Pushing market rationality too far

In a new post on Switzerland, Scott Sumner said (my emphasis):

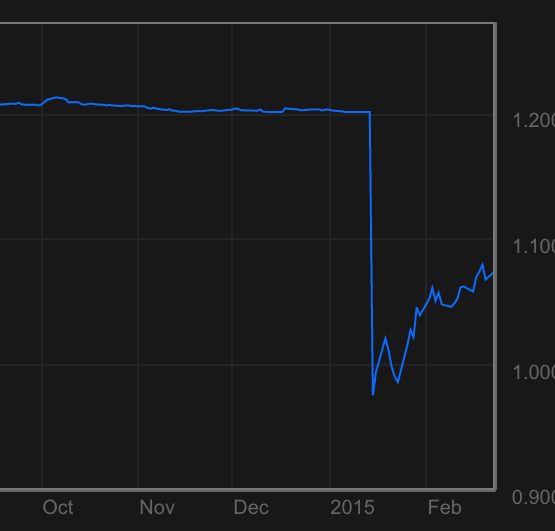

The following graph shows that the SF has fallen from rough parity with the euro after the de-pegging, to about 1.08 SF to the euro today:

And this graph shows that the Swiss stock market, which crashed on the decision that some claimed was “inevitable” (hint, markets NEVER crash on news that is inevitable), has regained most of its losses.

I often enjoy what Scott Sumner writes, but this comment is from someone who doesn’t understand, or has no experience in, financial markets. We all know that Sumner strongly believes in rational expectations and the EMH. But this is pushing market efficiency and rationality too far.

According to Sumner, “markets never crash on news that is inevitable”. Really? Is he saying that markets believed the Euro peg would remain in place forever (which is the only necessary condition for the de-pegging not being ‘inevitable’)?

In reality many investors, if not most (though it can’t be said with certainty), were aware that the peg would be removed and of the resulting potential consequences for Swiss companies. So why the crash?

While investors surely knew that the peg wouldn’t last, they didn’t know when it would end. They were acting on incomplete information. However, this is perhaps what Sumner implies: the Swiss central bank should have provided markets with a more precise statement of when, and in what conditions, the peg would end. Markets would have revised their expectations and priced in the information. This reasoning underpins the rationale for monetary policy rules and forward guidance. But in practice, providing ‘guidance’ isn’t easy: central bankers are not omniscient, have imperfect access to information and cannot accurately forecast the future in an ever-changing world. See what happened to the BoE’s forward guidance policy, which ended up not being much guidance at all as central bankers changed their minds as the economic situation in the UK evolved*.

But the rational expectations argument itself can be used to describe many different situations. If investors believe the peg will end at some point, but don’t know exactly when, it is arguably as ‘rational’ for them to try to maximise gains as long as they could and to try to exit the market just before it crashes, as it is ‘rational’ to adapt their positions to minimise their risk exposure. When the market finally does crash, it often overshoots, for the same reason: benefiting from a short-term situation to maximise profits.

Taking advantage of monetary policy is what traders do. It is their job. Of course, many will fail in their attempt. But necessarily identifying rational expectations with strong short-term risk-aversion and immediate inclusion of external information into prices is abusive.

This latest Bloomberg article shows that close to 20% of traders expect the Fed to raise rates in June, and consequently have surely put in place trading strategies around this belief, and are likely to react negatively if their expectations aren’t fulfilled. However, who doubts that a rate rise is ‘inevitable’? This demonstrates the price-distorting ability of central banks. In order to limit extreme price fluctuations and crashes, the better central banks can do is to disappear from the marketplace entirely.

*Other practical restrictions on guidance include the fact that, while professional investors are likely to be aware of their significance, the rest of the population has no idea what the hell you’re talking about, if it has even heard of it. As a result, the efforts the BoE made to reassure UK borrowers that rates would not rise in the short-run seemed pointless, as virtually no average Joe got it, implying that most people didn’t change their borrowing behaviour/plan in consequence.

I have made a case for rule-based policies a while ago, which I do believe would limit distortions to an extent.

Are ETFs making markets less efficient?

I don’t have an answer to that question. But I have been wondering for a little while.

Noah Smith, on Bloomberg, and John Authers, in the FT, are pointing out that passive funds keep witnessing inflows at the expense of actively managed funds (which still represent the large majority of assets under management). Smith adds that academic research overwhelmingly demonstrates that active fund management (whether hedge funds or more traditional, and cheaper, mutual funds) is a ‘waste’ of money.

Market efficiency requires that many different individuals make their own investment assessment and decisions, in accordance with their limited means, knowledge and preferences. Some will gain, some will lose, market prices will continuously fluctuate one way or another in a permanent state of disequilibrium that reflects investors’ evolving views of what constitutes an efficient allocation of resources. In turn market price movements in themselves lead investors to reassess their opinions, bringing about further fluctuations but eventually producing something that resemble a near-equilibrium market, which almost accurately reflects investors’ preferences… for a few instants… after which other investors’ reactions are triggered. This is confusing; this is perpetual discovery and adaptation; this is the market process*.

Hence the importance of prices. And in particular, of relative prices. Investors can pick investments among a very wide range of securities. Such market granularity eases the market process: when one particular security looks underpriced relative to its peers, investors might start buying (until its price has gone up).

ETFs, index funds, on the other hand, allow investors to buy the whole market, or a large part of it, or a whole sector. They merely replicate market movements. As such, granularity, relative prices, and intra-market fluctuations disappear. Consequently, if everyone starts buying the whole market, there is no room left to pick winners within the market. Efficient firms and investments benefit as much from the inflow of capital as bad ones. Once a majority of investors start buying the whole market through index funds, stock pickers will have very limited choice to pick winners. Resources allocation, and in the end economic efficiency, becomes impaired**.

All this remains very theoretical. I haven’t been able to find any theoretical or empirical paper that researched this particular topic (please let me know if you know any). 2013 Nobel-winner Eugene Fama recently dismissed those concerns:

There’s this fallacy that you need active managers to make the market efficient. That’s true to some extent, but you need informed active managers to make it more efficient. Bad active managers make it less efficient.

Basically, he hasn’t answered the question. According to him, no, ETFs don’t make markets less efficient, but yes that’s true to an extent but no if you have bad active managers. Not that helpful to say the least. He is the father of the efficient market hypothesis so probably a little biased to start with.

Smith has another answer: he believes that asset-class picking could become the new stock-picking and that active management could shift from relative intra-market prices to relative inter-market prices. Basically, investors would take positions on, let’s say, the German stock market vs. the British one, instead of picking companies or securities within each of those markets. This is a possibility, albeit one that doesn’t really solve the economic resources allocation efficiency problem described above. Investors also don’t always have the option to invest outside of their domestic market, for contractual or FX fluctuation reasons.

It is likely that stock picking won’t disappear. Investors will always want to buy promising or sell disappointing individual securities. Still, the rise of index investing could have some interesting (and possibly far-reaching) implications for the market process and resource allocations. It is, as yet, unclear what form these implications may take.

* This ‘market efficiency’ definition is very close to the one defined by Austrian school scholars (which I prefer), as opposed to the more common market efficiency as defined under the equilibrium neo/new classical and Keynesian frameworks. See summaries here, as well as a more detailed description of the New classical efficient market hypothesis here.

** A real life comparison would be: instead of purchasing one TV, after carefully weighing the pros and cons of each option out there, everyone starts buying all possible models from all manufacturers, independently of their respective qualities. The company offering the worst product would benefit as much as the one offering the best product. Needless to say, this isn’t the best way of maximising economic resources.

New research on finance and Austrian capital theories

Two brand new pieces of academic research have been published last month, directly or indirectly related to the Austrian theory of the business cycle (some readers might already know my RWA-based ABCT: here, here, here and here).

The first one, called Roundaboutness is Not a Mysterious Concept: A Financial Application to Capital Theory (Cachanosky and Lewin) attempts to start merging ABCT (or rather, Austrian capital theory) with corporate finance theory. The authors use the finance concepts of economic value added (EVA), modified duration, Macaulay duration and convexity in order to represent the Austrian concepts of ‘roundaboutness’ and ‘average period of production’. The paper provides a welcome and well-defined corporate finance background to the ABCT.

However, finance practitioners still don’t have the option to use a ‘full-Austrian’ alternative financial framework, as this paper still relies on some mainstream concepts. For instance, the EVA calculation for a given period t is as follows:

where ROIC is the return on invested capital, WACC the weighted average cost of capital and K the financial capital invested.

In order to compute the project’s market value added (MVA, i.e. whether or not the project has added value), it is then necessary to discount the expected future EVAs of each period t1, t2…, T, by the WACC of the project:

The WACC represents the minimum return demanded by investors to compensate for the risk of such a project (i.e. the opportunity cost), and is dependent on the interest rate level. The problem arises in the way it is calculated in modern mainstream finance. While the cost of debt capital is relatively straightforward to extract, the cost of equity capital is commonly computed using the capital asset pricing model (CAPM). Unfortunately, the CAPM is based on the Modern Portfolio Theory, itself based on new-classical economics and rational expectations/efficient market hypothesis premises, which are at odds with Austrian approaches.

(And I am not even mentioning some of the very dubious assumptions of the theory, such as “all investors can lend and borrow unlimited amounts at the risk-free rate of interest”…)

While it is easy for researchers to define a cost of equity for a theoretical paper, practitioners do need a method to estimate it from real life data. This is how the CAPM comes in handy, whereas the Austrian approach still has no real alternative to suggest (as far as I know).

Nevertheless, putting the cost of equity problem aside, the authors view the MVA as perfectly adapted to capital theory:

Note that the MVA representation captures the desired characteristics of capital-theory; (1) it is forward looking, (2) it focuses on the length of the EVA cash-flow, and (3) it captures the notion of capital-intensity.

Using the corporate finance framework outlined above, the authors easily show that the more capital intensive investments are the more they are sensitive to variations in interest rates (i.e. they have a larger ‘convexity’). They also show that more ‘roundabout’/longer projects benefit proportionally more from a decline in interest rates than shorter projects. Unsurprisingly, those projects are also the first ones to suffer when interest rates start going up.

The following chart demonstrates the trajectory of the MVA of both long time horizon (high roundabout – HR) and short time horizon (low roundabout – LR) projects as a function of WACC.

Overall, this is a very interesting paper that contains a lot more than what I just described. I wish more research was undertaken on that topic though.

The second paper, pointed by Tyler Cowen, while not directly related to the ABCT, nonetheless has several links to it (I am unsure why Cowen thinks this piece of research actually reflects the ABCT). What’s interesting in this paper is that it seems to confirm the link between credit expansion, financial instability and banks stock prices, as well as the ‘irrationality’ of bank shareholders, who do not demand a higher equity premium when credit expansion occurs (which doesn’t seem to fit the rational expectations framework very well…).

Nobel Prize in Economics

Today Eugene Fama, Lars Peter Hansen and Robert Shiller share the 2013 The Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel.

While I do not share some of their beliefs (Fama’s efficient market hypothesis based on rational expectations or Shiller’s irrational exuberance are a few examples), I can only but welcome the award of the prize to pro-free markets academics.

Congratulations!

{kind=link}

Recent Comments