BoE’s Mark Carney is burying Walter Bagehot a second time

Banks were partying on Thursday. Mark Carney, the new governor of the Bank of England, decided to ‘relax’ rules that had been put in place by its predecessor, Mervyn King. From now on, the BoE will lend to banks (as well as non-bank financial institutions) for longer maturities, accept less quality collateral in exchange, and lower the interest rate on/cost off those facilities. Mervin King was worried about ‘moral hazard’. Mark Carney has no idea what that means.

According to the FT, Barclays quickly figured out what this move implied: “it reduces the need for, and the cost of, holding large liquidity buffers.” Just wow. So, while we’ve just experienced a crisis during which some banks collapsed because they didn’t hold enough liquid assets on their balance sheet as they expected central banks and governments to step in if required, Carney’s move is expected to make the banks hold……even less liquidity.

It’s obviously nothing to say that this goes against every possible piece of regulation devised over the last few years. While the regulators were right in thinking that banks needed to hold more liquid assets, they took on the wrong problem: it was government and central bank support that brought about low liquidity holdings, and not free-markets recklessness. Anyway, Carney’s move kind of undermines that effort and risks rewarding mismanaged banks at the expense of safer ones.

Carney’s decision also goes against all the principles devised by the ‘father’ of central banking: Walter Bagehot. I guess it is time to decipher Bagehot, as he has been constantly misquoted since the start of the crisis by people who have apparently never read him. As a result he was used to justify what were actually anti-Bagehot policies. Bagehot’s principles are underlined in his famous book Lombard Street, written in 1873. What should a central bank do during a banking crisis? According to Bagehot (as described in chapters 2, 4 and 7), it should:

- Lend freely to solvent banks and companies

- Lend at a punitive rate of interest

- Only accept good quality collateral in exchange

For instance, in chapter 2:

The holders of the cash reserve must be ready not only to keep it for their own liabilities, but to advance it most freely for the liabilities of others. They must lend to merchants, to minor bankers, to ‘this man and that man,’ whenever the security is good.

In chapter 7:

First. That these loans should only be made at a very high rate of interest. This will operate as a heavy fine on unreasonable timidity, and will prevent the greatest number of applications by persons who do not require it. The rate should be raised early in the panic, so that the fine may be paid early; that no one may borrow out of idle precaution without paying well for it; that the Banking reserve may be protected as far as possible.

Secondly. That at this rate these advances should be made on all good banking securities, and as largely as the public ask for them. The reason is plain. The object is to stay alarm, and nothing therefore should be done to cause alarm. But the way to cause alarm is to refuse some one who has good security to offer… No advances indeed need be made by which the Bank will ultimately lose.

No central bank applied Bagehot’s recommendations during the financial crisis. Granted, given the organisation of today’s financial system, it is difficult for central bank to lend to non-financial firms. Nonetheless, it took them a little while to start lending freely and lent to insolvent banks as well. They also started to accept worse quality collateral than what they used to (think about the Fed now purchasing mortgage/asset-backed securities for example). Finally, central banks have never charged a punitive rate on their various facilities. Quite the contrary: interest rates were pushed down as much as humanly possible on all normal and exceptional refinancing facilities.

While the ECB and the Fed have made clear that some of those were temporary measures, Carney now seems to imply that, not only are they here to stay, but they also will be extended in non-crisis times. He calls that being “open for business”. Poor Bagehot must be turning in his grave right now.

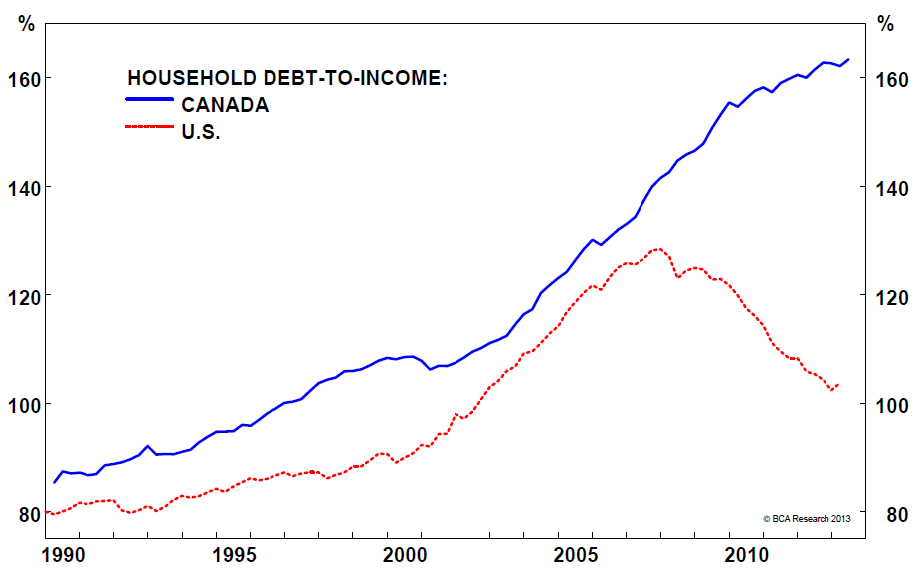

According to Carney, those measures will reinforce financial stability. Really? So no moral hazard involved? no bank taking unnecessary risks because it knows that the BoE has its back? If Mervyn King didn’t do everything perfectly while in charge, at least he had a point. Carney, after overseeing a large credit bubble in Canada over the past few years (he first joined the Bank of Canada in 2003, then rejoined it as Governor in 2008), is now applying his brilliant recipe to the UK.

I think that Carney’s decisions introduce considerable incentive distortions in the banking system. This is clearly not what a free-market should look like. In any case, if a new crisis strikes as a result, I am pretty sure that laissez-faire will be blamed again. It is ironic to see that some of those central bankers destroy faith in free-markets while trying to protect them.

Bagehot also said other things that go against the principles driving our current banking and regulatory system. More details in another post!

Photograph: Reuters/Bloomberg

Chart: The Big Picture

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

Trackbacks / Pingbacks