Crowdfunding, naivety and scandals

John Kay wrote an interesting article for the FT yesterday, titled “Regulators will get the blame for the stupidity of crowds.” He argues that, despite crowdfunding and P2P enthousiasts blaming regulators for being too slow and too cautious, this new market will eventually crash and trigger calls for more advanced regulation as well as the setup of compensation schemes. Desintermediation firms would then reintermediate lending and effectively transform into… banks.

I partly agree with Kay. A collapse/crash/losses/fraud/scandals is/are inevitable. And this is a good thing.

I have already written about the importance of failure in free market financial systems. New financial innovations need to experience failures in order to end up reinforced, to distinguish what works from what doesn’t work. This is a Darwinian learning process. The system then becomes ‘antifragile’. Consequently, the state should refrain from intervening in order not to postpone this necessary learning process and resulting adjustments. When crowdfunding crashes, the state should resist any call for intervention/bailout/regulation. This is the only way crowdfunding can become a mature industry.

I however also partly disagree with Kay, who I believe does not see the bigger picture.

Kay argues that investors (in this case ‘crowds’) are naïve. That intermediation has benefits and non-professional investors lack the ‘cynicism’ to assess the risk/reward profile of those investments.

Where Kay is wrong though, is in considering P2P lending as “a substitute for deposit account.” It is not. P2P lending is an investment. Unsophisticated retail investors can also lose much of their money by investing in various stocks. Or by betting on the wrong horse. I don’t believe investors mistake crowdfunding for bank deposits…

I think that what Kay also fails to see is that, if historically many start-ups and young SMEs have struggled to grow and eventually failed, it is partly because they lacked the funds required to grow. Some start-ups ended-up collapsing or selling themselves to larger competitors simply because funding became scarce at the second or third round of funding. This funding gap was particularly prevalent in some markets such as the UK (less so in the US). Some other markets, such as France, on the other hand, lack first round financing (seed funding, mainly provided by ‘Angel’ investors).

When the supply for loanable funds is scarce relative to the demand, demanded return on investment is high. Many new firms, particularly in non-growth markets, find it hard to cope with this situation and are pretty much avoided by venture capital investors. What equity crowdfunding and P2P lending do is to increase the supply of loanable funds, reducing the average required rate of return. Refinancing risk mechanically recedes, guaranteeing the success or the failure of an SME on its business strategy and execution alone.

In addition, crowdfunding multiply investment opportunities, making it easier to diversify a portfolio of investments. Historically, venture capital funds could not diversify too much if they wanted to maintain appropriate levels of returns.

Scandals are inevitable, but the learning mechanism inherent to the market process must be allowed to run its course. Learning, combined with the increased supply of loanable funds, would reduce the probability of scandals occurring in the long-run and make crowdfunding a solid industry.

The bank branch is dying. Some politicians don’t seem to get it

Technology is both a curse and a blessing for banks. It usually starts as a curse and ends up being a blessing (at least for the banks that eventually managed to master technological disruptions). I’ve personally argued several times during BarcampBank debates that the branch was outdated. The rebuttal I usually got (especially from French financial actors and entrepreneurs, probably a cultural thing) is that customers want to ‘feel’ some humanity, and not interact with some faceless system. I don’t disagree, but I would argue that they are massively overestimating the ‘humanity’ factor. What people want is convenience.

‘Humanity’ is just an inefficient way of providing convenient services to customers. When your services and IT systems aren’t convenient and instinctive enough for customers to use easily, they will naturally seek human help and reassurance. Does it mean customers necessarily want ‘access to other humans’ for most of their banking transactions? No. What it does mean it that banks don’t have straightforward enough and easy-to-use systems.

So here I reiterate: branches are outdated. And, once again, it is both a curse and a blessing for banks. For now, it is a curse: the retail banking business of most (large) banks is plagued by an unsustainable cost/income ratio (often around 70%+ when it should be closer to 50). The internet revolution led banks to open websites but not to close branches: branches were still the primary medium through which they could attract depositors (hence funding). Having a branch near potential customers’ home was crucial in order to both obtain funding and revenues. Internet obviously changes everything. But with a lag. Young people quickly get used to utilising internet websites for shopping and banking, but don’t have the financial resources that drive banking revenues. On the other hand, older customers are much slower to keep up with the trend. Some of the very first internet banks, like UK’s Egg, were not as successful as expected as a result.

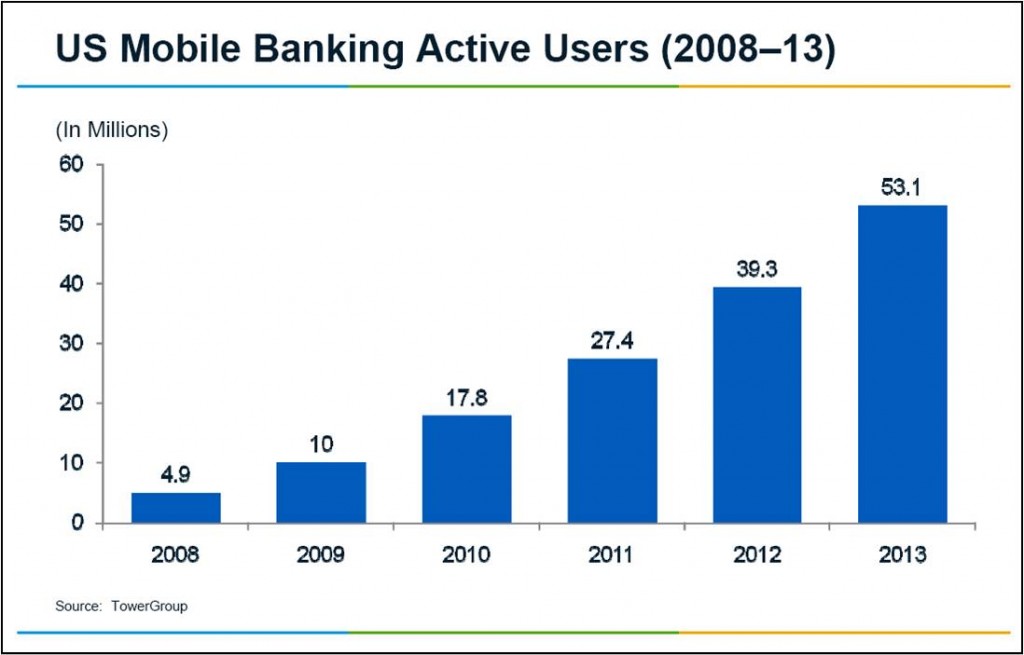

Now that mainstream internet use has been among us for around 15 years, much more customers use online services, including banking, and former early adopter but resource-poor students are now working professionals. Smartphones have compounded the trend. Brett King has extensively described the possible functions of a branch in the 21st century and documented the various trends in customer preferences in his Bank 2.0 and Bank 3.0 books. Mobile banking is booming and banks are at last starting to react. Over the last year, banks have followed each other in announcing reductions in their branch network, something that would have been unimaginable just a few years ago. In the US, banks are axing branches, the latest in line being Bank of America. In the UK, Barclays referred to branch closures as a ‘necessity’ at the end of last year. RBS and HSBC have also announced branch closures. In the rest of Europe, the trend is the same (see Belgian and French banks for instance). The other part of the curse is that banks do have to heavily invest in IT to catch up with the trend. And I am not even mentioning unions’ rejection of the branch axing plans, which indeed involve jobs cutting.

The blessing part of the story is that, while banks are constrained by increasing compliance costs and fall of revenues due to new regulations, smaller branch networks also means reduced cost bases. Bankers, desperate to improve their single-digit RoE can only welcome the change in the medium-term. More profitable banks also mean more flexible and more robust banks.

But. Some (most?) politicians don’t seem to get it. The UK’s Labour party came up with a brand new ‘brilliant’ idea to end the dominance of the largest retail banks of the country: a cap on the number (market share) of branches. As they are saying:

We are not asking whether existing banks might have to divest themselves of a significant number of branches. We are asking how we make that happen.

Well, you know what guys? It’s already happening. 21st century technological disruption does not require 20th century reasoning. Yet many professional politicians seem to have been blessed with the very skill of thinking using ‘previous century logic’. Politicians, please back away and let technology implement more efficient measures than anything you would have ever been able to plan.

PS: One of my (unrealistic at the moment) proposals was that alternative and independent interbank ‘superbranches’ could appear, gathering services/ATMs from all high-street banks under the same roof. This place would effectively be for banks what UK-based Carphone Warehouse and its competitors are for mobile phone providers. Banks would be a big step closer to being virtual service-providers and customers could potentially switch almost at will, intensifying competition. That would be a revolution.

PPS: Other technological disruptions I didn’t mention in the post were P2P-lending and associated services. This is also a big challenge but requires different responses, although some of the issues are interlinked.

- Chart 1: The Bankwatch, McKinsey

- Chart 2: McKinsey, The Triple Transformation, p. 33

- Chart 3: Mobility Enterprise

European banking resolution non-mechanism

The Financial Times and Zero Hedge had a pretty funny chart today describing the new mechanism to ‘resolve’ a failing bank, agreed yesterday by European ministers:

Zero Hedge calls this the “MinotEur Labyrinth”. As they say, good luck to them.

PS: I might talk about it in more details a later, when I have more time…

Cato Institute’s 31st Monetary Conference – Was the Fed a good idea?

About two weeks ago, the US-based think tank Cato organised its annual monetary conference. Great panels and very interesting speeches.

Three panels were of particular interest to me: panel 1 (“100 Years of the Fed: What Have We Learned?”), panel 2 (“Alternatives to Discretionary Government Fiat Money”), panel 3 (“The Fed vs. the Market as Bank Regulator”).

In panel 1, George Selgin destroys the Federal Reserve’s distorted monetary history. Nothing much new in what he says for those who know him but it just never gets boring anyway. He covers: some of the lies that the Federal Reserve tells the general public to justify its existence, pre-WW2 Canada and its better performing monetary system despite not having a central bank, the lack of real Fed independence from political influence and……the Fed not respecting Bagehot’s principles despite claiming to do so. In this panel, the speech of Jerry Jordan, former President of the Federal Reserve Bank of Cleveland, is also very interesting.

In panel 2, Larry White speaks about alternatives to government fiat money, counterfeiting laws and state laws making it illegal to issue private money. Scott Sumner describes NGDP level targeting. Here again, nothing really new for those who follow his blog, but interesting nonetheless (even though I don’t agree with everything) and a must see for those who don’t.

In panel 3, John Allison provides an insider view of regulators’ intervention in banking (he used to be CEO of BB&T, an American bank). He argues that mathematical risk management models provide unhelpful information to bankers. He would completely deregulate banking but increase capital requirements, which is an original position to say the least. Kevin Dowd’s speech is also interesting: he covers regulatory and accounting arbitrage (SPEs, rehypothecation…) and various banking regulations including Basel’s.

Overall, great stuff and you should watch the whole of it (I know, it’s long… you can probably skip most Q&As).

PS: Scott Sumner also commented on the Pope’s speech on “evil incarnate”. Reminds me of the vocabulary I used…

News digest (Krugman and deregulation, central banking for Bitcoin…)

A looooooooot of news since the beginning of the week. So I’ll just quickly go over a few of them. Guys please, next time, spread your news more evenly over time. There was nothing to comment on recently!

Not new news but the Swedish bank regulators are thinking of increasing RWAs on mortgages to fight a growing housing bubble. Well, raising them to 25% (from 15% floor…) would still not change much: they would remain below most other asset classes’ level and securitisation (RMBS) would allow banks to bypass the restrictions.

Meanwhile, Yves Mersch, member of the Executive Board of the ECB, spoke about how to revive SME lending in bank-reliant Europe. His solutions involve: strengthening banks, securitisation and… banking union. Any word of capital requirements/risk-weighted assets? Not a single one. When I told you that central bankers don’t seem to get it…

But the UK government wants to ditch the household lending side of the Funding for Lending Scheme! They now only want to provide cheap funding to banks if they prove that they lend to SMEs. Why not, but I doubt it would really work for a few reasons: 1. demand for loans remains quite low, 2. market funding remains cheap (it was cheaper than FLS), 3. banks haven’t drawn much on it anyway, 4. RWAs are still in place! Mortgage and household lending will still attract most of lending volume as it is more profitable from a capital point of view.

Meanwhile (again), SME financing from alternative lenders not subject to RWAs and other stupid capital rules, keeps growing in the UK. However, it is still tough for those lenders to assess the health of the companies that would like to lend to.

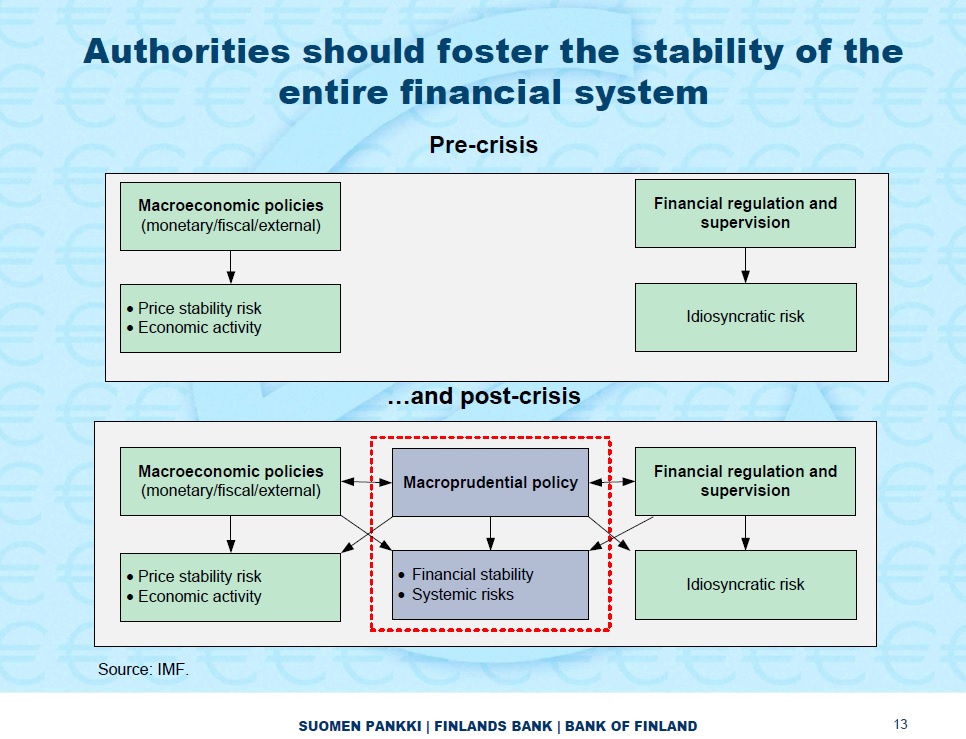

Erkki Liikanen, the Governor of the central bank of Finland, told us about his ideas to improve financial stability. Surprise: they haven’t changed. So macroprudential policy starts interfering with macroeconomic policies and financial regulation, with possibly opposite effects that don’t seem to bother him much. Look at that slide, which is the very definition of a messy policy goal, with multiple targets and interferences:

A very strange piece in the Washington Post: Bitcoin needs a central banker. Wait a second. No, it’s definitely not the 1st of April. First, the author asserts that Bitcoin’s wild changes in value make it difficult to be adopted as a currency. This is extraordinary. Does the author even understand FX rates? If the author wishes to purchase his coffee using Euros, despite the coffee being priced in Dollars, will he also declare that the fact the Euro’s value is unstable (making the effective Euro price of its coffee volatile) makes the currency improper for use? When prices are originally denominated in Bitcoin, the change in the value of the digital currency won’t affect them. When prices are actually denominated in USD, but converted into Bitcoin, then yes, changes in the value of the digital currency will affect them. But this is hardly Bitcoin’s fault… Then he gets mixed up with ‘menu costs’, ‘hyperinflation’, ‘money demand’, etc. Wow. Just one last thing: has he even understood that Bitcoin was designed to be free from central bankers and government intervention in the first place?

Izabella Kaminska in the FT wrote a new piece on Bitcoin and other alternative electronic currencies. She complains about the multiplication of such currencies that nothing backs and pretty much only see speculative motivations underlying them. I am not going to comment on the whole thing, but whether right or wrong, she should ask herself why there is such frenzy about those currencies at the moment. My guess is that, governments’ and central banks’ manipulation of their own currencies have unleashed a beast: people afraid to hold classic currencies started to look for alternatives, pushing up their prices, in turn attracting speculators. The process is similar to ‘bad’ financial innovations (the ones designed specifically to bypass restricting regulation): they often start as a benign innovation for the ‘common good’, but the surprising demand for them and large profits attract speculators until the market crashes. Not the fault of the innovation, but the fault of the regulation that triggered them…

Paul Krugman thinks that “the trouble with economics is economists”, and that mainstream economics is not to blame for the financial crisis. I partly disagree: 1. there are various schools of thought within mainstream economics that often disagree with each other altogether and 2. most (all?) of them cannot fully explain the crisis anyway. But, and this is where Krugman shows his limited knowledge of banking and therefore the limit of his reasoning, he declares that “the mania for financial deregulation, for example, didn’t come out of standard economic analysis.” I’m sorry? Which mania for financial deregulation? The international banking sector had never been as regulated in history as on the eve of the crisis! (even taking into account of the few one-off deregulations) I need to come back to this in a subsequent post. Really, Paul, you have to revise your history. And your reasoning.

On Free Banking, George Selgin urges Scots to ‘poundize’ unilaterally if ever they declare independence from the UK. And “if the British Parliament refuses to cooperate, so much the better. Who knows: Scotland could even end up with a banking system as good as the one it had before 1845, when Parliament, which knew almost as little about currency then as it does now, began to bugger it up.” If only Scotland could enlighten the world a second time and get back to a free banking system!

The ivory tower economist syndrome

Here we go. Academic economists are lost. Lawrence Summers just made a striking announcement in a speech a few days ago: we are likely to be in a secularly stagnating economy that needs recurrent bubbles to achieve full employment, as its natural rate of interest has been constantly below zero for a while. Evidently, Krugman, Sumner, Cowen, Wolf and many other economists started to discuss the issue. Some agree, some don’t. However, most seem to miss the main problem. I call that the ivory tower economist syndrome. Abstractly thinking in terms of aggregated economic figures locked in a university or government office won’t be of much help. Zerohedge rightly makes fun of Summers and Krugman, as the satiric newspaper The Onion made the same economic advices a few years ago:

Congress is currently considering an emergency economic-stimulus measure, tentatively called the Bubble Act, which would order the Federal Reserve to† begin encouraging massive private investment in some fantastical financial scheme in order to get the nation’s false economy back on track.

Who said that was fiction?

Many of them are backing their ideas using wrong arguments. For instance, Summers and Krugman don’t believe interest rates were too low before the crisis as… there was no inflation! Sure, but, how do you know that? CPI? RPI? GDP deflator? There are many problems with inflation figures. Let’s list some of them:

- They don’t accurately reflect inflation. You can change the calculation and the result changes dramatically. Moreover, the goods picked to calculate them and the weights applied to them are quite arbitrary. This is supposed to reflect the ‘average’ household basket. Well, I am not the average household apparently as my own inflation rate has been way higher than headline inflation over the past few years.

- 0% CPI increase does not mean that there is no inflation. Productivity increase drives inflation down. As a result, reasoning in terms of headline inflation is a mistake. Real inflation is hidden. The fastest economic growth in the history of the Western world (late 19th and early 20th century) occurred during a long period of secular deflation…

- Most asset prices aren’t reflected in inflation figures. Newly created money now mostly go to investments, a lot of which being speculation. Most of banks’ lending is mortgage lending. So newly-created money goes to housing, pushing up prices… which aren’t reflected in inflation figures. Sure, one can argue that, at some point, there will be inflationary pressure on consumer goods. But productivity increases reducing the price of domestically-produced goods (IT revolution anyone?) and cheap goods from developing countries mask that process. Moreover, when asset bubbles burst (which they eventually do), the wealth effect from asset price increases that could lead to inflation all but disappears. Lending was also different 50 or 100 years ago: much lending did not go directly to investments in financial or real assets. Consequently consumer goods inflation appeared a lot faster after new monetary injection (considering stable productivity).

So justifying the fact that nominal interest rates defined by central banks were not low because there was no inflation is in itself wrong, or at best inaccurate. In reality, low interest rates are very likely to have caused, or at least participated, in the recent credit bubble. Regarding the so-called ‘savings glut’, Cowen agrees with Kling on the fact that, if we really had ‘too much’ savings chasing ‘too few’ investment opportunities, we would not need central banks’ actions to push interest rates lower. The supply and demand of loanable funds would automatically drive the interest rate to a very low level.

But, most importantly, all those economists forget a fundamental fact that I have been mentioning a hundred times recently: regime uncertainty (yes, again…). For economists to speak in terms of monetary and spending aggregates alone and to not pay attention to the broader context surrounding businesses is a major mistake. I’ve kept repeating and giving many evidences recently (like here, here, and here) that businesses currently delay investments due to the uncertain regulatory and economic decisions taken by governments and regulators all around the world. This is now the major issue for SMEs and banks at least. Again today, Euromoney published an interesting short article on ‘renewed regulatory uncertainty’ for banks:

For all the populist fervor then about perceived policy inaction to address systemic risk, many banks see it differently: investor flight from banks’ equity and bond products has taken root over the years, amid fears that new rules will render business models uneconomic.

Take a look at that SEB and Deloitte chart summarising current regulatory reforms. It looks slightly messy doesn’t it? And look how it is named…

A bank analyst told Euromoney that:

Changes in regulations, changes in what other stakeholders consider to be acceptable, the risk that the behaviours of certain employees become associated with the institution as a whole – those are indeed much more expensive for banks these days than credit [risk].

As I have already highlighted in an earlier post, more than the number of rules, it is the fact that rules change that is crucial to business planning. You can’t play a certain game if the rules of the game constantly change. Yet none of those ‘great’ economists ever mentioned regulation, uncertainty, rules or anything related. Looks like abstract economic aggregates are a lot more interesting to manipulate…

Get out of your tower guys!

A few complementary notes on regime uncertainty

Not much about finance or banking today. I just wanted to come back to a few concepts I mentioned in earlier posts (like here, here and here), such as regulatory regime uncertainty.

We keep hearing economists, journalists and politicians complaining about companies not investing ‘enough’ at the moment. Keynesians like Krugman, de Long and co, and some other non-Keynesian mainstream economists think that the main underlying reason to this phenomenon is lack of demand. I argued several times that, while demand fell probably too low in 2009, one of the other main culprits since then had been regime uncertainty: regulations keep changing and red tape expanding, leading most firms to postpone their various investments and projects until they have a clearer view of the rules going forward.

The Economist’s Buttonwood’s blog had a post about business regulation two days ago, which led me to look for some evidence that increasing (and uncertain) regulation was negatively impacting investments. I found this US Chamber of Commerce Small Business Study, which is enlightening. What it reveals:

- 44% of SME owners ranked economic uncertainty as their number 1 worry (with over-regulation at number 3, or 39%, and high taxes number 4, or 37%). To be fair, economic uncertainty also comprises demand uncertainty. But read the rest first.

- Only 24% indicated that they thought that business climate for SME had improved over the last couple of years.

- 42% of SME owners ranked the US growing deficit and debt as number 2 worry.

- “Seventy-eight percent of small business owners said that the U.S. deficit and debt pose a threat to the success of their businesses. The current federal debt and deficit (40%) and the regulations coming out of Washington (35%) are the top two current issues coming out of Washington that cause concern about the future of their businesses. In addition, sentiment is strong that the climate for small businesses is worse than under the previous administration (80%).”

- “The majority of small business owners, when asked what they need most from Washington right now, would like Washington to get out of the way (84%) as opposed to lending a helping hand (11%). When asked about specific actions they needed from Washington, overwhelmingly small business owners wanted more certainty (87%).”

- “Government regulations on small businesses continue to be seen as unreasonable (73%) by small business owners with a two thirds majority (66%) saying that what Washington will do next to small businesses scares them most.”

Right. It’s kind of a proof, isn’t it? This is also applicable to banks: giving God-like powers to regulators (or anyone) is usually not a good idea. Uncertainty is everywhere in the banking world. Just look at the latest Swiss news: a top official announced that, perhaps, Swiss banks will be subject to a very high 10% leverage ratio. Or perhaps just 6%. Or in between. Or possibly not at all. Or…well, they’re gonna discuss and let you know later. How can any bank plan for the future and lend in such conditions?

On a side not, I am wondering whether or not increasing red tape is linked to The Decline of Creative Destruction, as this Bryan Caplan piece was named today. Surely it is. Very interesting chart anyway (see below). Job destructions during the crisis were actually at the same level as they were throughout the 1990’s… It would be interesting to compare this chart to the evolution of business red tape. Unfortunately, this isn’t my area, so I’ll let you do it!

What Walter Bagehot really said in Lombard Street (and it’s not nice for central bankers and regulators)

(Warning: this is quite a long post as I reproduce some parts of Bagehot’s writings)

As I promised in a post a few days ago, I am today getting back to the common ancestor of all of today’s central bankers, Walter Bagehot.

Bagehot is probably one of the most misquoted economist/businessmen of all times. Most people seem to think they can just cherry pick some of his claims to justify their own beliefs or policies, and leave aside the other ones. Sorry guys, it doesn’t work like that. Bagehot’s recommendations work as a whole. Here I am going to summarise what Bagehot really said about banking and regulation in his famous book Lombard Street: A description of the Money Market.

Let’s start with central banking. As I’ve already highlighted a few days ago, Bagehot said that the institution that holds bank reserves (i.e. a central bank) should:

- Lend freely to solvent banks and companies

- Lend at a punitive rate of interest

- Lend only against good quality collateral

I can’t recall how many times I’ve heard central bankers, regulators and journalists repeating again and again that “according to Bagehot” central banks had to lend freely. Period. Nothing else? Nop, nothing else. Sometimes, a better informed person will add that Bagehot said that central banks had to lend to solvent banks only or against good collateral. Very high interest rates? No way. Take a look at what Mark Carney said in his speech last week: “140 years ago in Lombard Street, Walter Bagehot expounded the duty of the Bank of England to lend freely to stem a panic and to make loans on “everything which in common times is good ‘banking security’.”” Typical.

Now hold your breath. What Bagehot said did not only involve central banking in itself but also the banking system in general, as well as its regulation. Bagehot attacked…regulatory ratios. Check this out (chapter 8, emphasis mine):

But possibly it may be suggested that I ought to explain why the American system, or some modification, would not or might not be suitable to us. The American law says that each national bank shall have a fixed proportion of cash to its liabilities (there are two classes of banks, and two different proportions; but that is not to the present purpose), and it ascertains by inspectors, who inspect at their own times, whether the required amount of cash is in the bank or not. It may be asked, could nothing like this be attempted in England? could not it, or some modification, help us out of our difficulties? As far as the American banking system is one of many reserves, I have said why I think it is of no use considering whether we should adopt it or not. We cannot adopt it if we would. The one-reserve system is fixed upon us.

Here Bagehot refers to reserve requirements, and pointed out that banks in the US had to keep a minimum amount of reserves (i.e. today’s equivalent would be base fiat currency) as a percentage of their liabilities (= customer deposits) but that it did not apply to Britain as all reserves were located at the Bank of England and not at individual banks (the US didn’t have a central bank at that time). He then follows:

The only practical imitation of the American system would be to enact that the Banking department of the Bank of England should always keep a fixed proportion—say one-third of its liabilities—in reserve. But, as we have seen before, a fixed proportion of the liabilities, even when that proportion is voluntarily chosen by the directors, and not imposed by law, is not the proper standard for a bank reserve. Liabilities may be imminent or distant, and a fixed rule which imposes the same reserve for both will sometimes err by excess, and sometimes by defect. It will waste profits by over-provision against ordinary danger, and yet it may not always save the bank; for this provision is often likely enough to be insufficient against rare and unusual dangers.

Bagehot thought that ‘fixed’ reserve ratios would not be flexible enough to cope with the needs of day-to-day banking activities and economic cycles: in good times, profits would be wasted; in bad times, the ratio is likely not to be sufficient. Then it gets particularly interesting:

But bad as is this system when voluntarily chosen, it becomes far worse when legally and compulsorily imposed. In a sensitive state of the English money market the near approach to the legal limit of reserve would be a sure incentive to panic; if one-third were fixed by law, the moment the banks were close to one-third, alarm would begin, and would run like magic. And the fear would be worse because it would not be unfounded—at least, not wholly. If you say that the Bank shall always hold one-third of its liabilities as a reserve, you say in fact that this one-third shall always be useless, for out of it the Bank cannot make advances, cannot give extra help, cannot do what we have seen the holders of the ultimate reserve ought to do and must do. There is no help for us in the American system; its very essence and principle are faulty.

To Bagehot, requirements defined by regulatory authorities were evidently even worse, whether for individual banks or applied to a central bank. I bet he would say the exact same thing of today’s regulatory liquidity and capital ratios, which are essentially the same: they can potentially become a threshold around which panic may occur. As soon as a bank reaches the regulatory limit (for whatever reason), alarm would ring and creditors and depositors would start reducing their lending and withdrawing their money, draining the bank’s reserves and either creating a panic, or worsening it. This reasoning could also be applied to all stress tests and public shaming of banks by regulators over the past few years: they can only make things worse.

Even more surprising: the spiritual leader of all of today’s central bankers was actually…against central banking. That’s right. Time and time again in Lombard Street he claimed that Britain’s central banking system was ‘unnatural’ and only due to special privileges granted by the state. In chapter 2, he said:

I shall have failed in my purpose if I have not proved that the system of entrusting all our reserve to a single board, like that of the Bank directors, is very anomalous; that it is very dangerous; that its bad consequences, though much felt, have not been fully seen; that they have been obscured by traditional arguments and hidden in the dust of ancient controversies.

But it will be said—What would be better? What other system could there be? We are so accustomed to a system of banking, dependent for its cardinal function on a single bank, that we can hardly conceive of any other. But the natural system—that which would have sprung up if Government had let banking alone—is that of many banks of equal or not altogether unequal size. In all other trades competition brings the traders to a rough approximate equality. In cotton spinning, no single firm far and permanently outstrips the others. There is no tendency to a monarchy in the cotton world; nor, where banking has been left free, is there any tendency to a monarchy in banking either. In Manchester, in Liverpool, and all through England, we have a great number of banks, each with a business more or less good, but we have no single bank with any sort of predominance; nor is there any such bank in Scotland. In the new world of Joint Stock Banks outside the Bank of England, we see much the same phenomenon. One or more get for a time a better business than the others, but no single bank permanently obtains an unquestioned predominance. None of them gets so much before the others that the others voluntarily place their reserves in its keeping. A republic with many competitors of a size or sizes suitable to the business, is the constitution of every trade if left to itself, and of banking as much as any other. A monarchy in any trade is a sign of some anomalous advantage, and of some intervention from without.

As reflected in those writings, Bagehot judged that the banking system had not evolved the right way due to government intervention (I can’t paste the whole quote here as it would double the size of my post…), and that other systems would have been more efficient. This reminded me of Mervyn King’s famous quote: “Of all the many ways of organising banking, the worst is the one we have today.” Another very interesting passage will surely remind my readers of a few recent events (chapter 4):

And this system has plain and grave evils.

1st. Because being created by state aid, it is more likely than a natural system to require state help.

[…]

3rdly. Because, our one reserve is, by the necessity of its nature, given over to one board of directors, and we are therefore dependent on the wisdom of that one only, and cannot, as in most trades, strike an average of the wisdom and the folly, the discretion and the indiscretion, of many competitors.

Granted, the first point referred to the Bank of England. But we can easily apply it to our current banking system, whose growth since Bagehot’s time was partly based on political connections and state protection. Our financial system has been so distorted by regulations over time than it has arguably been built by the state. As a result, when crisis strikes, it requires state help, exactly as Bagehot predicted. The second point is also interesting given that central bankers are accused all around the world of continuously controlling and distorting financial markets through various (misguided or not) monetary policies.

For all the system ills, however, he argued against proposing a fundamental reform of the system:

I shall be at once asked—Do you propose a revolution? Do you propose to abandon the one-reserve system, and create anew a many-reserve system? My plain answer is that I do not propose it. I know it would be childish. Credit in business is like loyalty in Government. You must take what you can find of it, and work with it if possible.

Bagehot admitted that it was not reasonable to try to shake the system, that it was (unfortunately) there to stay. The only pragmatic thing to do was to try to make it more efficient given the circumstances.

But what did he think was a good system then? (chapter 4):

Under a good system of banking, a great collapse, except from rebellion or invasion, would probably not happen. A large number of banks, each feeling that their credit was at stake in keeping a good reserve, probably would keep one; if any one did not, it would be criticised constantly, and would soon lose its standing, and in the end disappear. And such banks would meet an incipient panic freely, and generously; they would advance out of their reserve boldly and largely, for each individual bank would fear suspicion, and know that at such periods it must ‘show strength,’ if at such times it wishes to be thought to have strength. Such a system reduces to a minimum the risk that is caused by the deposit. If the national money can safely be deposited in banks in any way, this is the way to make it safe.

What Bagehot described is a ‘free banking’ system. This is a laissez faire-type banking system that involves no more regulatory constraints than those applicable to other industries, no central bank centralising reserves or dictating monetary policy, no government control and competitive currency issuance. No regulation? No central bank to adequately control the currency and the money supply and act as a lender of last resort? No government control? Surely this is a recipe for disaster! Well…no. There have been a few free banking systems in history, in particular in Scotland and Sweden in the 19th century, to a slightly lesser extent in Canada in the 19th and early 20th, and in some other locations around the world as well. Curiously (or not), all those banking systems were very stable and much less prone to crises than the central banking ones we currently live in. Selgin and White are experts in the field if you want to learn more. If free banking was so effective, why did it disappear? There are very good reasons for that, which I’ll cover in a subsequent post on the history of central banking.

I am not claiming that Bagehot held those views for his entire life though. A younger Bagehot actually favoured monopolised-currency issuance and the one-reserve system he decried in his later life. I am not even claiming that everything he said was necessarily right. But Bagehot as a defender of free banking and against regulatory requirements of all sort is a far cry from what most academics and regulators would like us to believe today. Personally, I find that, well, very ironic.

Should the Bank of England have tools to prick property bubbles?

The answer is no. (but not according to this FT article)

Wait… Actually, it already has tools: it’s called monetary policy. Place the interest rate at the right level and stop massively injecting cash in the economy and, perhaps, you won’t witness real estate bubbles?

There are other hugely distorting UK government policies at the moment: the Funding-for-Lending scheme and the more recent Help-to-Buy, which both push demand for property up through artificially low interest rates. I’ll explain that in details in another post.

So the question becomes: why adding other distorting tools (whether ‘macroprudential‘ or ‘microprudential‘) and policies, such as maximum loan-to-value or loan-to-income ratios, on top of already deficient tools and policies? I have another suggestion: why not trying to correct the failings of the first layer of policies? Just saying.

PS: Lord Turner is obviously mentioned in this FT article.

Recent Comments