The mystery of collateral

Collateral has been the new fashionable area of finance and capital markets research over the past few years. Collateral and its associated transactions have been blamed for all the ills of the crisis, from runs on banks’ short-term wholesale funding to a scarcity of safe assets preventing an appropriate recovery. Some financial journalists have jumped on the bandwagon: everything is now seen through a ‘collateral lens’. The words ‘assets’, and, to a lesser extent ‘liquidity’ and ‘money’ themselves, have lost their meaning: all are now being replaced by ‘collateral’, or used interchangeably, by people who don’t seem to understand the differences.

A few researchers are the root cause. The work of Singh keeps referring to any sort of asset transfer between two parties as ‘collateral transfer’. This is wrong. Assets are assets. Securities are securities, a subset of assets. Collateral can be any type of assets, if designated and pledged as such to secure a lending or derivative transaction. Real estate, commodities and Treasuries can all be used as collateral. Money too. Unlike what Singh and his followers claim, a securities lender lends a security not a collateral. Whether or not this security is used as collateral in further transactions is an independent event.

This unfortunate vocabulary problem has led to perverse ramifications: all liquid assets, or, as they often say, collateral, are now seen as new forms of money (see chart below, from this paper). Specifically, collateral becomes “the money of the shadow banking system”. I believe this is incorrect. Collateral is used by shadow banks to get hold of money proper. Building on this line of reasoning, people like Pozsar assert that repo transactions are money… This makes even less sense. Repos simply are collateralised lending transactions. Nobody exchanges repos. The assets swapped through a repo (money and securities) could however be exchanged further. Depressingly, this view is taken increasingly seriously. As this recent post by Frances Coppola demonstrates, all assets seem now to be considered as money. This view is wrong in many ways, but I am ready to reconsider my position if ever Treasuries or RMBSs start being accepted as media of exchange at Walmart, or between Aston Martin and its suppliers. Others have completely misunderstood the differences between loan collateralisation and loan funding, which is at the heart of the issue: you don’t fund a loan, whether in the light or the dark side of the banking system, with collateral! The monetary base/high-powered money/cash/currency, is the only medium of settlement, the only asset that qualifies as a generally-accepted medium of exchange, store of value and unit of account (the traditional definition of money).

There is one exception though. Some particular transactions involve, not a non-money asset for money swap, but non-money asset for another non-money asset swap. This is almost a barter-like transaction, which does occur from time to time in securities lending activities (the lender lends a security for a given maturity, and the borrower pledges another security as collateral). Nonetheless, the accounting (including haircuts and interest calculations) in such circumstances is still being made through the use of market prices defined in terms of the monetary base.

Still, collateral seems to have some mysterious properties and Singh’s work offers some interesting insights into this peculiar world. The evolution of the collateral market might well have very deep effects on the economy. The facilitation of collateral use and rehypothecation, as well as the requirements to use them, either through specific regulatory and contractual frameworks, through the spread of new technology, new accounting rules or simply through the increased abundance of ‘safe assets’ (i.e. increased sovereign debt issuance), might well play a role in business cycles, via the interest rate channel. Indeed, by facilitating or requiring the use of increasingly abundant collateral, interest rates tend to fall. The concept of collateral velocity is in itself valuable: when velocity increases, interest rates tend to fall further as more transactions are executed on a secured basis. Still, are those transactions, and the resulting fall in interest rates, legitimate from an economic point of view? What are the possible effects on the generation of malinvestments?

An example: let’s imagine that a legal framework clarification or modification, and/or regulatory change, increases the use and velocity of safe collateral (government debt). New technological improvements also facilitate the accounting, transfer, and controlling processes of collateral. This increases the demand for government debt, which depresses its yield. Motivated by lower yield, the government indeed issues more debt that flow through financial markets. As the newly-enabled average velocity of collateral increases substantially, more leveraged secured transactions take place and at lower interest rates. While banks still have exogenous limits to credit expansion (as the monetary base is controlled by the central bank), the price of credit (i.e. endogenous money creation) has therefore decreased as a result of a mere regulatory/legal/technological change.

I have been wondering for a while whether or not such a change in the regulatory paradigm of collateral use could actually trigger an Austrian-type business cycle. I do not yet have an answer. Implications seem to be both economic and philosophical. What are the limits to property rights transfer? How would a fully laisse-faire market deal with collateral and react to such technological changes? Perhaps collateral has no real influence on business fluctuations after all. There is nevertheless merit in investigating further. I am likely to explore the collateral topic over the next few months.

PS: I will be travelling in North America over the next 10 days, so might not update this blog much.

* There are many many flaws in Frances’ piece. See this one:

But suppose that instead of a sterling bank account, a smartcard or a smartphone app enabled me to pay a bill in Euros directly from my holdings of UK gilts? This is not as unlikely as it sounds. It would actually be two transactions – a sale of gilts for sterling and a GBPEUR exchange. This pair of transactions in today’s liquid markets could be done instantaneously. I would in effect have paid for my meal with UK government debt.

She fails to see that she would have paid for her mean with Sterling, not with government debt! Government debt must be converted into currency as it is not a medium of exchange/settlement.

News digest: P2P lending and HFT, CoCo bonds, Co-op Bank…

Ron Suber, President at Prosper, the US-based P2P lending company, sent me a very interesting NY Times article a few days ago. The article is titled “Loans That Avoid Banks? Maybe Not.” This is not really accurate: the article indeed mentions institutional investors such as mutual and hedge funds increasingly investing in bundles of P2P loans through P2P platforms, but never refers to banks. Unlike what the article says, I don’t think platforms were especially set up to bypass institutional investors… They were set up to bypass banks and their costly infrastructure and maturity transformation.

Some now fear that the industry won’t be ‘P2P’ for very long as institutional investors increasingly take over a share of the market. I think those beliefs are misplaced. Last year, I predicted that this would create opportunities for niche players to enter the market, focusing on real ‘P2P’.

A curious evolution is the application of high-frequency trading strategies to P2P. I haven’t got a lot of information about their exact mechanisms, but I doubt they would resemble the ones applied in the stock market given that P2P is a naturally illiquid and borrower-driven market.

The main challenge of the industry at the moment seems to be the lack of potential customer awareness. Despite offering better deals (i.e. cheaper borrowing rates) than banks, demand for loans remains subdued and the industry tiny next to the banking sector.

In this FT article, Alberto Gallo, head of macro-credit research at RBS, argues that regulators should intervene on banks’ contingent convertible bonds’ risks. I think this is strongly misguided. Investors’ learning process is crucial and relying on regulators to point out the potential risks is very dangerous in the long-term. Not only such paternalism disincentives investors to make their own assessment, but also regulators have a very bad track record at spotting risks, bubbles and failures (see Co-op bank below).

This piece here represents everything that’s wrong with today’s banking theory:

We know that a combination of transparency, high capital and liquidity requirements, deposit insurance and a central bank lender of last resort can make a financial system more resilient. We doubt that narrow banking would.

Not really… They also argue that 100% reserve banking would not prevent runs on banks:

The mutual funds of the narrow banking world would be subject to the same runs. Indeed, recent research highlights that – in the presence of small investors – relatively illiquid mutual funds are more likely to face exit in the event of past bad performance. […] Since the mutual funds would be holding illiquid loans – remember, they are taking over functions of banks – collective attempts at liquidation to meet withdrawal requests would lead to ruinous fire sales.

They misunderstand the purpose of such a banking system. Those ‘mutual funds’ would not be similar to the ones we currently have, which invests in relatively liquid securities on the stock market, and can as a result exit their positions relatively quickly and easily. Those 100% reserve funds would invest in illiquid loans and investors in those funds would have their money contractually locked in for a certain time. With no legal power to withdraw, no risk of bank run.

The FT reported a few days ago the results of the investigation on the Co-operative bank catastrophe. Despite regulators not noticing any of the problems of the bank, from corporate governance to bad loans and capital shortfall, as well as approving unsuitable CEOs and mergers, the report recommends to… “heed regulatory warnings.” I see…

The impossible sometimes happens: I actually agree with Paul Krugman’s last week piece on endogenous money. No guys, the BoE paper didn’t reveal any mystery of banking or anything…

Finally, Chris Giles wrote a very good article in the FT today, very clearly highlighting the contradictions in the Bank of England policies and speeches, and their tendency to be too dovish whatever the circumstances:

Mark Carney, the governor, certainly displays dovish leanings. Before he took the top job, he said monetary policy could be tightened once growth reached “escape velocity”. But now that growth has shot above 3 per cent, he advocates waiting until the economy has “sustained momentum” – without acknowledging that his position has changed. His attitude to prices also betrays a knee-jerk dovishness. When inflation was above target, he stressed the need to look at forecasts showing a more benign period ahead. Now that inflation is lower it is apparently the short-term data that matters – and it justifies stimulus.

So much for forward guidance… Time to move to a rule-based monetary policy?

What most people seem to have missed about high-frequency trading

I finished reading Michael Lewis’ new book Flashboys last week. I wasn’t a specialist of high-frequency trading (HFT) at all, so I found the book interesting. Overall, it was an easy read. Perhaps too easy. I am always suspicious of easy-to-read books and articles that supposedly describe complex phenomena and mechanisms. Flashboys partly falls in that trap. Lewis has a real talent to entertain the reader. He unfortunately often slightly exaggerates and attacks the HFT industry without giving them the opportunity to respond. More annoyingly, the whole book reads like a giant advertising campaign for IEX, the new ‘fair’ exchange set up by Brad Katsuyama. In the end, I was left with a slightly strange aftertaste: the book is very partisan. I guess I shouldn’t have been surprised.

The book, as well as HFT, have been the topic of much discussion over the past few weeks*. I won’t come back to most of those comments, but I wish here to highlight what many people seem to have missed. Lewis, as well as many commenters, drew the wrong conclusions from the recent HFT experience. They misinterpret both the role of regulation and the market process itself.

What is most people’s first answer to the potential ‘damage’ caused by HFT? Regulation. I would encourage those people to read the book a second time. Perhaps a third time. This is Lewis:

How was it legal for a handful of insiders to operate at faster speeds than the rest of the market and, in effect, steal from investors? He soon had his answer: Regulation National Market System. Passed by the SEC in 2005 but not implemented until 2007, Reg NMS, as it became known, required brokers to find the best market prices for the investors they represented. The regulation had been inspired by charges of front-running made in 2004 against two dozen specialists on the floor of the old New York Stock Exchange – a charge the specialists settled by paying a $241 million fine.

Bingo.

Until 2007, brokers had discretion over how to handle investors’ trade orders. Despite the few cases of fraud/front-running, most investors didn’t seem to particularly hate that system. In a free market, investors are free to change broker if they are displeased with the service provided by their current one. At the very least, nothing seemed to really justify government’s intervention to institutionalise and regulate the exact way brokers were supposed to handle trade orders. In fact, when government took private discretion away, investors started feeling worse off. This is the very topic of the book (though Lewis didn’t seem to notice): government and regulation created HFT.

Brad Katsuyama sums it up pretty well (emphasis mine):

I hate them [HFT traders] a lot less than before we started. This is not their fault. I think most of them have just rationalized that the market is creating inefficiencies and they are just capitalizing on them. Really, it’s brilliant what they have done within the bound of regulation. They are much less a villain than I thought. The system has let down the investor.

Brad is definitely less naïve than Lewis, who still believed in the power of regulation throughout his book**:

Like a lot of regulations, Reg NMS was well-meaning and sensible. If everyone on Wall Street abided by the rule’s spirit, the rule would have established a new fairness in the U.S. stock market.

Meanwhile, David Glasner questioned the ‘social value’ of HFT on his blog:

Lots of other people have weighed in on both sides, some defending high-frequency trading against Lewis’s accusations, pointing out that high-frequency trading has added liquidity to the market and reduced bid-ask spreads, so that ordinary investors are made better off, not worse off, as Lewis charges, and others backing him up. Still others argue that any problems with high-frequency trading are caused by regulators, not by high-speed trading as such.

I think all of this misses the point. Lots of investors are indeed benefiting from the reduced bid-ask spreads resulting from low-cost high-frequency trading. Does that mean that high-frequency trading is a good thing? Um, not necessarily.

I believe that here it is Glasner who completely misses the point. Should we blame HFT traders from exploiting loopholes created by regulation? Economists are better placed than anyone to know that people respond to economic incentives. The resources ‘wasted’ by HFT on ‘socially useless informational advantages’ emanate from government intervention. It is highly likely that HFT would have never developed under its current form should Reg NMS had not been passed. What we instead witness is another case of regulatory-incentivised spontaneous financial innovation.

The second problem lies in the fact that most people seem to have become particularly impatient and dependent on short-term (and short-sighted) regulatory interventions. They spot a new ‘problem’ in the way markets work (here, HFT) and highlight it as a ‘market inefficiency’. This evidently cannot be tolerated any longer and regulators need to intervene right now to make markets ‘fairer’ (putting aside the fact that they were the ones who created this ‘inefficiency’ in the first place).

This demonstrates a fundamental misinterpretation of the market process. Markets’ and competitive landscapes’ adaptations aren’t instantaneous. This allows first movers to take advantage of consumers/investors demand and/or regulatory loopholes to generate supernormal profits… temporarily. In the medium term, the new economic incentives attract new entrants, which progressively erode the first movers’ advantage.

This occurs in all industries. Financial firms are no different (assuming no government protection or subsidies). And, despite Lewis’ outrage at HFT firms’ super profits, the fact is… that the mechanism I just described has already applied to them. It was reported that the whole industry experienced an 80% fall in profits between 2009 and 2012 (which Tyler Cowen had already ‘predicted’ here).

Besides, the story the book tells is a pure free-market story: a group of entrepreneurs wish to offer an alternative platforms to investors who also decide to follow them. There is no government intervention here. The market, distorted for a little while, is sorting itself out. Even the big banks see the tide turning and start switching sides (Goldman Sachs is depicted in a relatively positive light in the book). Lewis’ book itself is also part of that free-market story: the finger-pointing and informational role it plays is a necessary feature of the market process. To me, this demonstrates the ability of markets to right themselves in the medium-term. Patience is nevertheless required. It unfortunately seems to be an increasingly scarce commodity nowadays.

There was a very good description of HFT and its strategies published by Oliver Wyman at the end of last year (from which the chart below is taken). Surprisingly, they described HFT’s strategies and the effects of Reg NMS before the publication of Lewis’ book, without unleashing such a public outcry…

* See some there: FT’s John Gapper, The Economist, David Glasner, Noah Smith, Zero Hedge, Tyler Cowen (and here), ASI’s Tim Worstall, as well as this new paper by Joseph Stiglitz, who completely misinterprets the market process. See also this older, but very interesting, article by JP Koning on Mises.org on HFT seen through both Walrasian and Mengerian descriptions of the pricing process.

I also wish to congratulate Bob Murphy for this magical tweet:

** This is also despite Lewis reporting this hilarious dialogue between Brad Katsuyama and SEC regulators (emphasis his):

When [Brad, who had just read a document describing how to prevent HFT traders from front-running investors] was finished, an SEC staffer said, What you are doing is not fair to high-frequency traders. You’re not letting them get out of the way.

Excuse me? said Brad

And to continue saying that 200 SEC employees had left their government jobs to go work for HFT and related firms, including some who had played an important role in defining HFT regulation. It reminded me of this recent study that showed that SEC employees benefited from abnormal positive returns on their securities portfolios…

News digest: central bank independence, TBTF and ironic regulators

I’m quite busy at the moment so not many updates here. However I am almost done with Michael Lewis’ new book on high-frequency trading Flashboys. I’ll surely write something about it soon.

The FT had this week an interesting and quite comprehensive article on fintech and new financial start-ups (not sure they all qualify as ‘fintech’ though…). It’s a good introduction for those who don’t know what’s going on in the sector.

On the other hand, about a week ago, Martin Wolf had one of the worst articles on the recent BoE paper on money creation I have had the occasion to read. It looks like Wolf is oblivious to the intense debate on the blogosphere (and elsewhere) that was triggered by the publication of this controversial, and flawed, paper. But… I guess I have given up on Martin Wolf…

US banks have published (through the Clearinghouse association) a new paper arguing that large banks had not been benefiting from the ‘too big to fail’ funding advantage since 2013. I believe this study is quite right but I also think it misses the point made by previous research papers (see one of them here): the main question wasn’t “are banks subsidised for being TBTF?” but “were banks subsidised for being TBTF?”, which could lead to a crisis. There are many reasons why spreads between TBTF and non-TBTF banks would narrow in the short-term. A simple one could be: many large banks are actually currently in a worse financial shape than smaller banks. Another one: states have kept repeating their intentions not to bail out banks and introduced bail-in mechanisms. The paper doesn’t seem to have an answer to this and takes a way too short time horizon to really assess the effectiveness of anti-TBTF measures. It will take another few years to have a definitive answer.

As I said in a recent post, regulators are taking over all the corners of our modern financial system. Another recent target: bank overdraft fees. They basically complain that overdrafts can be more expensive than…payday loans. But they attacked payday loans as predatory. They didn’t seem to get the underlying mechanism at play here… So what’s their logic? Protecting the consumer. But by limiting payday loans, some people will be cut off credit altogether, while some others will have to use…more expensive overdrafts. If overdrafts costs are then pushed down, then it is highly likely that the cost of other services will be pushed up. In the end, regulators just move the problem rather than solve it.

The ironic news of the week is: US state regulators are concerned about the methods used by US federal regulators to crack down on payday lenders (gated link). Just wow.

Christine Lagarde, head of the IMF, declared this week that central bank independence from government control should probably end. While central banks are already arguably not fully independent, I find really scary the types of reaction brought about by the financial crisis. It is like humanity had all of a sudden forgotten the lessons learnt from several centuries of financial history.

Finally, the FT reports a new research paper on the use of pseudo-mathematical models in investment strategies (paper available here). Researchers argue that most of those models are deeply flawed as they are twisted to fit past data. I haven’t read the paper yet but I will soon as I suspect their conclusions also involve other parts of the banking industry.

Mobile banking keeps growing, payday lenders perhaps not so much anymore

The Fed published last week a new mobile banking survey in the US. Here are the highlights: 33% of all mobile phone owners have used mobile banking over the past twelve months, up from 28% a year earlier. When only considering smartphones, those figures increased to 51% and 48% respectively, with 12% of mobile users who plan to move on to mobile banking soon. 39% of the ‘underbanked’ population used mobile banking over the period. Checking balances, monitoring transactions and transferring money are the most common activities.

Still more than half of mobile users who do not currently use mobile banking are reluctant to use it in the future though. But usage is correlated with age. 18 to 29yo users represent 39% of all mobile banking users but only 21% of mobile phones users, whereas 45 to 60yo represent 27% of mobile banking users but 53% of mobile users. I am indeed not surprised by those results, and, as I have described in a previous post, as current young people age, the bank branch will slowly disappear and mobile banking become the norm. (Bloomberg published an article on the end of the bank branch yesterday)

That the underbanked naturally benefit from mobile banking isn’t surprising, and isn’t new at all. The widespread use of the M-Pesa system in Kenya rested on the fact that a very large share of the population had no or limited access to banking services. However, some African countries with slightly more developed banking systems are resisting the introduction of mobile money in order not to interfere with the business as usual of the local incumbent banks. Another case of politicians and regulators acting for the greater good of their country. Anyway, mobile money/banking is now instead making its way to… Romania, as almost everyone there owns a mobile phone but more than a third of the population does not have access to conventional banking.

Meanwhile, in the UK, the regulators are doing what they can to clamp down on payday lenders. As I have described in a previous post, the result of this move is only likely to prevent underbanked people from accessing any sort of credit, as other regulations seriously limit mainstream banks’ ability to lend to those higher-risk customers.

Here again, the Fed mobile banking survey is quite enlightening. They asked underbanked people their reasons for using payday lenders. Here are their answers:

Right… So what are the consequences when you prevent people from temporarily borrowing small amount of cash that their bank aren’t willing to provide and who need it to pay for utility bills or buying some food or for any other emergency expenses? It looks like regulators believe that those families would indeed be better off not being able to pay their water bills.

Of course, over-borrowing is an issue (as are abuse and fraud), but regulators are merely clamping down on symptoms here. Society is confronted with a dilemma: either those households are unable to pay their bills or buy enough food, or they might face over-indebtedness… None of those two options are attractive. But in such a situation, it is customers’ responsibility to choose. If they can avoid payday lenders, so they should. If they really can’t, this option should remain on the table. Sam Bowman from the Adam Smith Institute made very good comments on BBC radio Wales earlier today (see here from 02:05:00) on this topic.

I know I am repeating myself, but you cannot regulate problems away.

Crowdfunding, naivety and scandals

John Kay wrote an interesting article for the FT yesterday, titled “Regulators will get the blame for the stupidity of crowds.” He argues that, despite crowdfunding and P2P enthousiasts blaming regulators for being too slow and too cautious, this new market will eventually crash and trigger calls for more advanced regulation as well as the setup of compensation schemes. Desintermediation firms would then reintermediate lending and effectively transform into… banks.

I partly agree with Kay. A collapse/crash/losses/fraud/scandals is/are inevitable. And this is a good thing.

I have already written about the importance of failure in free market financial systems. New financial innovations need to experience failures in order to end up reinforced, to distinguish what works from what doesn’t work. This is a Darwinian learning process. The system then becomes ‘antifragile’. Consequently, the state should refrain from intervening in order not to postpone this necessary learning process and resulting adjustments. When crowdfunding crashes, the state should resist any call for intervention/bailout/regulation. This is the only way crowdfunding can become a mature industry.

I however also partly disagree with Kay, who I believe does not see the bigger picture.

Kay argues that investors (in this case ‘crowds’) are naïve. That intermediation has benefits and non-professional investors lack the ‘cynicism’ to assess the risk/reward profile of those investments.

Where Kay is wrong though, is in considering P2P lending as “a substitute for deposit account.” It is not. P2P lending is an investment. Unsophisticated retail investors can also lose much of their money by investing in various stocks. Or by betting on the wrong horse. I don’t believe investors mistake crowdfunding for bank deposits…

I think that what Kay also fails to see is that, if historically many start-ups and young SMEs have struggled to grow and eventually failed, it is partly because they lacked the funds required to grow. Some start-ups ended-up collapsing or selling themselves to larger competitors simply because funding became scarce at the second or third round of funding. This funding gap was particularly prevalent in some markets such as the UK (less so in the US). Some other markets, such as France, on the other hand, lack first round financing (seed funding, mainly provided by ‘Angel’ investors).

When the supply for loanable funds is scarce relative to the demand, demanded return on investment is high. Many new firms, particularly in non-growth markets, find it hard to cope with this situation and are pretty much avoided by venture capital investors. What equity crowdfunding and P2P lending do is to increase the supply of loanable funds, reducing the average required rate of return. Refinancing risk mechanically recedes, guaranteeing the success or the failure of an SME on its business strategy and execution alone.

In addition, crowdfunding multiply investment opportunities, making it easier to diversify a portfolio of investments. Historically, venture capital funds could not diversify too much if they wanted to maintain appropriate levels of returns.

Scandals are inevitable, but the learning mechanism inherent to the market process must be allowed to run its course. Learning, combined with the increased supply of loanable funds, would reduce the probability of scandals occurring in the long-run and make crowdfunding a solid industry.

Could P2P Lending help monetary policy break through the ‘2%-lower bound’?

The ‘cut the middle man’ effect of P2P lending is already celebrated for offering better rates to both lenders and borrowers. But what many people miss is that this effect could also ease the transmission mechanism of central banks’ monetary policy.

I recently explained that the banking channel of monetary policy was limited in its effects by banks’ fixed operational costs. I came up with the following simplified net profit equation for a bank that only relies on interest income on floating rate lending as a source of revenues:

Net Profit = f1(central bank rate) – f2(central bank rate) – Costs, with

f1(central bank rate) = interest income from lending

= central bank rate + margin and,

f2(central bank rate) = interest expense on deposits

= central bank rate – margin

(I strongly advise you to take a look at the details here, which was a follow-up to my response to Ben Southwood’s own response on the Adam Smith Institute blog to my original post…which was also a response to his own original post…)

Consequently, banks can only remain profitable (from an accounting point of view) if the differential between interest income and interest expense (i.e. the net interest income) is greater than their operational costs:

Net interest income >= Costs

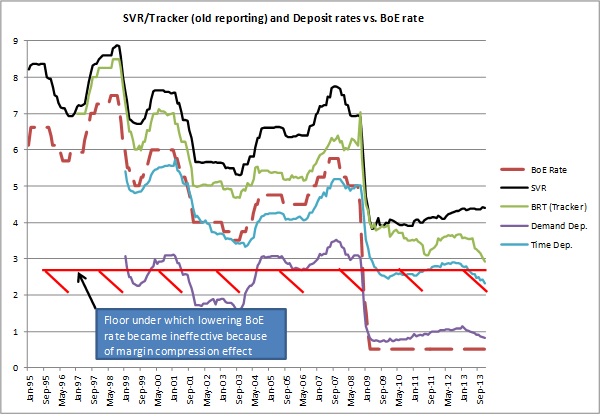

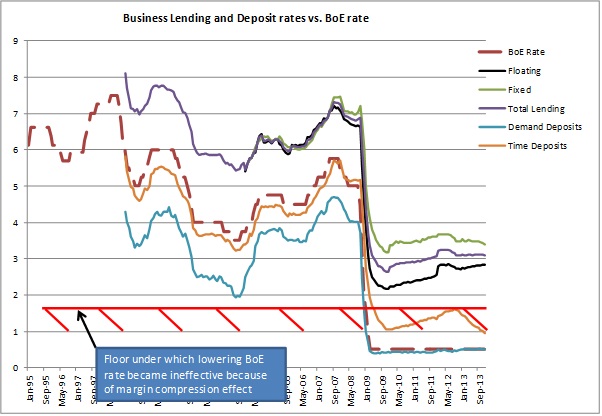

When the central bank base rate falls below a certain threshold, f2 reaches zero and cannot fall any lower, while f1 continues to decrease. This is the margin compression effect.

Above the threshold, the central bank base rate doesn’t matter much. Below, banks have to increase the margin on variable rate lending in order to cover their costs. This was evidenced by the following charts:

As the UK experience seems to show, banks stopped passing BoE rate cuts on to customers around a 2% BoE rate threshold. I called this phenomenon the ‘2%-lower bound’. I have yet to take a look at other countries.

Enter P2P lending.

By directly matching savers and borrowers and/or slicing and repackaging parts of loans, P2P platforms cut much of banks’ vital cost base. P2P platforms’ online infrastructure is much less cost-intensive than banks’ burdensome branch networks. As a result, it is well-known that both P2P savers and borrowers get better rates than at banks, by ‘cutting the middle man’. This is easy to explain using the equations described above, as costs approach zero in the P2P model. This is what Simon Cunningham called “the efficiency of Peer to Peer Lending”. As Simon describes:

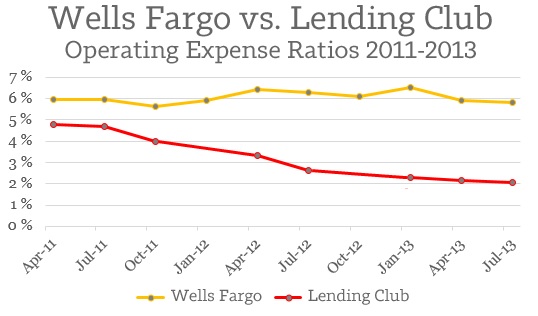

Looking purely at the numbers, Lending Club does business around 270% more efficiently than the comparable branch of a major American bank

Simon calculated the ‘efficiency’ of each type of lender by dividing the outstanding loans of Wells Fargo and Lending Club by their respective operational expenses (see chart below). I believe Lending Club’s efficiency is still way understated, though this would only become apparent as the platform grows. The marginal increase in lending made through P2P platforms necessitates almost no marginal increase in costs.

Perhaps P2P platforms’ disintermediation model could lubricate the banking channel of monetary policy the closer central banks’ base rate gets to the zero bound?

Possibly. From the charts above, we notice that the spread between savings rates and lending rates that banks require in order to cover their costs range from 2 to 3.5%. This is the cost of intermediation and maturity transformation. Banks hire experts to monitor borrowers and lending opportunities in-house and operate costly infrastructures as some of their liabilities (i.e. demand deposits) are part of the money supply and used by the payment system.

However, disintermediated demand and supply for loanable funds are (almost) unhampered by costs. As a result, the differential between borrowers and savers’ rate can theoretically be minimal, close to zero. That is, when the central bank lowers its target rate to 0%, banks’ deposit rates and short-term government debt yield should quickly follow. Time deposits and longer-dated government debt will remain slightly above that level. Savers would be incentivised to invest in P2P if the proposed rate at least matches them, adjusting for credit risk.

Let’s take an example: from the business lending chart above, we notice that business time deposit rates are currently quoted at around 1%. However, business lending is currently quoted at an average rate of about 3%. Banks generate income from this spread to pay salaries and other fixed costs, and to cover possible loan losses. Let’s now imagine that companies deposit their money in a time deposit-equivalent P2P product, yielding 1.5%. Theoretically, business lending could be cut to only slightly above 1.5%. This represents a much cheaper borrowing rate for borrowers.

P2P platforms would thus more closely follow the market process: the law of supply and demand. If most investments start yielding nothing, P2P would start attracting more investors through arbitrage, increasing the supply of loanable funds, and in turn lowering rates to the extent that they only cover credit risk.

The only limitation to this process stems from the nature of products offered by platforms. Floating rate products tend to be the most flexible and quickly follow changes in central banks’ rates. Fixed rate products, on the other hand, take some time to reprice, introducing a time lag in the implementation of monetary policy. I believe that most P2P products originated so far were fixed rate, though I could not seem to find any source to confirm that.

In the end, P2P lending is similar to market-based financing. The bond market already ‘cuts the middle man’, though there remains fees to underwriting banks, and only large firms can hope to issue bonds on the financial markets. In bond markets, investors exactly earn the coupon paid by borrowers. There is no differential as there is no middle man, unlike in banking. P2P platforms are, in a way, mini fixed-income markets that are accessible to a much broader range of borrowers and investors.

However, I view both bond markets and P2P lending as some version of 100%-reserve banking. While they could provide an increasingly large share of the credit supply, banks still have a role to play: their maturity transformation mechanism provides customers with a means of storing their money and accessing it whenever necessary. Would P2P platform start offering demand deposit accounts, their cost base would rise closer to that of banks, potentially raising the margin between savers and borrowers as described above.

It seems that, by partly shifting from the banking channel to the P2P channel over time, monetary policy could become more effective. I am sure that Yellen, Carney and Draghi will appreciate.

Regulating problems away doesn’t work

By ‘regulating’ the symptoms one does not cure the underlying disease. A few more examples in the press of this phenomenon that I keep describing:

– It’s no news that banks are being pressurised from all sides by regulation and lawsuits. The results? Banks aren’t that profitable anymore and remuneration stalls or even falls. Victory then? Wait a minute. Bloomberg reports that there is increased demand for young bankers by private equity funds, which are unsurprisingly more lightly regulated. This is part of a bigger trend that sees investors, funding and, as a result, credit, fleeing the traditional banking system towards the higher-yielding shadow banking system.

– The Economist also reports the same rebalancing towards shadow banking in China. I have already called China a ‘Spontaneous Finance Frankenstein’ given its strong, unnatural, regulatory-driven financial sector. This is typical:

China’s cap on deposit rates at banks is causing money to flood into shadow-banking products such as those offered by “trust” companies in search of higher yields. Offerings by internet firms, with their large existing customer bases, have opened the spigots wider. […]

Some see these online firms as a serious long-term threat to banks and the government’s ability to control the financial sector, prompting noisy demands (mostly by banks) to regulate the upstarts. Regulators have not yet expressed a clear view, but some observers see signals of a looming regulatory crackdown in attacks by the official media; a financial editor on the state-run television network recently branded online financial firms vampires and parasites.

What would be the effects of regulators successfully regulating those various areas of the shadow financial sector? A ‘shadow shadow’ banking sector would emerge. Liquidity, when in abundance, always finds its way. Regulation drives financial innovations, creating systemic risks through complex shadowy interlinked financial products and entities.

One does not regulate symptoms away. Market actors are the only natural, and the best, regulators.

News digest: Scotland, CoCos and electronic trading

Sam Bowman had a very good piece on the Adam Smith Institute blog about Scotland setting up a pound Sterling-based free banking system unilaterally (yeah I know I keep mentioning this blog now, but activity there seems to have been picking up recently). It draws on George Selgin’s post and is a very good read. One particular point was more than very interesting in the context of my own blog (emphasis added):

George Selgin has pointed to research by the Federal Reserve Bank of Atlanta about the Latin American countries that unilaterally use the dollar. Because these countries – Panama, Ecuador and El Salvador – lack a Lender of Last Resort, their banking systems have had to be far more prudent and cautious than most of their neighbours.

Panama, which has used the US Dollar for one hundred years, is the most useful example because it is a relatively rich and stable country. A recent IMF report said that:

“By not having a central bank, Panama lacks both a traditional lender of last resort and a mechanism to mitigate systemic liquidity shortages. The authorities emphasized that these features had contributed to the strength and resilience of the system, which relies on banks holding high levels of liquidity beyond the prudential requirement of 30 percent of short-term deposits.”

Panama also lacks any bank reserve requirement rules or deposit insurance. Despite or, more likely, because of these factors, the World Economic Forum’s Global Competitiveness Report ranks Panama seventh in the world for the soundness of its banks.

I don’t think I have anything to add…

SNL reported yesterday that Germany’s laws seem to make the issuance of contingent convertible bonds (CoCos) almost pointless. This is a vivid reminder of my previous post, which highlighted some of the ‘good’ principles of financial regulation and which advocated stable, simple and clear rules, a position I have had since I’ve opened this blog. All authorities and regulators try to push banks (including German banks) to boost their capital level, which are deemed too low by international standards. CoCos, which are bonds that convert into equity if the bank’s regulatory capital ratio gets below a certain threshold, are a useful tool for banks (as it allows them to prevent shareholder dilution by issuing equity) and investors (whose demand is strong as those bonds pay higher coupon rates). Yet lawmakers, who love to bash banks for their low level of capitalisation, seem to be in no hurry to provide a clear framework that would allow to partially solve the very problems they point at in the first place… This is a very obvious example of regime uncertainty. As one lawyer declared:

One thing is clear: Nothing is clear

Bloomberg reports that FX traders are facing ‘extinction’ due to the switch to electronic trading. In fact, this has been ongoing for now several years, with asset classes moving one after another towards electronic platforms. Electronic trading now represents 66% of all FX transactions (vs. 20% in 2001). Traditional traders are going to become increasingly scarce and replaced by IT specialists that set and programme those machines. Overall, this should also mean less staff and a lower cost base for banks that are still plagued by too high cost/income ratios. Part of this shift is due to regulation, which makes it even more expensive to trade some of those products. This only reinforces my belief that regulation is historically one of the primary drivers of financial innovation, from money market funds to P2P lending…

Banks’ branches/IT problems, and bank regulation vs. freedom

Barclays this week unsurprisingly announced the closure of a quarter of its 1600 branches. A ‘person familiar with the plans of Barclays’ said:

This is a fundamental 100-year transformation of the banking industry, that’s what I think we are seeing.

He/she is right. Though this has been obvious to banking innovators for a while already. SNL expands on that here and mentions high cost/income in retail banking. An analyst:

No bank in Europe can avoid the online banking issue. It is the future of the bank business.

As I have already said, it questions the plans of some of British politicians to cap the market share of large banks. How could their plan work when banks are already slashing branches by the thousands and when new and growing banks are increasingly established online or within other types of stores (see Tesco Bank, which has no actual branch but ‘in-store branches’ within its Tesco supermarkets). Politicians are able to foresee trends and innovation you said? How can one trust people who can only offer yesterday’s solutions to tomorrow’s problems? Same question about general banking regulation…

Anyway, banks also have some serious work to do. Many of them have antiquated IT systems, which makes us think that a transition to an IT-heavy (or perhaps IT-only…) banking business model won’t be smooth… UK banks have experienced a number of IT problems over the past few months (payment systems down mainly) as a result of their underinvestment in basic IT and the accumulation of various systems on top of one another following acquisitions, without never having really tried to integrate them all.

I personally check my accounts a lot more often now that I have access to smartphone apps, and I am certainly not the only one to do so. With the growth of mobile and contactless payments and the reduction in the number of hard cash transactions, the pressure on banks’ IT systems will become enormous. Increased mobile transaction volumes will also impact mobile telecom networks, though they often more rapidly update their systems than banks. What’s going to be interesting is that banks will increasingly rely on the infrastructure of private mobile and internet telcos. This emergent symbiosis may well accelerate the development of mobile networks, in terms of speed, security and coverage.

And banks better be in a hurry. As they now have payment systems competitors such as Paypal or Bitcoin, which ironically would also benefit from the same technological developments. Telcos could potentially also enter the payment space, as Kenya’s Safaricom did with M-Pesa.

Unrelated, a good piece by Sean Ryan on SNL (gated link) called “Bank regulation versus Americans’ freedom”, and reminiscent of one of my previous posts. This is Sean:

The power to regulate banks is impeding the ability of law-abiding citizens to exercise their rights. Washington is full of people with very strong ideas about how the rest of us should live, and I fear that increasingly intrusive bank regulation has given them an opening to do something about it.

[…]

Given the rapid proliferation of nominally legal activities being exiled from the economic mainstream by bank regulators, it seems only a modest exaggeration, and less modest by the week, to suggest that we are incubating a fourth branch of government. And this one isn’t so hamstrung by those pesky checks and balances.

I couldn’t have said it better myself.

Recent Comments