Banks don’t lend out reserves. Or do they?

Over the last weeks/months there has been a lot of agitation in some circles of the financial blogosphere: are banks lending out their reserves? The matter might sound trivial, but it theoretically impacts various monetary policies, such as quantitative easing. I won’t speak about that here. For those of you who don’t know what reserves are, here is a quick reminder:

The money supply comprises several elements. To make things simple the monetary base is the ‘real’ money (remnants of the gold standard and since then, created by the central bank) and the rest of the money supply is some sort of credit money created by the banking system. The ‘real’ money (monetary base) is also what we call high-powered money, and comprises both physical cash and… reserves held by banks at their respective central banks. Credit money created by banks is actually a claim on high-powered money, or high-powered money substitute. Reserves are convertible into physical cash and vice versa. In the UK, the monetary base represents about 17% of M4 (a measure of the money supply that does not include reserves). Reserves represent 82% of the monetary base.

Frances Coppola keeps reiterating again, and again, and again, and sometimes again, that banks don’t lend out reserves. She wrote her latest piece on the topic last week on the Forbes website. The title couldn’t be clearer: “Banks Don’t Lend Out Reserves”

A simple question that could come to anyone’s mind is: what do banks lend out then?

To be honest, I think that a large part of the misunderstanding comes from semantics. I actually agree with Frances on a number of points she makes. I have some objections to her ‘extreme’ view, or at least ‘extreme semantics’. Things aren’t that clear-cut.

While the endogenous money view suffers in my opinion from fallacy of composition, it looked to me at first that the view that banks don’t lend out their reserves suffered from the converse fallacy, the fallacy of division. But it doesn’t look like Frances falls in that trap, given what she made clear in the comment section of her article.

To be clear, banks do need reserves. If a (single) bank makes a loan to a customer, the bank is going to increase both its assets and its deposits (liabilities) by the amount of the loan. So far it does seem that the bank has created money out of thin air. But what happens if the customer withdraws the money from the bank? Deposits will get back to their previous amount, creating a discrepancy with the total loan figure. At the same time, there will be a drain on the bank’s reserves equal to the amount of the loan, as reserves will have been converted into physical cash (while total high-powered money remained the same). Seen this way, we could probably say that banks do lend out reserves.

What happens if the customer doesn’t withdraw the money but pays with it for a good by bank transfer? The drain on reserves still occurs as the beneficiary bank knocks on the door of the borrower’s bank to get hold of the money. In this case again, we could probably say that banks do lend out reserves.

The borrower’s bank also sees its deposits decrease while, on the other hand, the beneficiary bank experiences a deposit and reserves inflow. As a result, its deposit base grows without lending beforehand. Its now increased reserves will allow it to invest or lend more. This clearly nuances Frances’ claim that

when a bank creates a new loan, it also creates a new balancing deposit. It creates this “from thin air”, not from existing money: banks do not “lend out” existing deposits, as is commonly thought.

As we can see, reserves are used for two things: cash withdrawals and interbank settlements.

Let’s now consider the banking system as a whole in a closed economy. If lending leads to cash withdrawals, we could say again that banks lend out their reserves. However, let’s consider the following case: nobody ever withdraws cash. In this situation, all payments are made by electronic bank transfer. While individual banks experience fluctuations in their reserves, the total amount of reserves in the system never changes. Here, we could say that, indeed, banks don’t lend out reserves.

Here is what I meant by fallacy of division: what is true of the system as a whole isn’t for individual banks.

But so far, apart from semantic issues, I think that Frances and I agree although I wish she were more precise in differentiating single banks from the banking system as a whole. However, what I (kind of) disagree with is about her treatment of reserves as a source (or not) of lending and deposit creation. Frances says:

The volume of excess reserves in the system is what it is, and banks cannot reduce it by lending. […]

The volume of excess reserves in the system is what it is, and banks cannot reduce it by lending. They could reduce excess reserves by converting them to physical cash, but that would simply exchange one safe asset (reserves) for another (cash). It would make no difference whatsoever to their ability to lend. Only the Fed can reduce the amount of base money (cash + reserves) in circulation. While it continues to buy assets from private sector investors, excess reserves will continue to increase and the gap between loans and deposits will continue to widen.

This is something I cannot agree with. She is right to say that reserves will permanently be higher than before they were created (at least until the central bank tries to destroy them one way or another). But she overlooks the multiplier effect on lending and deposit expansion.

Assuming no reserve requirements, a fractional reserve bank will estimate how much high-powered money it needs to retain in order to face withdrawals and settlements. It is well-documented that banks in free banking systems naturally maintained reserves. Let’s assume that a whole banking system estimated that it needed to maintain 10% of the amount of its deposits as reserves to face settlements and withdrawals without endangering its existence. This would de facto become an internally-defined reserve requirement. The system can now create a maximum amount of demand deposits (claims on high-powered money) equal to 1/RR = 1/0.10 = 10 times the amount of reserves in its vaults*.

Now let’s get back to the situation described in Frances’ article. Reserves have been created, but have not been ‘lent out’ apparently. Of course, as Frances said, those reserves will not leave the system, unless they are withdrawn. But, they theoretically do provide banks with the ability to create extra deposits ‘out of thin air’ (the pyramiding process), allowing them to maintain their pre-crisis reserves to deposits ratio. And, as deposits expand, the reserves would not disappear but would simply not be considered ‘in excess’ anymore…

The question becomes: why didn’t banks expand their loans and deposit base in line with the increase in reserves? According to the chart below, the M2 multiplier (obtained by dividing all demand and saving deposits by the monetary base), declined significantly when the Fed started its quantitative easing policies.

I don’t think anybody has a clear answer to this. Low demand for loans, the Fed now paying interests on excess reserves, maintenance of precautionary excess reserves to face a possible future liquidity squeeze as long as the crisis isn’t completely over, are some of the possible underlying reasons. From my experience, the third reason is highly likely. I’ve heard many banking executives over the past few years who made clear that they were temporarily hoarding extra cash and reserves not to lend but… “just in case”.

* This multiplier is obviously a very simple one. Chester A. Phillips, in its famous 1921 book Bank Credit, identified the maximum amount x that can be lent out as:

, with c being the amount of reserves deposited, r the reserve/deposit ratio and k the derivative deposit/loan ratio (derivative deposits being the amount of newly-created deposits by lending that are not withdrawn or transferred by the depositors).

, with c being the amount of reserves deposited, r the reserve/deposit ratio and k the derivative deposit/loan ratio (derivative deposits being the amount of newly-created deposits by lending that are not withdrawn or transferred by the depositors).

In 1984, Alex Mcleod also wrote a brilliant, but barely readable, book called Principles of Financial Intermediation. He covers pretty much all possible and theoretical cases involving credit expansion based on the public’s acceptance ratio for claims (notes and deposits) on ‘money proper’, reserve to deposit ratio of financial intermediaries, external drain in case of an open economy, simple, cross and compound pyramiding (when the claims on money of one or several institutions can be used as reserves by other institutions)… There is no way I can reproduce his massive equations here…

Moreover, things get even more complex when you add in secondary reserves (very liquid low-yielding financial instruments almost instantly convertible into cash), as well as technology and financial innovations that allow banks to economise on reserves.

The central bank funding stigma

Yesterday the Federal Reserve Bank of New York published a brand new study about the stigma associated with banks borrowing from the central bank’s discount window. That was a nice coincidence following my response to Scott Fullwiler on the MMT and endogenous money theory, which seems to ignore this stigma (or at least to downplay its impact) and to consider that banks freely borrow from the central bank, providing a perfectly elastic high-powered money (reserves) supply. On the contrary, in my view, the stigma is one of the fundamental reasons that undermine the endogenous money theory.

Essentially, the NY Fed does not see much reason for this stigma to exist, but acknowledges that it does exist… I think they entirely forgot the possible impacts on a bank and its stakeholders of being considered illiquid, which I described in my previous post. Nonetheless, they made some good points (see below). A key point in my opinion is that banks are willing to pay more for other sources of funding than use the cheaper discount window.

The four main hypotheses they tested were very US-centric but interesting nonetheless. They found that:

- Banks inside the New York District were 14% less likely to experience the stigma than banks outside of the district (admittedly not that much difference)

- Foreign banks were 28% more likely to experience the stigma than similar US peers

- The largest the financial markets disruption, the higher the stigma

- The stigma does not decline when more banks utilise the discount window

Photo: MoneyAware

Blame the rich for the next asset bubble. Or not.

First of all, happy new year to all of you! Fingers crossed we don’t witness another market crash this year! 🙂

Indeed, credit markets are hot. Equity markets are also hot. The FT published an article yesterday with some striking facts about the ‘improvements’ in credit markets over the past couple of years. Some would say that it’s encouraging. I am not convinced…

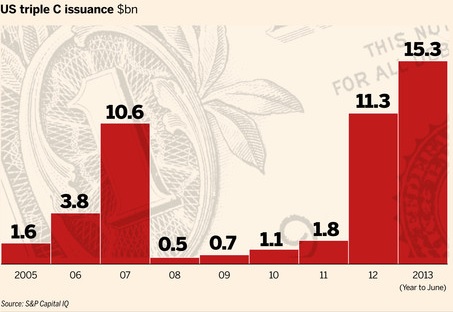

Most credit indicators are close to or above their pre-credit crisis high. Sales of leveraged loans and high-yield bonds are above their pre-crisis peak. The average leverage level of US LBOs is back to 2006 level. Issuance of collateralised loan obligations is close to its pre-crisis peak. Even CCC-rated junk bonds are way above their previous peak. I’ve already mentioned some of those facts a few months ago.

In a relatively recent presentation, Citi’s strategist Hans Lorenzen confirmed the trend: central banks are indirectly suppressing most risky investments’ risk premia. Most investors expect junk bonds’ spreads to tighten further or at least to stabilise at those narrow levels and emerging markets bonds and equities, as well as junk bonds are now among investors’ top asset classes .

My ‘theory’ at the time was that (see also here), if investors were piling in increasingly riskier asset classes, bringing their yield down to record low levels in the process, and nonetheless accepting this level of risk for such low returns, it was because current central bank-defined nominal interest rates were below the Wicksellian natural rate of interest. Inflation, as felt by investors rather than the one reported by national statistics agencies, was higher than most real rates of return on relatively safe assets. In order to see their capital growing (or at least to prevent it from declining), they were forced to pick riskier assets, such as high-yield bonds, which were not really high-yield anymore as a result but remained junk nonetheless. This would result in capital misallocation as, under ‘natural’ interest rate conditions, those investments would have never taken place. Thomas Aubrey’s Wicksellian differential, an indicator of the likely gap between the nominal and the natural rates of interest, was, in line with credit markets, reaching its pre-crisis high and seemed to confirm that ‘theory’.

Well, I now think that not all investors are responsible for what we are witnessing today. The (very) rich are.

This came to my mind some time ago while reading that FT piece by John Authers. This was revealing.

“Their wealth gives them scope to try imaginative investments, but they are terrified of inflation, even as deflation is emerging as a greater risk. That is in part because inflation for the goods and services bought by the very rich is running about 2 percentage points faster than retail inflation as a whole in the UK.” (my emphasis)

In the UK, real gilts’ yields were already in negative territory: adjusted by the (potentially underestimated) consumer price index, gilts were yielding around -1% early 2013. Savers were effectively losing money by investing in those bonds. Now think about the rich: by investing in such bonds, they would get a real return of around -3% instead.

Moreover, “71 per cent of respondents said they were more worried now about a steep rise in inflation than they were five years ago.”

Does it start to make sense? The cost of living I was mentioning earlier is increasing particularly quickly for the rich. And… they are the ones who own most financial assets. In order to offset those rising living costs, they naturally look for higher-yielding investments. And it is exactly what the FT reports:

“Their favourite asset classes for the next three decades are emerging markets equities, developed equities and agricultural land, in that order. Private equity comes close after farmland, while art and collectables were also a more popular asset class than any kind of bonds. […]

Hedge funds, as a group, have not fared well since the crisis. But wealthy investors preoccupied by inflation, and robbed of the easy option of bonds, are evidently disposed to give them a try, with an average projected allocation for the next three decades of 25 per cent. Meanwhile, the chance of a bubble in agricultural land prices, or in art, looks very real.”

Are the rich responsible for our current frothy markets then? Obviously not. They are acting rationally in response to central banks’ policies. Nonetheless, this raises an interesting question. Mainstream economics only considers a high aggregate inflation rate as dangerous. What about ‘class warfare’-type inflation? It does look like inflation experienced by one socioeconomic class could inadvertently lead to asset bubbles and bursts, despite aggregate inflation remaining subdued. This may be another destabilising effect of monetary injections on relative prices.

Granted, central banks possibly are on a Keynesian’s ‘euthanasia of the rentier’-type scheme in order to try to alleviate the pain of over-indebted borrowers (and/or to encourage further lending). But financial repression avoidance might well end-up coming back with a vengeance if savers’ reactions, and in particular, rich savers’, make financial markets bubble and crash.

Charts: FT (link above), Citi and Societé Générale

Cato Institute’s 31st Monetary Conference – Was the Fed a good idea?

About two weeks ago, the US-based think tank Cato organised its annual monetary conference. Great panels and very interesting speeches.

Three panels were of particular interest to me: panel 1 (“100 Years of the Fed: What Have We Learned?”), panel 2 (“Alternatives to Discretionary Government Fiat Money”), panel 3 (“The Fed vs. the Market as Bank Regulator”).

In panel 1, George Selgin destroys the Federal Reserve’s distorted monetary history. Nothing much new in what he says for those who know him but it just never gets boring anyway. He covers: some of the lies that the Federal Reserve tells the general public to justify its existence, pre-WW2 Canada and its better performing monetary system despite not having a central bank, the lack of real Fed independence from political influence and……the Fed not respecting Bagehot’s principles despite claiming to do so. In this panel, the speech of Jerry Jordan, former President of the Federal Reserve Bank of Cleveland, is also very interesting.

In panel 2, Larry White speaks about alternatives to government fiat money, counterfeiting laws and state laws making it illegal to issue private money. Scott Sumner describes NGDP level targeting. Here again, nothing really new for those who follow his blog, but interesting nonetheless (even though I don’t agree with everything) and a must see for those who don’t.

In panel 3, John Allison provides an insider view of regulators’ intervention in banking (he used to be CEO of BB&T, an American bank). He argues that mathematical risk management models provide unhelpful information to bankers. He would completely deregulate banking but increase capital requirements, which is an original position to say the least. Kevin Dowd’s speech is also interesting: he covers regulatory and accounting arbitrage (SPEs, rehypothecation…) and various banking regulations including Basel’s.

Overall, great stuff and you should watch the whole of it (I know, it’s long… you can probably skip most Q&As).

PS: Scott Sumner also commented on the Pope’s speech on “evil incarnate”. Reminds me of the vocabulary I used…

News digest

I have been so busy since last week that I didn’t have much time to write for this blog… And, to tell you the truth, I was almost shocked: barely any news on banks capital, regulation, monetary policy, etc, over the past few days. Sure, the ECB cut its rate by 25bp to 0.25%, but I’m not sure I should comment within the scope of this blog: I am still not convinced by such such a diverse monetary union as the Eurozone and find it hard to believe we can actually set a common interest rate for all country members within the union… Anyway, today I only wish to comment on a few articles published over the last few days.

A very interesting article published on SNL (subscription required) called Everybody wants to rule the world, including bank regulators, in which an analyst argued that “Banks are not only facing over-regulation. They are also emerging as a convenient channel through which regulators can extend their reach far beyond their legal writ.” You probably understand as well as I do how dangerous this is.

I found out yesterday that Bear Stearns liquidators filed a lawsuit against the three credit rating agencies for alleged manipulation of structured products’ ratings. They are basically arguing that, if ratings had been right, Bears Stearns’ hedge funds would not have collapsed. Blaming the rating agencies because…..hedge funds collapsed? We are not talking about simple retail investors here. We are talking about sophisticated investors. Aren’t hedge funds supposed to undertake their own analysis? Are they just blindly investing in various assets? If hedge funds managers and analysts did not believe in rating agencies’ ratings, why did they invest in those assets the first place? Or perhaps they indeed did not believe in those ratings and took on the risk on purpose. In both cases, we cannot blame the agencies for the lack of competence of those highly-remunerated hedge funds employees.

Yesterday, the FT reported that shadow banks had been among the biggest beneficiaries of the Fed’s monetary policies. I’ve already argued that it might well be a sign that real interest rates are too low (i.e. lower than the equilibrium natural rate of interest). As a result, regulators wish to regulate (of course) this segment of the financial system. My guess is that surplus liquidity would then shift to another less-regulated sector or asset class, as it always does.

A few days ago, I read in horror that Germany may start backing the financial transaction tax. A tax of 0.1% of the value of the transaction (as is proposed on cash instruments) would be a massive drain of wealth: just imagine what would happen to a newly set-up EUR100bn mutual fund (ok, no new fund would ever be of that size, but follow me just for the intellectual exercise). The fund has evidently to invest those 100bn on behalf of its clients, meaning they have to buy EUR100bn of assets. Taxing 0.1% off the total value of the transactions would mean…EUR100m to pay in taxes. This is EUR100m that EU states would withdraw from people’s savings and pensions. Bad idea.

In the Wall Street Journal, a Fed insider described how disillusioned he was from the Fed and QE: he ‘apologises’ to Americans (Scott Sumner comments on this) for QE’s bad or lack of effects. While I do not necessarily share everything he said, I also dislike the Fed’s large scale market manipulation.

On Free Banking, George Selgin criticised this Business Insider piece about airlines debasing their reward points. Reminds me of my own response to Matt Klein on the exact same topic a few weeks ago. No guys: those cases do not reflect free banking and private currencies.

Well, that’s all for the catch up.

The ‘great search for yield’ update, Taleb on bank disintermediation and Coeuré on Wicksell

This is a quick update on my post of last week on the rush for yield among private investors and what it meant in terms of interest rate disequilibrium.

Following my post, Thomas Aubrey from Credit Capital Advisory kindly provided me with an update of his ‘Wicksellian differential’ chart. You can also find it here.

As you can see the differential between the estimated natural rate and the money rate of interest in the US have kept increasing and almost reached pre-crisis peak. According to his calculation, the potential differential now reaches………10%. It’s indeed huge. Try for a second to imagine the Fed all of a sudden increasing their target interest rate by 10%…… No you’re right, we just can’t imagine it. Frankly, I hope his calculation is wrong but…I wouldn’t bet my life on it. Consequently, Thomas Aubrey believes that it backs up my claim about malinvestments.

As you can see the differential between the estimated natural rate and the money rate of interest in the US have kept increasing and almost reached pre-crisis peak. According to his calculation, the potential differential now reaches………10%. It’s indeed huge. Try for a second to imagine the Fed all of a sudden increasing their target interest rate by 10%…… No you’re right, we just can’t imagine it. Frankly, I hope his calculation is wrong but…I wouldn’t bet my life on it. Consequently, Thomas Aubrey believes that it backs up my claim about malinvestments.

Meanwhile, in a speech called ‘The economic consequences of low interest rates’ at the International Center for Monetary and Banking Studies on the 9 October, Benoit Coeuré, member of the Executive Board of the European Central Bank, misunderstood Wicksell and inflation, justifying very low interest rates. Not only Mr Coeuré seems to believe that CPI adequately reflects inflation, but also, according to him, inflation is always zero when the money rate of interest equals the natural rate. This is not true: real shocks can temporarily push inflation one way or another, but over the longer term productivity becomes the main driver behind inflation and deflation. In a world of productivity increases (and increasing output), deflation should be the norm (as it was the case at the end of the 19th century and early 20th). A zero level of inflation in this context would actually mean that there is hidden inflation. George Selgin has written a lot on this. See his Less than Zero book or this video.

Last Friday, FT’s Henny Sender discussed the Fed’s impact on markets. According to a Hong Kong-based hedge fund “the Fed is always there. It is clear that it will not tolerate a decline in asset values. If you sell in the face of QE, you look like an idiot.” Sounds like the best way to completely distort markets. Free markets you said?

Today, John Authers, in another FT piece, says that “Western economy is overcentralised, creating extra risk”. I obviously won’t disagree with him. He cites Nicholas Taleb (reminding me of Larry White). But one thing particularly struck me: Taleb seems to think that hedge funds “are developing strategies that aim to disintermediate the banks, such as loan funds.” This is very, very close to my own opinion, which I haven’t mentioned yet on this blog: technological developments will enable shadow banking to grow under one form or another to desintermediate credit creation. This is something big, and it will require many blog posts and possibly a research paper…and some time.

Macro(un)prudential regulation

From a free-market perspective, one can only be against macroprudential regulation. Macroprudential regulation is the new fashion among regulators and other policy-makers. It’s trendy, and I understand why: it sounds clever enough to impress friends during a night out. It aims at monitoring a few macroeconomic indicators in order to try to ‘cool’ the system if it seems to be overheating. Those tools are supposed to be countercyclicals: if the economic environment is good, regulators can force the whole banking system to start accumulating extra equity or liquid assets for example, or decide to cap the amount that all banks can lend to mortgage borrowers. As you can guess, it is not the kind of self-regulating financial system I particularly appreciate.

This is once again a typical example of trying to fix the symptoms created by the system’s defects, without touching those defects. Wrong monetary policy? Bad government policies and subsidies? Of course not, the financial system is inherently bad and fragile, regulators and politicians said. Well, to be fair, this is their job and how they make money.

Lars Christensen, chief analyst at Danske Bank and author of The Market Monetarist blog, had a couple of niece pieces against macroprudential regulation recently. In the first one, he quotes and agrees with a recent WSJ article by John Cochrane, financial economist at the University of Chicago (also available on his blog):

This is Cochrane:

Interest rates make the headlines, but the Federal Reserve’s most important role is going to be the gargantuan systemic financial regulator. The really big question is whether and how the Fed will pursue a “macroprudential” policy. This is the emerging notion that central banks should intensively monitor the whole financial system and actively intervene in a broad range of markets toward a wide range of goals including financial and economic stability.

For example, the Fed is urged to spot developing “bubbles,” “speculative excesses” and “overheated” markets, and then stop them—as Fed Governor Sarah Bloom Raskin explained in a speech last month, by “restraining financial institutions from excessively extending credit.” How? “Some of the significant regulatory tools for addressing asset bubbles—both those in widespread use and those on the frontier of regulatory thought—are capital regulation, liquidity regulation, regulation of margins and haircuts in securities funding transactions, and restrictions on credit underwriting.”

This is not traditional regulation—stable, predictable rules that financial institutions live by to reduce the chance and severity of financial crises. It is active, discretionary micromanagement of the whole financial system. A firm’s managers may follow all the rules but still be told how to conduct their business, whenever the Fed thinks the firm’s customers are contributing to booms or busts the Fed disapproves of.

I completely agree with Cochrane.

And I completely agree with both of them. Christensen argues that the central bank’s goal is to provide nominal stability – to have a single target and stick to it, but that macroprudential regulation would involve manipulating many different tools having opposite effects, with likely unintended consequences. He then goes on to argue that if “markets are often wrong”, central banks are even worse and “have a lousy track record” at spotting bubbles.

Another important point made by Cochrane in my opinion is:

Third lesson: Limited power is the price of political independence. Once the Fed manipulates prices and credit flows throughout the financial system, it will be whipsawed by interest groups and their representatives.

= crony capitalism. This has plagued all corners of our capitalist system for ages, and when things turn bad, free markets/laissez-faire capitalism/liberalism/neoliberalism/ultra turboliberalism/add the one you want is blamed… Go figure.

Christensen’s second post, published a few days ago, refers to a Bloomberg article on the so-called ability of a new Finnish model to ‘forecast’ all cyclical up and downswings in the US over the past 140 years… He helpfully remembers that nobody is ever able to constantly beat the market. While this sounds like a rational expectations/efficient market hypothesis point of view (I don’t know what Lars actually believes in), I do agree with him (and no I don’t believe in rational expectations, but constantly beating the market requires non-human skills and information-gathering abilities). He then goes on to say that while this is relatively basic economics, “nowadays central bankers increasingly think they can beat the markets. This is at the core of macroprudential thinking.”

Obviously, the whole thing rests on the myth that the financial system is fragile and must be ‘safeguarded’ or ‘protected’ (see this IMF article) by ‘benevolent dictators’, in Christensen’s words. I would also add that macroprudential ideas are now new and have been already tried one way or another since the early 19th century (but how many regulators and economists remember that? See an example here).

This is how I see things: no central body can ever have perfect knowledge of what’s happening in the economy and what the various plans, wishes and wants of the millions of actors in the system are (I am obviously not the first one to say this. See Mises, Hayek, Friedman and so many others). As a result, any central intervention is bound to fail or create distortions in the economic landscape.

Central banks are a monopoly: they define nominal interest rates and base money supply unilaterally and can only adjust their policies with a time lag, after they have already affected the economy. A distorting monetary policy can easily kickstart asset bubbles: an increasing supply of ‘high-powered’ money (base money) not matched by an increase in the demand for money can easily lead to excess credit creation. If real estate prices boom due to the flow of credit towards the sector, is it reasonable to try to stop it? The flow of credit is already here, and if it cannot go where it wanted in the first place, it will find another place to go to. China and its wealth management products is a good example of this process.

Let’s consider a current example in the UK. Due to a combination of interest rates maintained too low for too long, misguided government schemes such as Funding for Lending and Help to Buy, compounded by Basel regulations that favour mortgage lending and local restrictions on housing supply, if ever a housing bubble appears, the solution will be to… blame the banks and artificially restrict LTVs or cap lending??? Right…

Finance is a spontaneous process: people can be very innovative at finding ways of bypassing restrictions to achieve their desired financing and saving goals. Macroprudential controls would only move the problem from one sector to another, without correcting its very source. Macroprudential regulation would also introduce an unwelcome dose of discretionary rules and micromanagement, which have destabilising effects on trust, markets and economic actors.

Photograph: Wikipedia

Recent Comments