Modeling a Free Banking economy and NGDP: a Wicksellian portfolio approach (guest post by Justin Merrill)

My friend Alex Salter and his coauthor, Andrew Young, have an interesting new paper called “Would a Free Banking System Target NGDP Growth?” that I believe was presented at a symposium on monetary policy and NGDP targeting.

I too have wondered the same question. I believe there are real reasons why a dynamic economy might not have stable NGDP. One reason is demographic changes (maybe target NGDP per capita?). Another reason is problems with GDP accounting in general such as the underground economy, changes in workforce participation of women and the vertical integration of firms. Another micro-founded effect might be the income elasticity of demand and substitution effects. But even abstracting from these problems, it is still a worthy question to ask if monetary equilibrium is synonymous with stable NGDP and its relationship to free banking. If they are synonymous, we might expect stable NGDP from free banking. In my paper on a theoretical digital currency called “Wixle” I outline a currency that automatically adjusts its supply to respond to demand by arbitraging away the liquidity premium over a specified set of securities. This is a way to ensure monetary equilibrium without regard for aggregate spending, which is particularly useful if the currency is internationally used.

A small criticism I have of my free banking and Market Monetarist friends is that they often assert that monetary equilibrium and stable NGDP are the same thing, usually by applying the equation of exchange. As useful as the equation of exchange is, it is tautologically true as an accounting identity. But just as we know from C+I+G=Y, accounting identities’ predictive powers are limited when thinking about component variables. I have argued for the conceptual disaggregation of the money supply and money demand, because the motives for holding currency and deposits are different and the classification of money is more of a spectrum. So I was pleased to see that Salter and Young did this in their paper and added the transaction demand for money into their model. This leads them to conclude that a free banking system will respond to a positive supply shock, which results in an increased transaction demand for money, by stabilizing the price level rather than NGDP. This might be true, and whether this is good or bad is another question. Would this increase in currency lead to a credit fueled boom, or is this a feature and not a bug?

I have long been upset with the way that economists overly focus on reserve ratios and net clearings from a quantity perspective. This abstracts away from the micro-foundations of the banking system and ignores the mechanics of banking. This is the point I made at the Mises Institute when I rebutted Bagus and Howden. My moment of clarity for the theory of free banking actually came from reading the works of James Tobin and Gurley & Shaw, as well as Knut Wicksell. The determination of the money supply is the public’s willingness to hold inside money, and this willingness creates the profit opportunity for the financial sector to intermediate by borrowing short and lending long. I believe the case for free banking can be made more robust by adding the portfolio approach, as well as the transactions approach. I will outline here what that would look like without sketching a formal model.

The Model is a three sector economy: households, corporations and banks. Households hold savings in the form of corporate and bank liabilities and have bank loans as liabilities. Corporations hold real capital, bank notes and deposits as assets and bank loans, stocks and bonds as liabilities. Banks hold reserves, securities and loans as assets and net borrowed reserves, notes, deposits and equity as liabilities.

Households can hold their wealth in risky securities or safe, but lower yielding interest paying deposits that pay the risk-free rate in the economy or non-interest paying notes used for transactions. The model could include interest-free checking accounts, but these are economically the same as notes in my model.

Banks can then choose to invest in loans, securities or lending reserves. They fund investments largely by borrowing at the risk-free rate and borrowing reserves at the margin. Logically then, the cost of borrowed reserves will be higher than deposits but lower than that of loans and securities and arbitraging ensures this. If the cost of reserves goes above the return on securities, banks will sell bonds to households and lend reserves to each other. If the cost of reserves goes below the rate on deposits, banks will borrow reserves and deposit with each other. The return on loans and securities (adjusted for risk) will tend towards uniformity because they are close substitutes. Also, as Wicksell pointed out, if loan rates are below the return on securities or the return on real capital, households and firms would borrow from banks and invest.

Empirical evidence for the interest rate channels is provided here. Interestingly, the rules set out above were only violated in times of monetary disequilibrium, such as the Volcker contraction:

http://research.stlouisfed.org/fred2/graph/?g=1aRY

The natural rate of interest is equal to the return on assets for corporations. Most economists that try to model the natural rate mistakenly do it as the risk free rate or the policy rate. This is a misreading of Wicksell since he identified the “market rate” as the rate which banks charge for loans, and the important thing was the difference between the market rate and the natural rate. If the market rate is too low, people will borrow from banks and invest, increasing the money supply.

We can now apply the framework to the CAPM model and conceptualize the returns on various assets:

The slope of the securities market line (SML) is determined by the risk aversion/liquidity preference of the public. Should the public become more risk averse and demand a larger share of their wealth be in the form of money, they will sell securities in favor of deposits. If in aggregate, the household sector is a net seller, the only buyers are banks (ignoring corporate buybacks since this doesn’t change the results since corporations would end up needing to finance the repurchases with bank loans). So the banking sector would purchase the securities (at a bargain price) from households, crediting their accounts and simultaneously increasing the inside money supply. This becomes more lucrative as the yield curve steepens or other kinds of risk premia widen, increasing the net interest margins (NIMs). As the banking sector responds to changes in demand it equilibrates asset prices.

This is another way of coming to the same conclusion: that a free banking system would tend to stabilize NGDP in response to endogenous demand shocks. But how about supply shocks? We know that when the spread between the banks’ return on assets and costs of funding widens, the balance sheet will increase. An increase in productivity will raise both the return on new investments and the rate the banks have pay on deposits. We can assume for now these cancel out. But the public will have a higher demand for notes, and since notes pay no interest, they are a very cheap source of funding. This lowers the average cost of funding overall. However, more gross clearings will increase the demand for reserves and their cost of borrowing relative to the yield on other assets. This would put a check on overexpansion and excess maturity transformation. The net effect on the total inside money supply is uncertain, but probably positive assuming the amount of currency held by the public is larger than borrowed reserves by banks.

Another thing to consider about supply shocks: despite the lower funding costs of increased note issuance, an increase in the natural rate of interest will decrease banks’ net interest margins because their loan book will be locked in at the old, lower rate, but the rate on deposits will have to go up. This is a counter-cyclical effect (in both directions) that may outweigh the transaction demand effect. Another possible counter-cyclical effect is the psychological liquidity preference effect that accompanies optimism associated with supply shocks. So in a strong economy individuals will be more willing to hold the market portfolio directly, which flattens the SML. Depending on the strength of these effects, it may lead to different results than Salter and Young.

The real reason the Federal Reserve started paying interest on reserves (guest post by Justin Merrill)

I am fascinated by recent policies of interest on reserves, both positive and negative. I understand the argument for the People’s Bank of China paying interest on its deposits since they have a combination of a large balance sheet and high reserve ratios in order to control their exchange rate; their banks would go broke if 20% of their assets earned no income and their domestic inflation would run rampant if they didn’t curb lending. I also understand the logic for negative interest rates to stimulate the economies in Europe. I disagree with these policies, but there’s an internally coherent argument there. What hasn’t made sense to me is the Federal Reserve’s policy of paying interest on both required and excess reserves.

Why would the Fed simultaneously start the counterproductive policies of quantitative easing (QE) and interest on reserves (IOR)? Why would the Fed pursue the deflationary policy of IOR throughout the crisis when labor markets were weak and inflation was usually below their target? What if they could have achieved their policy goals as well or better by sticking to more traditional policies and not been stuck with such a large balance sheet and potential exit problem? My cynical intuition was that it was just a backdoor bailout to banks.

Determined to find the answer, I looked for statements and other sources from the Fed to find out the history of and justifications for IOR. What I finally found confirmed my suspicions and I think shows a big flaw in the Fed’s transparency and policy. What recently renewed my interest was Chair Janet Yellen’s Congressional testimony before the Senate in February, 2015. Senator Pat Toomey asked her about interest on reserves policy. Toomey used to be a bond trader, so he’s more financially savvy than most of his peers. I will summarize their dialogue about IOR but the video is available here and starts a little before one hour-seventeen minutes in: http://www.c-span.org/video/?324477-1/federal-reserve-chair-janet-yellen-testimony-monetary-policy

PT: In the past the Fed conducted monetary policy via Open Market Operations. You have said that you intend to raise the Fed Funds rate by increasing the interest paid on reserves. Since this will transfer money to big money center banks that would have gone to tax payers, why are you doing that instead of simply selling bonds? (emphasis added)

JY: We are paying banks a rate comparable with the market, so there is not a subsidy to banks. Our future contributions may decline when interest rates rise, but our contributions to the Treasury have been enormous in recent times.

Notice what she didn’t answer? The part of his question about why they are even using IOR at all!

According to the Fed’s Oct 6, 2008, press release:

The Financial Services Regulatory Relief Act of 2006 originally authorized the Federal Reserve to begin paying interest on balances held by or on behalf of depository institutions beginning October 1, 2011. The recently enacted Emergency Economic Stabilization Act of 2008 accelerated the effective date to October 1, 2008.

So we know the Fed was interested in using IOR as a tool prior to the crisis but weren’t in a hurry to do so until after the Lehman shock. The expedited authorization came from the TARP bill. So why were they interested in using it at all, and why did it become urgent and necessary in late September, 2008? The press release mentions “Paying interest on required reserve balances should essentially eliminate the opportunity cost of holding required reserves, promoting efficiency in the banking sector” and “Paying interest on excess balances should help to establish a lower bound on the federal funds rate. […] The payment of interest on excess reserves will permit the Federal Reserve to expand its balance sheet as necessary to provide the liquidity necessary to support financial stability while implementing the monetary policy that is appropriate in light of the System’s macroeconomic objectives of maximum employment and price stability.”

So paying interest on required reserves “promotes efficiency?” I think they are channeling Milton Friedman’s observation that reserve requirements are a tax on banks by forcing them to hold non-income earning assets. I’m not a fan of reserve requirements, and maybe it could be argued that they encourage disintermediation or alternative financing schemes that aren’t subject to the regulation, such as shadow banking, and that by paying IORR it offsets that. Fine, what I think is more interesting is the justification for interest on excess reserves. Why were they trying to provide liquidity without creating price inflation or overheating the labor market? Core CPI was below 2% at the time, PCE (an indicator the Fed looks at) was sharply negative, GDP numbers for the first two quarters were really weak and unemployment was trending up and was above 6% since August. There’s a lag to data, but in the October-early December timeframe we are focusing on here, they would have at least had August’s numbers.

Still not satisfied, I looked around at almost a dozen other Fed sources that tried to justify IOR. All of the sources said two or three things in particular: “Milton Friedman told us to pay interest on required reserves in 1959*, Marvin Goodfriend told us IOR could be used as a policy tool in 2002 and in 2008 we were having a hard time hitting our Fed Funds target.” I know hindsight is 20/20, but given the economic environment explained above, if you are providing liquidity and the economy is still stalling and you are missing your Fed Funds target on the low side, the problem is your target! You must REALLY trust your models to be so confident that a Fed Funds rate of two percent is worth defending in a liquidity crisis. I was about to chalk up the policy to mere incompetence and panicking in the fog of war when I came across this wonderful essay published by the Richmond Fed. It actually gives a fully honest account of what happened and why it was deemed urgent to start IOR:

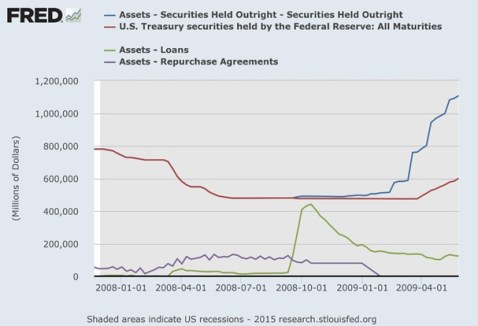

This feature became important once the Fed began injecting liquidity into financial markets starting in December 2007 to ease credit conditions. In making these injections, the Fed created money to extend loans to financial institutions. Those institutions provided as collateral securities from their portfolio that had, as a result of the financial market turmoil, become difficult to trade and value. This action essentially replaced illiquid assets in their portfolio with a credit to their account at the Fed, which would add reserves to the banking system. Adding reserves to the system will, under usual circumstances, exert downward pressure on the fed funds rate. At the time the Fed was not yet facing the zero-lower-bound on interest rates that it faces today. Thus, the injections had the potential to push the fed funds rate below its target, increasing the overall supply of credit to the economy beyond a level consistent with the Fed’s macroeconomic policy goals, particularly concerning price stability. To avoid this outcome, the Fed “sterilized” the effect of liquidity injections on the overall economy: It sold an equal amount in Treasury securities from its own account to banks. Sterilization offset the injections’ effect on the monetary base and therefore the overall supply of credit, keeping the total supply of reserves largely unchanged and the fed funds rate at its target. Sterilization reduced the amount in Treasury securities that the Fed held on its balance sheet by roughly 40 percent in a year’s time, from over $790 billion in July 2007 to just under $480 billion by June 2008. However, following the failure of Lehman Brothers and the rescue of American International Group in September 2008, credit market dislocations intensified and lending through the Fed’s new lending facilities ballooned. The Fed no longer held enough Treasury securities to sterilize the lending.

This led the Fed to request authority to accelerate implementation of the IOR policy that had been approved in 2006. Once banks began earning interest on the excess reserves they held, they would be more willing to hold on to excess reserves instead of attempting to purge them from their balance sheets via loans made in the fed funds market, which would drive the fed funds rate below the Fed’s target for that rate. When the Fed stopped sterilizing its liquidity injections, the monetary base (which is comprised of total reserves in the banking system plus currency in circulation) ballooned in line with Fed lending, from about $847 billion in August 2008 to almost $2 trillion by October 2009. However, this did not result in a proportional increase in the overall money supply. This result is likely due largely to an undesirable lending environment: Banks likely found it more desirable to hold excess reserves in their accounts at the Fed, earning the IOR rate with zero risk, given that there were few attractive lending opportunities. That the liquidity injections did not result in a proportional increase in the money supply may also be due to banks’ increased demand to hold liquid reserves (as opposed to individually lending those excess reserves out) in the wake of the financial crisis.

So the truth is that when the subprime mortgage crisis blew-up in December, 2007 the Fed started SELLING hundreds of billions in treasuries to sterilize their credit facility that engaged in repo of MBS. Since this did not provide aggregate liquidity, this was not a lender of last resort function, this was a credit policy to support MBS. Then after Bear Stearns failed in March, 2008 the Fed sold more treasuries to make billions in direct loans to firms such as Bear (to aid in their purchase by JP Morgan) and AIG. At their peak, during the Lehman shock, their direct lending totaled well over $400 billion, or about half their balance sheet.

http://research.stlouisfed.org/fred2/graph/?g=16fS

http://research.stlouisfed.org/fred2/graph/?g=16fS

The damning truth is the Fed felt the urgent need to institute IOR because they were running low on treasuries but wanted to provide more liquidity. They were afraid to initially expand their balance sheet because in October, 2008 they were still concerned about inflation! Talk about missing the mark. They were concerned because the Fed Funds rate was below their target and they couldn’t control it. What they don’t seem to realize is that the Fed Funds is a barometer of liquidity. You don’t make the weather warmer by tricking your thermometer into not going below 70 degrees. I suspect it is the “Neo-Wicksellians” like Michael Woodford who took the money out of Wicksell who are to blame for this. This is a perfect example of Goodhart’s Law: “when a measure becomes a target, it ceases to be a good measure.” You can see in the chart below they tried, and failed, to create an interest rate channel by initially pegging the interest on excess reserves lower than the target rate. Eventually they gave up and harmonized all the rates at 25 bps. The effective Fed Funds remained below that because some institutions, such as the GSEs, have access to the Fed Funds market but not deposits at the Fed. This means there’s an arbitrage opportunity for banks to borrow on the Fed Funds market and deposit at the Fed. Since GSEs were nationalized, this might be considered another public subsidy. Either way, the primary dealer model and other differential treatment of institutions is broken.

http://research.stlouisfed.org/fred2/graph/?g=16fY

http://research.stlouisfed.org/fred2/graph/?g=16fY

We no longer have the initial conditions that justified interest on reserves. We are not above the ZLB and fearing inflation while wanting to increase the balance sheet. We are in the exact opposite. The Fed should normalize, including abandoning IOR. This is Bernanke’s legacy. The same man who promised, “We won’t do it again” got so caught up in the act of directing credit, experimenting with new tools and obeying his models that he forgot to listen to Bagehot’s advice or even professor Bernanke’s.

*Friedman, Milton. 1959. A Program for Monetary Stability.

Macroprudential policy tools: a primer (guest post by Justin Merrill)

In case you hadn’t heard, there’s a new fad in central banking called “macroprudential regulation.” During the Great Moderation there was a belief that low and stable inflation would be sufficient to stabilize financial markets and the economy. When the Great Moderation turned into the Great Recession, this paradigm shifted, but I’m afraid that the wrong conclusions are being drawn. In a series of posts, I shall explain what macroprudential policies are, who some popular people making the arguments for them are and what the risks of the policies are.

Most places I’ve read about macroprudential policies are vague in their description and only list a couple of the tools that central bankers/regulators can use. The policies are intended to prevent systemic risk by preventing/diffusing concentrations of risk. I hope to provide here a nearly comprehensive list of the tools. Conceptually, the tools can be categorized into four categories and theoretically all of the following risks may contribute to asset bubbles or financial instability:

- Leverage/Market Risk

- Reducing leverage is intended to reduce the risk of insolvency in case of a fall in asset prices.

- Liquidity

- Increasing liquidity reduces the risk that payments won’t be made to creditors and may curb fire-sales from credit crunches.

- Credit Quality

- Controlling credit quality intends to prevent future non-performing loans from debtors that would be most susceptible to economic shocks.

- FX/Capital Controls

- FX/Capital controls attempt to prevent hot money from pushing up asset prices and prevents firms from being over-exposed to FX risk from unhedged positions.

Also note that time-varying/dynamic/counter-cyclical rules are a popular concept and can be applied to possibly all of the following tools.

Leverage/Market Risk

- Debt/equity ratios: Also commonly referred to as “capital” in the banking sector. Requiring more funding from equity reduces the risk of insolvency.

- Margin requirements: Determines how much investment can be made with borrowed money. There is a high correlation between margin debt and asset prices.

- Provisioning: Banks account for loss provisions in their financial statements. If they expect losses or are required to hold higher provisions, they will hold a higher equity buffer to offset the losses. If actual losses are less than expected, the bank records a profit.

- Restrictions on profit distribution: If debt/equity ratios are above what regulators want, they may require the firm to retain earnings instead of pay dividends.

- Collateral, hypothecation and haircuts: Regulators may determine which assets may be used as collateral, how much collateral is required for lending, and how much of a haircut is applied to the asset in the repo market. If market prices fall below the repo price the seller may not buy it back. Haircuts (over-collateralization) and margin calls are used to mitigate this risk. Repos and reverse-repos are being increasingly used by central banks as a new tool for an exit strategy from QE and since QE has drained the private markets of credit-worthy assets. Repos also can have broader participation than open market operations (OMOs), the Fed Funds market or deposits at the central banks. OMOs are restricted to primary dealers and deposits at the Fed are restricted to members of the Federal Reserve System and membership is restricted to qualifying commercial banks.

- Too Big To Fail (TBTF) taxes: TBTF taxes have been proposed to reduce the concentration of risk or political power of a single firm as a sort of Pigouvian tax to offset externalities. The taxes could be an assessment on firms whose assets are above an arbitrary cutoff (such as $1 trillion), on firms whose assets exceed a percentage of GDP, or on firms that own above a certain percent of market share.

Liquidity

- Reserve requirements: Reserve requirements are a unique item on this list since they are considered a traditional monetary policy tool. Even though use of changing reserve requirements fell out of favor as a traditional tool, it has gained renewed interest in conjunction with QE, especially in countries with pegged currencies, such as China. This allows the central bank to increase the monetary base without creating price or asset inflation.

- Limits on maturity mismatch: Financial intermediaries such as banks generally engage in maturity transformation by borrowing short and lending long. This can create a funding risk if they are unable to roll over their debts at a reasonable rate. Also, the long dated assets they hold will have more convexity, which means they will be more sensitive to changes in interest rates.

- Liquidity Coverage Ratios (LCR): Basel regulations require financial institutions to hold a level of highly liquid assets to cover their net outflows over a period of time.

Credit Quality

- Caps on the loan-to-value (LTV) ratio: Requiring a larger down payment reduces the risk that the borrower will walk away in case of a decline in property value. It also helps the bank profitably resell the property in case of foreclosure.

- Caps on the debt-to-income (DTI) ratio: DTIs help gauge the borrower’s ability to repay the loan.

- Lending Policies- “No second homes” and risk weighting: Lending policies can target specific sectors of the economy or have specific goals. These can include requiring a larger down payment on second homes, increased risk weightings for real estate, discouraging foreign buyers, and discouraging house flipping by having higher taxes on short term sales.

FX/Capital Controls

- Caps on foreign currency lending: Foreign currency lending that is unhedged exposes the borrower to FX risk.

- Limits on net open currency positions/currency mismatch: Borrowing and investing in different currencies exposes FX risk.

- Capital controls: Capital controls are used to prevent hot money flows in and out of a country that could fuel a boom and bust. Controls are also used for financial repression and increasing domestic investment. Additionally, capital controls are often used in conjunction with a fixed exchange rate, like in China. This is due to the Trilemma. If China wants to peg its currency to the USD and control its domestic interest rate for monetary policy, it must have capital controls. Otherwise, the higher interest rate in China would attract hot money deposits from abroad and there would be an asset boom. The alternatives to a pegged currency with capital controls are a floating exchange rate with free capital or a currency board with free capital.

Links

http://www.imf.org/external/pubs/ft/fandd/basics/macropru.htm

Greenspan put, Draghi call? (guest post by Vaidas Urba)

(This is a monetary economics guest post by Vaidas Urba, a market monetarist from Lithuania. He has previously appeared at The Insecurity Analyst blog and TheMoneyIllusion. You can follow him on Twitter here)

Greenspan put, Bernanke put – everybody uses these expressions half-jokingly to describe monetary policy and asset prices. Ricardo Caballero and Emmanuel Farhi have proposed a very serious classification of policy tools, distinguishing between monetary puts and calls. According to Caballero and Farhi, policy puts support the economy in bad states of the world, while policy calls support the economy in good states of world. There is much to disagree with in their “Safety Traps and Economic Policy” paper, but their definition of policy puts and calls is very useful.

QE1 and ARRA stimulus in 2009 are examples of policy puts. On the other hand, QE3 and Evans rule are primarily policy calls. Evans rule supported expectations of low interest rates in good states of the world, while QE3 compressed the term premium by reducing the risk of bond market volatility during the recovery. Policy calls are riskier than policy puts. Evan’s rule increased the risk of suboptimally low interest rates during late stages of recovery, while QE3 increased the risk of losses in Fed’s portfolio. Indeed, on March 1, 2013 Bernanke indicated that the estimated treasury term premium is negative. The Fed has walked back from policy calls. Tapering has restored the bond term premium to more normal levels, and the Fed has replaced the Evans rule with a more vague guidance. Bernanke call was replaced by Yellen put.

The Fed has used both monetary puts and calls, but the ECB has never used policy calls, and is not planning to use them. The policy of the ECB was a succession of impressive policy puts. Temporary liquidity injection in August 2007 has addressed the liquidity panic. Full allotment in October 2008 has placed a floor on the functioning of euro and dollar money markets. Three year LTROs in 2011 have prevented Greece’s default from becoming Lehman II. OMTs are out-of the money policy puts – they were never activated. Forward guidance is a policy put too, the ECB describes it as being all about “subdued outlook for inflation and broad-based weakness of the economy”, and low rates are signalled in bad states of the world without affecting interest rate expectations in good states of the world.

On further weakness the ECB is likely to start QE. Executive Board member Benoit Coeure has recently given us a glimpse of likely modalities of QE in his “Asset purchases as an instrument of monetary policy” speech. Coeure has stressed the continuity of ECB’s approach, he also said that “asset purchases in the euro area would not be about quantity, but about price”, and the ECB will use the yardstick of “the observable effect of our operations on term premia”. Presumably, the intent of QE will be to reduce term premia that are unduly high (policy put), and not to recreate boom conditions in financial markets by driving term premia to excessively low levels (policy call).

The Eurozone economy is very far away from any sensible macro equilibrium, and monetary call would be a very sensible step to take. Unfortunately, a blocking minority exists for any explicit decision. However, Draghi could communicate an implicit policy call by signalling the existence of majority coalition which would block a premature interest rate increase. The rate hike of 2011 was unanimous, so the bar is high for any such communication. Draghi’s talk of “plenty of slack” is a step to the right direction, but stronger and clearer words are needed to persuade the markets that ECB’s reaction function has changed unrecognizably since 2011.

Endogenous Money vs. the Money Multiplier (guest post by Justin Merrill)

(This is a guest post by Justin Merrill, an investment advisor in Fairfax, Virginia, who independently studies banking, free banking and monetary theory. He is also a media editor at freebanking.org and you can find some of its work here and here)

The proponents of the “New View”, especially Tobin and Gurley and Shaw, have been a large influence on me, but so has Leland Yeager. This discussion prompted me to reread Yeager’s work, “What are Banks?” and see if their views could be reconciled.

I believe the following to be true:

- Outside money is exogenous with a couple (Post-Keynesian) qualifications and also a “hot potato”.

- Inside money is endogenously created and subject to market forces.

- The reserve multiplier explanation should die a quick, painful death.

- Monetary policy does influence inside money creation through controlling expectations and liquidity, which affects banks’ cost of funds.

- Attempts to regulate inside money creation for “macro-prudential” purposes are folly because the problem is monetary policy. The only way to keep both money and credit harmonized is by allowing a natural rate of interest.

Framing the Discussion:

To be clear, what is being debated is the usefulness of the money multiplier model (MMM) and the endogeneity of money and how these are related. Someone (I think it was Julien) recently blogged that the pro-endo critics of the MMM are contradicting themselves because the model explicitly states that commercial banks create the majority of money. But this is not what the debate is. The debate is what limits the creation of money (reserve requirements or market forces) and if the textbook MMM is remotely accurate or even useful.

James Tobin and the “New View”:

I mostly agree with the new view. I believe that inside money is determined mostly by market forces and that banks compete with other financial intermediaries. They provide liquidity by optimally allocating society’s wealth between deposits and risk assets.

Where I disagree with the New View is when they go so far as to say that banks are pure intermediaries and not in anyway special. This overlooks the other functions of banks and also leads one to ask why banks exist at all when we could all just hold diversified financial assets with lower fees/higher yields? While these financial assets compete with bank deposits, they are not perfect substitutes. Banks’ liabilities are special and so are some other functions they provide.

Leland Yeager’s Monetarist view:

In Yeager’s essay, “What are Banks?”, he explicitly says that the broad money supply is exogenously controlled by the monetary authority. He argues that fluctuations in money demand don’t impact money supply, only the price level and nominal income.

Yeager thinks the old view, that reserves multiplied by reserve ratios determine the broad money supply, is correct. His most convincing argument is that banks will invest any excess reserves in marketable securities. One flaw in this particular argument is that the return on excess reserves isn’t just the opportunity cost of marketable securities, but also of lending to other banks, which is a usually higher rate than T-bills. One notable difference is that lending Federal Funds is an unsecured market while T-bills are “riskless” and this risk difference might explain some of the spread. The more recent innovation of interest on reserves also complicates the MMM explanation and has partially caused the Fed Funds market to dry up since implementation. If interbank lending rates or IOR are higher than the return of near perfect substitutes (marketable securities such as T-bills), the reserves will stay in the system.

Some Problems with the Money Multiplier Model:

The reason I want to see the MMM die a fast, painful death is because it abstracts away from real decisions of individuals involved in the market process and turns the entire banking system into a policy lever for bureaucrats to adjust.

One way we could attempt to settle the validity of the MMM is empirically. We could survey bank treasurers and ask them what their bottlenecks are, such as: costs of funding, lending opportunities, or reserve maintenance. In the US, banks report their regulatory reserve status every two weeks and have to maintain reserve requirements over the average of the period. This means that if a firm sees an outflow of reserves in week one, in week two they must retain a surplus to offset last week’s deficit.

We could also use macro data to try to verify if reserve requirements determine the money supply and if the banking system remains fully loaned up. I would rather challenge it with the following proposition: imagine a truly free banking system with no central bank and no special regulations. The outside money could be a commodity but that is irrelevant to my point. The point is that with no regulator to enforce reserve requirements, what determines the inside money supply? Some might answer that individual banks would determine their own reserve ratio and that would in aggregate set the money supply, but this begs the question because it doesn’t explain what the prudent bank treasurer is thinking when deciding on a ratio or even if they are thinking in terms of reserve ratios at all!

I suspect that the prudent bank treasurer is only tangentially thinking about reserve ratios in regards to net redemptions and that what they are really thinking about is maximizing profits. If they can make a loan at a risk adjusted rate that is higher than what they can borrow on the wholesale market, why wouldn’t they make a loan and borrow reserves? This kind of interbank lending usually has higher costs than interest paid on deposits so it is not the ideal source of funding, but if the marginal investment return is high enough, the treasurer will authorize the loan and borrow reserves until they can secure more “sticky” and affordable funding. One thing I noticed is that both sides of the debate, Tobin and Yeager, accuse the other side of assuming that banks are not profit maximizers. I suspect it is Yeager who is guilty because the New View actually incorporates marginal profit/loss into its analysis.

Checking accounts aren’t that interesting, or interest bearing. The textbook version explains that reserves create bank deposits without any specification between demand and time deposits. When Tobin was writing, both were subject to reserve requirements, if I’m not mistaken. Interest on checking accounts was also forbidden. My interpretation of Tobin’s point is that bank deposits compete with other financial assets, and should they be allowed to pay interest, will do so. Time deposits are a better characterization of Tobin’s point because they are held for their certainty and return, whereas demand deposits are for transactions.The MMM is still taught like it is the 1960’s even though we have financial liberalization and innovation. No longer do time deposits have interest ceilings, MMMFs are checkable, NOW accounts enable demand deposits to pay interest (and I think Dodd-Frank scrapped all prohibitions of interest on demand deposits), and maybe most importantly, time deposits are not subject to reserve requirements. So how do MMM proponents explain the supply and yield of time deposits, especially if savings accounts are still counted as money? This leads into a paradox that can only be countered with either a concession that the Fed doesn’t control M2, or only M1 is money, or maybe that the MMM should be abandoned.

A Final Note on Institutional Analysis:

Regulatory reserve requirements are an intervention, to be specific, a quota. Interventions only take effect if they are binding. The reason the MMM is insufficient is because it is a specific theory of money creation, not a general theory. Relying on the MMM is as naive as relying on minimum wage laws to explain labor market wages for unskilled labor. Some might argue that binding reserve requirements are required to create artificial scarcity and give a fiat currency a positive value, but I’m sufficiently convinced by Eugene Fama’s “Banking in the Theory of Finance” that the services rendered from money are sufficient to give it positive value so long as the issuer constrains the supply. I also believe that monetary policy can be effective (or destructive) absent reserve requirements. One final argument for reserve requirements is that someone needs to make the banks stay liquid enough to pay off depositors. This justification was codified at the national level under the National Banking Act of 1863 and was made obsolete with the creation of the Federal Reserve System. The central bank can offset a reserve drain and be the lender of last resort. Empirically, reserve requirements were an ineffective tool for regulating liquidity and theoretically may even contribute to panics, but that’s worthy of a different post altogether. I also plan on writing a more detailed post explaining the mechanics behind the reasoning that inside money is not a “hot potato”.

Recent Comments