The Economist on Bitcoin (and some weird claims)

The Economist has two interesting articles on Bitcoin this week (here and here), as well as a blog entry (here). Coloured coins and the potential development (and other uses) of Bitcoin’s technology are mentioned.

But two of the articles make very strange (if not outright wrong) claims in order to criticise some of the principles underlying Bitcoin. One considers the inherent deflationary effect of Bitcoin as being a limitation on the ability of the currency to become mainstream. The article once again seems to miss the difference between good and bad deflation. For sure, this differentiation wasn’t mainstream until recently and is still not accepted by many mainstream economists (see one of the latest examples here). Still, introducing some nuance in its articles wouldn’t hurt the newspaper. In addition, the Economist makes claims such as:

A modicum of inflation greases the system by, in effect, cutting the wages of workers whose pay cheques fail to keep pace with inflation.

Don’t they see the problem with this sentence? Inflation fuelling inflation anyone?

In the blog post, Ryan Avent also makes a very inaccurate claim:

What’s more, the idea that modern central banks with their loosey-goosey printing presses have generated an epidemic of inflation is a little nuts; if anything, rich-world central banks have become too effective at protecting the value of their respective currencies.

Really? According to research by Selgin and White, the dollar has lost most of its value since the Fed was set up (whereas the value remained relatively stable over the previous century, though with short-term large fluctuations). (although it is possible that Ryan only refers to the last few years)

While I agree that Bitcoin isn’t perfect, its critics will have to find other angles of attack.

Bitcoin Burgers in London!

Walking in London yesterday, look at what I found near Bricklane:

This is genius 🙂

Congrats guys for democratising cryptocurrencies!

China as a spontaneous finance Frankenstein

China is an interesting case. Underneath its very tight government-controlled financial repression hide numerous financial experiments aimed at bypassing those very controls. The Chinese shadow banking system is now a well-known financial Frankenstein, with multiple asset management companies, wealth management products and other off-balance sheet entities providing around half the country’s credit volume. The more the government tries to regulate the system, the more financial innovation finds new workarounds and become increasingly more opaque.

Bitcoin is following this typical mechanism. China was one of the world’s most successful Bitcoin markets as local retailers and customers attempted to avoid government control and manipulation. In short, Chinese users liked that Bitcoin had fixed rules that could not be twisted by some corrupted officials. Bitcoin allowed them to transfer currency internationally almost without restriction. Its Chinese supporters felt free. Indeed, freedom and facilitation of transaction and saving is what drives most spontaneous financial innovations. Nonetheless, the love story couldn’t last as I have already described and the government launched a crackdown on Bitcoin in December.

Nonetheless, Bitcoin is coming back, the Frankenstein way. The FT reported today that local Chinese Bitcoin exchanges are now finding ways around new government rules. Surprising? It shouldn’t be. Governments around the world, a simple message: don’t underestimate your citizens. You’ll always run after them. Never ahead.

The issue is now that all those rules are pushing Bitcoin and other innovations even more into the shadows, making the whole system even more opaque and hard to analyse. For instance, while Chinese banks are now forbidden to clear Bitcoin transactions, a local platform route the money through its founder’s account. Some others have started to use voucher systems, essentially transferable claims on RMB accounts for people who want to buy and sell Bitcoins. Those vouchers effectively become claims on claims on money, or some sort of money substitutes redeemable on money substitutes (bitcoins) redeemable on money (USD)…

I personally don’t really welcome such evolutions. Government should stay away and not add further systemic risks to innovations already trying to figure out what their own limits are. As I recently said, learning is intrinsic to any system and should not be suppressed.

The Financial Times on Bitcoin, P2P lending and secular stagnation

The FT has a few articles on some of my favourite topics today.

John Authers argue that it is time to take Bitcoin seriously. Who would say that I disagree? In his article he refers to several points I had already mentioned in some of my previous posts. He adds an interesting analogy with previous internet firms and concepts:

[…] even if Bitcoin is as successful as it is possible now to imagine, it looks overvalued at recent prices. It is in a bubble.

But this does not prove that the concept has no future. Shares in Amazon.com were also in a bubble in the late 1990s, and yet proved a great long-term investment after the bubble burst. Wild swings in value are typical when new technologies arrive.

A commenter also had a very good point, which highlighted Bitcoin’s (or other similar alternative digital currencies’) potential trade-boosting abilities:

Can you imagine a world where anyone can set up a shop on the internet and instantly accept payments from all over the world to sell its product or service without any intermediary? Well that’s only one face of what Bitcoin enables.

Naysayers will keep saying that Bitcoin is useless or only diverts wealth from ‘productive opportunities’ anyway.

FT Alphaville continued its long tradition of confused/confusing posts with this one on P2P lending today. I don’t know about you, but it does look to me that everything in the financial world that’s innovative and far from regulators’ grip is now under attack from Alphaville bloggers. They could have a point. But in this case, they don’t. They completely miss the point. The author misunderstands the financial crisis and draws the wrong conclusions from it.

According to the author, P2P is ‘pro-cyclical’ and has ‘no skin in the game’, which makes this asset class of systemic risk. He’d like to see P2P platforms to hold capital buffers to absorb losses. This makes no sense whatsoever. P2P is an investment. There are tons on possible investments. Anybody can invest directly in equities or bonds or FX or whatever, or through mutual funds/investment managers. P2P works the same way. Are we asking mutual funds to hold a capital buffer to absorb losses suffered by their clients’ portfolio? Of course not.

Banks need to retain capital as they hold deposits, which are part of the money supply and can be drawn down at any time by depositors, and also because they play a critical role in the payment system. If banks make losses on lending, capital allows them not to transfer the loss onto customers, who often just wanted to store their money there. This has absolutely nothing to do with the kind of voluntary investments I described above. Moreover, some P2P platforms have already set up loss-absorbing funds anyway… Platforms also have their ‘skin in the game’: if everybody stops lending through them, they don’t earn any revenue and go out of business. While I agree that platforms should not hide the fact that losses could occur on P2P investments, paternalism and regulation is the wrong way to go. Education and responsibility should be the goals.

In another Alphaville blog post, Izabella Kaminska reports the arguments of two economists against the Summers/Krugman secular stagnation story. And it basically reflects mine: it doesn’t exist. It also has a particular Austrian flavour: savings and productivity generate long-term economic growth, and low interest rates caused the economy to boom above potential (debt accumulation) and caused malinvestments (investments that generated short-term growth but that no one wanted in the end).

• There is no shortage of high return investment projects in the world. And the dearth of global corporate investment, which drove the great recession, means that productive potential is shrinking despite corporate profitability, leverage and cash balances being sound.

• The three ingredients for growth are a) a stable macro environment; b) a sound banking system; c) economic reforms that encourage entrepreneurship. What is missing right now is private sector confidence in the ability of governments and central bankers to provide all three.

• Credit bubbles can boost growth only temporarily and incur heavy costs in terms of subsequent deleveraging and misallocation of resources.

Hedge funds keep attracting new money (assets under management are up 16% since end-2012)… I won’t remind you that I’m wondering whether or not this is a sign that nominal interest rates are lower than their Wicksellian natural rates, forcing investors to take extra risk to achieve the real rates of return they would normally obtain from safer investments. But I guess that Summers and Krugman would say that, anyway, bubbles are necessary for the economy. Another side of the story is that not that many people seem to believe anymore in hedge funds outperforming the markets. Hedge funds seem to be transformed into mutual funds… But in this case, why paying such high management and performance fees? This doesn’t make so much sense.

Statism and the ideological war against Bitcoin

While the US Senate provided some support to Bitcoin and other digital alternative ‘currencies’, most of central banks and regulatory authorities around the world seem to have declared war against them. Yesterday, Alan Greenspan, the former Fed Chairman, said that Bitcoin was a bubble and that it had no intrinsic value. Although his track record at spotting bubbles is rather… poor.

China’s central bank, the PBoC, banned financial institutions from doing any kind of business with it. Is it surprising from a country in which citizens are subject to financial repression and capital controls and who as a result see Bitcoin as a step towards financial freedom? It was very unlikely that China would endorse a medium of exchange over which it has no control. This is also true of other central banks. Today, Business Insider reported that the former Dutch central bank president declared that Bitcoin was worse than the 17th century Tulip mania. FT Alphaville continued its recurrent attacks against Bitcoin. The Banque de France also published a very bearish note on the now famous digital currency. The title couldn’t be more explicit: “The dangers related to virtual currencies’ development: the Bitcoin example”. What’s striking with the Banque de France note is that it pretty much sums up all criticisms (misplaced or not) against the virtual currency.

They start with the fact that Bitcoin is “not regulated.” Horror. Well, not only it is the goal guys, but it‘s not even completely true: Bitcoin’s issuance is actually very tightly regulated by its own algorithm, which replaces the discretionary powers of central banks. They add that Bitcoin provides “no guarantee of being paid back” and that its value is volatile. Yes, this is what happens when we invest in any sort of asset. To them, Bitcoin’s limited growth and resulting scarcity was intentionally introduced by its designer to provide it with a speculative nature. Not really… The design was a response to central banks’ lax use of their currency-issuing power. Moreover, Bitcoin’s value is the “exclusive result of supply and demand”! I guess that, for central bankers, this is indeed shocking. For classical liberals like me, or libertarians, this is the way it should be.

I think the ‘best’ argument against Bitcoin is the fact that, as it is anonymous, it can be used in criminal and fraudulent activities and money laundering. Wait… isn’t central bank cash even more anonymous? Hasn’t central bank cash been used in fraudulent activities and money laundering for decades, if not centuries? Are central banks involved in Know Your Customer practices? Finally, another argument of the Bank de France is: there is no authority safeguarding the virtual wallets, exposing them to hackers and other potential threats. True, there is no example in history of ‘authorities’ stealing, debasing or manipulating the reserves of media of exchange they were supposed to ‘safeguard’…* The central bank harshly concludes that Bitcoin’s use “presents no interest to economic agents beyond marketing and advertising, while exposing them to large risks.”

As I have said several times, Bitcoin is surely not perfect. But neither are our current official fiat currencies. I am neither for nor against Bitcoin or any digital currency. I am in favour of letting the markets experiment and pick the currency they judge appropriate. I am against a central authority forcing the use of a certain currency.

Let’s debunk a few other myths.

First, Bitcoin is not money. It is at best a commodity-like asset, such as gold, or a very limited medium of exchange. But it is not a generally accepted medium of exchange, the traditional definition of money. Perhaps someday. But not at the moment. Current institutional frameworks also make it very difficult for it to become generally accepted: legal tender laws, taxation in official currencies, and central banks’ monopoly on the issuance of money severely slow down the process.

As a result, the complaints that we keep hearing that its value is volatile and doesn’t allow for stable prices and economic efficiency through menu costs is completely misplaced. For a simple reason: apart from a few exceptions, there is no price denominated in Bitcoin! When you want to buy a good using Bitcoin, Dollar or Euro (or whatever) prices are converted into Bitcoins. Because Bitcoin has its own FX rate against those various currencies, when its value against another currency fluctuates, the purchasing power of Bitcoin in this currency fluctuates and prices converted into Bitcoins fluctuate! Prices originally denominated in Bitcoin would not fluctuate however.

What happens when you are an American tourist visiting Europe? Your purchasing power is in USD. But you have to buy goods denominated in EUR. As a result, your purchasing power fluctuates every day as you use USD to buy EUR goods. It is the same with Bitcoin. For now Bitcoin effectively involves FX risk. Either the consumer bears the risk of seeing its purchasing power fluctuates, or the seller/producer bears it, knowing that his own input prices were not in Bitcoin. At the moment, in the majority of cases, consumers/buyers bear the risk. Perhaps a bank could step in and start proposing Bitcoin FX derivatives for hedging purposes to its clients? Actually, a Bitcoin trading platform actually already offers an equivalent service.

Something that is really starting to annoy me every time I hear it is that Bitcoin is not like traditional fiat money, as it is not backed by anything and thus has no intrinsic value. Sorry? The very definition of fiat money is that it is not backed by anything! And none of the efforts of some Modern Monetary theorists, chartalists, or FT Alphaville bloggers will manage to convince us of the contrary. They claim that fiat money has intrinsic value as it is backed by “the government’s ability to tax the community which bestows power on it in the first place. This tax base represents the productive capacity of the collective wealth assets of the US community, its land and its resources. The dollar in that sense is backed by the very real wealth and output of the system. It is not just magic paper”, as described by the FT Alphaville blog post mentioned above. Right. This all sounds nice and abstract but can I show up at my local central bank and redeem my note for my share of “the productive capacity of the country”?**

A fiat money isn’t backed by anything at all but by faith. The only thing that gives fiat money its value is economic agents’ trust in it. When this trust disappears the currency collapses. It happened numerous times in history but I guess it is always convenient for some people to forget about those cases. A recent example was the hyperinflation in Zimbabwe: despite legal tenders laws and the fact that taxes were collected in Zimbabwean Dollars, the population lost faith in the currency and turned towards alternatives, mainly USD, EUR and South African Rand. People could well lose faith in advanced economies’ official currencies and start trusting Bitcoin (or any other medium of exchange) more. At that point, Bitcoin would still be fiat but become effectively ‘backed’ by the faith of economic agents and could well trigger a switch in the money we use on a day to day basis.

Another (half) myth is that Bitcoin is only a tool for speculation that diverts real money from real ‘productive purposes’. It is true that, as an asset, Bitcoin will always attract speculators. But it doesn’t necessarily divert money from the real economy: 1. when Bitcoins are sold, they are swapped for real money, money that does not remain idle but then can be used for ‘productive purposes’ by the new holder (or his bank) and 2. as a medium of exchange, Bitcoin can actually facilitate trade and hence ‘productive activities’. Don’t get me wrong: this does not mean that there are no better investment opportunities than Bitcoin. Investors will decide, and if the digital currency is destined to fail, it will, and the markets will learn.

There are other problems with Bitcoin, one of which being that it provides an inelastic currency as its supply is basically fixed. However, in a Bitcoin-standard world (as opposed to a gold-standard), we could probably see the emergence of fractional reserve banks that would lend Bitcoin substitutes and issue various liabilities (notes and deposits mainly) denominated in Bitcoin and redeemable in actual Bitcoin (which would then play the role of high-powered money). This mechanism would then provide some elasticity to the currency (and therefore to the money supply) to respond to increases and decreases in the demand for money.

Bitcoin seems to enrage central bankers, regulators, Keynesians (particularly post-Keynesians), chartalists, Modern Monetary theorists and other statists. Consequently they resort to myths and misconceptions in order to threaten its credibility. As I have already said, my stance is neutral. Alternative currencies will come and go. Some will fail. Others will succeed. Markets will decide. I argue that alternative currencies contribute to the greater good as they all of a sudden introduce monetary competition between emerging private actors and traditional centralised institutions. If alternative currencies can eventually force central banks and states to better manage their own currencies, it would be for the benefit of everyone.

To end this piece, let me quote Hayek:

But why should we not let people choose freely what money they want to use? By ‘people’ I mean the individuals who ought to have the right whether they want to buy or sell for francs, pounds, dollars, D-marks or ounces of gold. I have no objection to governments issuing money, but I believe their claim to a monopoly, or their power to limit the kinds of money in which contracts may be concluded within their territory, or to determine the rates at which monies can be exchanged, to be wholly harmful.

Well said mate.

* This was irony, for those who didn’t get it.

** The spontaneous development of alternative local currencies (such as this one) by individuals lacking balances in the official currency of the country but willing to trade goods or to propose services, is another example of a non-state issued money (and not collected to pay taxes) that facilitate economic output and the generation of wealth, in direct contradiction to the state theory exposed above.

Chart: CNN

Cato Institute’s 31st Monetary Conference – Was the Fed a good idea?

About two weeks ago, the US-based think tank Cato organised its annual monetary conference. Great panels and very interesting speeches.

Three panels were of particular interest to me: panel 1 (“100 Years of the Fed: What Have We Learned?”), panel 2 (“Alternatives to Discretionary Government Fiat Money”), panel 3 (“The Fed vs. the Market as Bank Regulator”).

In panel 1, George Selgin destroys the Federal Reserve’s distorted monetary history. Nothing much new in what he says for those who know him but it just never gets boring anyway. He covers: some of the lies that the Federal Reserve tells the general public to justify its existence, pre-WW2 Canada and its better performing monetary system despite not having a central bank, the lack of real Fed independence from political influence and……the Fed not respecting Bagehot’s principles despite claiming to do so. In this panel, the speech of Jerry Jordan, former President of the Federal Reserve Bank of Cleveland, is also very interesting.

In panel 2, Larry White speaks about alternatives to government fiat money, counterfeiting laws and state laws making it illegal to issue private money. Scott Sumner describes NGDP level targeting. Here again, nothing really new for those who follow his blog, but interesting nonetheless (even though I don’t agree with everything) and a must see for those who don’t.

In panel 3, John Allison provides an insider view of regulators’ intervention in banking (he used to be CEO of BB&T, an American bank). He argues that mathematical risk management models provide unhelpful information to bankers. He would completely deregulate banking but increase capital requirements, which is an original position to say the least. Kevin Dowd’s speech is also interesting: he covers regulatory and accounting arbitrage (SPEs, rehypothecation…) and various banking regulations including Basel’s.

Overall, great stuff and you should watch the whole of it (I know, it’s long… you can probably skip most Q&As).

PS: Scott Sumner also commented on the Pope’s speech on “evil incarnate”. Reminds me of the vocabulary I used…

News digest (Krugman and deregulation, central banking for Bitcoin…)

A looooooooot of news since the beginning of the week. So I’ll just quickly go over a few of them. Guys please, next time, spread your news more evenly over time. There was nothing to comment on recently!

Not new news but the Swedish bank regulators are thinking of increasing RWAs on mortgages to fight a growing housing bubble. Well, raising them to 25% (from 15% floor…) would still not change much: they would remain below most other asset classes’ level and securitisation (RMBS) would allow banks to bypass the restrictions.

Meanwhile, Yves Mersch, member of the Executive Board of the ECB, spoke about how to revive SME lending in bank-reliant Europe. His solutions involve: strengthening banks, securitisation and… banking union. Any word of capital requirements/risk-weighted assets? Not a single one. When I told you that central bankers don’t seem to get it…

But the UK government wants to ditch the household lending side of the Funding for Lending Scheme! They now only want to provide cheap funding to banks if they prove that they lend to SMEs. Why not, but I doubt it would really work for a few reasons: 1. demand for loans remains quite low, 2. market funding remains cheap (it was cheaper than FLS), 3. banks haven’t drawn much on it anyway, 4. RWAs are still in place! Mortgage and household lending will still attract most of lending volume as it is more profitable from a capital point of view.

Meanwhile (again), SME financing from alternative lenders not subject to RWAs and other stupid capital rules, keeps growing in the UK. However, it is still tough for those lenders to assess the health of the companies that would like to lend to.

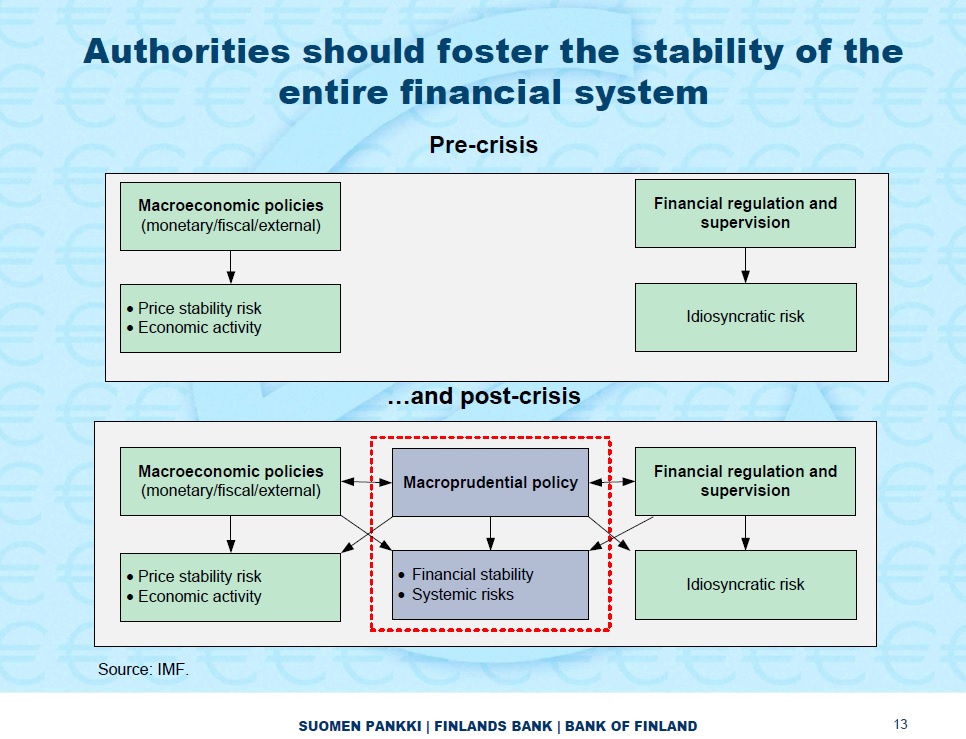

Erkki Liikanen, the Governor of the central bank of Finland, told us about his ideas to improve financial stability. Surprise: they haven’t changed. So macroprudential policy starts interfering with macroeconomic policies and financial regulation, with possibly opposite effects that don’t seem to bother him much. Look at that slide, which is the very definition of a messy policy goal, with multiple targets and interferences:

A very strange piece in the Washington Post: Bitcoin needs a central banker. Wait a second. No, it’s definitely not the 1st of April. First, the author asserts that Bitcoin’s wild changes in value make it difficult to be adopted as a currency. This is extraordinary. Does the author even understand FX rates? If the author wishes to purchase his coffee using Euros, despite the coffee being priced in Dollars, will he also declare that the fact the Euro’s value is unstable (making the effective Euro price of its coffee volatile) makes the currency improper for use? When prices are originally denominated in Bitcoin, the change in the value of the digital currency won’t affect them. When prices are actually denominated in USD, but converted into Bitcoin, then yes, changes in the value of the digital currency will affect them. But this is hardly Bitcoin’s fault… Then he gets mixed up with ‘menu costs’, ‘hyperinflation’, ‘money demand’, etc. Wow. Just one last thing: has he even understood that Bitcoin was designed to be free from central bankers and government intervention in the first place?

Izabella Kaminska in the FT wrote a new piece on Bitcoin and other alternative electronic currencies. She complains about the multiplication of such currencies that nothing backs and pretty much only see speculative motivations underlying them. I am not going to comment on the whole thing, but whether right or wrong, she should ask herself why there is such frenzy about those currencies at the moment. My guess is that, governments’ and central banks’ manipulation of their own currencies have unleashed a beast: people afraid to hold classic currencies started to look for alternatives, pushing up their prices, in turn attracting speculators. The process is similar to ‘bad’ financial innovations (the ones designed specifically to bypass restricting regulation): they often start as a benign innovation for the ‘common good’, but the surprising demand for them and large profits attract speculators until the market crashes. Not the fault of the innovation, but the fault of the regulation that triggered them…

Paul Krugman thinks that “the trouble with economics is economists”, and that mainstream economics is not to blame for the financial crisis. I partly disagree: 1. there are various schools of thought within mainstream economics that often disagree with each other altogether and 2. most (all?) of them cannot fully explain the crisis anyway. But, and this is where Krugman shows his limited knowledge of banking and therefore the limit of his reasoning, he declares that “the mania for financial deregulation, for example, didn’t come out of standard economic analysis.” I’m sorry? Which mania for financial deregulation? The international banking sector had never been as regulated in history as on the eve of the crisis! (even taking into account of the few one-off deregulations) I need to come back to this in a subsequent post. Really, Paul, you have to revise your history. And your reasoning.

On Free Banking, George Selgin urges Scots to ‘poundize’ unilaterally if ever they declare independence from the UK. And “if the British Parliament refuses to cooperate, so much the better. Who knows: Scotland could even end up with a banking system as good as the one it had before 1845, when Parliament, which knew almost as little about currency then as it does now, began to bugger it up.” If only Scotland could enlighten the world a second time and get back to a free banking system!

News digest

I have been so busy since last week that I didn’t have much time to write for this blog… And, to tell you the truth, I was almost shocked: barely any news on banks capital, regulation, monetary policy, etc, over the past few days. Sure, the ECB cut its rate by 25bp to 0.25%, but I’m not sure I should comment within the scope of this blog: I am still not convinced by such such a diverse monetary union as the Eurozone and find it hard to believe we can actually set a common interest rate for all country members within the union… Anyway, today I only wish to comment on a few articles published over the last few days.

A very interesting article published on SNL (subscription required) called Everybody wants to rule the world, including bank regulators, in which an analyst argued that “Banks are not only facing over-regulation. They are also emerging as a convenient channel through which regulators can extend their reach far beyond their legal writ.” You probably understand as well as I do how dangerous this is.

I found out yesterday that Bear Stearns liquidators filed a lawsuit against the three credit rating agencies for alleged manipulation of structured products’ ratings. They are basically arguing that, if ratings had been right, Bears Stearns’ hedge funds would not have collapsed. Blaming the rating agencies because…..hedge funds collapsed? We are not talking about simple retail investors here. We are talking about sophisticated investors. Aren’t hedge funds supposed to undertake their own analysis? Are they just blindly investing in various assets? If hedge funds managers and analysts did not believe in rating agencies’ ratings, why did they invest in those assets the first place? Or perhaps they indeed did not believe in those ratings and took on the risk on purpose. In both cases, we cannot blame the agencies for the lack of competence of those highly-remunerated hedge funds employees.

Yesterday, the FT reported that shadow banks had been among the biggest beneficiaries of the Fed’s monetary policies. I’ve already argued that it might well be a sign that real interest rates are too low (i.e. lower than the equilibrium natural rate of interest). As a result, regulators wish to regulate (of course) this segment of the financial system. My guess is that surplus liquidity would then shift to another less-regulated sector or asset class, as it always does.

A few days ago, I read in horror that Germany may start backing the financial transaction tax. A tax of 0.1% of the value of the transaction (as is proposed on cash instruments) would be a massive drain of wealth: just imagine what would happen to a newly set-up EUR100bn mutual fund (ok, no new fund would ever be of that size, but follow me just for the intellectual exercise). The fund has evidently to invest those 100bn on behalf of its clients, meaning they have to buy EUR100bn of assets. Taxing 0.1% off the total value of the transactions would mean…EUR100m to pay in taxes. This is EUR100m that EU states would withdraw from people’s savings and pensions. Bad idea.

In the Wall Street Journal, a Fed insider described how disillusioned he was from the Fed and QE: he ‘apologises’ to Americans (Scott Sumner comments on this) for QE’s bad or lack of effects. While I do not necessarily share everything he said, I also dislike the Fed’s large scale market manipulation.

On Free Banking, George Selgin criticised this Business Insider piece about airlines debasing their reward points. Reminds me of my own response to Matt Klein on the exact same topic a few weeks ago. No guys: those cases do not reflect free banking and private currencies.

Well, that’s all for the catch up.

Bitcoin, Silk Road, and weird stuff going on at City AM

Alright… I have to catch up with a lot of things after a long and very busy weekend…

First thing, I’d like that all of you who mention the Silk Road story as a ‘defeat’ for the classical liberal/libertarian ideals and for the possibility of a laissez-faire monetary system to stop right now. This Silk Road story and illegal trade have nothing to do with free-markets. Nothing. Illegal trade, and crazy people, and murders, and crime, existed before any alternative currency appeared. Liberalism does not advocate some kind of Mad Max anarchism, but voluntary cooperation.

Bitcoin has its faults (and apparently some of them might involve loss of anonymity), and if it does not satisfy the requirements of its users, it will disappear and be replaced by another medium of exchange. People will learn, new media of exchange will perform better. It’s the essence of evolution under free-markets.

Following my last-week’s post, I found it ‘funny’ to find out that the British financial newspaper City AM had two days in row published comments that reminded mine… See here and here. Coincidence?

Matthew Klein is drawing the wrong lessons on private currencies

Matthew C. Klein is a columnist for Bloomberg. He used to write on The Economist’s economic blog, Free Exchange. Despite not agreeing with him most of the times, I found that he had some of the most provocative and interesting pieces among the usually quite dull Economist posts. And I used to comment on those pieces. A lot.

He today published a new piece on the Bloomberg website, arguing that the ‘devaluation’ of US-based Southwest Airlines’ frequent flier reward points explains why private currencies (including free banking, Bitcoin and equivalents) have never taken off: they have unstable and unpredictable purchasing power.

His argument is really misguided. Let me explain why.

- First, I would not really call reward points currency. They are media of exchange of very limited use. They are definitely not generally accepted media of exchange (to be honest, Bitcoins aren’t either, as George Selgin explains).

- Bitcoins cannot even lose purchasing power unpredictably: its algorithm has been defined so that new Bitcoins are created following a very steady pattern. So I don’t see why Klein even mentions them…

- Matthew Klein seems to have limited knowledge of banking history: free banking systems have been very stable where and when they existed (White, Selgin, Dowd, Horwitz, and others have published enough on the topic). It is the state that monopolised currency issuance for its own benefits which very often led to financial crises. Currency depreciation has also been much more acute under government’s fiat currency systems.

- Finally – and this is where Klein’s argument really breaks down, the Southwest frequent-flier points devaluation is linked to the devaluation of the dollar! How? Like free banks’ private currency issuance is based on outside money reserve (usually gold or some other commodities), frequent-flier points are also based on another type of outside money (here, the US Dollar) although the analogy is not exact. Basically, every time a customer pays X USD to Southwest, Southwest generates Y reward points. As a result, there is an ex-ante Y/X exchange rate, which is supposed to remain constant over time. Issuing those points is a cost for the company, but which is offset by the potential profit of keeping loyal customers, at this specific exchange rate. When enough reward points have been accumulated, they can then be exchanged for a flight (which are priced in terms of both USD and reward points separately). While Southwest does control the reward points supply, it does not control the outside money supply. And unfortunately, the USD is slowly depreciating thanks to the Fed, thereby increasing the ex-post Y/X exchange rate and the relative purchasing power of the reward points… Like any price, reward points-based prices are sticky, and have to be revaluated over time to reflect the change in the medium of account (which is also USD) that Southwest uses to report its profits. It looks like in this case that reward points-based prices are stickier than USD-based prices, making devaluations both less frequent and sharper in order to catch up with the depreciation of their underlying outside money.

This phenomenon isn’t isolated. My internet monthly bill was recently increased by….25%! I was shocked for a few minutes when I found out. But it is easily explained: internet bills aren’t revaluated every month or even every year, despite the fact that inflation depreciates the currency’s purchasing power every month. At some point, internet firms have to readjust the prices that they charge in order to respond to the increase in their own supply costs and maintain their margins. And when it happens, increases are usually big. This is also valid for many other goods.

So Matt, you’re going to have to find another argument to justify government-controlled currencies!

Recent Comments