China as a spontaneous finance Frankenstein

China is an interesting case. Underneath its very tight government-controlled financial repression hide numerous financial experiments aimed at bypassing those very controls. The Chinese shadow banking system is now a well-known financial Frankenstein, with multiple asset management companies, wealth management products and other off-balance sheet entities providing around half the country’s credit volume. The more the government tries to regulate the system, the more financial innovation finds new workarounds and become increasingly more opaque.

Bitcoin is following this typical mechanism. China was one of the world’s most successful Bitcoin markets as local retailers and customers attempted to avoid government control and manipulation. In short, Chinese users liked that Bitcoin had fixed rules that could not be twisted by some corrupted officials. Bitcoin allowed them to transfer currency internationally almost without restriction. Its Chinese supporters felt free. Indeed, freedom and facilitation of transaction and saving is what drives most spontaneous financial innovations. Nonetheless, the love story couldn’t last as I have already described and the government launched a crackdown on Bitcoin in December.

Nonetheless, Bitcoin is coming back, the Frankenstein way. The FT reported today that local Chinese Bitcoin exchanges are now finding ways around new government rules. Surprising? It shouldn’t be. Governments around the world, a simple message: don’t underestimate your citizens. You’ll always run after them. Never ahead.

The issue is now that all those rules are pushing Bitcoin and other innovations even more into the shadows, making the whole system even more opaque and hard to analyse. For instance, while Chinese banks are now forbidden to clear Bitcoin transactions, a local platform route the money through its founder’s account. Some others have started to use voucher systems, essentially transferable claims on RMB accounts for people who want to buy and sell Bitcoins. Those vouchers effectively become claims on claims on money, or some sort of money substitutes redeemable on money substitutes (bitcoins) redeemable on money (USD)…

I personally don’t really welcome such evolutions. Government should stay away and not add further systemic risks to innovations already trying to figure out what their own limits are. As I recently said, learning is intrinsic to any system and should not be suppressed.

Blame the rich for the next asset bubble. Or not.

First of all, happy new year to all of you! Fingers crossed we don’t witness another market crash this year! 🙂

Indeed, credit markets are hot. Equity markets are also hot. The FT published an article yesterday with some striking facts about the ‘improvements’ in credit markets over the past couple of years. Some would say that it’s encouraging. I am not convinced…

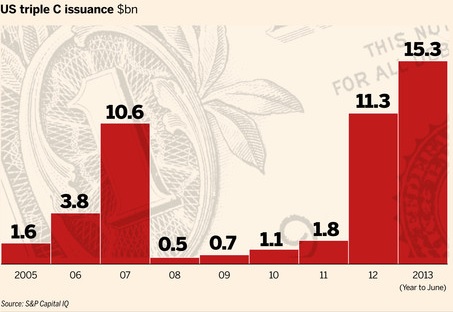

Most credit indicators are close to or above their pre-credit crisis high. Sales of leveraged loans and high-yield bonds are above their pre-crisis peak. The average leverage level of US LBOs is back to 2006 level. Issuance of collateralised loan obligations is close to its pre-crisis peak. Even CCC-rated junk bonds are way above their previous peak. I’ve already mentioned some of those facts a few months ago.

In a relatively recent presentation, Citi’s strategist Hans Lorenzen confirmed the trend: central banks are indirectly suppressing most risky investments’ risk premia. Most investors expect junk bonds’ spreads to tighten further or at least to stabilise at those narrow levels and emerging markets bonds and equities, as well as junk bonds are now among investors’ top asset classes .

My ‘theory’ at the time was that (see also here), if investors were piling in increasingly riskier asset classes, bringing their yield down to record low levels in the process, and nonetheless accepting this level of risk for such low returns, it was because current central bank-defined nominal interest rates were below the Wicksellian natural rate of interest. Inflation, as felt by investors rather than the one reported by national statistics agencies, was higher than most real rates of return on relatively safe assets. In order to see their capital growing (or at least to prevent it from declining), they were forced to pick riskier assets, such as high-yield bonds, which were not really high-yield anymore as a result but remained junk nonetheless. This would result in capital misallocation as, under ‘natural’ interest rate conditions, those investments would have never taken place. Thomas Aubrey’s Wicksellian differential, an indicator of the likely gap between the nominal and the natural rates of interest, was, in line with credit markets, reaching its pre-crisis high and seemed to confirm that ‘theory’.

Well, I now think that not all investors are responsible for what we are witnessing today. The (very) rich are.

This came to my mind some time ago while reading that FT piece by John Authers. This was revealing.

“Their wealth gives them scope to try imaginative investments, but they are terrified of inflation, even as deflation is emerging as a greater risk. That is in part because inflation for the goods and services bought by the very rich is running about 2 percentage points faster than retail inflation as a whole in the UK.” (my emphasis)

In the UK, real gilts’ yields were already in negative territory: adjusted by the (potentially underestimated) consumer price index, gilts were yielding around -1% early 2013. Savers were effectively losing money by investing in those bonds. Now think about the rich: by investing in such bonds, they would get a real return of around -3% instead.

Moreover, “71 per cent of respondents said they were more worried now about a steep rise in inflation than they were five years ago.”

Does it start to make sense? The cost of living I was mentioning earlier is increasing particularly quickly for the rich. And… they are the ones who own most financial assets. In order to offset those rising living costs, they naturally look for higher-yielding investments. And it is exactly what the FT reports:

“Their favourite asset classes for the next three decades are emerging markets equities, developed equities and agricultural land, in that order. Private equity comes close after farmland, while art and collectables were also a more popular asset class than any kind of bonds. […]

Hedge funds, as a group, have not fared well since the crisis. But wealthy investors preoccupied by inflation, and robbed of the easy option of bonds, are evidently disposed to give them a try, with an average projected allocation for the next three decades of 25 per cent. Meanwhile, the chance of a bubble in agricultural land prices, or in art, looks very real.”

Are the rich responsible for our current frothy markets then? Obviously not. They are acting rationally in response to central banks’ policies. Nonetheless, this raises an interesting question. Mainstream economics only considers a high aggregate inflation rate as dangerous. What about ‘class warfare’-type inflation? It does look like inflation experienced by one socioeconomic class could inadvertently lead to asset bubbles and bursts, despite aggregate inflation remaining subdued. This may be another destabilising effect of monetary injections on relative prices.

Granted, central banks possibly are on a Keynesian’s ‘euthanasia of the rentier’-type scheme in order to try to alleviate the pain of over-indebted borrowers (and/or to encourage further lending). But financial repression avoidance might well end-up coming back with a vengeance if savers’ reactions, and in particular, rich savers’, make financial markets bubble and crash.

Charts: FT (link above), Citi and Societé Générale

On the importance of failure in free-market banking systems

An article from Gillian Tett in the FT earlier this week reminded me of the importance of experimenting short-term failures for free markets to succeed in the long-term. This is a key principle of a self-sufficient and self-correcting system that has unfortunately been forgotten with the rise of the paternalist state.

This is what Larry White referred to with the expression ‘antifragile banking and monetary system’, based on Nassim Taleb’s antifragile concept. In her article, Tett mentions how actors in financial markets, as well as central bankers, have changed their views following the crisis. The vocabulary she used is misleading. Facts have not changed. Facts have always remained the same. Economic agents simply didn’t know how to interpret those facts. We call that learning.

As Larry White says, “the banking system is not inherently fragile” and “a more thorough look at theory and empirical evidence indicates clearly that banking is not naturally fragile.” (his emphasis)

He then adds:

The view of banking institutions as naturally fragile is implausibly anti-Darwinian. It defies the Darwinian principle of natural selection (“the survival of the fittest”). Given a few centuries, financial institutions that are inherently prone to collapse should be expected to collapse and thereby to disappear over time, while sturdier structures should be expected to survive. The inherent-fragility view of banking cannot explain how modern banking survived, much less how it flourished and spread across the world, as it did for the seven-plus centuries between its emergence around 1200 (Lopez 1979: 12) and the arrival of official safety nets after 1900 in the form of government-sponsored lenders of last resort and national deposit insurance.

While single institutions are indeed prone to failure, the whole financial system is not inherently weak but is made weaker by restrictive/intrusive/limiting institutional frameworks. Paternalist frameworks attempt to forbid banks to engage is what regulators view as ‘risky’ activities. The consequence of this being to prevent the system from learning from its mistakes and reinforcing itself.

Crashes following financial liberalisations are often used as evidence of the impossibility of the banking system to self-regulate by proponents of a tight control of the financial sector by the state. Those critics are misplaced. Crashes following financial liberalisation are normal. Like children discovering some risky new games, financial actors haven’t yet found out the inherent risks associated to their new activities. The system crashes and it learns.

However, crashes need not be that painful. State intervention (or ‘protection’) postpones the learning process. Meanwhile, innovations accumulate in order to bypass some of the state’s introduced artificial limitations. When the system is finally ‘released’, multiple live experiments, some really spontaneously emerging from the natural evolution of the system, some others pure products of regulation avoidance, are launched simultaneously, with potentially disastrous consequences when many of them crash at the same time.

But free markets are not to blame in such circumstances. The system followed its natural Darwinian selection rules and should the state not have restricted financial activities in the first place, the process would have been smoother and spread out over a longer period of time. Historically, the freest banking systems were also the most robust ones (comparing the US and Canadian banking systems at the end of the 19th and early 20th century quickly confirms that).

This mechanism inevitably played a role in some of the previous financial crises, from the S&L crisis of the 1980s to the recent 2008 crash. China seems to have taken a cautious view and aims only at liberalising its banking system step by step. This sounds sensible.

Learning from experience is crucial in all aspects of life. By preventing the system from learning through various regulations, protection schemes, deposit insurances and other paternalist interventions, the state and regulators prevent whole generations of bankers (as well as the overall population) from discovering what they should and should not do. This is dangerous. Short-term mild pain is often a necessary evil that promotes long-term robustness. We call that wisdom.

Spontaneous Finance wishes you a Merry Christmas!

Merry Christmas and best wishes to all my readers!

Let’s watch again John Papola’s last year brilliant economics video:

PS: John, we’re gonna have a problem with Santa pretty soon… Time for an update!

“It was approved by regulators”

If ever you needed a single sentence to symbolically prove that today’s financial markets aren’t free, there you go.

You can’t possibly imagine the countless times I’ve heard this, both as part of my various jobs* or in the financial press. The process is pretty much always the following:

- Banking executives privately or publicly denounce regulators as incompetent and/or not understanding much about actual banking practice

- Investors/shareholders/journalists/analysts/other bankers question those executives about a recent, often suspect, change in their internal methodology that allows them to book higher profits/ROE

- Banking executives seriously justify their decision with: “It was approved by regulators”

Let’s clarify something: not all bankers are critical of regulators, and not all bankers are so inconsistent either. Most bankers thrive to do their job correctly and honestly, and believe that their decisions are appropriate and for the long-term benefit of both clients and shareholders.

Nonetheless, regulators have become some bankers’ strongest ally and the easiest justification to bypass market discipline. When shareholders are worried about a new, apparently risky, change in internal models, underwriting criteria or anything else, bankers don’t have to look very far to find a good excuse anymore. Regulators inadvertently become bankers’ best friends.

A typical illustration of that story occurred about a year ago, when Morgan Stanley changed its internal Value-at-Risk-based market risk model, which all of a sudden made its trading book look less risky than it would have been under the previous version of that same model. Many finance professionals and investors were critical of the move. How did Morgan Stanley’s CFO dismiss analysts’ questions?

It’s been approved by regulators.

While she may have been honestly thinking that the new model was better or more appropriate, the use of this argument is unfortunate. This is now the best – and the worst – defence bankers have against crucial free markets’ scrutiny.

*no, no names again, and none of my previous or current firms

European banking resolution non-mechanism

The Financial Times and Zero Hedge had a pretty funny chart today describing the new mechanism to ‘resolve’ a failing bank, agreed yesterday by European ministers:

Zero Hedge calls this the “MinotEur Labyrinth”. As they say, good luck to them.

PS: I might talk about it in more details a later, when I have more time…

The problems with the MMT-derived banking theory

(Update: Following Scott Fullwiler’s comment, I published an update here, in which I provide extra clarifications and introduce what I see as the fallacy of composition of the endogenous money theory (I moved this update to the top of my post following a few questions I received).)

Today will be a little long and technical… Many people have heard of the classic textbook story of the banking money multiplier, a characteristic of fractional reserve banking systems. Banks obtain reserves (i.e. central bank-issued high-powered money – HPM, which forms the monetary base) as customers deposit their money in, then lend out a fraction of those deposits that gets redeposited at another bank, effectively creating money in the process, and so on. In fine, reserve requirements at central banks prevent banks from expanding lending (and hence money supply) beyond a certain point. This led to the view that banks’ expansion is reserve-constrained.

But proponents of Modern Monetary Theory (MMT), and others who have no idea what MMT is, but who have been convinced by the argument, have been shouting out for a while now that this view is wrong. Banks do not lend out reserves they assert. Banks aren’t reserve-constrained but capital-constrained. Therefore, lending is endogenous, the supply of bank loans is almost perfectly elastic and the quantity supplied only driven by demand. Scott Fullwiler described the process on Warren Mosler’s (aka current MMT Guru) website. Cullen Roche has also been a strong proponent of this view (see here and here for example).

I managed to find a relatively good detailed summary of this view here:

[…] we had discussed the orthodox belief that the government controls the money supply through control over bank reserves. This position is rejected by Post Keynesians, who argue that banks expand the money supply endogenously. How is this possible in nations with a legally required reserve ratio? Banks, like other firms, take positions in assets by issuing liabilities on the expectation of making profits. Much bank activity can be analyzed as a “leveraging” of HPM–because banks issue liabilities that can be exchanged on demand for HPM on the expectation that they can obtain HPM as necessary to meet withdrawals–but many other firms engage in similar activity. For our purposes, however, the main difference between banks and other types of firms involves the nature of the liabilities. Banks “make loans” by purchasing IOUs of “borrowers”; this results in a bank liability–usually a demand deposit, at least initially–that shows up as an asset (“money”) of the borrower. Thus, the “creditors” of a bank are created simultaneously with the “debtors” to the bank. The creditors will almost immediately exercise their right to use the created demand deposit as a medium of exchange.

Indeed, bank liabilities are the primary “money” used by non-banks. The government accepts some bank liabilities in payment of taxes, and it guarantees that many bank liabilities are redeemable at par against HPM. In turn, reserves are the “money” used as means of payment (or inter-bank settlement) among banks and for payments made to the central bank; as bank “creditors” draw down demand deposits, this causes a clearing drain for the individual bank. The bank may then operate either on its asset side (selling an asset) or on its liability side (borrowing reserves) to cover the loss of reserves. In the aggregate, however, such activities only shift reserves from bank-to-bank. Aggregate excesses or deficiencies of reserves have to be rectified by the central bank. Ultimately, then, reserves are not discretionary in the short run; the central bank can determine the price of reserves–admittedly, within some constraints–but then must provide reserves more-or-less on demand to hit its “price” target (the fed funds rate in the US, or the bank rate in the UK). This is because excess or deficient reserves would cause the fed funds rate (or bank rate) to move away from the target immediately.

This means that central banks cannot control the money supply.

I am going to argue here that this view is at best inexact. And that, if the textbook description is outdated, it is still mostly right.

Scott Sumner argued on his blog that lending was effectively endogenous in the short-run but not in the long-run. I only partially agree, as even in the short-run in-built markets limits are in place.

Banks raise funding to obtain reserves

My arguments come both from my theoretical knowledge and from my practical experience of analysing banks all day long and meeting banks’ management, including treasurers/ALM managers. On a side note, the MMT story is wrong in a commodity-backed currency environment. But its proponents reply that it is only valid in our modern fiat money-based banking systems. Fair enough.

The reality is… banks do obtain funding (hence reserves) before lending in most cases. The opposite would be suicidal. Equity funding is obvious: a bank issues equity liabilities in exchange for cash that it then invests/lends. Non-equity funding, by far the largest component of banks’ funding structure (around 95% of funding), mainly comes from two sources: customer deposits and wholesale funding. Banks primarily rely on deposits to fund their lending activities. They try to attract depositors as they provide banks with more funds to lend. Of course they don’t lend out the deposits but the increase in reserves that comes along an increase in deposits allows the bank to lend more without risking a depletion of its reserve base.

Banks at the same time try to minimise the interest rate they pay on deposits in order to minimise their funding costs and maximise their net interest margin (basically the margin between the rate at which banks lend and the rate at which they borrow from depositors and other creditors). They also try to attract sticky saving and term deposits, rather than more volatile (but cheaper) demand deposits.

When banks want to lend more than what their deposit base allows them to lend, they need to turn to wholesale funding. Wholesale funding roughly comprises senior and subordinated liabilities (bonds) issued on the markets as well as interbank borrowings and repurchase agreements. Bond issues are quite simple: the bank issues its liabilities on the financial markets in exchange for cash. Cash that will then complement its existing cash reserves, and that the bank consequently lends out at a margin (unless of course the purpose of the issue was to refinance existing bonds). Interbank borrowings and repos are usually minimally used by banks as a source of funding, as they are very often short-term and unstable (i.e. can be withdrawn by other banks or not rolled over). Interbank funding (and borrowing from central banks) is the cheapest source of funds (although continuously rolling over this type of funding makes it expensive in the end). Deposits and other wholesale issues are more expensive.

What do banks do with the cash/reserves/HPM that they acquire through their various funding sources? Well, as you guessed, they lend. But not only. Banks invest. In order to maintain an adequately liquid balance sheet at all times to face withdrawals and settlements, banks mostly 1. keep some cash in hands and at the central bank, which represents their official reserves (as specified by reserve requirements), 2. invest the remaining of their cash in liquid securities, often sovereign bonds or highly-rated firms’ debt securities, which represent their ‘secondary reserves’, and 3. place some cash at other banks (interbank lending mainly).

In the end, all banks hold a liquidity buffer that represents between around 10% and 25% of their assets (and between 10 and 40% of their deposit base), under the form of both primary and secondary reserves. Why not keeping all as cash? Because of the opportunity cost of holding cash. To maximise their margins, banks prefer to invest that cash in liquid, easily marketable, interest-bearing securities. Why even keeping reserves in the first place? To minimise the probability of a liquidity crisis (i.e. not being able to face deposit withdrawals, interbank settlements or other liability maturity). If liquidity were not a constraint and banks’ only goal was to maximise profits independently of liquidity risk, they would simply avoid investing in low-yielding securities and lend at a higher margin instead. In order to maintain their net interest margin, it also happens that banks try to slow the pace of deposit inflows by lowering their rates on saving accounts, if they don’t have enough lending opportunities.

Are you starting to see the differences with the MMT/endogenous lending story?

Let’s take a real life example (figures at end-2012): Wells Fargo (a large bank that does not have oversized investment banking activities that distort its balance sheet, which makes it similar to smaller-sized banks as a result). What does its funding structure (liability side of the balance sheet) look like? Unsurprisingly, 83% of its non-equity funding comes from customer deposits. Long-term senior and wholesale funding represents 9% of its funding structure. What about short-term wholesale and interbank funding? 6% only of its total funding. Clearly, Wells Fargo does not fund its lending by borrowing from other banks. Its loans/deposits ratio is 84%. It gets its reserves from other sources.

Let’s pick another similar bank that has a 126% loans/deposits ratio, UK-based Lloyds Banking Group. In this case, deposits could obviously not fund all lending. Did the bank fund its additional lending through interbank borrowing? No. Interbank borrowing only represents 2% of its funding structure. Adding other short-term wholesale funding makes it 10%.

A few points directly stand out:

- Why would banks try to attract depositors, or even bother issuing expensive debt on the bond markets, if all they have to do to fund their lending is an accounting entry followed by some interbank or central bank borrowing?

- Why would banks bother attracting expensive stable funding sources if all they have to do is to continuously increase (or roll over) short-term interbank or central bank borrowings?

- Why are banks even keeping such amounts of primary and secondary reserves if, once again, reserves are not a constraint and all they have to do is to go ask fellow banks or central banks for reserves, which they have to provide to stick to their monetary policy?

From all those points, MMTers could reach the conclusion that bankers don’t seem to know what they’re doing.

There is a relatively straightforward answer to those questions: reserves still matter. Reserves are not directly lent out. They are indirectly lent out. When a bank credits the account of a customer out of thin air following a loan agreement, it exposes itself to a flight of reserves whose amount is equal to the loan, as correctly described by MMTers. Therefore, banks need to maintain an adequate level of reserves, as represented by their primary and secondary reserve buffers. If their primary reserves are low, banks can sell some of their secondary reserves to get hold of new cash for settlements. No need to borrow from the interbank market. However, there is a limit to this process: at some point, secondary reserves will also be exhausted. This is extremely unlikely though. Such a fall in balance sheet liquidity would be punished by financial markets (see below), incentivising banks to retain enough liquidity.

Moreover, banks usually try to avoid borrowing more than a limited amount on the interbank/money market. Why?

- Because this is a suicidal way of funding banking activities. A bank that would only rely on short-term and volatile interbank borrowing to fund its lending would expose itself to market actors’ furore: banks would start reducing their exposures to it, rating agencies would downgrade it, its share price would fall, and its cost of borrowing on the interbank market (or anywhere else) would rise.

- Because borrowing at very short-notice on wholesale markets would expose the bank to penalty interest rates. Most central banks also apply penalty rates to banks short of reserves.

But, the central bank has a target rate and needs to stick to it, MMTers are going to reply, thereby providing all the required reserves to this bank. What are the implications of such a claim?

Implications for a single bank

A bank that would have single-handedly increased its lending, and hence its liabilities, without securing reserves in the first place, is at risk of experiencing adverse interbank clearing and losing some of its reserves. At some point, its reserves could fall below the required amount. However, as we have seen above, the bank holds secondary reserves that it can deplete before running out of primary reserves. What the MMT story overlooks is market reactions to a bank losing its liquidity. I know no investor or no banker that would provide funds to a bank running out of liquid reserves, unless at increasingly high interest rates, even if they know that the bank could obtain reserves from the central bank. As a result, a bank single-handedly expanding beyond what its reserve would normally allow it to is going to experience a quickly rising marginal cost of funding as a response to the loss of its liquid holdings, pressurising its net interest margin and stopping its expansion.

If the bank reaches the point at which it has to borrow directly from the central bank as it has no other choice, it is already too late: markets are aware of its lack of primary or secondary reserves and won’t deal with it anymore. As a result, central banks’ overnight lending in such conditions is self-defeating. Banks, which is an industry based on trust and reputation, will do everything they can to prevent this situation from occurring in order to avoid the stigma associated with it, as we’ve seen many times during the crisis (see also a Fed study here, as well as this one). However, a bank in good financial health could well borrow from the central bank’s discount window from time to time to optimise its liability structure and cost of funding. In the end, a single bank might not technically be reserve-constrained, but it becomes reserve-constrained through market discipline! Of course, in good times, market participants can become more tolerant towards less-liquid balance sheet structures, but the principle still applies.

We could apply the same line of reasoning to asset quality. As a bank expands, the marginal return on lending diminishes and it has to lend to increasingly less creditworthy borrowers. The resulting pressure on its asset quality starts worrying market actors, impacting its cost of funding and slowing its expansion.

Moreover, the interbank lending rate need not rise if a single bank is having difficulties to fund itself. Other banks could actually see their borrowing cost fall as they see massive money market deposit inflows, keeping the aggregate rate stable. Second, central banks clearly cannot completely control the rate: it jumps way above target from time to time.

Implications for the system as a whole

There seems to be an inherent implication to the MMT/endogenous lending story: all banks have a natural incentive to expand as they can freely borrow reserves from the central bank. By literally following their description, it seems that most, if not all banks are fully loaned up as there is no risk of becoming illiquid. Although in such a case, there is no way they can borrow and lend from the interbank market: none of them has excess reserves. The only thing they can do is borrow from the central bank, which cannot refuse if it wants its target interest rate to remain on target. Consequently, the central bank cannot control the money supply as demand for commercial loans is out of its control.

There are a couple of contradictions here. If all banks are short of reserves, there is no interbank market anymore. Nonetheless, it is true that money markets can still exist with money market funds and other non-bank financial institutions and businesses supplying short-term cash to banks. However, this situation is unlikely to happen: as described above, increasing marginal cost of funding for all the banks trying to expand beyond reasonable will slow and eventually stop the process. Only a simultaneous increase in lending by all banks could lead to all banks expanding beyond the limit. In such a case, interbank settlements would cancel out, leaving the reserve positions of each bank unaffected, with no need to borrow for settlements. In practice, banks never expand at the exact same time: some banks are aggressive, some banks are conservative.

What about empirical evidence?

The evident conclusion that MMTers reach is that reserve requirements are ineffective in reducing loan growth. Is there any empirical evidence to confirm this claim? There is. But it doesn’t exactly reach the same conclusion. A few central banks actively use reserve requirements as a monetary policy tool, such as China’s, Russia’s, Brazil’s and Turkey’s. Take a look at the charts from this recent Gavyn Davies article in the FT on China:

From those charts, we can see that every time reserve requirements are cut (mid-2008, early 2012), loan growth surges temporarily while the newly-available reserves are released. When reserve requirements are increased (early 2010, early 2011), loan growth slightly falls relative to trend. Granted, those charts do not show us the whole picture: other factors may well impact loan growth.

Another FT blog post summarised the trend, although the chart stops in 2010:

A BIS study on Chinese reserve requirements also found a link:

I don’t have data for Turkey and Russia, but this study found that increases in reserve requirements led to a contraction in domestic credit in Brazil.

What about interbank lending rate? It is pretty well reported that banks in worse financial health have to pay more for reserves on the interbank market (or on any other market). This should not be a surprise to financial markets actors: everyone knows that illiquid and/or insolvent banks have wider credit spreads. Does it necessarily mean that, as soon as a bank has to pay more than the target rate, it should instead borrow from the central bank? Obviously not. And we have already mentioned the stigma associated to this.

Finally, what about the moral hazard associated with unrestricted supply of reserves? If this were true, surely this is a very bad way of designing and managing a banking system?

This leaves us with the good’ol money multiplier textbook explanation. As I said at the beginning of this (long) post, it is quite outdated, but it remains essentially right, albeit in an indirect way. Nowadays, banks engage in what they call ALM (asset/liability management) through specific departments that identify and manage mismatches between the maturities of assets and liabilities and their respective cash inflows and outflows. As a result of this dynamic and active management, banks try to economise on reserves and take slightly more funding and liquidity risks than 19th century “collect and lend”-type banks. Nonetheless, reserves still matter and ALM bankers and treasurers also set up contingency liquidity plans, which would not make sense if they could freely access interbank or central bank funding without repercussions.

There are probably other things I could say about the MMT/endogenous money story. I may follow-up later, but for now this post is long enough… I just thought that some reality had to be reintroduced into the story, which sounds theoretically as pleasant as a fairy tale but doesn’t seem to stand its ground when you dig a little deeper.

Update: I initially quoted Frances Coppola in this post as her view seemed to be pretty similar to the quoted MMT story. She told me it wasn’t the case, and I updated the post as a result. There are still several things she said that I don’t agree with though.

Fiat money is backed by men with guns

Only a quick post today unfortunately (I’ve been working on another looooooooooooong post over the last few days).

However, I thought I should mention at least two things.

Yesterday, Lawrence Summers published a piece in the Financial Times about his secular stagnation theory. Anything new? Nop. Like nothing had happened since he first mentioned the concept. Like if his original speech had never triggered a great debate among economists. So he obviously didn’t address any of the counter-arguments made by other people… Ivory towers anyone?…

About a week ago, Bob Murphy had a ‘funny’ post on Krugman. Remember when I said that fiat money wasn’t backed by the ‘productive capacity of the country’ and other meaningless abstract concepts like that? Krugman seems to agree… Well… sort of, as he believes that fiat money is backed by… men with guns!… which gives fiat money its value… Nice type of money, that’s for sure. I love the sense of liberty that some Keynesians have.

The Financial Times on Bitcoin, P2P lending and secular stagnation

The FT has a few articles on some of my favourite topics today.

John Authers argue that it is time to take Bitcoin seriously. Who would say that I disagree? In his article he refers to several points I had already mentioned in some of my previous posts. He adds an interesting analogy with previous internet firms and concepts:

[…] even if Bitcoin is as successful as it is possible now to imagine, it looks overvalued at recent prices. It is in a bubble.

But this does not prove that the concept has no future. Shares in Amazon.com were also in a bubble in the late 1990s, and yet proved a great long-term investment after the bubble burst. Wild swings in value are typical when new technologies arrive.

A commenter also had a very good point, which highlighted Bitcoin’s (or other similar alternative digital currencies’) potential trade-boosting abilities:

Can you imagine a world where anyone can set up a shop on the internet and instantly accept payments from all over the world to sell its product or service without any intermediary? Well that’s only one face of what Bitcoin enables.

Naysayers will keep saying that Bitcoin is useless or only diverts wealth from ‘productive opportunities’ anyway.

FT Alphaville continued its long tradition of confused/confusing posts with this one on P2P lending today. I don’t know about you, but it does look to me that everything in the financial world that’s innovative and far from regulators’ grip is now under attack from Alphaville bloggers. They could have a point. But in this case, they don’t. They completely miss the point. The author misunderstands the financial crisis and draws the wrong conclusions from it.

According to the author, P2P is ‘pro-cyclical’ and has ‘no skin in the game’, which makes this asset class of systemic risk. He’d like to see P2P platforms to hold capital buffers to absorb losses. This makes no sense whatsoever. P2P is an investment. There are tons on possible investments. Anybody can invest directly in equities or bonds or FX or whatever, or through mutual funds/investment managers. P2P works the same way. Are we asking mutual funds to hold a capital buffer to absorb losses suffered by their clients’ portfolio? Of course not.

Banks need to retain capital as they hold deposits, which are part of the money supply and can be drawn down at any time by depositors, and also because they play a critical role in the payment system. If banks make losses on lending, capital allows them not to transfer the loss onto customers, who often just wanted to store their money there. This has absolutely nothing to do with the kind of voluntary investments I described above. Moreover, some P2P platforms have already set up loss-absorbing funds anyway… Platforms also have their ‘skin in the game’: if everybody stops lending through them, they don’t earn any revenue and go out of business. While I agree that platforms should not hide the fact that losses could occur on P2P investments, paternalism and regulation is the wrong way to go. Education and responsibility should be the goals.

In another Alphaville blog post, Izabella Kaminska reports the arguments of two economists against the Summers/Krugman secular stagnation story. And it basically reflects mine: it doesn’t exist. It also has a particular Austrian flavour: savings and productivity generate long-term economic growth, and low interest rates caused the economy to boom above potential (debt accumulation) and caused malinvestments (investments that generated short-term growth but that no one wanted in the end).

• There is no shortage of high return investment projects in the world. And the dearth of global corporate investment, which drove the great recession, means that productive potential is shrinking despite corporate profitability, leverage and cash balances being sound.

• The three ingredients for growth are a) a stable macro environment; b) a sound banking system; c) economic reforms that encourage entrepreneurship. What is missing right now is private sector confidence in the ability of governments and central bankers to provide all three.

• Credit bubbles can boost growth only temporarily and incur heavy costs in terms of subsequent deleveraging and misallocation of resources.

Hedge funds keep attracting new money (assets under management are up 16% since end-2012)… I won’t remind you that I’m wondering whether or not this is a sign that nominal interest rates are lower than their Wicksellian natural rates, forcing investors to take extra risk to achieve the real rates of return they would normally obtain from safer investments. But I guess that Summers and Krugman would say that, anyway, bubbles are necessary for the economy. Another side of the story is that not that many people seem to believe anymore in hedge funds outperforming the markets. Hedge funds seem to be transformed into mutual funds… But in this case, why paying such high management and performance fees? This doesn’t make so much sense.

A brief comment on Blackrock, groupthinking and ‘secular stagnation’

Two interesting articles on Blackrock, the world’s largest asset manager (here and here) in this week’s Economist. The Economist is right to point out that regulators would be wrong to classify Blackrock as systematically important, which would considerably increase its regulatory burden. Unlike banks, Blackrock (and other asset managers) transfers money rather than creates it. As a result, there is no risk of ‘secondary deflation’, or money supply contraction, during a crisis if the value of its assets under management fall or if Blackrock itself fails. If markets collapse, investors take the hit, not Blackrock or any other asset manager (although they do take a hit to their revenues as assets under management fall). Of course, investors suffering from a fall in asset value can have other repercussions on the economy. But at least the collapse is not made worse by banks contracting their lending or failing, putting pressure on the money supply at the very moment money demand jumps.

The other issue raised by The Economist is about ‘groupthinking’, as many investors now use the asset manager’s analytics platform to guide them in their investment and trading decisions. The Economist is right on that topic too. However, I would say that groupthinking does not only emanate from Blackrock’s platforms… It is probably a topic I’ll discuss more in details another time, but we could argue that financial exams such as the CFA also push towards groupthinking by making it compulsory to follow certain analytical frameworks while not offering any real alternative. Therefore investors end up using the same models. Various investors will evidently come up with differing inputs; but those would then pass through the same machinery and outputs would be only slightly different.

A quick note on the fashionable ‘secular stagnation’, Lawrence Summers’ and Paul Krugman’s new favourite topic (actually, I don’t know). Apparently, there aren’t enough productive investments in the world relative to the stock of savings. The “appetite to invest” (in The Economist’s words) is low.

I found an interesting short video yesterday:

Does it remind you anything? I’ve argued many times over the past few months that there are indeed plenty of productive investments, but that entrepreneurs and investors are too scared to invest due to regime uncertainty and red tape (see also here and here). Let’s name a few: fracking, mobile IT, emerging markets, commercial space ventures, drones, green energy… And I’m surely forgetting a lot. Yet, so many economists try to reach conclusions from analysing a few aggregated macro-economic data while forgetting to take a look at what’s going on the micro-economics side. This is a big mistake.

Recent Comments