Hayekian legal principles and banking structure

The latest CATO journal contains a truly fascinating article (at least to me) of George Selgin titled Law, Legislation, and the Gold Standard. Selgin roots his arguments in Hayekian legal theory, as developed by Hayek in his books The Constitution of Liberty and Law, Legislation and Liberty*.

Hayek differentiates ‘law’ (that is, general backward-looking ‘meta-legal’ rules that follow the principle of the rule of law) from forward-looking ‘legislation’, which is unfortunately too often described as ‘law’ despite not respecting the very fundamentals of the rule of law. As such, Hayek describes the rule of law as being

a doctrine concerning what the law ought to be, concerning the general attributes that particular laws should possess. This is important because today the conception of the rule of law is sometimes confused with the requirement of mere legality in all government action. The rule of law, of course, presupposes complete legality, but this is not enough: if a law gave the government unlimited power to act as it pleased, all its actions would be legal, but it would certainly not be under the rule of law. The rule of law, therefore, is also more than constitutionalism: it requires that all laws conform to certain principles.

Therefore, the rule of law, according to Hayek, relies on general ‘meta-legal’ rules that have progressively, spontaneously, if not tacitly, been discovered and evolved in a given society to facilitate social interactions and exchanges between individuals (“a government of law and not of men”). Those custom-based rules have certain attributes, namely that they be “known and certain”, apply equally to everyone, define a clear limit to the coercive power of government, require the separation of power and finally only allow the judiciary to exert discretionary rulemaking (within the boundaries of those meta-legal rules). Hayek explains that “under a reign of freedom the free sphere of the individual includes all action not explicitly restricted by a general law.”

Within this framework, Selgin describes the appearance of the gold standard as following the generic principle described by Hayek:

The difference between private or customary law and public law or legislation is, I submit, one of great importance for a proper understanding of the gold standard’s success. For, despite both appearances to the contrary and conventional wisdom, that success depended crucially upon the gold standard’s having been upheld by customary law rather than by legislation. It follows that any scheme for recreating a durable gold standard by means of legislation calling for the Federal Reserve or other public monetary authorities to stand ready to convert their own paper notes into fixed quantities of gold cannot be expected to succeed.

According to him, the gold standard and its definition was mostly a spontaneous monetary arrangement rooted in private commercial customs, and enforced through the private law of contracts. He sums up:

In short, countries abided by the rules of the gold standard game because that game was played by private citizens and firms, not by governments.

Consequently, a gold standard put in place and enforced by governments is unlikely to work. He continues:

Although it may seem paradoxical, our understanding of the classical gold standard suggests that, if that standard had been deliberately set up by governments to enhance their borrowing ability, it is unlikely that it would have worked as intended. This conclusion follows because, once public (or quasi-public) authorities, governed by statute law rather than the private law of contracts, become responsible for enforcing the rules of the gold standard game, the convertibility commitments crucial to that standard’s survival cease to be credible.

He, as a result, doubts about the ability of the gold standard to be ‘forced’ to return through government policy, and demonstrates that post-WW1 attempts to reinstate the gold standard were doomed from the start as states “tragically misunderstood the true legal foundations” of the famous 19th century monetary arrangement. But Selgin also believes that a ‘spontaneous’ return to gold would be unlikely because the public has been ‘locked-into’ a fiat money standard, and that customary law tends to reinforce that trend – by legitimizing the practice over time – rather than providing a way out. Moreover, he concludes, if a new commodity-like standard were to emerge, nothing guarantees that it wouldn’t be based on another sort of medium (including synthetic commodities such as cryptocurrencies).

Now that I have explained the basics of Selgin’s reasoning, I will try to understand what it involves for banking structure and regulation. While free banking systems, such as Scotland’s, have arguably spontaneously evolved following a custom-based legal framework, the structure of the whole of today’s financial system comprises barely anything ‘natural’ left, as Bagehot would point out. Banking, as we know it, is a pure product of decades, if not centuries, of accumulating layers of positive legislation and government discretionary policies. In short, there is now little overlap between banking and the rule of law**.

The inherent instability of banking systems regulated by statute-based law, as opposed to the relative stability of free banking systems (which Larry White referred to as ‘anti-fragile banking and monetary systems’), is therefore unsurprising seen through Hayek’s and Selgin’s lens: governments, even with the best of all possible intentions, could simply not come up with a banking arrangement that could outperform decades or centuries of experience and decentralised knowledge gains that were reflected in rule of law-compliant free banking. Their attempt at centralising and harmonising the “particular circumstances of time and place” were self-defeating.

But the question isn’t what’s wrong about today’s financial system, but can we do anything about it? Can we get back to a rather ‘pure’, rule of law-compliant, free banking system? And my answer is, unfortunately, rather Bagehotian: despite how much I wish to witness the re-emergence of a financial structure based on laissez-faire principles, I believe it’s unlikely to happen… (but wait, there’s a new hope)

Why? For the very reason mentioned by Selgin: regulations have shaped the financial structure for such a long time that innovations and practices have been established that seem now unlikely to disappear. Let me give two examples:

- Money market funds were originally created to bypass the US regulation Q, which has since then been abolished. But MMF are still major financial players and unlikely to disappear any time soon. They have become an established part of the financial structure.

- Mathematical model-based risk frameworks, which existed before the introduction of Basel regulations but were not as widespread, and certainly not as uniform. Basel rules and domestic regulators required common standards that are now used both by analysts and commentators as data, and by bankers for internal risk, capital and liquidity management purposes, despite their limitations and the distortion they insert into the decision-making process. Abolishing Basel and its local implementations (such as CRD4 or Dodd-Frank) are unlikely to remove what is now accepted as market practice. However, less uniformisation in models and uses are likely to appear over time.

What about the very basic component of our modern banking system, the main beneficiary of statutory law, namely the central bank? Bagehot declared that “we are so accustomed to a system of banking, dependent for its cardinal function on a single bank, that we can hardly conceive of any other”, and opposed a radical transformation of the system which, unfortunately, was there to stay. Yet I believe the probability of getting rid of central banks without causing too much disruption is higher than what Bagehot believed. There are a number of countries that do not rely on any central bank, use foreign currencies as medium of exchange, and seem to do perfectly fine (such as Panama). This seems to show that market practices and relationships with central banks aren’t that entrenched and other models currently do exist, and which could spread relatively quickly.

But what is, in my view, our best hope of getting back to a financial system that follows Hayekian legal principles is Fintech. While Fintech firms have to comply with a number of statute-based laws, they nevertheless remain relatively free (for now) of the all intrusive banking rulebooks and discretionary power of regulators. As such, the multiple IT-enabled Fintech firms and decentralised technologies offer us the best hope of reshaping the financial system in a rule of law-based, spontaneously-emerging, manner. Of course, there will be bumps along the road and some business models will fail and other succeed, but this learning process through trial and error is key in shaping a sustainable system along Hayekian decentralised and experience-based principles. For the sake of our future, let’s refrain from the temptation of legislating and regulating at the first bump.

*At the time of my writing, I have only read the first one, although the second one is next on my reading list

**Although I am not an expert, the evolution of accounting standards over time seems to me to have mostly happened along rule of law principles (although Gordon Kerr, and Kevin Dowd and Martin Hutchinson, would perhaps argue otherwise, which is understandable as IFRS comes from statute-based law systems).

Update: See this follow-up post, which includes some Public Choice theory insights

Photo: Bauman Rare Books

Cachanosky on the productivity norm, Hayek’s rule and NGDP targeting

Nicolas Cachanosky and I should get married (intellectually, don’t get overexcited). Some time ago, I wrote about his very interesting paper attempting to start the integration of finance and Austrian capital theories. A couple of weeks ago, I discovered another of his papers, published a year ago, but which I had completely missed (coincidentally, Ben Southwood also discovered that paper at the exact same time).

Titled Hayek’s Rule, NGDP Targeting, and the Productivity Norm: Theory and Application, this paper is an excellent summary of the policies named above and the theories underpinning them. It includes both theoretical and practical challenges to some of those theories. Cachanosky’s paper reflects pretty much exactly my views and deserved to be quoted at length.

Cachanosky defines the productivity norm as “the idea that the price level should be allowed to adjust inversely to changes in productivity. […] In other words, money supply should react to changes in money demand, not to changes in production efficiency.” Referring to the equation of exchange, he adds that “because a change in productivity is not in itself a sign of monetary disequilibrium, an increase in money supply to offset a fall in P moves the money market outside equilibrium and puts into motion an unnecessary and costly process of readjustment”, which is what current central bank policies of price level targeting do. The productivity norm allows mild secular deflation by not reacting to positive ‘real’ shocks.

He goes on to illustrate in what ways Hayek’s rule and NGDP targeting resemble and differ from the productivity norm:

There are instances where the productivity norm illuminated economists that talked about monetary policy. Two important instances are Hayek during his debate with Keynes on the Great Depression and the market monetarists in the context of the Great Recession. Both, Hayek and market monetarism are concerned with a policy that would keep monetary equilibrium and therefore macroeconomic stability. Hayek’s Rule and NGDP Targeting are the denominations that describe Hayek’s and market monetarism position respectively. Taking the presence of a central bank as a given, Hayek argues that a neutral monetary policy is one that keeps constant nominal income (MV) stable. Sumner argues instead that

“NGDP level targeting (along 5 percent trend growth rate) in the United States prior to 2008 would similarly have helped reduce the severity of the Great Recession.”

Hayek’s Rule of constant nominal income can be understood in total values or as per factor of production. In the former, Hayek’s Rule is a notable case of the productivity norm in which the quantity of factors of production is assumed to be constant. In the latter case, Hayek’s rule becomes the productivity norm. However, for NGDP Targeting to be interpreted as an application that does not deviate from the productivity norm, it should be understood as a target of total NGDP, with an assumption of a 5% increase in the factors of production. In terms of per factor of production, however, NGDP Targeting implies a deviation of 5% from equilibrium in the money market.

Cachanosky then highlights his main criticisms of NGDP targeting as a form of nominal income control, that is the distinction between NGDP as an ‘emergent order’ and NGDP as a ‘designed outcome’. He says that targeting NGDP itself rather than considering NGDP as an outcome of the market can affect the allocation of resources within the NGDP: “the injection point of an increase in money supply defines, at least in the short-run, the effects on relative prices and, as such, the inefficient reallocation of factors of production.” In short, he is referring to the so-called Cantillon effect, in which Scott Sumner does not believe. I am still wondering whether or not this effect could be sterilized (in a closed economy) simply by growing the money supply through injections of equal sums of money directly into everyone’s bank accounts.

To Cachanosky (and Salter), “NGDP level matters, but its composition matters as well.” He believes that targeting an NGDP growth level by itself confuses causes and effects: “that a sound and healthy economy yields a stable NGDP does not mean that to produce a stable NGDP necessary yields a sound and healthy economy.” He points out that the housing bubble is a signal of capital misallocation despite the fact that NGDP growth was pretty stable in pre-crisis years.

I evidently fully agree with him, and my own RWA-based ABCT also points to lending misallocation that would also occur and trigger a crisis despite aggregate lending growth remaining stable or ‘on track’ (whatever that means). I should also add that it is unclear what level of NGDP growth the central bank should target. See the following chart. I can identify many different NGDP growth ‘trends’ since the 1940s, including at least two during the ‘great moderation’. Fluctuations in the trend rate of US NGDP growth can reach several percentage points. What happens if the ‘natural’ NGDP growth changes in the matter of months whereas the central bank continues to target the previous ‘natural’ growth rate? Market monetarists could argue that the differential would remain small, leading to only minor distortions. Possibly, but I am not fully convinced. I also have other objections to NGDP level targeting (related to banking and transmission mechanism), but this post isn’t the right one to elaborate on this (don’t forget that I view NGDP targeting as a better monetary policy than inflation targeting but a ‘less ideal’ alternative to free banking or the productivity norm).

Cachanosky also points out that NGDP targeting policies using total output (Py in the equation of exchange) and total transactions (PT) do not lead to the same result. According to him “the housing bubble before 2008 crisis is an exemplary symptom os this problem, where PT increases faster than Py.”

Cachanosky also points out that NGDP targeting policies using total output (Py in the equation of exchange) and total transactions (PT) do not lead to the same result. According to him “the housing bubble before 2008 crisis is an exemplary symptom os this problem, where PT increases faster than Py.”

Finally, he reminds us that a 100%-reserve banking system would suffer from an inelastic money supply that could not adequately accommodate changes in the demand for money, leading to monetary equilibrium issues.

I can’t reproduce the whole paper here, but it is full of very interesting (though quite technical) details and I strongly encourage you to take a look.

I am also a free banking theorist

George Selgin wrote a very true post on Freebanking.org. He claims that we are all, in a way or another, free banking theorists. Why? As Selgin very well explains:

Consider: an economist says that central banks prevent or limit the severity of financial crises, or that without mandatory deposit insurance even sound banks are likely to face runs, or that banks can never be expected to hold enough capital unless we force them to, or that commercially-supplied banknotes will tend to be discounted. All such claims–which is to say any claims about the need for or consequences of government intervention in banking–depend, if not on an explicit understanding of the nature and workings of a laissez-faire banking system, then on some implicit understanding. And this understanding in turn implies a theory of some sort, for reference to experience alone won’t suffice for drawing the sort of sweeping conclusions I’m talking about. It follows that all economists who have anything to say about the effects of government intervention in the banking system are either self-proclaimed free banking theorists or are free banking theorists who don’t admit (and perhaps don’t realize) it.

Indeed, most banking academic research studies and banking reform proposals base their ideas and models on certain assumptions of how the banking system, left to its own device, would behave, and how to correct the market failures that could possibly arise from such systems.

As my (and most people’s) experience can also testify, this tacit conventional wisdom is present in the mind of the general public and finance practitioners (I can still remember my father’s face when I told him we should get rid of central banks. Like he had just spotted some sort of ghost). The success of the usual US-centric misrepresentation of banking history is almost complete.

With this blog, I have been trying to explain what would (not) have happened if we had left banking free of all the rules that distort its natural behaviour. Seen this way, I am also a free banking theorist. I am trying to get back to the roots, asking questions such as: let’s supposed we never implemented Basel rules, would have real estate lending grown that much over the past three decades? What about securitization? Or interest rates on sovereign debt? And banks’ capital and liquidity buffers? What if we hadn’t had central banks nor deposit insurance over the period? What compounded what?

A lot of this is counterfactual, hence uncertain. Still, the intellectual challenge this represents is worth it, as current banking reformers and regulators still rely on and take for granted the inaccurate conventional story to justify the exponential growth of increasingly tight rules. Rules which, as I explain on this blog, are more likely to harm the banking system than to make it safer.

Larry White once says that free banks should be ‘anti-fragile’, and that the only reason they remain fragile is because of government-institutionalised rules that prevent them from self-correcting and learning. I have also already said that this does not mean that banks would never fail or that no crisis would ever occur. But it is likely that the accumulation of financial imbalances, which under our current system slowly emerge hidden behind the regulatory curtain until it is too late, would appear much sooner, limiting the destructive potential of any crisis. The market process, in order to become anti-fragile, needs to learn through experience. The more ‘safety’ rules one implement the less likely market actors will learn and the more likely the following crisis is going to be catastrophic. Institutionalised paternalism is self-defeating.

Unfortunately, the conventional story has seriously twisted everyone’s mind, and it is highly likely that any government announcing the end of the Fed/ECB/BoE/deposit insurance/currency monopoly would trigger market crashes and a lack of confidence in banks. Most commentators would describe the move as “crazy given what we’ve learnt from history”. In short, it would be a ‘history misreading-induced’ panic. While this would be short-lived, this would also be damaging. It is our role to tell the public that, in fact, it should not fear such changes. It should welcome them.

The rather curious and awkward alliance between statists and libertarians against free banking

Free banking has a very bad reputation within mainstream economics. As free banking scholars such as George Selgin, Larry White, Kevin Dowd or Steve Horwitz have been demonstrating over the past 30 years, this is mostly due to a misunderstanding of history. The track record of the systems that were as close as possible to free banking is crystal clear however: free banking episodes were more stable than any alternative banking frameworks.

However, this doesn’t seem to please many, from both sides of the political spectrum. Izabella Kaminska, a long-time libertarian critic from FT Alphaville, wrote a piece on the Alphaville blog partly criticizing non-central banking-based banking systems. In two separate replies (here and here), George Selgin highlighted all the self-serving ‘inaccuracies’ of her post (this is a euphemism). He also wrote a rebuttal in a follow-up post. Izabella skipped the interesting bits, accused Selgin of ad hominem, and wrote in turn another unsourced name-calling post on her own private blog. So much for the academic debate.

Perhaps more surprisingly, David Howden just posted a curious article on the Mises Institute website, which described the Fed as arising from “fractional-reserve free banks”. I say surprisingly, because Howden and the Mises Institute are at the other end of the political spectrum: libertarians, and often anarcho-capitalists. Nevertheless, he seemed to agree with Izabella Kaminska to an extent.

Unfortunately, Howden and Kaminska make the same mistake: they misread history, and/or focus far too much on US banking history. First, Howden claims that:

The year 1857 is a somewhat strange one for these clearinghouse certificates to make their first appearance. It was, after all, a full twenty years into America’s experiment with fractional-reserve free banking. This banking system was able to function stably, especially compared to more regulated periods or central banking regimes. However, the dislocation between deposit and lending activities set in motion a credit-fuelled boom that culminated in the Panic of 1857.

This could not be more inaccurate. The so-called ‘US free banking era’ had nothing much to do with free banking. And the credit boom and crises that follow were unrelated to either free banking or fractional reserves (see here for details, as well as below). I’d like Howden to explain why other fractional reserve free banking systems did not experience such recurring crises…

I have been left bewildered by Howden’s claim that privately-created clearinghouses were ‘illegal’ entities involved in ‘illegal’ activities (i.e. issuing clearinghouse certificates to get bank runs under control). Not only does this ironically sound like contradicting laissez-faire principles, but his whole argument rests on a lacking understanding of 19th century US banking.

What Howden got wrong is that, if American banks had such recurring liquidity issues before the creation of the Fed, it wasn’t due to their fractional reserve nature, but to the rule requiring them to back their note issues with government debt, thereby limiting the elasticity of those issues and the ability of banks to respond to fluctuations in the demand for money. Laws preventing cross-state branching also weakened banks as their ability to diversify was inherently limited. Banks viewed local clearinghouses as a way to make the system more resilient. It was a free-market answer to a state-created problem. This does not mean that the system was perfect of course. But Howden the libertarian blames a free-market solution here, and completely ignores the laws that originally created the problem.

Moreover, clearinghouses weren’t only a characteristic of the 19th century US banking system. They were present in several major free banking systems throughout history and set up by private parties (Scotland being a prime example). Their original goal wasn’t to create ‘illegal money claims’, but to help settle large volume of interbank transactions and economise on reserves: they were a necessary part of a well-functioning privately-owned free banking system. US clearinghouse certificates were merely a private solution to tame state-created liquidity crises. Those solutions were not perfect, but Howden is guilty of shooting the messenger here.

Clearinghouse-equivalents still exist today: the German savings and cooperative banks, as well as the Austrian Raiffeisen operate under the same sort of model, in which multiple tiny institutions park their reserves at their local central bank/clearinghouse. Finally, it is necessary to point out that clearinghouse would also surely exist in a full reserve banking system and would have the same basic goal: settle interbank payments.

Why a libertarian such as Howden would be against this natural laissez-faire process is beyond me. My guess is that at the end of the day, it all goes down to the fractional/full reserve banking debate within the libertarian space. Howden is trying at all costs to justify his views that full reserve banking would be more stable. But this time, such rhetoric is counter-productive and only demonstrates Howden’s ignorance of the issue (at least as described in this article). Using the fractional reserve argument to explain the 19th century US crises is self-serving and wholly inappropriate. Blaming a free-market reaction (i.e. the clearinghouse system) to such crises for the creation of the Fed completely misses the point. By doing so, and cherry-picking facts, Howden helps Kaminska’s arguments (despite fundamentally disagreeing with her) and shoots himself in the foot.

Update: I mistakenly thought that Peter Klein had written the article as his profile appeared on it. I should have paid more attention, but David Howden was the author. I have updated the post and apologised to Peter.

Update 2: I only just found out that David Glasner and Scott Sumner also wrote two good posts on free banking and Iza Kaminska/Selgin, followed by very interesting comments (here and here).

Photo: Marvel

Cato Institute’s 31st Monetary Conference – Was the Fed a good idea?

About two weeks ago, the US-based think tank Cato organised its annual monetary conference. Great panels and very interesting speeches.

Three panels were of particular interest to me: panel 1 (“100 Years of the Fed: What Have We Learned?”), panel 2 (“Alternatives to Discretionary Government Fiat Money”), panel 3 (“The Fed vs. the Market as Bank Regulator”).

In panel 1, George Selgin destroys the Federal Reserve’s distorted monetary history. Nothing much new in what he says for those who know him but it just never gets boring anyway. He covers: some of the lies that the Federal Reserve tells the general public to justify its existence, pre-WW2 Canada and its better performing monetary system despite not having a central bank, the lack of real Fed independence from political influence and……the Fed not respecting Bagehot’s principles despite claiming to do so. In this panel, the speech of Jerry Jordan, former President of the Federal Reserve Bank of Cleveland, is also very interesting.

In panel 2, Larry White speaks about alternatives to government fiat money, counterfeiting laws and state laws making it illegal to issue private money. Scott Sumner describes NGDP level targeting. Here again, nothing really new for those who follow his blog, but interesting nonetheless (even though I don’t agree with everything) and a must see for those who don’t.

In panel 3, John Allison provides an insider view of regulators’ intervention in banking (he used to be CEO of BB&T, an American bank). He argues that mathematical risk management models provide unhelpful information to bankers. He would completely deregulate banking but increase capital requirements, which is an original position to say the least. Kevin Dowd’s speech is also interesting: he covers regulatory and accounting arbitrage (SPEs, rehypothecation…) and various banking regulations including Basel’s.

Overall, great stuff and you should watch the whole of it (I know, it’s long… you can probably skip most Q&As).

PS: Scott Sumner also commented on the Pope’s speech on “evil incarnate”. Reminds me of the vocabulary I used…

News digest (Krugman and deregulation, central banking for Bitcoin…)

A looooooooot of news since the beginning of the week. So I’ll just quickly go over a few of them. Guys please, next time, spread your news more evenly over time. There was nothing to comment on recently!

Not new news but the Swedish bank regulators are thinking of increasing RWAs on mortgages to fight a growing housing bubble. Well, raising them to 25% (from 15% floor…) would still not change much: they would remain below most other asset classes’ level and securitisation (RMBS) would allow banks to bypass the restrictions.

Meanwhile, Yves Mersch, member of the Executive Board of the ECB, spoke about how to revive SME lending in bank-reliant Europe. His solutions involve: strengthening banks, securitisation and… banking union. Any word of capital requirements/risk-weighted assets? Not a single one. When I told you that central bankers don’t seem to get it…

But the UK government wants to ditch the household lending side of the Funding for Lending Scheme! They now only want to provide cheap funding to banks if they prove that they lend to SMEs. Why not, but I doubt it would really work for a few reasons: 1. demand for loans remains quite low, 2. market funding remains cheap (it was cheaper than FLS), 3. banks haven’t drawn much on it anyway, 4. RWAs are still in place! Mortgage and household lending will still attract most of lending volume as it is more profitable from a capital point of view.

Meanwhile (again), SME financing from alternative lenders not subject to RWAs and other stupid capital rules, keeps growing in the UK. However, it is still tough for those lenders to assess the health of the companies that would like to lend to.

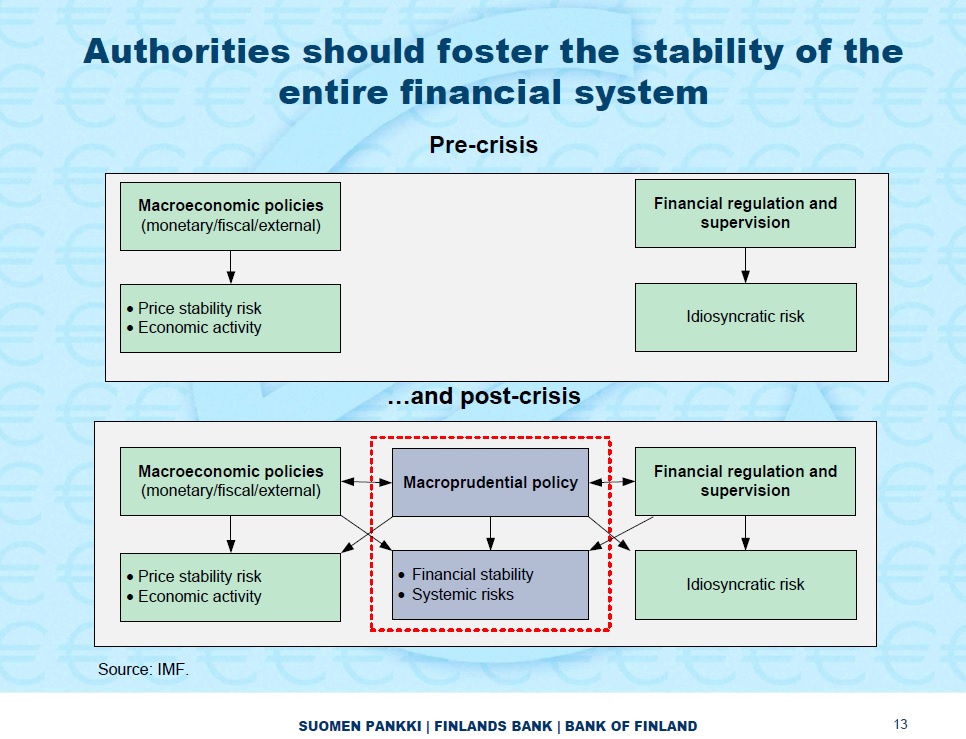

Erkki Liikanen, the Governor of the central bank of Finland, told us about his ideas to improve financial stability. Surprise: they haven’t changed. So macroprudential policy starts interfering with macroeconomic policies and financial regulation, with possibly opposite effects that don’t seem to bother him much. Look at that slide, which is the very definition of a messy policy goal, with multiple targets and interferences:

A very strange piece in the Washington Post: Bitcoin needs a central banker. Wait a second. No, it’s definitely not the 1st of April. First, the author asserts that Bitcoin’s wild changes in value make it difficult to be adopted as a currency. This is extraordinary. Does the author even understand FX rates? If the author wishes to purchase his coffee using Euros, despite the coffee being priced in Dollars, will he also declare that the fact the Euro’s value is unstable (making the effective Euro price of its coffee volatile) makes the currency improper for use? When prices are originally denominated in Bitcoin, the change in the value of the digital currency won’t affect them. When prices are actually denominated in USD, but converted into Bitcoin, then yes, changes in the value of the digital currency will affect them. But this is hardly Bitcoin’s fault… Then he gets mixed up with ‘menu costs’, ‘hyperinflation’, ‘money demand’, etc. Wow. Just one last thing: has he even understood that Bitcoin was designed to be free from central bankers and government intervention in the first place?

Izabella Kaminska in the FT wrote a new piece on Bitcoin and other alternative electronic currencies. She complains about the multiplication of such currencies that nothing backs and pretty much only see speculative motivations underlying them. I am not going to comment on the whole thing, but whether right or wrong, she should ask herself why there is such frenzy about those currencies at the moment. My guess is that, governments’ and central banks’ manipulation of their own currencies have unleashed a beast: people afraid to hold classic currencies started to look for alternatives, pushing up their prices, in turn attracting speculators. The process is similar to ‘bad’ financial innovations (the ones designed specifically to bypass restricting regulation): they often start as a benign innovation for the ‘common good’, but the surprising demand for them and large profits attract speculators until the market crashes. Not the fault of the innovation, but the fault of the regulation that triggered them…

Paul Krugman thinks that “the trouble with economics is economists”, and that mainstream economics is not to blame for the financial crisis. I partly disagree: 1. there are various schools of thought within mainstream economics that often disagree with each other altogether and 2. most (all?) of them cannot fully explain the crisis anyway. But, and this is where Krugman shows his limited knowledge of banking and therefore the limit of his reasoning, he declares that “the mania for financial deregulation, for example, didn’t come out of standard economic analysis.” I’m sorry? Which mania for financial deregulation? The international banking sector had never been as regulated in history as on the eve of the crisis! (even taking into account of the few one-off deregulations) I need to come back to this in a subsequent post. Really, Paul, you have to revise your history. And your reasoning.

On Free Banking, George Selgin urges Scots to ‘poundize’ unilaterally if ever they declare independence from the UK. And “if the British Parliament refuses to cooperate, so much the better. Who knows: Scotland could even end up with a banking system as good as the one it had before 1845, when Parliament, which knew almost as little about currency then as it does now, began to bugger it up.” If only Scotland could enlighten the world a second time and get back to a free banking system!

The ‘great search for yield’ update, Taleb on bank disintermediation and Coeuré on Wicksell

This is a quick update on my post of last week on the rush for yield among private investors and what it meant in terms of interest rate disequilibrium.

Following my post, Thomas Aubrey from Credit Capital Advisory kindly provided me with an update of his ‘Wicksellian differential’ chart. You can also find it here.

As you can see the differential between the estimated natural rate and the money rate of interest in the US have kept increasing and almost reached pre-crisis peak. According to his calculation, the potential differential now reaches………10%. It’s indeed huge. Try for a second to imagine the Fed all of a sudden increasing their target interest rate by 10%…… No you’re right, we just can’t imagine it. Frankly, I hope his calculation is wrong but…I wouldn’t bet my life on it. Consequently, Thomas Aubrey believes that it backs up my claim about malinvestments.

As you can see the differential between the estimated natural rate and the money rate of interest in the US have kept increasing and almost reached pre-crisis peak. According to his calculation, the potential differential now reaches………10%. It’s indeed huge. Try for a second to imagine the Fed all of a sudden increasing their target interest rate by 10%…… No you’re right, we just can’t imagine it. Frankly, I hope his calculation is wrong but…I wouldn’t bet my life on it. Consequently, Thomas Aubrey believes that it backs up my claim about malinvestments.

Meanwhile, in a speech called ‘The economic consequences of low interest rates’ at the International Center for Monetary and Banking Studies on the 9 October, Benoit Coeuré, member of the Executive Board of the European Central Bank, misunderstood Wicksell and inflation, justifying very low interest rates. Not only Mr Coeuré seems to believe that CPI adequately reflects inflation, but also, according to him, inflation is always zero when the money rate of interest equals the natural rate. This is not true: real shocks can temporarily push inflation one way or another, but over the longer term productivity becomes the main driver behind inflation and deflation. In a world of productivity increases (and increasing output), deflation should be the norm (as it was the case at the end of the 19th century and early 20th). A zero level of inflation in this context would actually mean that there is hidden inflation. George Selgin has written a lot on this. See his Less than Zero book or this video.

Last Friday, FT’s Henny Sender discussed the Fed’s impact on markets. According to a Hong Kong-based hedge fund “the Fed is always there. It is clear that it will not tolerate a decline in asset values. If you sell in the face of QE, you look like an idiot.” Sounds like the best way to completely distort markets. Free markets you said?

Today, John Authers, in another FT piece, says that “Western economy is overcentralised, creating extra risk”. I obviously won’t disagree with him. He cites Nicholas Taleb (reminding me of Larry White). But one thing particularly struck me: Taleb seems to think that hedge funds “are developing strategies that aim to disintermediate the banks, such as loan funds.” This is very, very close to my own opinion, which I haven’t mentioned yet on this blog: technological developments will enable shadow banking to grow under one form or another to desintermediate credit creation. This is something big, and it will require many blog posts and possibly a research paper…and some time.

Recent Comments