George Selgin weighs in on the excess reserves/MM debate

I used to feel lonely in the ‘banks do/don’t lend out reserves’ debate. Almost everyone on the blogosphere seemed to have been converted by either a rough ‘banks create money out of thin air’ (see here and here) or a more subtle MMT endogenous money version of the story (see here). Reserves, we were told, were pretty much useless in the ‘modern’ monetary system. They were only used for interbank settlements (which actually still implies some serious constraints on lending and deposit expansion, but whatever).

So all the Fed’s, ECB’s and BoE’s quantitative easing was futile because the excess reserves those policies created merely kept accumulating with no chance of ever being ‘lent out’, because the banking system as a whole could not get rid of excess reserves. It’s not how it worked we were told. We were doomed to live in a world of permanently high excess reserves.

Imagine my relief when George Selgin started publishing three massive posts on interest on reserves and the crisis (here, here and here, and of course, let’s not forget Justin Merrill’s post, which made similar remarks). It’s a fascinating and highly recommended read. I just wish to point out a couple of his comments on the new reserve myth.

Here’s George:

it’s simple: “reserves” and “excess reserves” aren’t the same thing. Banks can’t collectively get rid of “reserves” by lending them — the reserves just get shifted around, exactly as Walter and Courtois suggest. But banks most certainly can get rid of excess reserves by lending them, because as banks acquire new assets, they also create new liabilities, including deposits. As the nominal quantity of deposits increases, so do banks’ required reserves. As required reserves increase, excess reserves decline correspondingly. It follows that an extraordinarily large quantity of excess reserves is proof, not only of a large supply of reserves, but of a heightened real demand for such, and of an equivalently reduced flow of credit.

And again:

Here is that silly fallacy again: for the question isn’t whether a lower rate of IOR can reduce banks’ total reserve balances. It is whether it can reduce their excess (“idle”) balances by inducing them to lend more. For while such lending wouldn’t serve to reduce the aggregate stock of reserves, it would lead to an increase in the nominal quantity of bank deposits, and a proportional increase in banks’ required reserves. So, even as they caution their readers that “Language Matters,” Antinolfi and Keister blunder badly by neglecting to heed the crucial distinction between the total quantity of bank reserves, which no amount of bank lending can alter, and the quantity of excess reserves, which, by means of sufficient bank lending, might always be reduced to zero.

And after quoting Frances Coppola, he concludes:

There you have it: banks can hold on to reserves, and yet lend all they wish to (though not, for some reason, overnight). Such a marvelous business! Whoever said that one can’t have one’s cake and eat it, too?

Frances Coppola wasn’t really pleased and replied on Forbes. But she left me confused. She does start by saying that she had been ‘sloppy’ with her use of the term ‘excess reserves’:

For the US, it would indeed be possible for a bank to reduce its excess reserves by converting them to required reserves.

But then, in the comment section, she adds a qualification in her reply to George Selgin:

I have never said that individual banks could not “lend away” excess reserves. Clearly banks do lend reserves to each other: I have said this many times. But I dispute that banks COLLECTIVELY can lend away excess reserves. Banks do not lend reserves to non-banks. The only way reserves can leave the banking system is in the form of physical cash. That is the point I was making in the Forbes post you quoted.

Wait, I don’t follow. There is no case of fallacy of composition here. What is true for an individual bank is also true for the system as a whole. A given bank can get rid of excess reserves by growing its loan book. This triggers a reserve drain (either by cash withdrawal or interbank settlement), leading to a reduction in the amount of reserves that this bank holds at the central bank, and an offsetting gain for the receiving bank (if interbank transfer).

But, given a fixed amount of excess reserves in the banking system, the system as a whole simply has to increase the amount of credit (and hence deposits) it extends in order to get rid of the reserves that it has in excess. For instance, if the system has 500 units of required reserves and 100 of excess reserves (600 in total), and that it is subject to a 10% reserve requirement, it merely has to grow its lending by 1,000 units to get rid of its excess. Total reserves in the system would not change (600), but excess reverses would all but vanish as they get converted into ‘required’ ones. This is precisely George’s point.

(of course things work a bit differently in systems with no reserve requirements, but as I have said elsewhere, an informal, market-determined, reserve requirement play the same role)

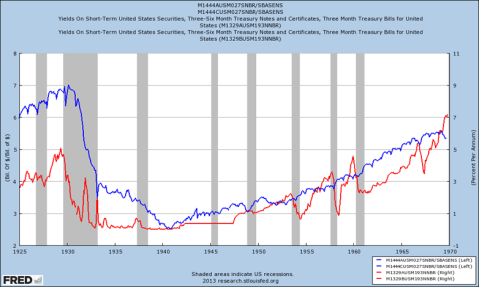

Let me remind my readers that the same situation occurred during the Great Depression. Excess reserves spiked and the money multiplier collapsed (see this previous post of mine and the following nice chart from Mark Sadowski). It then took 30 years for the multiplier to bounce back from its lows to close to its previous highs:

However, she’s very right that banks are/were also constrained by capital and liquidity requirements, and that the crisis is likely the primary driver of a reduction in lending. But it doesn’t seem to me that George disputes this.

I tend to agree with her that George seems to be underestimating the impact of regulatory capital requirements to an extent. I described in another post that regulators don’t seem to care much about regulatory minima or about whether or not a bank still have some loss-absorbing capital left: they force bank management to raise capital when it becomes lower than where they’d like it to be (even if capital ratios remain above minima they have themselves defined in the first place… go figure).

Consequently, despite having ‘excess capital’ from a formal and official point of view, banks did not have enough capital from the discretionary point of view of regulators in charge. They were forced to maintain or raise capital levels in the middle of the worst financial crisis in 50 years. Hard to think of a better pro-cyclical stance. Worse, from 2010 onwards, new tighter regulatory requirements were progressively implemented, which is in effect not the most effective way of kick-starting an economic recovery.

PS: I think Frances’ point that commercial banking rates were well above IOER and so are unlikely to hinder lending is more unclear than she thinks. Only risk-adjusted rates could give us an answer, as credit risk premia jump during a crisis, and capital requirements increase as customers suffer from rating downgrades. Moreover, liquidity risk also jumps so the liquidity premium associated to lending is raised (i.e. better to reduce profitability temporarily to survive in the long-run by not putting pressure on reserves). So at the end of the day, it’s hard to say whether the margin made on those loans was sufficient to cover the increased risk of loan loss and the increased risk of getting illiquid, especially after factoring in the operating costs of monitoring those borrowers (as opposed to pretty much zero operating cost in leaving the money at the central bank).

8 responses to “George Selgin weighs in on the excess reserves/MM debate”

Trackbacks / Pingbacks

- - 21 February, 2016

Leave a comment

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

Julien, I think this may be the beginning of a beautiful friendship.

George,

This would be a pleasure.

I am however afraid that my unfortunate and recurrent use of the term ‘incentivise’ will not be to your liking! 🙂

Julien, it is never too late to turn a new leaf! Consider yourself encouraged, prompted, led, inspired, motivated, emboldened (but not the least bit incentivised) to do so!

I am presently engaging with the economists at FRB Richmond on the matter of IOR and excess reserves. If you like, I will share some of that correspondence with you.

George, will do my best!

Yes that would be very interesting, thanks.

I have myself been engaged in a debate with a couple of BoE economists on the money creation topic, which I unfortunately couldn’t publish for confidentiality reasons.

Is your Cato email the right one to use? Thank you.

Hi Julien,

as you already mentioned in your previous post, it is a little bit unclear how Mark Sadowski obtained the long-run data from the FRED system so I’m kinda reluctant using this chart. Do you have any idea where to get the relevant data? Strictly speaking, I want a reliable source for a nice graph like this.

Thanks in advance, Anton

Anton,

Levi Russell, from the Farmer Hayek blog, told me a few months ago that it was possible by searching the following ID: M1444AUSM027SNBR

He also reconstructed the dataset and sent me a full chart from the Depression till today. I unfortunately can’t attach it to this comment.

I haven’t tried myself but feel free to try and let me know.

Great blogging