The importance of intragroup funding – 19th century Canada

This is a quick follow-up post on intragroup funding, as promised in the one focusing on the US experience during the 19th century.

The Canadian case is interesting, because Canada is also a ‘recent’ country that experienced its own banking development at the same time as its close, also ‘recent’, neighbour, the US. Though the contrast cannot be starker; while the US was prone to recurrent financial crises during the 19th century, Canada’s financial system remained pretty stable throughout the period, and continued to do so until today.

The main difference between the Canadian and the US banking systems was their fragmentation and regulation. The US, as described earlier, had a very fragmented and highly regulated (though much less than today…) banking system, whereas Canada had a lightly regulated and quite concentrated one (some could argue that it was pretty much an oligopoly). In the US, a multitude of unit banks with no branches and local monopolies prevailed. In Canada, large nationwide banks with multitude of branches prevailed. This was due to the specific political and institutional arrangements in Canada: unlike in the US, where states had most of the powers to charter banks, the Canadian government was the one who decided whether or not to grant a bank charter, not the provinces. In 1890, there were 38 chartered banks in Canada and around 8000 in the US.

It is easy to understand why the Canadian banking system was more stable: nationwide branch network allowed banks to move liquidity around and continue to accept each others’ notes at par, and loan books were much more diversified and less prone to local asset quality deterioration. When branches in the West of the country were experiencing a liquidity shortage, it was easy to provide them with extra liquidity from their cousin in the East in order to avoid contagion as banks tried to protect their name and reputation. Moreover, the fact that only a few banks had large market shares in the country made it a lot easier to coordinate a response in times of financial tension, pretty much like the US clearinghouse system, but on a much larger scale.

The consequences of this design were that banks operated on thinner liquidity and capital buffers than banks in the US, as credit and liquidity risks could be consolidated and diversified away. Furthermore, credit was as available in Canada as in the US and deposit rates were higher, while banks were nonetheless more profitable thanks to centralised back office functions on a nationwide basis (i.e. economies of scale).

In the end, Canada experienced not a single bank failure during the Great Depression, despite having no central bank nor deposit insurance, the two tenets of current banking regulatory ‘good practices’.

What is striking from my series of posts on intragroup funding is that history is crystal clear: it is large, diversified, banking groups that represent a more stable ideal than insulated, but reinforced, smaller local banks. Unfortunately, most regulators and economists don’t seem to know much banking history…

Bundesbank’s Dombret has strange free market principles

Andreas Dombret, member of the executive board of the Bundesbank, made two very similar speeches last week (The State as a Banker? and Striving to achieve stability – regulations and markets in the light of the crisis). When I started to read them, I was delighted. Take a look:

If one were to ask the question whether or not the market economy merits our trust, another question has to be added immediately: “Does the state merit our trust?”

[…]

Sometimes it seems as if we are witnessing a transformation of values and a redefinition of fundamental concepts. The close connection between risk-taking and liability, which is an important element of a market economy, has weakened.

Conservative and risk-averse business models have become somewhat old-fashioned. If the state is bearing a significant part of the losses in the case of a default of a bank, banks are encouraged to take on more risks.

[…]

[High bonuses and short-termism] are the result of violated market principles and blurred lines between the state and the banks. They are not the result of a well-designed market economy but rather indicative of deformed economies. However, the market economy stands accused of these faults.

Brilliant. I was just about to become a Dombret fan when…I read the rest:

In my view, the solution is to be found in returning the state to its role of providing a framework in which the private sector can operate. This means a return to the role the founding fathers of the social market economy had in mind.

They knew that good banking regulation is a key element of a well-designed framework for a well-functioning banking industry and a proper market economy in general.

[…]

This is where good bank capitalisation comes into play. It is the other side of the coin. Good regulation should directly address the key problem. If the system is too fragile, an important and direct measure to reduce fragility is to have enough capital.

[…]

Good capitalisation will have the positive side effect of reducing many of the wrong incentives and distortions created by taxpayers’ implicit guarantees and therefore making the bail-in threat more credible ex ante.

And from the second article:

In view of all this, I believe that two elements will be especially important in making banks more stable: capital and liquidity. Deficits in both of these things were factors which contributed significantly to the financial crisis. The state can bring in regulation to address these deficits, and has done so very successfully.

And on shadow banking:

In terms of financial stability, the crux of the matter is that these entities can cause similar risks to banks but are not subject to bank regulation.And the shadow banking system can certainly generate systemic risks which pose a threat to the entire financial system.

Much the same applies to insurance companies. Although they aren’t a direct component of the shadow banking system, they can also be a source of systemic risk. All of this makes it appropriate to extend the reach of regulation.

Sorry but I will postpone joining the fan club…

Mr. Dombret correctly identifies the issue with the financial system: too much state involvement. What is his solution? More state involvement. It is hard to believe that one person could come up with the exact same solution that had not worked in the past. Were the banks not already subject to capital requirements before the crisis? Even if not ‘high’ enough they were still higher than no capital requirement at all. So in theory they should have at least mitigated the crisis. But the crisis was the worst one since 1929, and much worse than previous ones during which there were no capital requirements. Efficient regulation indeed…

Like 95% of regulators, he makes such mistakes because of his (voluntary?) ignorance of banking history. A quick look at a few books or papers such as this one, comparing US and Canadian banking systems historically, would have shown him that Canadian banks were more leveraged than US banks on average since the early 19th century, yet experienced a lot fewer bank failures. There is clearly so much more at play than capital buffers in banking crises…

Moreover, he views formerly ‘low’ capital requirements as a justification for bankers to take on more risks to generate high return on equity. This doesn’t make sense. For one thing, the higher the capital requirements the higher the risks that need to be taken on to generate the same RoE. It also encourages gaming the rules. This is what is currently happening, as banks are magically managing to reduce their risk-weighted assets so that their regulatory-defined capital ratios look healthier without having to increase their capital.

Mr. Dombret starts by seriously questioning the state’s ability to manage the system and highlights the very harmful and distortive effects of state regulation to eventually… back further and deeper state regulation.

A question Mr. Dombret: what are we going to do following the next crisis? Continue down the same road?

Can please someone remind Mr. Dombret of what a free market economy, which he seems to cherish, means?

Picture: Marius Becker

BoE’s Mark Carney is burying Walter Bagehot a second time

Banks were partying on Thursday. Mark Carney, the new governor of the Bank of England, decided to ‘relax’ rules that had been put in place by its predecessor, Mervyn King. From now on, the BoE will lend to banks (as well as non-bank financial institutions) for longer maturities, accept less quality collateral in exchange, and lower the interest rate on/cost off those facilities. Mervin King was worried about ‘moral hazard’. Mark Carney has no idea what that means.

According to the FT, Barclays quickly figured out what this move implied: “it reduces the need for, and the cost of, holding large liquidity buffers.” Just wow. So, while we’ve just experienced a crisis during which some banks collapsed because they didn’t hold enough liquid assets on their balance sheet as they expected central banks and governments to step in if required, Carney’s move is expected to make the banks hold……even less liquidity.

It’s obviously nothing to say that this goes against every possible piece of regulation devised over the last few years. While the regulators were right in thinking that banks needed to hold more liquid assets, they took on the wrong problem: it was government and central bank support that brought about low liquidity holdings, and not free-markets recklessness. Anyway, Carney’s move kind of undermines that effort and risks rewarding mismanaged banks at the expense of safer ones.

Carney’s decision also goes against all the principles devised by the ‘father’ of central banking: Walter Bagehot. I guess it is time to decipher Bagehot, as he has been constantly misquoted since the start of the crisis by people who have apparently never read him. As a result he was used to justify what were actually anti-Bagehot policies. Bagehot’s principles are underlined in his famous book Lombard Street, written in 1873. What should a central bank do during a banking crisis? According to Bagehot (as described in chapters 2, 4 and 7), it should:

- Lend freely to solvent banks and companies

- Lend at a punitive rate of interest

- Only accept good quality collateral in exchange

For instance, in chapter 2:

The holders of the cash reserve must be ready not only to keep it for their own liabilities, but to advance it most freely for the liabilities of others. They must lend to merchants, to minor bankers, to ‘this man and that man,’ whenever the security is good.

In chapter 7:

First. That these loans should only be made at a very high rate of interest. This will operate as a heavy fine on unreasonable timidity, and will prevent the greatest number of applications by persons who do not require it. The rate should be raised early in the panic, so that the fine may be paid early; that no one may borrow out of idle precaution without paying well for it; that the Banking reserve may be protected as far as possible.

Secondly. That at this rate these advances should be made on all good banking securities, and as largely as the public ask for them. The reason is plain. The object is to stay alarm, and nothing therefore should be done to cause alarm. But the way to cause alarm is to refuse some one who has good security to offer… No advances indeed need be made by which the Bank will ultimately lose.

No central bank applied Bagehot’s recommendations during the financial crisis. Granted, given the organisation of today’s financial system, it is difficult for central bank to lend to non-financial firms. Nonetheless, it took them a little while to start lending freely and lent to insolvent banks as well. They also started to accept worse quality collateral than what they used to (think about the Fed now purchasing mortgage/asset-backed securities for example). Finally, central banks have never charged a punitive rate on their various facilities. Quite the contrary: interest rates were pushed down as much as humanly possible on all normal and exceptional refinancing facilities.

While the ECB and the Fed have made clear that some of those were temporary measures, Carney now seems to imply that, not only are they here to stay, but they also will be extended in non-crisis times. He calls that being “open for business”. Poor Bagehot must be turning in his grave right now.

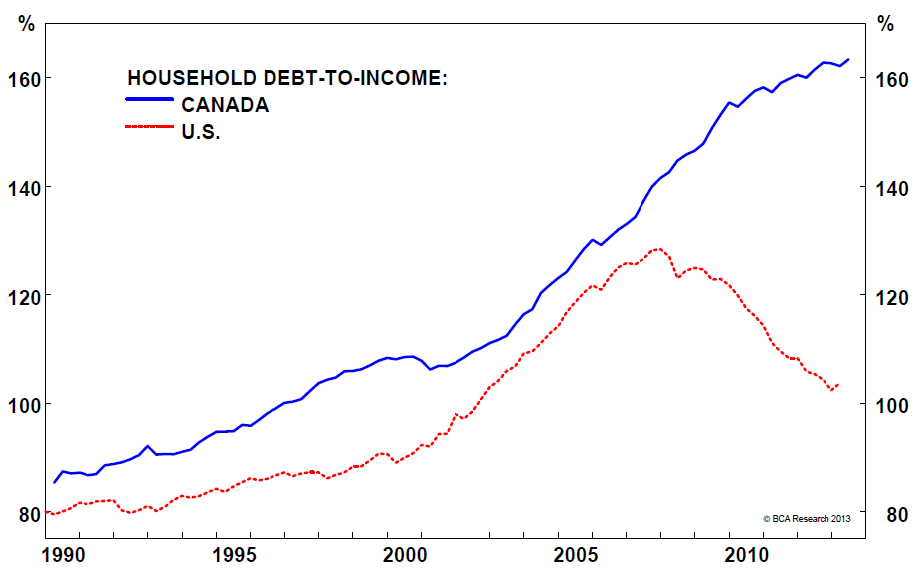

According to Carney, those measures will reinforce financial stability. Really? So no moral hazard involved? no bank taking unnecessary risks because it knows that the BoE has its back? If Mervyn King didn’t do everything perfectly while in charge, at least he had a point. Carney, after overseeing a large credit bubble in Canada over the past few years (he first joined the Bank of Canada in 2003, then rejoined it as Governor in 2008), is now applying his brilliant recipe to the UK.

I think that Carney’s decisions introduce considerable incentive distortions in the banking system. This is clearly not what a free-market should look like. In any case, if a new crisis strikes as a result, I am pretty sure that laissez-faire will be blamed again. It is ironic to see that some of those central bankers destroy faith in free-markets while trying to protect them.

Bagehot also said other things that go against the principles driving our current banking and regulatory system. More details in another post!

Photograph: Reuters/Bloomberg

Chart: The Big Picture

Recent Comments