McKinsey on banking and debt

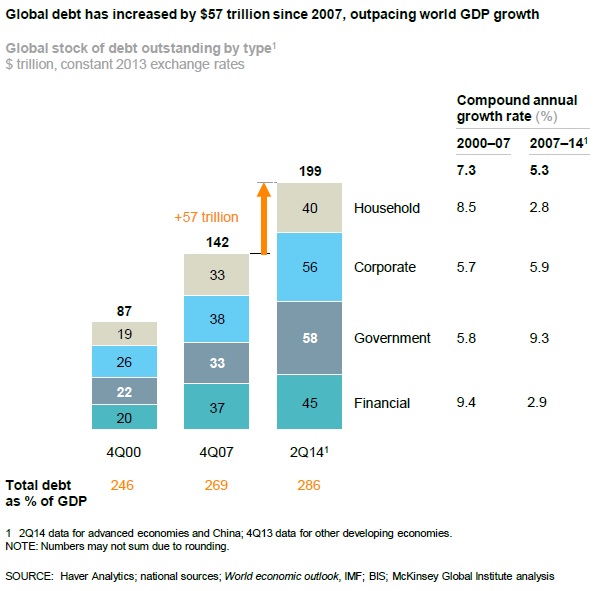

A recent report by the consultancy McKinsey highlights how much the world has not deleveraged since the onset of the financial crisis. Many newspapers have jumped on the occasion to question whether or not the policies adopted since the crisis were the right ones (FT, Telegraph, The Economist…). This is how the total stock of debt has evolved since 2000:

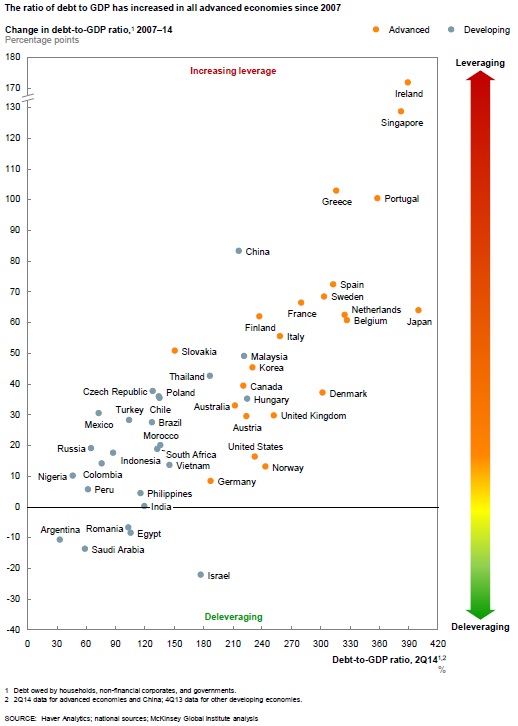

As the following chart shows, the vast majority of countries saw their overall level of debt increase:

As the following chart shows, the vast majority of countries saw their overall level of debt increase:

McKinsey affirms that “household debt continues to grow rapidly, and deleveraging is rare”, and that the same broadly applies to corporate debt. China is an extreme case: total debt level, as a share of GDP, grew from 121% of GDP in 2000, to 158% in 2007 to…282% at end-H114. And growing.

McKinsey affirms that “household debt continues to grow rapidly, and deleveraging is rare”, and that the same broadly applies to corporate debt. China is an extreme case: total debt level, as a share of GDP, grew from 121% of GDP in 2000, to 158% in 2007 to…282% at end-H114. And growing.

Unsurprisingly, household debt is driven by mortgage lending (including in China). It isn’t a surprise to see house prices increasing in so many countries. How this is a reflection that we currently are in a sustainable recovery, I can’t tell you. How this is a signal that monetary policy has been ‘tight’, I can’t tell you either. If monetary policy has indeed been ‘tight’, then it shows the power of Basel regulation in transforming a ‘tight’ monetary policy into an ‘easy’ one for households through mortgage lending. How this total stock of debt will react when interest rates start rising is anyone’s guess…

McKinsey’s claim that “banks have become healthier” is questionable at best, as they use regulatory Tier 1 ratios as a benchmark. Indeed a lot of banks have boosted their Tier 1 ratio by reducing RWA density (i.e. the average risk-weight applied to their assets) rather than actually raising or internally generating extra capital.

As expected given how capital intensive corporate lending has become thanks to our banking regulatory framework, and in line with recent research, banks are now mostly funding households at the expense of businesses:

As expected given how capital intensive corporate lending has become thanks to our banking regulatory framework, and in line with recent research, banks are now mostly funding households at the expense of businesses:

McKinsey highlights that P2P lending, while still small in terms of total volume, doubles in size every year, and is mostly present in China and the US.

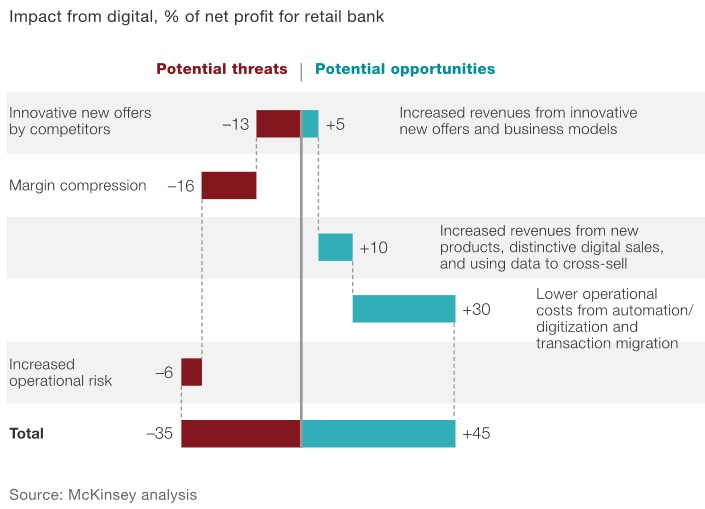

And in fact, in another article, McKinsey explains that the digital revolution is going to severely hit retail banking. I have several times described that banks’ IT systems were on average out-of-date, that this weighed on their cost efficiency and hence profitability, and that it even possibly impaired the monetary policy transmission channel. I also said that banks needed to react urgently if they were not to be taken over by more recent, more efficient, IT-enabled competitors. A point also made in The End of Banking, according to which technology allows us to get rid of banks altogether.

McKinsey is now backing up those claims with interesting estimates. According to the consultancy, and unsurprisingly, operating costs would be the main beneficiary of a more modern IT framework:

McKinsey goes as far as declaring that:

McKinsey goes as far as declaring that:

The urgency of acting is acute. Banks have three to five years at most to become digitally proficient. If they fail to take action, they risk entering a spiral of decline similar to laggards in other industries.

Unfortunately, current extra regulatory costs and litigation charges are making it very hard for banks to allocate any budget to replace antiquated IT systems.

If banks already had those systems in place as of today, I would expect to see lending rates declining further – in line with monetary policy – across all lending products as margin compression becomes less of an issue. In a world where banks have zero operating cost, its net interest income doesn’t need to be high to generate a net profit.

In the end, regulators are shooting themselves in the foot: not only new regulations and continuous litigations may well have the effect of facilitating new non-banking firms’ takeover of the financial system, but also monetary policy cannot have the effect that regulators/central bankers themselves desire.

Recent Comments