litigation settlements, and it is no surprise that banks have to deleverage to comply with regulatory capital ratio deadlines and upcoming stress tests… Such high amounts, if justified, could probably have been raised by prosecutors at a slower pace in the post-crisis period without endangering the economic recovery (banks’ balance sheets would have been more solid more quickly, which would have facilitated the lending channel of the monetary transmission mechanism).

In the end, regulatory regime uncertainty strikes banks twice: financial regulations keep changing (and new ones are designed), and opaque litigation risk is at an all-time high. Banks are now very risk-averse, depressing lending and international transactions. This seems to me to replicate some of the mistakes made by Roosevelt during the Great Depression. Despite all the central banks’ money injection programmes, this may not be the best way out of an economic crisis…

PS: Commenting on the forthcoming P2P lender Lending Club IPO, Matt Levine argues that:

But Lending Club can grow its balance sheet all it wants. Lending Club is not a bank. So it’s not subject to banking regulation, which means that it can do a core function of banking much more efficiently than an actual bank can.

He is (at least) partly right. By killing banks, regulatory constraints are likely to trigger the emergence of new types of lenders.

Wait… Isn’t it what’s already happened (MMF and other shadow banking entities…)?

Is the BIS on the Dark Side of macroeconomics?

The BIS has got a hobby: to annoy other economists and central bankers. It’s a good thing. It published its annual report about two weeks ago, and the least we can say is that it didn’t please many.

Gavin Davies wrote a very good piece in the FT last week, summarising current opposite views: “Keynesian Yellen versus Wicksellian BIS”. What’s interesting is that Davies views the BIS as representing the ‘Wicksellian’ view of interest rates: that current interest rates are lower than their natural level (i.e. monetary policy is ‘loose’ or ‘easy’). On the other hand, Scott Sumner and Ryan Avent seem to precisely believe the opposite: that current rates are higher than their natural level and that the BIS is mistaken in believing that low nominal rates mean easy money. This is hard to reconcile both views.

Neither is the BIS particularly explicit. Why does it believe that interest rates are low? Because their headline nominal level is low? Because their real level is low? Or because its own natural rates estimates show that central banks’ rates are low?

It is hard to estimate the Wicksellian ‘natural rate’ of interest. Some people, such as Thomas Aubrey, attempt to estimate the natural rate using the marginal product of capital theory. There are many theories of the rate of interest. Fisher (described by Milton Friedman as America’s best ever economist), Bohm-Bawerk, and Mises would argue that the natural interest rate is defined by time preference (even though they differ on details), and Keynes liquidity preference. Some economists, such as Miles Kimball, currently argue that the natural rate of interest is negative. This view is hard to reconcile with any of the theories listed above. Fisher himself declared in The Rate of Interest that interest rates in money terms cannot be negative (they can in commodity terms).

Unfortunately, and as I have been witnessing for a while now, Wicksell is very often misinterpreted, even by senior economists. The latest example is Paul Krugman, evidently not a BIS fan. Apart from his misinterpretation of Wicksell (see below), he shot himself in the foot by declaring (my emphasis):

Now, what about the BIS? It is arguing that central banks have consistently kept rates too low for the past couple of decades. But this is not a statement about the Wicksellian natural rate. After all, inflation is lower now than it was 20 years ago.

Given that we indeed got two decades of asset bubbles and crashes, it looks to me that the BIS view was vindicated…

Furthermore, in a very good post, Thomas Aubrey corrects some of those misconceptions:

The second issue to note is that when the natural rate is higher than the money rate there is no necessary impact on the general price level. As the Swedish economist Bertie Ohlin pointed in the 1930s, excess liquidity created during a Wicksellian cumulative process can flow into financial assets instead of the real economy. Hence a Wicksellian cumulative process can have almost no discernible impact on the general price level as was seen during the 1920s in the US, the 1980s in Japan and more recently in the credit bubble between 2002-2007.

(Bob Murphy also wrote a very good post here on Krugman vs. Wicksell)

But there are other problematic issues. First, inflation (as defined by CPI/RPI/general increase in the price level) itself is hard to measure, and can be misleading. Second, as I highlighted in an earlier post, wealthy people, who are the ones who own most investible assets, experience higher inflation rates. In order to protect their wealth from declining through negative real returns (what Keynes called the ‘euthanasia of the rentiers’), they have to invest it in higher-yielding (and higher-risk) assets, causing bubbles is some asset classes (while expectations that central bank support to asset prices will remain and allow them to earn a free lunch, effectively suppressing risk-aversion).

If natural rates were negative – or at least very low – and the environment deflationary, it is unlikely that we would witness such hunt for yield: people care about real rates, not nominal ones (though in the short-run, money illusion can indeed prevail). But this is not only an ultra-rich problem: there are plenty of stories of less well-off savers complaining of reduced purchasing power.

Meanwhile, the rest of the population and overleveraged companies, supposedly helped by lower interest rates, seem not to deleverage much: overall debt levels either stagnate or even increase in most economies, as the BIS pointed out.

Banks also suffer from the combination of low rates* and higher regulatory requirements that continue to pressurise their bottom line, and have ceased to pass lower rates on to their customers.

In this context, the BIS seems to have a point: rates may well be too low. Current interest rate levels seem to only prevent the reallocation of capital towards more economically efficient uses, while struggling banks are not able to channel funds to productive companies.

Critics of the BIS point to their call to rise rates to counter inflation back in 2011. Inflation, as conventionally measured, indeed hasn’t stricken in many countries. In the UK and some other European countries though, complaints about quickly rising prices and falling purchasing power have been more than common (and I’m not even referring to house price inflation). This mismatch between aggregate inflation indicators and widespread perception is a big issue, which underlies financial risk-taking.

In the end, Keynes’ euthanasia of the rentiers only seem to prop up dying overleveraged businesses and promote asset bubbles (and financial instability) as those rentiers pile in the same asset classes. I side with the BIS in believing this is not a good and sustainable policy.

I also side with the BIS and with Mohamed El-Erian in believing in the poor forecasting ability of most central bankers, who seem to constantly display a dovish view of the economy, which apparently experiences never-ending ‘slack’, as well as the very uncertain effect of macro-prudential policies, which cannot and will not get in all the cracks. Nevertheless, many mainstream economists and economic publications seem to be overconfident in the effectiveness of macro-prudential policies (see The Economist here, Yellen here, Haldane here, who calls macropru policies “targeted lightning strikes”…).

While central banks’ rates should probably already have risen in several countries (and remain low in others, hence the absurdity of having a single monetary policy for the whole Eurozone), everybody should keep the BIS warnings in mind: after all, they were already warning us before the financial crisis, yet few people listened and many laughed at them.

Unfortunately, politicians and regulators have repeated some of the mistakes made during the Great Depression: they increased regulation of business and banking while the economy was struggling. I have many times referred to the concept of regulatory uncertainty, as well as the over-regulation that most businesses are now subject to (in the US at least, though this is also valid in most European countries). Businesses complaints have been increasing and The Economist reported on that issue last week.

In the meantime, while monetary policy has done (almost) everything it could to boost credit growth and to prevent the money supply from collapsing, harsher banking regulation has been telling banks to do the exact opposite: raise capital, deleverage, and don’t take too much risk.

In the end, monetary policy cannot fix those micro-level issues. It is time to admit that we do not live in the same microeconomic environment as before the crisis. What about cutting red tape to unleash growth rather than risk another financial crisis?

* Yes, for banks, rates are low, whichever way you look at them. Banks can simply not function by earning zero income on their interest-earning assets (loan book and securities portfolio).

PS: Noah Smith, another member of the anti-BIS crowd, has a nonsense ‘let’s keep interest rate low forever’-type article here: raising interest rates would lead to an asset price crash, so we should keep them low to have a crash later. Thanks Noah. The way he describes a speculative bubble is also wrong (my emphasis):

The theory of speculation tells us that bubbles form when people think they can find some greater fool to sell to. But when practically everyone is convinced that asset prices are relatively high, like now, it’s pretty obvious that there aren’t many greater fools out there.

Really? No, speculation involved buying as long as you believe you can get the right timing to exit the position. Even if everyone believed that asset prices were overvalued, as long as investors expect prices to continue to increase, speculation would continue: profits can still be made by exiting on time, even if you join the party late.

PPS: A particularly interesting chart from the BIS report was the one below:

It is interesting to see how coordinated financial cycles have become. Yet the BIS seems not to be able to figure out that its own work (i.e. Basel banking rules) could well be the common denominator of those cycles (which were rarely that synchronised in the past).

It is interesting to see how coordinated financial cycles have become. Yet the BIS seems not to be able to figure out that its own work (i.e. Basel banking rules) could well be the common denominator of those cycles (which were rarely that synchronised in the past).

News digest: Scotland, CoCos and electronic trading

Sam Bowman had a very good piece on the Adam Smith Institute blog about Scotland setting up a pound Sterling-based free banking system unilaterally (yeah I know I keep mentioning this blog now, but activity there seems to have been picking up recently). It draws on George Selgin’s post and is a very good read. One particular point was more than very interesting in the context of my own blog (emphasis added):

George Selgin has pointed to research by the Federal Reserve Bank of Atlanta about the Latin American countries that unilaterally use the dollar. Because these countries – Panama, Ecuador and El Salvador – lack a Lender of Last Resort, their banking systems have had to be far more prudent and cautious than most of their neighbours.

Panama, which has used the US Dollar for one hundred years, is the most useful example because it is a relatively rich and stable country. A recent IMF report said that:

“By not having a central bank, Panama lacks both a traditional lender of last resort and a mechanism to mitigate systemic liquidity shortages. The authorities emphasized that these features had contributed to the strength and resilience of the system, which relies on banks holding high levels of liquidity beyond the prudential requirement of 30 percent of short-term deposits.”

Panama also lacks any bank reserve requirement rules or deposit insurance. Despite or, more likely, because of these factors, the World Economic Forum’s Global Competitiveness Report ranks Panama seventh in the world for the soundness of its banks.

I don’t think I have anything to add…

SNL reported yesterday that Germany’s laws seem to make the issuance of contingent convertible bonds (CoCos) almost pointless. This is a vivid reminder of my previous post, which highlighted some of the ‘good’ principles of financial regulation and which advocated stable, simple and clear rules, a position I have had since I’ve opened this blog. All authorities and regulators try to push banks (including German banks) to boost their capital level, which are deemed too low by international standards. CoCos, which are bonds that convert into equity if the bank’s regulatory capital ratio gets below a certain threshold, are a useful tool for banks (as it allows them to prevent shareholder dilution by issuing equity) and investors (whose demand is strong as those bonds pay higher coupon rates). Yet lawmakers, who love to bash banks for their low level of capitalisation, seem to be in no hurry to provide a clear framework that would allow to partially solve the very problems they point at in the first place… This is a very obvious example of regime uncertainty. As one lawyer declared:

One thing is clear: Nothing is clear

Bloomberg reports that FX traders are facing ‘extinction’ due to the switch to electronic trading. In fact, this has been ongoing for now several years, with asset classes moving one after another towards electronic platforms. Electronic trading now represents 66% of all FX transactions (vs. 20% in 2001). Traditional traders are going to become increasingly scarce and replaced by IT specialists that set and programme those machines. Overall, this should also mean less staff and a lower cost base for banks that are still plagued by too high cost/income ratios. Part of this shift is due to regulation, which makes it even more expensive to trade some of those products. This only reinforces my belief that regulation is historically one of the primary drivers of financial innovation, from money market funds to P2P lending…

A brief comment on Blackrock, groupthinking and ‘secular stagnation’

Two interesting articles on Blackrock, the world’s largest asset manager (here and here) in this week’s Economist. The Economist is right to point out that regulators would be wrong to classify Blackrock as systematically important, which would considerably increase its regulatory burden. Unlike banks, Blackrock (and other asset managers) transfers money rather than creates it. As a result, there is no risk of ‘secondary deflation’, or money supply contraction, during a crisis if the value of its assets under management fall or if Blackrock itself fails. If markets collapse, investors take the hit, not Blackrock or any other asset manager (although they do take a hit to their revenues as assets under management fall). Of course, investors suffering from a fall in asset value can have other repercussions on the economy. But at least the collapse is not made worse by banks contracting their lending or failing, putting pressure on the money supply at the very moment money demand jumps.

The other issue raised by The Economist is about ‘groupthinking’, as many investors now use the asset manager’s analytics platform to guide them in their investment and trading decisions. The Economist is right on that topic too. However, I would say that groupthinking does not only emanate from Blackrock’s platforms… It is probably a topic I’ll discuss more in details another time, but we could argue that financial exams such as the CFA also push towards groupthinking by making it compulsory to follow certain analytical frameworks while not offering any real alternative. Therefore investors end up using the same models. Various investors will evidently come up with differing inputs; but those would then pass through the same machinery and outputs would be only slightly different.

A quick note on the fashionable ‘secular stagnation’, Lawrence Summers’ and Paul Krugman’s new favourite topic (actually, I don’t know). Apparently, there aren’t enough productive investments in the world relative to the stock of savings. The “appetite to invest” (in The Economist’s words) is low.

I found an interesting short video yesterday:

Does it remind you anything? I’ve argued many times over the past few months that there are indeed plenty of productive investments, but that entrepreneurs and investors are too scared to invest due to regime uncertainty and red tape (see also here and here). Let’s name a few: fracking, mobile IT, emerging markets, commercial space ventures, drones, green energy… And I’m surely forgetting a lot. Yet, so many economists try to reach conclusions from analysing a few aggregated macro-economic data while forgetting to take a look at what’s going on the micro-economics side. This is a big mistake.

The ivory tower economist syndrome

Here we go. Academic economists are lost. Lawrence Summers just made a striking announcement in a speech a few days ago: we are likely to be in a secularly stagnating economy that needs recurrent bubbles to achieve full employment, as its natural rate of interest has been constantly below zero for a while. Evidently, Krugman, Sumner, Cowen, Wolf and many other economists started to discuss the issue. Some agree, some don’t. However, most seem to miss the main problem. I call that the ivory tower economist syndrome. Abstractly thinking in terms of aggregated economic figures locked in a university or government office won’t be of much help. Zerohedge rightly makes fun of Summers and Krugman, as the satiric newspaper The Onion made the same economic advices a few years ago:

Congress is currently considering an emergency economic-stimulus measure, tentatively called the Bubble Act, which would order the Federal Reserve to† begin encouraging massive private investment in some fantastical financial scheme in order to get the nation’s false economy back on track.

Who said that was fiction?

Many of them are backing their ideas using wrong arguments. For instance, Summers and Krugman don’t believe interest rates were too low before the crisis as… there was no inflation! Sure, but, how do you know that? CPI? RPI? GDP deflator? There are many problems with inflation figures. Let’s list some of them:

- They don’t accurately reflect inflation. You can change the calculation and the result changes dramatically. Moreover, the goods picked to calculate them and the weights applied to them are quite arbitrary. This is supposed to reflect the ‘average’ household basket. Well, I am not the average household apparently as my own inflation rate has been way higher than headline inflation over the past few years.

- 0% CPI increase does not mean that there is no inflation. Productivity increase drives inflation down. As a result, reasoning in terms of headline inflation is a mistake. Real inflation is hidden. The fastest economic growth in the history of the Western world (late 19th and early 20th century) occurred during a long period of secular deflation…

- Most asset prices aren’t reflected in inflation figures. Newly created money now mostly go to investments, a lot of which being speculation. Most of banks’ lending is mortgage lending. So newly-created money goes to housing, pushing up prices… which aren’t reflected in inflation figures. Sure, one can argue that, at some point, there will be inflationary pressure on consumer goods. But productivity increases reducing the price of domestically-produced goods (IT revolution anyone?) and cheap goods from developing countries mask that process. Moreover, when asset bubbles burst (which they eventually do), the wealth effect from asset price increases that could lead to inflation all but disappears. Lending was also different 50 or 100 years ago: much lending did not go directly to investments in financial or real assets. Consequently consumer goods inflation appeared a lot faster after new monetary injection (considering stable productivity).

So justifying the fact that nominal interest rates defined by central banks were not low because there was no inflation is in itself wrong, or at best inaccurate. In reality, low interest rates are very likely to have caused, or at least participated, in the recent credit bubble. Regarding the so-called ‘savings glut’, Cowen agrees with Kling on the fact that, if we really had ‘too much’ savings chasing ‘too few’ investment opportunities, we would not need central banks’ actions to push interest rates lower. The supply and demand of loanable funds would automatically drive the interest rate to a very low level.

But, most importantly, all those economists forget a fundamental fact that I have been mentioning a hundred times recently: regime uncertainty (yes, again…). For economists to speak in terms of monetary and spending aggregates alone and to not pay attention to the broader context surrounding businesses is a major mistake. I’ve kept repeating and giving many evidences recently (like here, here, and here) that businesses currently delay investments due to the uncertain regulatory and economic decisions taken by governments and regulators all around the world. This is now the major issue for SMEs and banks at least. Again today, Euromoney published an interesting short article on ‘renewed regulatory uncertainty’ for banks:

For all the populist fervor then about perceived policy inaction to address systemic risk, many banks see it differently: investor flight from banks’ equity and bond products has taken root over the years, amid fears that new rules will render business models uneconomic.

Take a look at that SEB and Deloitte chart summarising current regulatory reforms. It looks slightly messy doesn’t it? And look how it is named…

A bank analyst told Euromoney that:

Changes in regulations, changes in what other stakeholders consider to be acceptable, the risk that the behaviours of certain employees become associated with the institution as a whole – those are indeed much more expensive for banks these days than credit [risk].

As I have already highlighted in an earlier post, more than the number of rules, it is the fact that rules change that is crucial to business planning. You can’t play a certain game if the rules of the game constantly change. Yet none of those ‘great’ economists ever mentioned regulation, uncertainty, rules or anything related. Looks like abstract economic aggregates are a lot more interesting to manipulate…

Get out of your tower guys!

The Economist joins the regime uncertainty crowd

Has The Economist been reading my blog recently? Over the past two weeks, the newspaper that used to justify the use of more and more monetary and fiscal stimulus to push firms to invest (as the only reason why they would not invest was lack of demand) seems to have suddenly waken up to the fact that, after all, regulatory regime uncertainty could well be part of the current low business investment problem. This is welcome but a little late.

In a short Buttonwood article last week, the newspaper asserts that “arbitrary decisions by governments may reduce business confidence, and thus inhibit the investment the politicians want to see” and that:

What troubles businessfolk and investors most is the random nature of the process. They do not know where the next tax will be levied or regulatory boot descend. When rules are proposed, it can take ages for the details to emerge, making it hard for companies to plan ahead. That is the most insidious—and most underestimated—form of political risk.

Indeed.

The piece highlights that, in the latest World Economic Forum competitiveness survey, Singapore ranks first in terms of regulatory burden, whereas struggling EU countries are ranked close to the bottom: Spain is 125th, France 130th, Greece 144th, and Italy 146th. The US has also experienced a huge collapse over the past seven years regarding the perception of its regulatory burden: 23rd to…..80th. It’s probably not going to help the economic recovery, is it?

In this week’s edition of the newspaper, the Free Exchange column takes a look at recent research on uncertainty and investment. Results are striking:

They find that doubts about tomorrow have a big influence on what happens today. For every ten percentage points their measure of uncertainty rose, investment fell by one percentage point. During the financial crisis of 2008-09, for example, they calculate that implied volatility rose by almost 40 percentage points, suggesting a drop in investment due to uncertainty of just under four percentage points. That implies that uncertainty accounted for around half of the total drop in investment during the crisis. And it is not just spending on physical assets that declines. The authors find that other long-term outlays—hiring staff and launching advertising campaigns—also plunge when uncertainty rises.

Interestingly, The Economist also mentions the banking sector:

Governments, however, are still breeding fears about the future. The most glaring form of uncertainty in the rich world is fiscal. In the euro area cash-strapped peripheral states rely on bail-outs from richer members or the IMF. As each round of talks—on a banking union, or a deposit-insurance scheme—approaches, sensible bosses decide to wait and see what happens. In America endless budgetary brinkmanship has led to a quarterly debate over whether the government will default on its debts (the next deadline is in February). This is self-imposed uncertainty. If the fiscal path were a little clearer, the reduction in uncertainty should spur investment and output, which in turn should improve the fiscal picture. To cut the debt, first clear the doubt.

Of course, The Economist falls short of claiming that stimulus does not work. Of course not. It declares that even more stimulus is necessary in uncertain conditions. Someday they’ll hopefully notice the fallacy in such logic…

Chart: The Economist

A few complementary notes on regime uncertainty

Not much about finance or banking today. I just wanted to come back to a few concepts I mentioned in earlier posts (like here, here and here), such as regulatory regime uncertainty.

We keep hearing economists, journalists and politicians complaining about companies not investing ‘enough’ at the moment. Keynesians like Krugman, de Long and co, and some other non-Keynesian mainstream economists think that the main underlying reason to this phenomenon is lack of demand. I argued several times that, while demand fell probably too low in 2009, one of the other main culprits since then had been regime uncertainty: regulations keep changing and red tape expanding, leading most firms to postpone their various investments and projects until they have a clearer view of the rules going forward.

The Economist’s Buttonwood’s blog had a post about business regulation two days ago, which led me to look for some evidence that increasing (and uncertain) regulation was negatively impacting investments. I found this US Chamber of Commerce Small Business Study, which is enlightening. What it reveals:

- 44% of SME owners ranked economic uncertainty as their number 1 worry (with over-regulation at number 3, or 39%, and high taxes number 4, or 37%). To be fair, economic uncertainty also comprises demand uncertainty. But read the rest first.

- Only 24% indicated that they thought that business climate for SME had improved over the last couple of years.

- 42% of SME owners ranked the US growing deficit and debt as number 2 worry.

- “Seventy-eight percent of small business owners said that the U.S. deficit and debt pose a threat to the success of their businesses. The current federal debt and deficit (40%) and the regulations coming out of Washington (35%) are the top two current issues coming out of Washington that cause concern about the future of their businesses. In addition, sentiment is strong that the climate for small businesses is worse than under the previous administration (80%).”

- “The majority of small business owners, when asked what they need most from Washington right now, would like Washington to get out of the way (84%) as opposed to lending a helping hand (11%). When asked about specific actions they needed from Washington, overwhelmingly small business owners wanted more certainty (87%).”

- “Government regulations on small businesses continue to be seen as unreasonable (73%) by small business owners with a two thirds majority (66%) saying that what Washington will do next to small businesses scares them most.”

Right. It’s kind of a proof, isn’t it? This is also applicable to banks: giving God-like powers to regulators (or anyone) is usually not a good idea. Uncertainty is everywhere in the banking world. Just look at the latest Swiss news: a top official announced that, perhaps, Swiss banks will be subject to a very high 10% leverage ratio. Or perhaps just 6%. Or in between. Or possibly not at all. Or…well, they’re gonna discuss and let you know later. How can any bank plan for the future and lend in such conditions?

On a side not, I am wondering whether or not increasing red tape is linked to The Decline of Creative Destruction, as this Bryan Caplan piece was named today. Surely it is. Very interesting chart anyway (see below). Job destructions during the crisis were actually at the same level as they were throughout the 1990’s… It would be interesting to compare this chart to the evolution of business red tape. Unfortunately, this isn’t my area, so I’ll let you do it!

Recent Comments