McKinsey on banking and debt

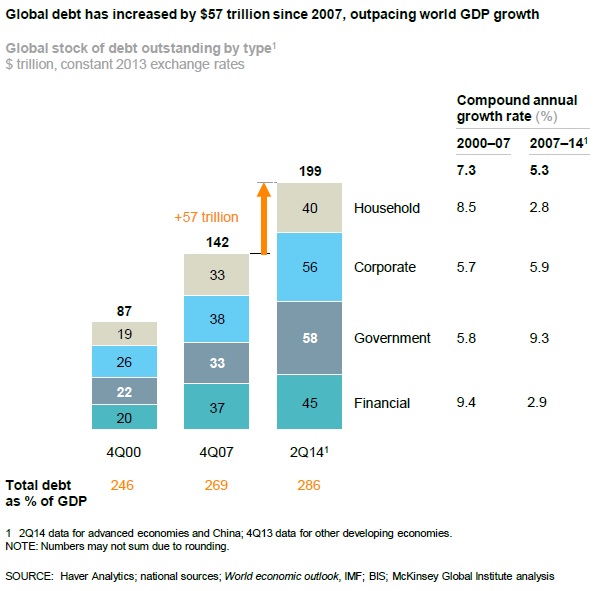

A recent report by the consultancy McKinsey highlights how much the world has not deleveraged since the onset of the financial crisis. Many newspapers have jumped on the occasion to question whether or not the policies adopted since the crisis were the right ones (FT, Telegraph, The Economist…). This is how the total stock of debt has evolved since 2000:

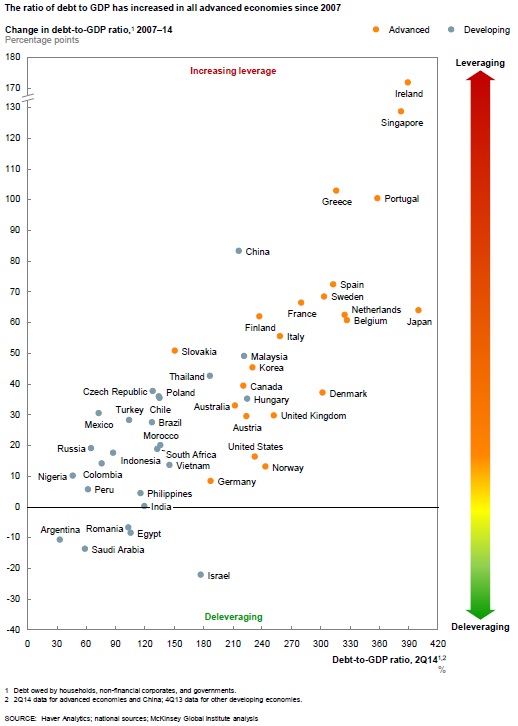

As the following chart shows, the vast majority of countries saw their overall level of debt increase:

As the following chart shows, the vast majority of countries saw their overall level of debt increase:

McKinsey affirms that “household debt continues to grow rapidly, and deleveraging is rare”, and that the same broadly applies to corporate debt. China is an extreme case: total debt level, as a share of GDP, grew from 121% of GDP in 2000, to 158% in 2007 to…282% at end-H114. And growing.

McKinsey affirms that “household debt continues to grow rapidly, and deleveraging is rare”, and that the same broadly applies to corporate debt. China is an extreme case: total debt level, as a share of GDP, grew from 121% of GDP in 2000, to 158% in 2007 to…282% at end-H114. And growing.

Unsurprisingly, household debt is driven by mortgage lending (including in China). It isn’t a surprise to see house prices increasing in so many countries. How this is a reflection that we currently are in a sustainable recovery, I can’t tell you. How this is a signal that monetary policy has been ‘tight’, I can’t tell you either. If monetary policy has indeed been ‘tight’, then it shows the power of Basel regulation in transforming a ‘tight’ monetary policy into an ‘easy’ one for households through mortgage lending. How this total stock of debt will react when interest rates start rising is anyone’s guess…

McKinsey’s claim that “banks have become healthier” is questionable at best, as they use regulatory Tier 1 ratios as a benchmark. Indeed a lot of banks have boosted their Tier 1 ratio by reducing RWA density (i.e. the average risk-weight applied to their assets) rather than actually raising or internally generating extra capital.

As expected given how capital intensive corporate lending has become thanks to our banking regulatory framework, and in line with recent research, banks are now mostly funding households at the expense of businesses:

As expected given how capital intensive corporate lending has become thanks to our banking regulatory framework, and in line with recent research, banks are now mostly funding households at the expense of businesses:

McKinsey highlights that P2P lending, while still small in terms of total volume, doubles in size every year, and is mostly present in China and the US.

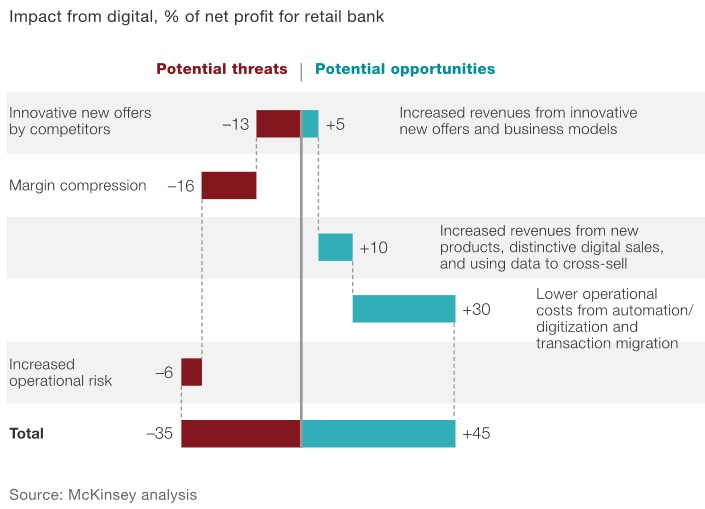

And in fact, in another article, McKinsey explains that the digital revolution is going to severely hit retail banking. I have several times described that banks’ IT systems were on average out-of-date, that this weighed on their cost efficiency and hence profitability, and that it even possibly impaired the monetary policy transmission channel. I also said that banks needed to react urgently if they were not to be taken over by more recent, more efficient, IT-enabled competitors. A point also made in The End of Banking, according to which technology allows us to get rid of banks altogether.

McKinsey is now backing up those claims with interesting estimates. According to the consultancy, and unsurprisingly, operating costs would be the main beneficiary of a more modern IT framework:

McKinsey goes as far as declaring that:

McKinsey goes as far as declaring that:

The urgency of acting is acute. Banks have three to five years at most to become digitally proficient. If they fail to take action, they risk entering a spiral of decline similar to laggards in other industries.

Unfortunately, current extra regulatory costs and litigation charges are making it very hard for banks to allocate any budget to replace antiquated IT systems.

If banks already had those systems in place as of today, I would expect to see lending rates declining further – in line with monetary policy – across all lending products as margin compression becomes less of an issue. In a world where banks have zero operating cost, its net interest income doesn’t need to be high to generate a net profit.

In the end, regulators are shooting themselves in the foot: not only new regulations and continuous litigations may well have the effect of facilitating new non-banking firms’ takeover of the financial system, but also monetary policy cannot have the effect that regulators/central bankers themselves desire.

The end of banking? Not like this please

I recently read Jonathan McMillan’s The End of Banking, which I first heard of through FT Alphaville here (McMillan is actually a pseudonym to cover it two authors: an academic and a banker). I have mixed feelings about this book. I really wanted to agree with it. And I do, to some extent. But I simply cannot agree with a number of other points they make.

Their proposal to reform banking is as follows (see the book for details): lending can be disintermediated through P2P lending platforms (and equivalent), which both monitor potential borrowers through credit scoring and allocate savers’ funds to minimise the probability of losses. Marketplaces set up by platforms would enable savers to sell their investments to generate cash if needed. What about the payment system? Their solution is for non-bank FIs to continuously provide market liquidity a number of financial instruments using algorithmic trading. Current accounts would in fact be invested like mutual funds, which would instantly convert those investments into cash when required for payment. They also propose accounting rule changes to prevent corporations from creating money-like instruments.

As such, they propose to end banks’ inside money and have a financial system exclusively based on digital outside money controlled by a monetary authority. While they don’t classify it this way, it does seem to me to be some sort of 100%-reserve banking proposal: the money supply is fixed in the very-short term and exogenously-defined by the monetary authority.

What I agree with:

- The main thesis of the book is completely valid and is something I have also argued for a little while: technological disruptions are now allowing us to go beyond banking and disintermediate it. P2P lending, non-banking payment systems, decentralised payment frameworks and currencies, algorithm-driven credit scoring… In many areas, banks have almost become redundant. I totally adhere to the authors’ thesis (although credit scoring does have real limitations).

- Technological developments have facilitated regulatory arbitrage, if not enabled it. Computing power now allow banks to optimise their capital requirements through the use of complex models which, it is important to point out, are validated by regulators.

What I disagree with:

- The authors seem to believe that banking regulation is usually a good thing and cannot seem to understand the various distortions, bubbles and inefficiencies those regulations create. According to them, if only technology hadn’t boomed over the past three decades, the banking system would be more stable. I strongly disagree.

- I dislike the top-down banking reform approach taken by their thesis. Free markets, driven by technology, should decide under what form the next iteration of banking should arise.

- I also see weaknesses in their proposal. First, I cannot agree with their view that money belongs to the public sphere, and that IOUs must benefit from a state guarantee to qualify as money. This has been disproved by history over and over again. Second, I see their proposal to have algorithmic trading manage the payment system as not only unworkable, but also dangerous. As already witnessed, algorithmic trading is imperfect and can amplify crashes rather than prevent them. How their payment system would react during a crisis, when everyone tries to exit most investments and pile into a few others, is anyone’s guess. Mine is that the payment system would suddenly be down, paralysing the entire economy. To be fair, their treatment of cash is unclear: could we maintain a custody account comprising only digital cash in their framework?

- Their 100%-reserve banking reform does not address fluctuations in the demand for money. Centralised monetary authorities do neither have access to the right information, nor within the right timeframe, to accurately provide extra media of exchange when needed by the public. Private entities, in direct contact with the public, can.

- Finally, though this is a minor point, I disagree with their monetary policy stance. It is inaccurate to present price stability as ideal to avoid economic distortions: productivity increases should lead to mild deflation in a growing economy (see Selgin’s Less than Zero or any market monetarist or Austrian blog and research paper). I also reject their physical cash ban, from a libertarian standpoint: people should be able to withdraw cash if ever they wish to*. This would seriously limit their negative interest rates policy proposal.

Overall, it is a thought-provoking and interesting book, which also quite accurately describes our current banking system in its first part (mostly aimed at people who don’t know that much about banking). Its two authors are also right to point out the defects of regulation in an IT-intensive era. But, in my opinion, they draw the wrong conclusions and the wrong reform proposals from their original assessment.

* Here again, their treatment of cash is unclear: can cash be withdrawn in a digital form and maintain in a digital wallet outside the financial system? I doesn’t look so from their book but I cannot say for sure.

Two kinds of financial innovation

Paul Volcker famously said that the only meaningful financial innovation of the past decades was the ATM. Not only do I believe that his comment was strongly misguided, but he also seemed to misunderstand the very essence of innovation in the financial services sector.

Financial innovations are essentially driven by:

- Technological shocks: new technologies (information-based mostly) allow banks to adapt existing financial products and risk management techniques to new technological paradigms. Without tech shocks, innovations in banking and finance are relatively slow to appear.

- Regulatory arbitrage: financiers develop financial products and techniques that bypass or use loopholes in existing regulations. Some of those regulatory-driven innovations also benefit from the appearance of new technological and theoretical paradigms. Those innovations are typically quick to appear.

I usually view regulatory-driven innovations as the ‘bad’ ones. Those are the ones that add extra layers of complexity and opacity to the financial system, hiding risks and misleading investors in the process.

It took a little while, but financial innovations are currently catching up with the IT revolution. Expect to change the way you make or receive payments or even invest in the near future.

See below some of the examples of financial innovation in recent news. Can you spot the one(s) that is(are) the most likely to lead to a crisis, and its underlying driver?

- Bank branches: I have several times written about this, but a new report by CACI and estimates by Deutsche Bank forecasted that between 50% and 75% of all UK branches will have disappeared over the next decade. Following the growing branch networks of the 19th and 20th centuries, which were seen as compulsory to develop a retail banking presence, this looks like a major step back. Except that this is actually now a good thing as the IT and mobile revolution is enabling such a restructuring of the banking sector. SNL lists 10,000 branches for the top 6 UK bank and 16,000 in Italy. Cutting half of that would sharply improve banks’ cost efficiency (it would, however, also be painful for banks’ employees). It is widely reported that banks’ branches use has plunged over the past three years due to the introduction of digital and mobile banking.

- In China, regulators have introduced new rules to try to make it harder for mainstream banks to deal with shadow banks in order to slow the growth of the Chinese shadow banking system, which has grown to USD4.9 trillion from almost nothing just a few years ago. The Economist reports that, by using a simple accounting trick, banks got around the new rules. Moreover, while Chinese regulators are attempting to constrain investments in so-called trust and asset management companies, investors and banks have now simply moved the new funds to new products in securities brokerage companies.

- In London, underground travellers can now pay for their journey by simply using their contactless bank card. No need of a specific underground card anymore. NFC-enabled smartphones will be able to do the same in the near future.

- Barclays is experimenting contactless wristband that would effectively replace your contactless card for payments (or, for Londoners, your underground Oyster Card).

- Apple announced Apple Pay, a contactless payment system managed by Apple through its new iPhones and Watch devices. Apple will store your bank card details and charge your account later on. This allows users to bypass banks’ contactless payments devices entirely. Vodafone also just released a similar IT wallet-contactless chip system (why not using the phone’s NFC system though? I don’t know. Perhaps they were also targeting customers that did not own NFC-enabled devices).

- Lending Club, the large US-based P2P lending firm, has announced its IPO. This is a signal that such firms are now becoming mainstream, as well as growing competitors to banks.

Of course, a lot more is going on in the financial innovation area at the moment, and I only highlighted the most recent news. Identifying the regulatory arbitrage-driven innovations will help us find out where the next crisis is most likely to appear.

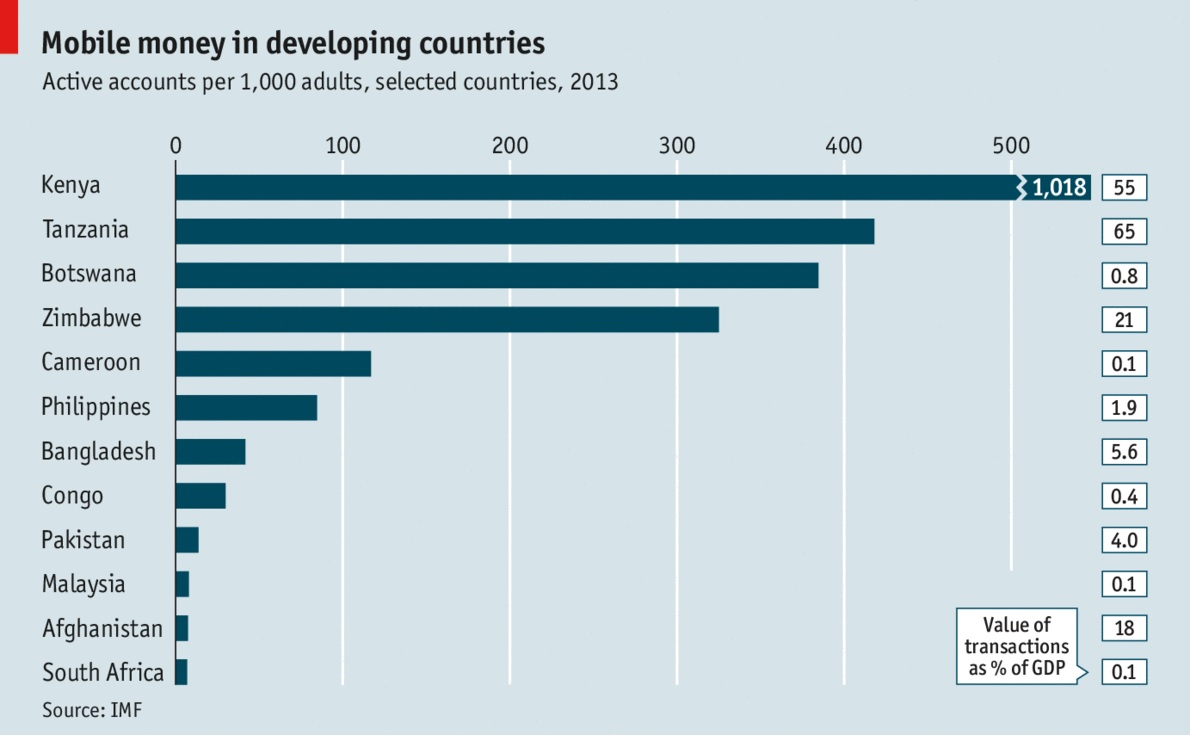

PS: the growth of cashless IT wallets has interesting repercussions on banks’ liquidity management and ability to extend credit (endogenous inside money creation), by reducing the drain of physical cash on the whole banking system’s reserves (outside money). If African economies are any guide to the future (see below, from The Economist), cash will progressively disappear from circulation without governments even outlawing it.

What most people seem to have missed about high-frequency trading

I finished reading Michael Lewis’ new book Flashboys last week. I wasn’t a specialist of high-frequency trading (HFT) at all, so I found the book interesting. Overall, it was an easy read. Perhaps too easy. I am always suspicious of easy-to-read books and articles that supposedly describe complex phenomena and mechanisms. Flashboys partly falls in that trap. Lewis has a real talent to entertain the reader. He unfortunately often slightly exaggerates and attacks the HFT industry without giving them the opportunity to respond. More annoyingly, the whole book reads like a giant advertising campaign for IEX, the new ‘fair’ exchange set up by Brad Katsuyama. In the end, I was left with a slightly strange aftertaste: the book is very partisan. I guess I shouldn’t have been surprised.

The book, as well as HFT, have been the topic of much discussion over the past few weeks*. I won’t come back to most of those comments, but I wish here to highlight what many people seem to have missed. Lewis, as well as many commenters, drew the wrong conclusions from the recent HFT experience. They misinterpret both the role of regulation and the market process itself.

What is most people’s first answer to the potential ‘damage’ caused by HFT? Regulation. I would encourage those people to read the book a second time. Perhaps a third time. This is Lewis:

How was it legal for a handful of insiders to operate at faster speeds than the rest of the market and, in effect, steal from investors? He soon had his answer: Regulation National Market System. Passed by the SEC in 2005 but not implemented until 2007, Reg NMS, as it became known, required brokers to find the best market prices for the investors they represented. The regulation had been inspired by charges of front-running made in 2004 against two dozen specialists on the floor of the old New York Stock Exchange – a charge the specialists settled by paying a $241 million fine.

Bingo.

Until 2007, brokers had discretion over how to handle investors’ trade orders. Despite the few cases of fraud/front-running, most investors didn’t seem to particularly hate that system. In a free market, investors are free to change broker if they are displeased with the service provided by their current one. At the very least, nothing seemed to really justify government’s intervention to institutionalise and regulate the exact way brokers were supposed to handle trade orders. In fact, when government took private discretion away, investors started feeling worse off. This is the very topic of the book (though Lewis didn’t seem to notice): government and regulation created HFT.

Brad Katsuyama sums it up pretty well (emphasis mine):

I hate them [HFT traders] a lot less than before we started. This is not their fault. I think most of them have just rationalized that the market is creating inefficiencies and they are just capitalizing on them. Really, it’s brilliant what they have done within the bound of regulation. They are much less a villain than I thought. The system has let down the investor.

Brad is definitely less naïve than Lewis, who still believed in the power of regulation throughout his book**:

Like a lot of regulations, Reg NMS was well-meaning and sensible. If everyone on Wall Street abided by the rule’s spirit, the rule would have established a new fairness in the U.S. stock market.

Meanwhile, David Glasner questioned the ‘social value’ of HFT on his blog:

Lots of other people have weighed in on both sides, some defending high-frequency trading against Lewis’s accusations, pointing out that high-frequency trading has added liquidity to the market and reduced bid-ask spreads, so that ordinary investors are made better off, not worse off, as Lewis charges, and others backing him up. Still others argue that any problems with high-frequency trading are caused by regulators, not by high-speed trading as such.

I think all of this misses the point. Lots of investors are indeed benefiting from the reduced bid-ask spreads resulting from low-cost high-frequency trading. Does that mean that high-frequency trading is a good thing? Um, not necessarily.

I believe that here it is Glasner who completely misses the point. Should we blame HFT traders from exploiting loopholes created by regulation? Economists are better placed than anyone to know that people respond to economic incentives. The resources ‘wasted’ by HFT on ‘socially useless informational advantages’ emanate from government intervention. It is highly likely that HFT would have never developed under its current form should Reg NMS had not been passed. What we instead witness is another case of regulatory-incentivised spontaneous financial innovation.

The second problem lies in the fact that most people seem to have become particularly impatient and dependent on short-term (and short-sighted) regulatory interventions. They spot a new ‘problem’ in the way markets work (here, HFT) and highlight it as a ‘market inefficiency’. This evidently cannot be tolerated any longer and regulators need to intervene right now to make markets ‘fairer’ (putting aside the fact that they were the ones who created this ‘inefficiency’ in the first place).

This demonstrates a fundamental misinterpretation of the market process. Markets’ and competitive landscapes’ adaptations aren’t instantaneous. This allows first movers to take advantage of consumers/investors demand and/or regulatory loopholes to generate supernormal profits… temporarily. In the medium term, the new economic incentives attract new entrants, which progressively erode the first movers’ advantage.

This occurs in all industries. Financial firms are no different (assuming no government protection or subsidies). And, despite Lewis’ outrage at HFT firms’ super profits, the fact is… that the mechanism I just described has already applied to them. It was reported that the whole industry experienced an 80% fall in profits between 2009 and 2012 (which Tyler Cowen had already ‘predicted’ here).

Besides, the story the book tells is a pure free-market story: a group of entrepreneurs wish to offer an alternative platforms to investors who also decide to follow them. There is no government intervention here. The market, distorted for a little while, is sorting itself out. Even the big banks see the tide turning and start switching sides (Goldman Sachs is depicted in a relatively positive light in the book). Lewis’ book itself is also part of that free-market story: the finger-pointing and informational role it plays is a necessary feature of the market process. To me, this demonstrates the ability of markets to right themselves in the medium-term. Patience is nevertheless required. It unfortunately seems to be an increasingly scarce commodity nowadays.

There was a very good description of HFT and its strategies published by Oliver Wyman at the end of last year (from which the chart below is taken). Surprisingly, they described HFT’s strategies and the effects of Reg NMS before the publication of Lewis’ book, without unleashing such a public outcry…

* See some there: FT’s John Gapper, The Economist, David Glasner, Noah Smith, Zero Hedge, Tyler Cowen (and here), ASI’s Tim Worstall, as well as this new paper by Joseph Stiglitz, who completely misinterprets the market process. See also this older, but very interesting, article by JP Koning on Mises.org on HFT seen through both Walrasian and Mengerian descriptions of the pricing process.

I also wish to congratulate Bob Murphy for this magical tweet:

** This is also despite Lewis reporting this hilarious dialogue between Brad Katsuyama and SEC regulators (emphasis his):

When [Brad, who had just read a document describing how to prevent HFT traders from front-running investors] was finished, an SEC staffer said, What you are doing is not fair to high-frequency traders. You’re not letting them get out of the way.

Excuse me? said Brad

And to continue saying that 200 SEC employees had left their government jobs to go work for HFT and related firms, including some who had played an important role in defining HFT regulation. It reminded me of this recent study that showed that SEC employees benefited from abnormal positive returns on their securities portfolios…

Mobile banking keeps growing, payday lenders perhaps not so much anymore

The Fed published last week a new mobile banking survey in the US. Here are the highlights: 33% of all mobile phone owners have used mobile banking over the past twelve months, up from 28% a year earlier. When only considering smartphones, those figures increased to 51% and 48% respectively, with 12% of mobile users who plan to move on to mobile banking soon. 39% of the ‘underbanked’ population used mobile banking over the period. Checking balances, monitoring transactions and transferring money are the most common activities.

Still more than half of mobile users who do not currently use mobile banking are reluctant to use it in the future though. But usage is correlated with age. 18 to 29yo users represent 39% of all mobile banking users but only 21% of mobile phones users, whereas 45 to 60yo represent 27% of mobile banking users but 53% of mobile users. I am indeed not surprised by those results, and, as I have described in a previous post, as current young people age, the bank branch will slowly disappear and mobile banking become the norm. (Bloomberg published an article on the end of the bank branch yesterday)

That the underbanked naturally benefit from mobile banking isn’t surprising, and isn’t new at all. The widespread use of the M-Pesa system in Kenya rested on the fact that a very large share of the population had no or limited access to banking services. However, some African countries with slightly more developed banking systems are resisting the introduction of mobile money in order not to interfere with the business as usual of the local incumbent banks. Another case of politicians and regulators acting for the greater good of their country. Anyway, mobile money/banking is now instead making its way to… Romania, as almost everyone there owns a mobile phone but more than a third of the population does not have access to conventional banking.

Meanwhile, in the UK, the regulators are doing what they can to clamp down on payday lenders. As I have described in a previous post, the result of this move is only likely to prevent underbanked people from accessing any sort of credit, as other regulations seriously limit mainstream banks’ ability to lend to those higher-risk customers.

Here again, the Fed mobile banking survey is quite enlightening. They asked underbanked people their reasons for using payday lenders. Here are their answers:

Right… So what are the consequences when you prevent people from temporarily borrowing small amount of cash that their bank aren’t willing to provide and who need it to pay for utility bills or buying some food or for any other emergency expenses? It looks like regulators believe that those families would indeed be better off not being able to pay their water bills.

Of course, over-borrowing is an issue (as are abuse and fraud), but regulators are merely clamping down on symptoms here. Society is confronted with a dilemma: either those households are unable to pay their bills or buy enough food, or they might face over-indebtedness… None of those two options are attractive. But in such a situation, it is customers’ responsibility to choose. If they can avoid payday lenders, so they should. If they really can’t, this option should remain on the table. Sam Bowman from the Adam Smith Institute made very good comments on BBC radio Wales earlier today (see here from 02:05:00) on this topic.

I know I am repeating myself, but you cannot regulate problems away.

News digest: Scotland, CoCos and electronic trading

Sam Bowman had a very good piece on the Adam Smith Institute blog about Scotland setting up a pound Sterling-based free banking system unilaterally (yeah I know I keep mentioning this blog now, but activity there seems to have been picking up recently). It draws on George Selgin’s post and is a very good read. One particular point was more than very interesting in the context of my own blog (emphasis added):

George Selgin has pointed to research by the Federal Reserve Bank of Atlanta about the Latin American countries that unilaterally use the dollar. Because these countries – Panama, Ecuador and El Salvador – lack a Lender of Last Resort, their banking systems have had to be far more prudent and cautious than most of their neighbours.

Panama, which has used the US Dollar for one hundred years, is the most useful example because it is a relatively rich and stable country. A recent IMF report said that:

“By not having a central bank, Panama lacks both a traditional lender of last resort and a mechanism to mitigate systemic liquidity shortages. The authorities emphasized that these features had contributed to the strength and resilience of the system, which relies on banks holding high levels of liquidity beyond the prudential requirement of 30 percent of short-term deposits.”

Panama also lacks any bank reserve requirement rules or deposit insurance. Despite or, more likely, because of these factors, the World Economic Forum’s Global Competitiveness Report ranks Panama seventh in the world for the soundness of its banks.

I don’t think I have anything to add…

SNL reported yesterday that Germany’s laws seem to make the issuance of contingent convertible bonds (CoCos) almost pointless. This is a vivid reminder of my previous post, which highlighted some of the ‘good’ principles of financial regulation and which advocated stable, simple and clear rules, a position I have had since I’ve opened this blog. All authorities and regulators try to push banks (including German banks) to boost their capital level, which are deemed too low by international standards. CoCos, which are bonds that convert into equity if the bank’s regulatory capital ratio gets below a certain threshold, are a useful tool for banks (as it allows them to prevent shareholder dilution by issuing equity) and investors (whose demand is strong as those bonds pay higher coupon rates). Yet lawmakers, who love to bash banks for their low level of capitalisation, seem to be in no hurry to provide a clear framework that would allow to partially solve the very problems they point at in the first place… This is a very obvious example of regime uncertainty. As one lawyer declared:

One thing is clear: Nothing is clear

Bloomberg reports that FX traders are facing ‘extinction’ due to the switch to electronic trading. In fact, this has been ongoing for now several years, with asset classes moving one after another towards electronic platforms. Electronic trading now represents 66% of all FX transactions (vs. 20% in 2001). Traditional traders are going to become increasingly scarce and replaced by IT specialists that set and programme those machines. Overall, this should also mean less staff and a lower cost base for banks that are still plagued by too high cost/income ratios. Part of this shift is due to regulation, which makes it even more expensive to trade some of those products. This only reinforces my belief that regulation is historically one of the primary drivers of financial innovation, from money market funds to P2P lending…

Banks’ branches/IT problems, and bank regulation vs. freedom

Barclays this week unsurprisingly announced the closure of a quarter of its 1600 branches. A ‘person familiar with the plans of Barclays’ said:

This is a fundamental 100-year transformation of the banking industry, that’s what I think we are seeing.

He/she is right. Though this has been obvious to banking innovators for a while already. SNL expands on that here and mentions high cost/income in retail banking. An analyst:

No bank in Europe can avoid the online banking issue. It is the future of the bank business.

As I have already said, it questions the plans of some of British politicians to cap the market share of large banks. How could their plan work when banks are already slashing branches by the thousands and when new and growing banks are increasingly established online or within other types of stores (see Tesco Bank, which has no actual branch but ‘in-store branches’ within its Tesco supermarkets). Politicians are able to foresee trends and innovation you said? How can one trust people who can only offer yesterday’s solutions to tomorrow’s problems? Same question about general banking regulation…

Anyway, banks also have some serious work to do. Many of them have antiquated IT systems, which makes us think that a transition to an IT-heavy (or perhaps IT-only…) banking business model won’t be smooth… UK banks have experienced a number of IT problems over the past few months (payment systems down mainly) as a result of their underinvestment in basic IT and the accumulation of various systems on top of one another following acquisitions, without never having really tried to integrate them all.

I personally check my accounts a lot more often now that I have access to smartphone apps, and I am certainly not the only one to do so. With the growth of mobile and contactless payments and the reduction in the number of hard cash transactions, the pressure on banks’ IT systems will become enormous. Increased mobile transaction volumes will also impact mobile telecom networks, though they often more rapidly update their systems than banks. What’s going to be interesting is that banks will increasingly rely on the infrastructure of private mobile and internet telcos. This emergent symbiosis may well accelerate the development of mobile networks, in terms of speed, security and coverage.

And banks better be in a hurry. As they now have payment systems competitors such as Paypal or Bitcoin, which ironically would also benefit from the same technological developments. Telcos could potentially also enter the payment space, as Kenya’s Safaricom did with M-Pesa.

Unrelated, a good piece by Sean Ryan on SNL (gated link) called “Bank regulation versus Americans’ freedom”, and reminiscent of one of my previous posts. This is Sean:

The power to regulate banks is impeding the ability of law-abiding citizens to exercise their rights. Washington is full of people with very strong ideas about how the rest of us should live, and I fear that increasingly intrusive bank regulation has given them an opening to do something about it.

[…]

Given the rapid proliferation of nominally legal activities being exiled from the economic mainstream by bank regulators, it seems only a modest exaggeration, and less modest by the week, to suggest that we are incubating a fourth branch of government. And this one isn’t so hamstrung by those pesky checks and balances.

I couldn’t have said it better myself.

News digest (Libor 1.7bn fine, banks’ poor IT systems, banking, telco, IT, retailing convergence…)

Again this week, so many things happening that I can’t spend much time commenting on each and I have to make choices!

George Osborne, UK’s Chancellor of the Exchequer, is about to announce a tax-free treatment for P2P lending, which could be included in individual Isa accounts. This is a good thing. Nothing much more to say…

The Bank of England is thinking of asking UK-based banks to provide regulatory capital ratios calculated using standard risk-weights as defined by Basel’s Standardised method. These ratios would not replace those banks’ main capital ratios as currently calculated (under the IRB method) but would ‘complement’ them. It’s a good idea and we may well end up having a few surprises…

The EU has fined some of the large global banks as part of the Libor rate-rigging. Banks will have to pay EUR1.7bn. This isn’t that significant given what JPMorgan has paid so far in fines in the US… I stopped counting and I may well be wrong but I think they paid around USD$15bn so far this year. Surely this should make me doubt about the ability of laissez-faire to regulate banks? Not really. First, we are not in a laissez-faire environment. Second, laissez-faire does not mean laissez-faire fraudulent activities. It means laissez-faire people to negotiate their own contracts and agreements. When those contracts are not respected, when there is fraud, punishment should ensue. Laissez-faire is completely in favour of the rule of law. Moreover in a real free-market environment, it is likely that most fraudulent banks would already be out of business…

Something I know from experience: many banks have really poor IT systems and poorly-designed databases. This week, Royal Bank of Scotland’s customers could not access their accounts anymore for a whole day (and pretty busy shopping day on top of that). Its CEO acknowledged that the bank will have to invest… GBP1bn in its IT systems. That’s a massive bill. It shows how outdated its IT systems must have been. It is scary to see that some banks (nop, no name), whether small, medium-sized or massively massive have such poorly-designed systems that they cannot adequately track simple data such as their exposures and the level of provisioning against them by industrial sector or geographical area for example. This is the result of years, if not decades, of underinvestment in IT. This is also why start-up banks are usually much more efficient: they have top-notch IT. For large banks, no surprise, trading systems have been upgraded at a much faster pace than commercial and retail banking ones. Banks are currently plagued by their high cost base. But more efficient IT systems would have helped maintain their costs lower while improving internal productivity.

Moreover, banks are also under threat from new financial actors, and possibly future data-heavy entrants such as Google and Amazon. Those firms have great IT systems: it is their core business. What if they entered the banking business? It’s what Spain’s BBVA’s CEO asked in the FT this week. Indeed, banks are now closing branches one by one as customers move online or mobile. It also means that new entrants possibly wouldn’t need any branch network altogether and could offer more efficient services to customers, using their huge data centres and cloud computing capabilities. A quick visit to the annual Barcamp Bank ‘unconference’ shows how many people are currently working on new customer-friendly and efficient banking API and other systems. We’ve already seen the ‘convergence’ of IT, telecoms and media. Are we about to witness a banking, IT, telecom, retailing, online search and payment convergence?

Are synthetic CDOs making a comeback? Well, issuance volume is still pretty low… Unless low interest rates start over-boosting this market too?

Finally, Columbia University’s Charles Calomiris has his own take on Admati and Hellwig’s recommendations and rejects some of their claims (such as the fact that higher equity levels would not impair lending, a claim that I have already made here, although my reasoning was different). He also favours rising banks’ equity requirements though.

Recent Comments