More on the natural rate of interest

Since my recent post on Wicksell, a number of famous economists have also blogged on the Wicksellian ‘natural’ rate of interest.

Tyler Cowen asked ‘what’s the natural rate of interest?’ and has a few interesting points. Paul Krugman responds to Cowen by making the usual mistake (albeit shared by most mainstream academics) of defining the natural Wicksellian rate as the “the rate of interest at which the economy would be more or less at full employment, which in turn implies that inflation will be more or less stable.” He adds that there is no reasonable case that interest rates are kept artificially low. Meanwhile, on Econlog, Scott Sumner added that there was “nothing natural about the natural rate of interest” and added some comments and charts on his own blog, declaring that the natural rate is surely negative.

Cowen in turn responded to Krugman, highlighting that risk was not a good reason to justify low risk-free natural rates. He elaborates on a few points, but one in particular was, I believe, spot on: what he calls “growing legal and institutional requirements for T-Bills as collateral”. While he believes that this hypothesis still has to be demonstrated empirically, he linked to a 2-year old post of his I had missed in which he discusses this theory in more detail.

Here are his first few points:

1. Imagine that financial institutions and traders have to hold large quantities of T-Bills (and similar assets) to participate in financial markets. That may be to satisfy collateral requirements, to meet government regulations, to be credible in private market transactions, and so on.

2. The demand for these assets is now so high and so persistent that the assets have persistently low nominal returns and often negative real returns.

3. The holders of these assets do not however receive negative returns on their portfolio as a whole, when deciding to hold these T-Bills. Holding the T-Bills is like paying an entry fee into financial markets. And once they are in financial markets of the right kind, these market players can earn high returns by possessing special trading technologies (the technology may vary across market participants, but think HFT, hedge funds, prop trading, employing quants, and so on).

4. Let’s say you are not a major financial institution. Then you really will earn negative returns on your safe saving. You might try holding equities, but a) you are not wealthy and thus you are fairly risk averse, and b) as a small player you do not have access to these special trading technologies and indeed you must trade against those who do. You thus will often earn negative or low returns on your portfolio no matter what.

5. The implied prediction is that differential rates of wealth accumulation will be a driver of inequality over time. This seems to be the case.

It is sad that Cowen is not an expert in banking and financial regulation, because he had a remarkable insight there.

US Treasury yields (as well as most government-issued securities and a number of highly-rated corporate ones) do not reflect the ‘natural’ supply and demand of the market. Instead, demand is artificially raised by financial regulation, as I have explained in a number of posts (see this previous blog post on the BIS, which explained how its recent financial reforms will impact a number of reference rates, and also this post for instance). This is where Krugman is wrong when he says that interest rates are not kept artificially low. While we can argue whether or not the Fed and other central banks manipulate rates downward, there is no argument here: regulation does push a number of reference interest rates down.

This was also the case (to a lesser extent) in the post-war era, making Scott Sumner’s reasoning inaccurate, as pointed out by one his commenters. Remarkably, Scott seemed to agree that this might indeed be a good point. Over the past three decades, regulation has fundamentally influenced the demand for a number of assets, modifying their market prices/yields in the process. Any comprehensive analysis, from the causes of the crisis to secular stagnation, should take those microeconomic changes into account. I have read countless academic papers over the past few years, and almost none did. They seemed to consider that banking behaviour and incentives were (mostly) constant over time. They weren’t.

So a number of economists might be slowly waking up to the fact that financial market prices are not freely determined, which seriously constrains our ability to reach conclusions based on market trends. There are many other underlying drivers (the ‘microeconomics of banking’ that I keep mentioning) that are at play.

PS: Marcus Nunes has an interesting post on determining (or not) the natural rate of interest. I agree that there is no point trying to determine the rate to target it.

News digest: P2P lending and HFT, CoCo bonds, Co-op Bank…

Ron Suber, President at Prosper, the US-based P2P lending company, sent me a very interesting NY Times article a few days ago. The article is titled “Loans That Avoid Banks? Maybe Not.” This is not really accurate: the article indeed mentions institutional investors such as mutual and hedge funds increasingly investing in bundles of P2P loans through P2P platforms, but never refers to banks. Unlike what the article says, I don’t think platforms were especially set up to bypass institutional investors… They were set up to bypass banks and their costly infrastructure and maturity transformation.

Some now fear that the industry won’t be ‘P2P’ for very long as institutional investors increasingly take over a share of the market. I think those beliefs are misplaced. Last year, I predicted that this would create opportunities for niche players to enter the market, focusing on real ‘P2P’.

A curious evolution is the application of high-frequency trading strategies to P2P. I haven’t got a lot of information about their exact mechanisms, but I doubt they would resemble the ones applied in the stock market given that P2P is a naturally illiquid and borrower-driven market.

The main challenge of the industry at the moment seems to be the lack of potential customer awareness. Despite offering better deals (i.e. cheaper borrowing rates) than banks, demand for loans remains subdued and the industry tiny next to the banking sector.

In this FT article, Alberto Gallo, head of macro-credit research at RBS, argues that regulators should intervene on banks’ contingent convertible bonds’ risks. I think this is strongly misguided. Investors’ learning process is crucial and relying on regulators to point out the potential risks is very dangerous in the long-term. Not only such paternalism disincentives investors to make their own assessment, but also regulators have a very bad track record at spotting risks, bubbles and failures (see Co-op bank below).

This piece here represents everything that’s wrong with today’s banking theory:

We know that a combination of transparency, high capital and liquidity requirements, deposit insurance and a central bank lender of last resort can make a financial system more resilient. We doubt that narrow banking would.

Not really… They also argue that 100% reserve banking would not prevent runs on banks:

The mutual funds of the narrow banking world would be subject to the same runs. Indeed, recent research highlights that – in the presence of small investors – relatively illiquid mutual funds are more likely to face exit in the event of past bad performance. […] Since the mutual funds would be holding illiquid loans – remember, they are taking over functions of banks – collective attempts at liquidation to meet withdrawal requests would lead to ruinous fire sales.

They misunderstand the purpose of such a banking system. Those ‘mutual funds’ would not be similar to the ones we currently have, which invests in relatively liquid securities on the stock market, and can as a result exit their positions relatively quickly and easily. Those 100% reserve funds would invest in illiquid loans and investors in those funds would have their money contractually locked in for a certain time. With no legal power to withdraw, no risk of bank run.

The FT reported a few days ago the results of the investigation on the Co-operative bank catastrophe. Despite regulators not noticing any of the problems of the bank, from corporate governance to bad loans and capital shortfall, as well as approving unsuitable CEOs and mergers, the report recommends to… “heed regulatory warnings.” I see…

The impossible sometimes happens: I actually agree with Paul Krugman’s last week piece on endogenous money. No guys, the BoE paper didn’t reveal any mystery of banking or anything…

Finally, Chris Giles wrote a very good article in the FT today, very clearly highlighting the contradictions in the Bank of England policies and speeches, and their tendency to be too dovish whatever the circumstances:

Mark Carney, the governor, certainly displays dovish leanings. Before he took the top job, he said monetary policy could be tightened once growth reached “escape velocity”. But now that growth has shot above 3 per cent, he advocates waiting until the economy has “sustained momentum” – without acknowledging that his position has changed. His attitude to prices also betrays a knee-jerk dovishness. When inflation was above target, he stressed the need to look at forecasts showing a more benign period ahead. Now that inflation is lower it is apparently the short-term data that matters – and it justifies stimulus.

So much for forward guidance… Time to move to a rule-based monetary policy?

Fiat money is backed by men with guns

Only a quick post today unfortunately (I’ve been working on another looooooooooooong post over the last few days).

However, I thought I should mention at least two things.

Yesterday, Lawrence Summers published a piece in the Financial Times about his secular stagnation theory. Anything new? Nop. Like nothing had happened since he first mentioned the concept. Like if his original speech had never triggered a great debate among economists. So he obviously didn’t address any of the counter-arguments made by other people… Ivory towers anyone?…

About a week ago, Bob Murphy had a ‘funny’ post on Krugman. Remember when I said that fiat money wasn’t backed by the ‘productive capacity of the country’ and other meaningless abstract concepts like that? Krugman seems to agree… Well… sort of, as he believes that fiat money is backed by… men with guns!… which gives fiat money its value… Nice type of money, that’s for sure. I love the sense of liberty that some Keynesians have.

The Financial Times on Bitcoin, P2P lending and secular stagnation

The FT has a few articles on some of my favourite topics today.

John Authers argue that it is time to take Bitcoin seriously. Who would say that I disagree? In his article he refers to several points I had already mentioned in some of my previous posts. He adds an interesting analogy with previous internet firms and concepts:

[…] even if Bitcoin is as successful as it is possible now to imagine, it looks overvalued at recent prices. It is in a bubble.

But this does not prove that the concept has no future. Shares in Amazon.com were also in a bubble in the late 1990s, and yet proved a great long-term investment after the bubble burst. Wild swings in value are typical when new technologies arrive.

A commenter also had a very good point, which highlighted Bitcoin’s (or other similar alternative digital currencies’) potential trade-boosting abilities:

Can you imagine a world where anyone can set up a shop on the internet and instantly accept payments from all over the world to sell its product or service without any intermediary? Well that’s only one face of what Bitcoin enables.

Naysayers will keep saying that Bitcoin is useless or only diverts wealth from ‘productive opportunities’ anyway.

FT Alphaville continued its long tradition of confused/confusing posts with this one on P2P lending today. I don’t know about you, but it does look to me that everything in the financial world that’s innovative and far from regulators’ grip is now under attack from Alphaville bloggers. They could have a point. But in this case, they don’t. They completely miss the point. The author misunderstands the financial crisis and draws the wrong conclusions from it.

According to the author, P2P is ‘pro-cyclical’ and has ‘no skin in the game’, which makes this asset class of systemic risk. He’d like to see P2P platforms to hold capital buffers to absorb losses. This makes no sense whatsoever. P2P is an investment. There are tons on possible investments. Anybody can invest directly in equities or bonds or FX or whatever, or through mutual funds/investment managers. P2P works the same way. Are we asking mutual funds to hold a capital buffer to absorb losses suffered by their clients’ portfolio? Of course not.

Banks need to retain capital as they hold deposits, which are part of the money supply and can be drawn down at any time by depositors, and also because they play a critical role in the payment system. If banks make losses on lending, capital allows them not to transfer the loss onto customers, who often just wanted to store their money there. This has absolutely nothing to do with the kind of voluntary investments I described above. Moreover, some P2P platforms have already set up loss-absorbing funds anyway… Platforms also have their ‘skin in the game’: if everybody stops lending through them, they don’t earn any revenue and go out of business. While I agree that platforms should not hide the fact that losses could occur on P2P investments, paternalism and regulation is the wrong way to go. Education and responsibility should be the goals.

In another Alphaville blog post, Izabella Kaminska reports the arguments of two economists against the Summers/Krugman secular stagnation story. And it basically reflects mine: it doesn’t exist. It also has a particular Austrian flavour: savings and productivity generate long-term economic growth, and low interest rates caused the economy to boom above potential (debt accumulation) and caused malinvestments (investments that generated short-term growth but that no one wanted in the end).

• There is no shortage of high return investment projects in the world. And the dearth of global corporate investment, which drove the great recession, means that productive potential is shrinking despite corporate profitability, leverage and cash balances being sound.

• The three ingredients for growth are a) a stable macro environment; b) a sound banking system; c) economic reforms that encourage entrepreneurship. What is missing right now is private sector confidence in the ability of governments and central bankers to provide all three.

• Credit bubbles can boost growth only temporarily and incur heavy costs in terms of subsequent deleveraging and misallocation of resources.

Hedge funds keep attracting new money (assets under management are up 16% since end-2012)… I won’t remind you that I’m wondering whether or not this is a sign that nominal interest rates are lower than their Wicksellian natural rates, forcing investors to take extra risk to achieve the real rates of return they would normally obtain from safer investments. But I guess that Summers and Krugman would say that, anyway, bubbles are necessary for the economy. Another side of the story is that not that many people seem to believe anymore in hedge funds outperforming the markets. Hedge funds seem to be transformed into mutual funds… But in this case, why paying such high management and performance fees? This doesn’t make so much sense.

A brief comment on Blackrock, groupthinking and ‘secular stagnation’

Two interesting articles on Blackrock, the world’s largest asset manager (here and here) in this week’s Economist. The Economist is right to point out that regulators would be wrong to classify Blackrock as systematically important, which would considerably increase its regulatory burden. Unlike banks, Blackrock (and other asset managers) transfers money rather than creates it. As a result, there is no risk of ‘secondary deflation’, or money supply contraction, during a crisis if the value of its assets under management fall or if Blackrock itself fails. If markets collapse, investors take the hit, not Blackrock or any other asset manager (although they do take a hit to their revenues as assets under management fall). Of course, investors suffering from a fall in asset value can have other repercussions on the economy. But at least the collapse is not made worse by banks contracting their lending or failing, putting pressure on the money supply at the very moment money demand jumps.

The other issue raised by The Economist is about ‘groupthinking’, as many investors now use the asset manager’s analytics platform to guide them in their investment and trading decisions. The Economist is right on that topic too. However, I would say that groupthinking does not only emanate from Blackrock’s platforms… It is probably a topic I’ll discuss more in details another time, but we could argue that financial exams such as the CFA also push towards groupthinking by making it compulsory to follow certain analytical frameworks while not offering any real alternative. Therefore investors end up using the same models. Various investors will evidently come up with differing inputs; but those would then pass through the same machinery and outputs would be only slightly different.

A quick note on the fashionable ‘secular stagnation’, Lawrence Summers’ and Paul Krugman’s new favourite topic (actually, I don’t know). Apparently, there aren’t enough productive investments in the world relative to the stock of savings. The “appetite to invest” (in The Economist’s words) is low.

I found an interesting short video yesterday:

Does it remind you anything? I’ve argued many times over the past few months that there are indeed plenty of productive investments, but that entrepreneurs and investors are too scared to invest due to regime uncertainty and red tape (see also here and here). Let’s name a few: fracking, mobile IT, emerging markets, commercial space ventures, drones, green energy… And I’m surely forgetting a lot. Yet, so many economists try to reach conclusions from analysing a few aggregated macro-economic data while forgetting to take a look at what’s going on the micro-economics side. This is a big mistake.

News digest (Krugman and deregulation, central banking for Bitcoin…)

A looooooooot of news since the beginning of the week. So I’ll just quickly go over a few of them. Guys please, next time, spread your news more evenly over time. There was nothing to comment on recently!

Not new news but the Swedish bank regulators are thinking of increasing RWAs on mortgages to fight a growing housing bubble. Well, raising them to 25% (from 15% floor…) would still not change much: they would remain below most other asset classes’ level and securitisation (RMBS) would allow banks to bypass the restrictions.

Meanwhile, Yves Mersch, member of the Executive Board of the ECB, spoke about how to revive SME lending in bank-reliant Europe. His solutions involve: strengthening banks, securitisation and… banking union. Any word of capital requirements/risk-weighted assets? Not a single one. When I told you that central bankers don’t seem to get it…

But the UK government wants to ditch the household lending side of the Funding for Lending Scheme! They now only want to provide cheap funding to banks if they prove that they lend to SMEs. Why not, but I doubt it would really work for a few reasons: 1. demand for loans remains quite low, 2. market funding remains cheap (it was cheaper than FLS), 3. banks haven’t drawn much on it anyway, 4. RWAs are still in place! Mortgage and household lending will still attract most of lending volume as it is more profitable from a capital point of view.

Meanwhile (again), SME financing from alternative lenders not subject to RWAs and other stupid capital rules, keeps growing in the UK. However, it is still tough for those lenders to assess the health of the companies that would like to lend to.

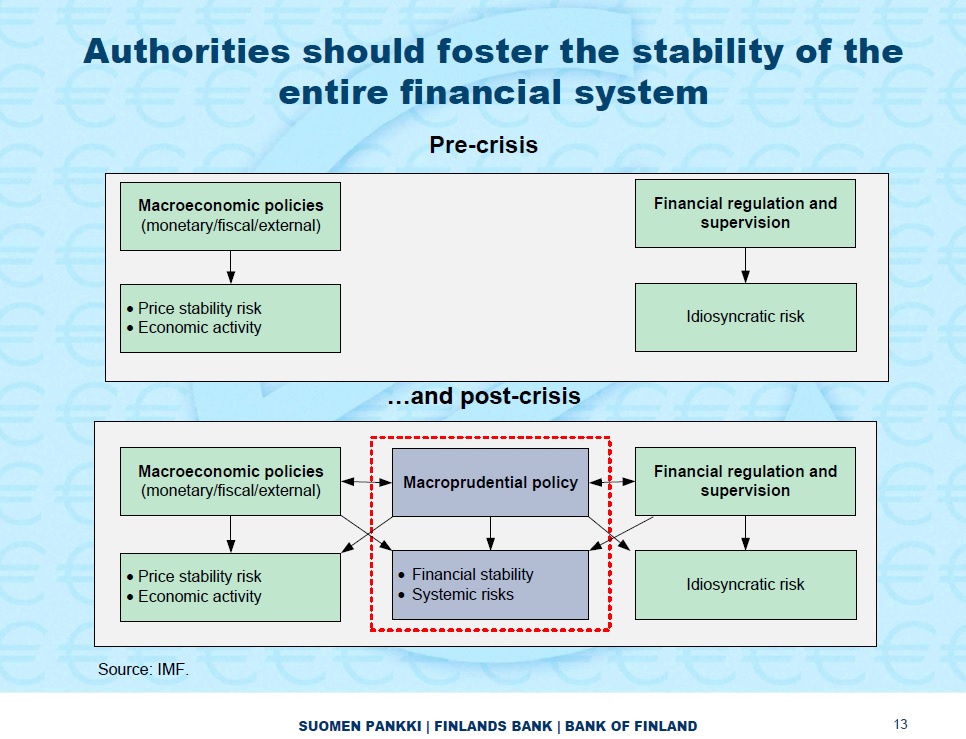

Erkki Liikanen, the Governor of the central bank of Finland, told us about his ideas to improve financial stability. Surprise: they haven’t changed. So macroprudential policy starts interfering with macroeconomic policies and financial regulation, with possibly opposite effects that don’t seem to bother him much. Look at that slide, which is the very definition of a messy policy goal, with multiple targets and interferences:

A very strange piece in the Washington Post: Bitcoin needs a central banker. Wait a second. No, it’s definitely not the 1st of April. First, the author asserts that Bitcoin’s wild changes in value make it difficult to be adopted as a currency. This is extraordinary. Does the author even understand FX rates? If the author wishes to purchase his coffee using Euros, despite the coffee being priced in Dollars, will he also declare that the fact the Euro’s value is unstable (making the effective Euro price of its coffee volatile) makes the currency improper for use? When prices are originally denominated in Bitcoin, the change in the value of the digital currency won’t affect them. When prices are actually denominated in USD, but converted into Bitcoin, then yes, changes in the value of the digital currency will affect them. But this is hardly Bitcoin’s fault… Then he gets mixed up with ‘menu costs’, ‘hyperinflation’, ‘money demand’, etc. Wow. Just one last thing: has he even understood that Bitcoin was designed to be free from central bankers and government intervention in the first place?

Izabella Kaminska in the FT wrote a new piece on Bitcoin and other alternative electronic currencies. She complains about the multiplication of such currencies that nothing backs and pretty much only see speculative motivations underlying them. I am not going to comment on the whole thing, but whether right or wrong, she should ask herself why there is such frenzy about those currencies at the moment. My guess is that, governments’ and central banks’ manipulation of their own currencies have unleashed a beast: people afraid to hold classic currencies started to look for alternatives, pushing up their prices, in turn attracting speculators. The process is similar to ‘bad’ financial innovations (the ones designed specifically to bypass restricting regulation): they often start as a benign innovation for the ‘common good’, but the surprising demand for them and large profits attract speculators until the market crashes. Not the fault of the innovation, but the fault of the regulation that triggered them…

Paul Krugman thinks that “the trouble with economics is economists”, and that mainstream economics is not to blame for the financial crisis. I partly disagree: 1. there are various schools of thought within mainstream economics that often disagree with each other altogether and 2. most (all?) of them cannot fully explain the crisis anyway. But, and this is where Krugman shows his limited knowledge of banking and therefore the limit of his reasoning, he declares that “the mania for financial deregulation, for example, didn’t come out of standard economic analysis.” I’m sorry? Which mania for financial deregulation? The international banking sector had never been as regulated in history as on the eve of the crisis! (even taking into account of the few one-off deregulations) I need to come back to this in a subsequent post. Really, Paul, you have to revise your history. And your reasoning.

On Free Banking, George Selgin urges Scots to ‘poundize’ unilaterally if ever they declare independence from the UK. And “if the British Parliament refuses to cooperate, so much the better. Who knows: Scotland could even end up with a banking system as good as the one it had before 1845, when Parliament, which knew almost as little about currency then as it does now, began to bugger it up.” If only Scotland could enlighten the world a second time and get back to a free banking system!

The ivory tower economist syndrome

Here we go. Academic economists are lost. Lawrence Summers just made a striking announcement in a speech a few days ago: we are likely to be in a secularly stagnating economy that needs recurrent bubbles to achieve full employment, as its natural rate of interest has been constantly below zero for a while. Evidently, Krugman, Sumner, Cowen, Wolf and many other economists started to discuss the issue. Some agree, some don’t. However, most seem to miss the main problem. I call that the ivory tower economist syndrome. Abstractly thinking in terms of aggregated economic figures locked in a university or government office won’t be of much help. Zerohedge rightly makes fun of Summers and Krugman, as the satiric newspaper The Onion made the same economic advices a few years ago:

Congress is currently considering an emergency economic-stimulus measure, tentatively called the Bubble Act, which would order the Federal Reserve to† begin encouraging massive private investment in some fantastical financial scheme in order to get the nation’s false economy back on track.

Who said that was fiction?

Many of them are backing their ideas using wrong arguments. For instance, Summers and Krugman don’t believe interest rates were too low before the crisis as… there was no inflation! Sure, but, how do you know that? CPI? RPI? GDP deflator? There are many problems with inflation figures. Let’s list some of them:

- They don’t accurately reflect inflation. You can change the calculation and the result changes dramatically. Moreover, the goods picked to calculate them and the weights applied to them are quite arbitrary. This is supposed to reflect the ‘average’ household basket. Well, I am not the average household apparently as my own inflation rate has been way higher than headline inflation over the past few years.

- 0% CPI increase does not mean that there is no inflation. Productivity increase drives inflation down. As a result, reasoning in terms of headline inflation is a mistake. Real inflation is hidden. The fastest economic growth in the history of the Western world (late 19th and early 20th century) occurred during a long period of secular deflation…

- Most asset prices aren’t reflected in inflation figures. Newly created money now mostly go to investments, a lot of which being speculation. Most of banks’ lending is mortgage lending. So newly-created money goes to housing, pushing up prices… which aren’t reflected in inflation figures. Sure, one can argue that, at some point, there will be inflationary pressure on consumer goods. But productivity increases reducing the price of domestically-produced goods (IT revolution anyone?) and cheap goods from developing countries mask that process. Moreover, when asset bubbles burst (which they eventually do), the wealth effect from asset price increases that could lead to inflation all but disappears. Lending was also different 50 or 100 years ago: much lending did not go directly to investments in financial or real assets. Consequently consumer goods inflation appeared a lot faster after new monetary injection (considering stable productivity).

So justifying the fact that nominal interest rates defined by central banks were not low because there was no inflation is in itself wrong, or at best inaccurate. In reality, low interest rates are very likely to have caused, or at least participated, in the recent credit bubble. Regarding the so-called ‘savings glut’, Cowen agrees with Kling on the fact that, if we really had ‘too much’ savings chasing ‘too few’ investment opportunities, we would not need central banks’ actions to push interest rates lower. The supply and demand of loanable funds would automatically drive the interest rate to a very low level.

But, most importantly, all those economists forget a fundamental fact that I have been mentioning a hundred times recently: regime uncertainty (yes, again…). For economists to speak in terms of monetary and spending aggregates alone and to not pay attention to the broader context surrounding businesses is a major mistake. I’ve kept repeating and giving many evidences recently (like here, here, and here) that businesses currently delay investments due to the uncertain regulatory and economic decisions taken by governments and regulators all around the world. This is now the major issue for SMEs and banks at least. Again today, Euromoney published an interesting short article on ‘renewed regulatory uncertainty’ for banks:

For all the populist fervor then about perceived policy inaction to address systemic risk, many banks see it differently: investor flight from banks’ equity and bond products has taken root over the years, amid fears that new rules will render business models uneconomic.

Take a look at that SEB and Deloitte chart summarising current regulatory reforms. It looks slightly messy doesn’t it? And look how it is named…

A bank analyst told Euromoney that:

Changes in regulations, changes in what other stakeholders consider to be acceptable, the risk that the behaviours of certain employees become associated with the institution as a whole – those are indeed much more expensive for banks these days than credit [risk].

As I have already highlighted in an earlier post, more than the number of rules, it is the fact that rules change that is crucial to business planning. You can’t play a certain game if the rules of the game constantly change. Yet none of those ‘great’ economists ever mentioned regulation, uncertainty, rules or anything related. Looks like abstract economic aggregates are a lot more interesting to manipulate…

Get out of your tower guys!

Recent Comments