The Economist declares that financial crises are due to…

The Economist surprised me this week. In a good way.

Over the past few years, the newspaper’s main rhetoric has been that the financial system needed to be more regulated. From time to time, the ancient roots of the venerable newspaper seemed to make a comeback to denounce the increasing red tape that financial businesses were now subject to. But overall, The Economist seemed to have been partly taken over by statist fever and the general editorial line was: regulation and inflation will be the saviours of our capitalist system. Unsurprisingly, I tended to disagree (euphemism spotted).

When this week The Economist decided to publish two articles under the umbrella title of A History of Finance in Five Crises, and How the Next One Could be Prevented (see here and here), I was very sceptical. I was indeed expecting the usual arguments that bankers try to abuse the system, that regulation is necessary to prevent those abuses, that more central bank control of the financial system is a good thing, that financial innovations should be regulated out of existence.

I was plain, delightfully, wrong.

This is The Economist:

Whatever was wrong with the American housing market, it was not lack of government: far from a free market, it was one of the most regulated industries in the world, funded by taxpayer subsidies and with lending decisions taken by the state.

Amen.

In a very timely and remarkable echo to my very recent post on the obsession of financial stability, the newspaper also pointed out the risk of too much protection:

The more the state protected the system, the more likely it was that people in it would take risks with impunity.

[…] In many cases the rationale for the rules and the rescues has been to protect ordinary investors from the evils of finance. Yet the overall effect is to add ever more layers of state padding and distort risk-taking.

This fits an historical pattern. As our essay this week shows, regulation has responded to each crisis by protecting ever more of finance. Five disasters, from 1792 to 1929, explain the origins of the modern financial system. This includes hugely successful innovations, from joint-stock banks to the Federal Reserve and the New York Stock Exchange. But it has also meant a corrosive trend: a gradual increase in state involvement.

The newspaper even attacked… deposit insurance! Blasphemy! To tell you the truth, I still find it hard to believe:

The numbers would amaze Bagehot. In America a citizen can now deposit up to $250,000 in any bank blindly, because that sum is insured by a government scheme: what incentive is there to check that the bank is any good?

[…] Today America is an extreme case, but insurance of over $100,000 is common in the West. This protects wealth, and income, and means investors ignore creditworthiness, worrying only about the interest-rate offer, sending deposits flocking to flimsy Icelandic banks and others with pitiful equity buffers.

[…] How can the zombie-like shuffle of the state into finance be stopped? Deposit insurance should be gradually trimmed until it protects no more than a year’s pay, around $50,000 in America. That is plenty to keep the payments system intact. Bank bosses might start advertising their capital ratios, as happened before deposit insurance was introduced.

Those are two brilliant articles. Personally, I find that very encouraging. It means that my blog, as well as the work of the very few people who think like me, aren’t pointless.

Dear Economist, welcome back.

(and please stay with us this time)

Some ‘good’ principles of financial regulation

Readers of this blog know the extent of my love for banking regulation. I love regulation. I really do. Otherwise I wouldn’t have much to write about.

Irony aside, I recently read a very good paper by Calomiris (Financial Innovation, Regulation, and Reform, 2009, which you can find here) that made me give regulation a rethink (to be frank, I was disappointed that there’s not much about financial innovation in this paper, but the rest is pretty good).

Calomiris is a free-market guy. He makes it clear is most of his papers, this one included:

The risk-taking mistakes of financial managers were not the result of random mass insanity; rather they reflected a policy environment that strongly encouraged financial managers to underestimate risk in the subprime mortgage market. Risk-taking was driven by government policies; government’s actions were the root problem, not government inaction.

He is right. But he also seems to be a ‘realist’ (if ever this really means anything). He considers that, given our current distortive institutional framework, the best thing we can do is to mitigate its effect through proper regulation. He writes:

If there were no governmental safety nets, no government manipulation of credit markets, no leverage subsidies, and no limitations on the market for corporate control, one could reasonably argue against the need for prudential regulation. Indeed, the history of financial crises shows that in times and places where government interventions were absent, financial crises were relatively rare and not very severe.

[…But] it is not very helpful to suggest only regulatory changes that are very far beyond the feasible bounds of the current political environment. […] Absent the elimination of [all the policies described above], government prudential regulation is a must.

In a way, he has a point. Whereas I’d like to see the implementation of a free banking system, I also have to admit that this possibility is pretty unlikely to ever reoccur (unless a once in a thousand years financial collapse suddenly strikes). Which led me to think about a ‘second best’. This ‘second best’ solution should follow the principles I described here (where I argued in favour of a stable rule set and regulatory framework) and here (where I agreed with Lars Christensen and John Cochrane and argued against macro-prudential regulations). This is what I wrote:

Stable rules are a fundamental feature of intertemporal coordination between savers and borrowers, between investors and entrepreneurs. In order for economic agents to (more or less) accurately plan for the future, for entrepreneurs to develop their business ideas and anticipate future demand, for savers to invest their money and know that their property rights are not going to disappear overnight and accordingly plan their own delayed consumption and provide entrepreneurs with directly available funds, the economic system needs a stable and predictable rule framework. Production and investments take time and as a result involve uncertainty, which should not be exacerbated by an instable rule set. The rule of law is part of this framework. Monetary policy, financial regulation and government policies should follow the same pattern, instead of being discretionary.

What I am about to describe is a non-exhaustive list of ‘good’ principles of regulation that fit (to an extent) a free-market framework. I may update the list over time. Following the principles above, and even though not perfect, a ‘second best’ solution would have to be:

- As least distortive as possible (i.e. introducing as few loopholes and incentives to game the rules as possible)

- As stable as possible (i.e. no discretionary powers), and

- As simple, transparent and clear as possible (i.e. a few clear and straightforward rules are better than a multitude of obscure and complex ones)

On the monetary policy side, despite its flaws, NGDP targeting seems to be the only ‘easily implementable’ policy that meets the three criteria. I won’t discuss it here (see The Money Illusion, The Market Monetarist, Worthwhile Canadian Initiative, and many other blogs for more information). On the slightly ‘less easily implementable’ side, the ‘productivity norm’ would nonetheless be an even better alternative (see George Selgin’s implementation here, from page 64 onwards).

What about financial and banking regulation? In order to respect the three fundamental rules described above, regulators should:

- Define few transparent, straightforward limits and ratios based on objective and easily measurable criteria that are neither pro- nor counter-cyclical

- Not impose their own perception of risk to the market

- Not vary regulatory limits and requirements over time

- Not publicly shame financial institutions that respect regulatory requirements even if borderline-compliant: the regulators’ role is to make sure that institutions respect the requirements, period

- Publicly make clear that regulations only represent minimums, that regulators are only here to make those minimums respected, and that it is the role of market actors to identify stronger from weaker institutions within those regulatory-defined limits

- Not interfere with financial institutions’ strategy and internal organisational structures: harmonising business models takes the risk of weakening the whole system

- Refrain from making any comment unrelated to the (non)compliance of institutions to regulatory requirements

- Allow the market process to run its course and not institutionalise moral hazard by implementing bailout and other backstop mechanisms

Banking regulation is divided into micro-prudential and macro-prudential regulation. The former provides individual banks with rules they have to respect at all times, independently of the performance of the whole economy. The latter provides all banks with rules that vary according to the state of the economy, independently of the performance of each bank. Following the principles above, fixed and straightforward sets of micro-prudential regulations may be acceptable. On the other hand, most macro-prudential regulations would be eliminated given their discretionary component and their variability over time. It is indeed very hard for regulators to identify bubbles and other excesses (see White, 2011, here). They have a poor track record at it. Discretion could well prevent a bubble from growing too much but it could also prevent a genuinely growing market to reach its full potential. Regulators suffer from the central planner’s problem. As Hayek said in his essay The Use of Knowledge in Society:

The peculiar character of the problem of a rational economic order is determined precisely by the fact that the knowledge of the circumstances of which we must make use never exists in concentrated or integrated form, but solely as the dispersed bits of incomplete and frequently contradictory knowledge which all the separate individuals possess.

I can already hear the rebuttals: “but counter-cyclical macro-prudential policies would help mitigate the bust after the boom!” To which I would respond: “how do you identify a ‘boom’?” For a bust to occur, a boom must be unsustainable. Solid and sustainable growth may well happen and should not be interfered with by counter-cyclical regulations that would in fact not be counter-cyclical at all in this case. Nominal stability is primarily the role of monetary policy, which should promote a stable framework to the real economy. An unsustainable boom is likely to emanate from nominal instability. The goal of regulation is not to mitigate the effects of destabilising monetary policies.

Of course, this does not mean that one should not strive to reduce political and regulatory distortions. ‘Idealists’ (if ever this also means anything) are a necessary part of a healthy democratic process. Moreover, too much compromise can be dangerous: where to fix the limit? Because the very distortive sources are still present, crises can still occur and provide extra arguments to further expand the regulatory burden.

PS: I’ll provide examples of regulations that comply or not with those principles in a subsequent post. This post would have been too long otherwise!

Cato Institute’s 31st Monetary Conference – Was the Fed a good idea?

About two weeks ago, the US-based think tank Cato organised its annual monetary conference. Great panels and very interesting speeches.

Three panels were of particular interest to me: panel 1 (“100 Years of the Fed: What Have We Learned?”), panel 2 (“Alternatives to Discretionary Government Fiat Money”), panel 3 (“The Fed vs. the Market as Bank Regulator”).

In panel 1, George Selgin destroys the Federal Reserve’s distorted monetary history. Nothing much new in what he says for those who know him but it just never gets boring anyway. He covers: some of the lies that the Federal Reserve tells the general public to justify its existence, pre-WW2 Canada and its better performing monetary system despite not having a central bank, the lack of real Fed independence from political influence and……the Fed not respecting Bagehot’s principles despite claiming to do so. In this panel, the speech of Jerry Jordan, former President of the Federal Reserve Bank of Cleveland, is also very interesting.

In panel 2, Larry White speaks about alternatives to government fiat money, counterfeiting laws and state laws making it illegal to issue private money. Scott Sumner describes NGDP level targeting. Here again, nothing really new for those who follow his blog, but interesting nonetheless (even though I don’t agree with everything) and a must see for those who don’t.

In panel 3, John Allison provides an insider view of regulators’ intervention in banking (he used to be CEO of BB&T, an American bank). He argues that mathematical risk management models provide unhelpful information to bankers. He would completely deregulate banking but increase capital requirements, which is an original position to say the least. Kevin Dowd’s speech is also interesting: he covers regulatory and accounting arbitrage (SPEs, rehypothecation…) and various banking regulations including Basel’s.

Overall, great stuff and you should watch the whole of it (I know, it’s long… you can probably skip most Q&As).

PS: Scott Sumner also commented on the Pope’s speech on “evil incarnate”. Reminds me of the vocabulary I used…

BoE’s Mark Carney is burying Walter Bagehot a second time

Banks were partying on Thursday. Mark Carney, the new governor of the Bank of England, decided to ‘relax’ rules that had been put in place by its predecessor, Mervyn King. From now on, the BoE will lend to banks (as well as non-bank financial institutions) for longer maturities, accept less quality collateral in exchange, and lower the interest rate on/cost off those facilities. Mervin King was worried about ‘moral hazard’. Mark Carney has no idea what that means.

According to the FT, Barclays quickly figured out what this move implied: “it reduces the need for, and the cost of, holding large liquidity buffers.” Just wow. So, while we’ve just experienced a crisis during which some banks collapsed because they didn’t hold enough liquid assets on their balance sheet as they expected central banks and governments to step in if required, Carney’s move is expected to make the banks hold……even less liquidity.

It’s obviously nothing to say that this goes against every possible piece of regulation devised over the last few years. While the regulators were right in thinking that banks needed to hold more liquid assets, they took on the wrong problem: it was government and central bank support that brought about low liquidity holdings, and not free-markets recklessness. Anyway, Carney’s move kind of undermines that effort and risks rewarding mismanaged banks at the expense of safer ones.

Carney’s decision also goes against all the principles devised by the ‘father’ of central banking: Walter Bagehot. I guess it is time to decipher Bagehot, as he has been constantly misquoted since the start of the crisis by people who have apparently never read him. As a result he was used to justify what were actually anti-Bagehot policies. Bagehot’s principles are underlined in his famous book Lombard Street, written in 1873. What should a central bank do during a banking crisis? According to Bagehot (as described in chapters 2, 4 and 7), it should:

- Lend freely to solvent banks and companies

- Lend at a punitive rate of interest

- Only accept good quality collateral in exchange

For instance, in chapter 2:

The holders of the cash reserve must be ready not only to keep it for their own liabilities, but to advance it most freely for the liabilities of others. They must lend to merchants, to minor bankers, to ‘this man and that man,’ whenever the security is good.

In chapter 7:

First. That these loans should only be made at a very high rate of interest. This will operate as a heavy fine on unreasonable timidity, and will prevent the greatest number of applications by persons who do not require it. The rate should be raised early in the panic, so that the fine may be paid early; that no one may borrow out of idle precaution without paying well for it; that the Banking reserve may be protected as far as possible.

Secondly. That at this rate these advances should be made on all good banking securities, and as largely as the public ask for them. The reason is plain. The object is to stay alarm, and nothing therefore should be done to cause alarm. But the way to cause alarm is to refuse some one who has good security to offer… No advances indeed need be made by which the Bank will ultimately lose.

No central bank applied Bagehot’s recommendations during the financial crisis. Granted, given the organisation of today’s financial system, it is difficult for central bank to lend to non-financial firms. Nonetheless, it took them a little while to start lending freely and lent to insolvent banks as well. They also started to accept worse quality collateral than what they used to (think about the Fed now purchasing mortgage/asset-backed securities for example). Finally, central banks have never charged a punitive rate on their various facilities. Quite the contrary: interest rates were pushed down as much as humanly possible on all normal and exceptional refinancing facilities.

While the ECB and the Fed have made clear that some of those were temporary measures, Carney now seems to imply that, not only are they here to stay, but they also will be extended in non-crisis times. He calls that being “open for business”. Poor Bagehot must be turning in his grave right now.

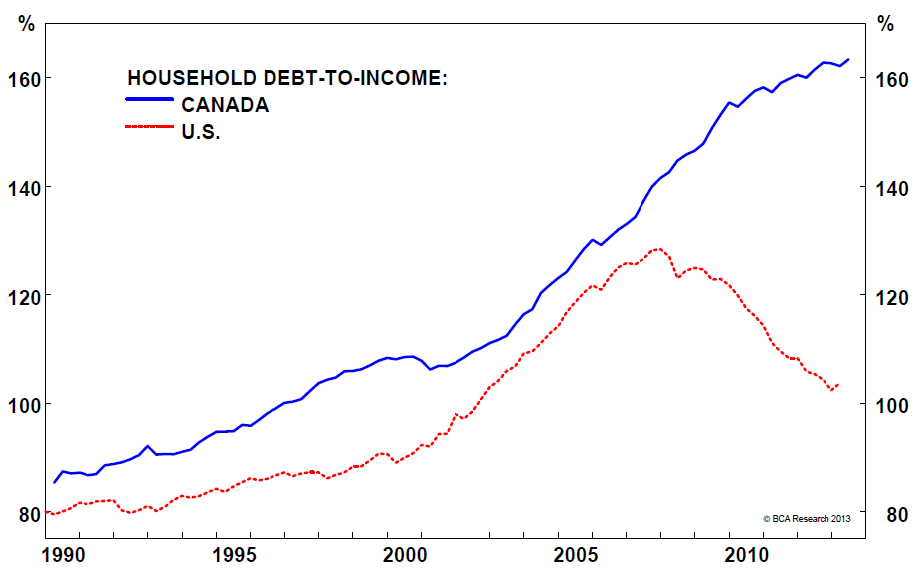

According to Carney, those measures will reinforce financial stability. Really? So no moral hazard involved? no bank taking unnecessary risks because it knows that the BoE has its back? If Mervyn King didn’t do everything perfectly while in charge, at least he had a point. Carney, after overseeing a large credit bubble in Canada over the past few years (he first joined the Bank of Canada in 2003, then rejoined it as Governor in 2008), is now applying his brilliant recipe to the UK.

I think that Carney’s decisions introduce considerable incentive distortions in the banking system. This is clearly not what a free-market should look like. In any case, if a new crisis strikes as a result, I am pretty sure that laissez-faire will be blamed again. It is ironic to see that some of those central bankers destroy faith in free-markets while trying to protect them.

Bagehot also said other things that go against the principles driving our current banking and regulatory system. More details in another post!

Photograph: Reuters/Bloomberg

Chart: The Big Picture

Recent Comments