What most people seem to have missed about high-frequency trading

I finished reading Michael Lewis’ new book Flashboys last week. I wasn’t a specialist of high-frequency trading (HFT) at all, so I found the book interesting. Overall, it was an easy read. Perhaps too easy. I am always suspicious of easy-to-read books and articles that supposedly describe complex phenomena and mechanisms. Flashboys partly falls in that trap. Lewis has a real talent to entertain the reader. He unfortunately often slightly exaggerates and attacks the HFT industry without giving them the opportunity to respond. More annoyingly, the whole book reads like a giant advertising campaign for IEX, the new ‘fair’ exchange set up by Brad Katsuyama. In the end, I was left with a slightly strange aftertaste: the book is very partisan. I guess I shouldn’t have been surprised.

The book, as well as HFT, have been the topic of much discussion over the past few weeks*. I won’t come back to most of those comments, but I wish here to highlight what many people seem to have missed. Lewis, as well as many commenters, drew the wrong conclusions from the recent HFT experience. They misinterpret both the role of regulation and the market process itself.

What is most people’s first answer to the potential ‘damage’ caused by HFT? Regulation. I would encourage those people to read the book a second time. Perhaps a third time. This is Lewis:

How was it legal for a handful of insiders to operate at faster speeds than the rest of the market and, in effect, steal from investors? He soon had his answer: Regulation National Market System. Passed by the SEC in 2005 but not implemented until 2007, Reg NMS, as it became known, required brokers to find the best market prices for the investors they represented. The regulation had been inspired by charges of front-running made in 2004 against two dozen specialists on the floor of the old New York Stock Exchange – a charge the specialists settled by paying a $241 million fine.

Bingo.

Until 2007, brokers had discretion over how to handle investors’ trade orders. Despite the few cases of fraud/front-running, most investors didn’t seem to particularly hate that system. In a free market, investors are free to change broker if they are displeased with the service provided by their current one. At the very least, nothing seemed to really justify government’s intervention to institutionalise and regulate the exact way brokers were supposed to handle trade orders. In fact, when government took private discretion away, investors started feeling worse off. This is the very topic of the book (though Lewis didn’t seem to notice): government and regulation created HFT.

Brad Katsuyama sums it up pretty well (emphasis mine):

I hate them [HFT traders] a lot less than before we started. This is not their fault. I think most of them have just rationalized that the market is creating inefficiencies and they are just capitalizing on them. Really, it’s brilliant what they have done within the bound of regulation. They are much less a villain than I thought. The system has let down the investor.

Brad is definitely less naïve than Lewis, who still believed in the power of regulation throughout his book**:

Like a lot of regulations, Reg NMS was well-meaning and sensible. If everyone on Wall Street abided by the rule’s spirit, the rule would have established a new fairness in the U.S. stock market.

Meanwhile, David Glasner questioned the ‘social value’ of HFT on his blog:

Lots of other people have weighed in on both sides, some defending high-frequency trading against Lewis’s accusations, pointing out that high-frequency trading has added liquidity to the market and reduced bid-ask spreads, so that ordinary investors are made better off, not worse off, as Lewis charges, and others backing him up. Still others argue that any problems with high-frequency trading are caused by regulators, not by high-speed trading as such.

I think all of this misses the point. Lots of investors are indeed benefiting from the reduced bid-ask spreads resulting from low-cost high-frequency trading. Does that mean that high-frequency trading is a good thing? Um, not necessarily.

I believe that here it is Glasner who completely misses the point. Should we blame HFT traders from exploiting loopholes created by regulation? Economists are better placed than anyone to know that people respond to economic incentives. The resources ‘wasted’ by HFT on ‘socially useless informational advantages’ emanate from government intervention. It is highly likely that HFT would have never developed under its current form should Reg NMS had not been passed. What we instead witness is another case of regulatory-incentivised spontaneous financial innovation.

The second problem lies in the fact that most people seem to have become particularly impatient and dependent on short-term (and short-sighted) regulatory interventions. They spot a new ‘problem’ in the way markets work (here, HFT) and highlight it as a ‘market inefficiency’. This evidently cannot be tolerated any longer and regulators need to intervene right now to make markets ‘fairer’ (putting aside the fact that they were the ones who created this ‘inefficiency’ in the first place).

This demonstrates a fundamental misinterpretation of the market process. Markets’ and competitive landscapes’ adaptations aren’t instantaneous. This allows first movers to take advantage of consumers/investors demand and/or regulatory loopholes to generate supernormal profits… temporarily. In the medium term, the new economic incentives attract new entrants, which progressively erode the first movers’ advantage.

This occurs in all industries. Financial firms are no different (assuming no government protection or subsidies). And, despite Lewis’ outrage at HFT firms’ super profits, the fact is… that the mechanism I just described has already applied to them. It was reported that the whole industry experienced an 80% fall in profits between 2009 and 2012 (which Tyler Cowen had already ‘predicted’ here).

Besides, the story the book tells is a pure free-market story: a group of entrepreneurs wish to offer an alternative platforms to investors who also decide to follow them. There is no government intervention here. The market, distorted for a little while, is sorting itself out. Even the big banks see the tide turning and start switching sides (Goldman Sachs is depicted in a relatively positive light in the book). Lewis’ book itself is also part of that free-market story: the finger-pointing and informational role it plays is a necessary feature of the market process. To me, this demonstrates the ability of markets to right themselves in the medium-term. Patience is nevertheless required. It unfortunately seems to be an increasingly scarce commodity nowadays.

There was a very good description of HFT and its strategies published by Oliver Wyman at the end of last year (from which the chart below is taken). Surprisingly, they described HFT’s strategies and the effects of Reg NMS before the publication of Lewis’ book, without unleashing such a public outcry…

* See some there: FT’s John Gapper, The Economist, David Glasner, Noah Smith, Zero Hedge, Tyler Cowen (and here), ASI’s Tim Worstall, as well as this new paper by Joseph Stiglitz, who completely misinterprets the market process. See also this older, but very interesting, article by JP Koning on Mises.org on HFT seen through both Walrasian and Mengerian descriptions of the pricing process.

I also wish to congratulate Bob Murphy for this magical tweet:

** This is also despite Lewis reporting this hilarious dialogue between Brad Katsuyama and SEC regulators (emphasis his):

When [Brad, who had just read a document describing how to prevent HFT traders from front-running investors] was finished, an SEC staffer said, What you are doing is not fair to high-frequency traders. You’re not letting them get out of the way.

Excuse me? said Brad

And to continue saying that 200 SEC employees had left their government jobs to go work for HFT and related firms, including some who had played an important role in defining HFT regulation. It reminded me of this recent study that showed that SEC employees benefited from abnormal positive returns on their securities portfolios…

Blame the rich for the next asset bubble. Or not.

First of all, happy new year to all of you! Fingers crossed we don’t witness another market crash this year! 🙂

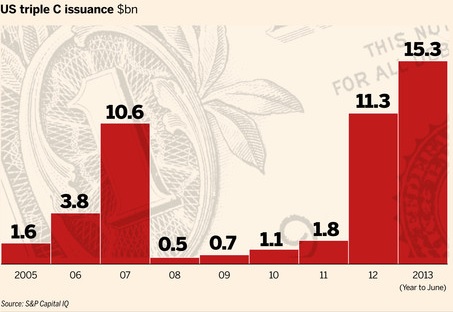

Indeed, credit markets are hot. Equity markets are also hot. The FT published an article yesterday with some striking facts about the ‘improvements’ in credit markets over the past couple of years. Some would say that it’s encouraging. I am not convinced…

Most credit indicators are close to or above their pre-credit crisis high. Sales of leveraged loans and high-yield bonds are above their pre-crisis peak. The average leverage level of US LBOs is back to 2006 level. Issuance of collateralised loan obligations is close to its pre-crisis peak. Even CCC-rated junk bonds are way above their previous peak. I’ve already mentioned some of those facts a few months ago.

In a relatively recent presentation, Citi’s strategist Hans Lorenzen confirmed the trend: central banks are indirectly suppressing most risky investments’ risk premia. Most investors expect junk bonds’ spreads to tighten further or at least to stabilise at those narrow levels and emerging markets bonds and equities, as well as junk bonds are now among investors’ top asset classes .

My ‘theory’ at the time was that (see also here), if investors were piling in increasingly riskier asset classes, bringing their yield down to record low levels in the process, and nonetheless accepting this level of risk for such low returns, it was because current central bank-defined nominal interest rates were below the Wicksellian natural rate of interest. Inflation, as felt by investors rather than the one reported by national statistics agencies, was higher than most real rates of return on relatively safe assets. In order to see their capital growing (or at least to prevent it from declining), they were forced to pick riskier assets, such as high-yield bonds, which were not really high-yield anymore as a result but remained junk nonetheless. This would result in capital misallocation as, under ‘natural’ interest rate conditions, those investments would have never taken place. Thomas Aubrey’s Wicksellian differential, an indicator of the likely gap between the nominal and the natural rates of interest, was, in line with credit markets, reaching its pre-crisis high and seemed to confirm that ‘theory’.

Well, I now think that not all investors are responsible for what we are witnessing today. The (very) rich are.

This came to my mind some time ago while reading that FT piece by John Authers. This was revealing.

“Their wealth gives them scope to try imaginative investments, but they are terrified of inflation, even as deflation is emerging as a greater risk. That is in part because inflation for the goods and services bought by the very rich is running about 2 percentage points faster than retail inflation as a whole in the UK.” (my emphasis)

In the UK, real gilts’ yields were already in negative territory: adjusted by the (potentially underestimated) consumer price index, gilts were yielding around -1% early 2013. Savers were effectively losing money by investing in those bonds. Now think about the rich: by investing in such bonds, they would get a real return of around -3% instead.

Moreover, “71 per cent of respondents said they were more worried now about a steep rise in inflation than they were five years ago.”

Does it start to make sense? The cost of living I was mentioning earlier is increasing particularly quickly for the rich. And… they are the ones who own most financial assets. In order to offset those rising living costs, they naturally look for higher-yielding investments. And it is exactly what the FT reports:

“Their favourite asset classes for the next three decades are emerging markets equities, developed equities and agricultural land, in that order. Private equity comes close after farmland, while art and collectables were also a more popular asset class than any kind of bonds. […]

Hedge funds, as a group, have not fared well since the crisis. But wealthy investors preoccupied by inflation, and robbed of the easy option of bonds, are evidently disposed to give them a try, with an average projected allocation for the next three decades of 25 per cent. Meanwhile, the chance of a bubble in agricultural land prices, or in art, looks very real.”

Are the rich responsible for our current frothy markets then? Obviously not. They are acting rationally in response to central banks’ policies. Nonetheless, this raises an interesting question. Mainstream economics only considers a high aggregate inflation rate as dangerous. What about ‘class warfare’-type inflation? It does look like inflation experienced by one socioeconomic class could inadvertently lead to asset bubbles and bursts, despite aggregate inflation remaining subdued. This may be another destabilising effect of monetary injections on relative prices.

Granted, central banks possibly are on a Keynesian’s ‘euthanasia of the rentier’-type scheme in order to try to alleviate the pain of over-indebted borrowers (and/or to encourage further lending). But financial repression avoidance might well end-up coming back with a vengeance if savers’ reactions, and in particular, rich savers’, make financial markets bubble and crash.

Charts: FT (link above), Citi and Societé Générale

Izabella Kaminska gets confused on 100%-reserve banking, or collateral, unless it’s… wait, I’m confused now

Meanwhile, Izabella Kaminska in the FT had an interesting (as usual), but very confused and confusing, blog post. I asked whether or not she was reading my blog given that some of her claims pretty much reflect mine (she calls the shadow banking system a “decentralised full-reserve banking system that just happens to run parallel with the official fractional system we are used to.” Compare that with my “[…] parallel 100%-reserve banking system. The shadow banking system is effectively some version of a 100%-reserve banking.”). But the similarities stop here. She sounds very confused… She gets mixed up between various terms, principles and concepts and tries to hide it behind quite complex wordings.

She mixes collateralised lending with 100%-reserve and uncollateralised lending with money creation. They are in fact totally unrelated. A bank or shadow bank can be fractional-reserve-based or 100%-reserve-based, which simply relates to whether or not a bank lends out a share of its deposits or if it maintains them in full in its vaults. Collateralised lending is, well, just lending provided against collateral (which can be almost any type of assets). Both fractional and 100%-reserve banks can lend against collateral in order to minimise the risk of loss in case of default. 100%-collateralised lending is not 100%-reserve.

True, 100%-cash collateralised lending could be thought of as some form of 100%-reserve banking as the cash reserve at the bank would virtually never depart from the deposit base amount. For example, if a fractional bank collects USD100 in deposits and lends out USD90, it only keeps 10% of cash deposits in reserve. If, though, it lends out USD90 collateralised against USD90 of cash, then it ends up with USD100 in its vault, the same amount as the deposit base (although there will be limitations on the liquidity of the cash as the collateral will likely be ‘stuck’ until repayment or default). But, following her claim, a mortgage bank would be a 100%-reserve bank as the value of the housing portfolio on which lending is secured is worth more than the amount of lending. This is obviously wrong. Unless houses are now a generally-accepted medium of exchange?

Then she claims that “the official banking sector, for example, has the capacity to make uncollateralised investments in growth areas it feels are promising regardless of whether borrowers have collateral, or whether they can be fully funded.” Not really. First, banks usually collateralise between a quarter and more than 100% of their lending. Second, “uncollateralised investments in growth areas it feels are promising regardless of whether borrowers have collateral” is called venture capital and is clearly not what banks do. Venture capital funds, business angels, and some crowdfunding and P2P platforms are here for that (you could also probably add the junk bond market to the list). She then adds that, in contrast to banks, “the shadow banking sector’s strength, of course, is that it is prepared to service those entities (whether directly or indirectly) the official banking sector is not prepared to service, thanks to a greater emphasis on collateral or funding.” As I just said, this is not the case. Venture capital-type investments cannot accept collateral as… there is none! This is why they are high-risk.

According to Izabella, there is a reason why shadow banks cannot create money: their use of collateral. While it is true that (most, probably all) shadow banks cannot create money, it is not because they lend against collateral as described above. A lot of shadow banks don’t lend against collateral: think most money market funds, P2P lending, hedge funds, mutual funds, payday lenders…or simply the bond market! But they don’t create money either! They only transfer cash.

In the comment section she also seems to claim that fractional reserve banking is an innovation of our modern banking system. Where did she get that? Fractional reserves have been used since antiquity: the use of the ‘monetary irregular-deposit’ contract in classical Roman law gave rise to fractional reserves as deposits were mixed with other ones of equivalent nature (as opposed to the mutuum, or monetary loan contract, which is similar to what we could describe as today’s mutual funds for example). Despite the illegality of lending out irregular-deposits, some bankers took advantage of the fungibility of money, and of the fact that many irregular-deposits were rarely withdrawn, to lend out a part of their deposit base. The ‘bank’ of Pope Callistus I (see photo) failed as it was unable to return the irregular-deposits on demand. Other examples of failed banks exist at this period but fractional reserves really took off from the late middle ages in Europe.

Not everything is wrong in her article as I mentioned at the beginning of my post. She’s right to claim that regulation would only displace risk to another corner of the financial system that shadow banking is merely a response to the regulatory-incentivised under-banked part of the economic system, and that P2P lending is a kind of shadow banking. But too many confusions or misunderstandings around collateral, money creation, bank funding, bank reserves, etc., obfuscate the topic.

Financial innovation is back with a vengeance

What didn’t we hear about financial innovation throughout the crisis? Whereas innovation in general is good, financial innovation on the other hand was the worst possible thing coming out of a human mind. Paul Volcker, former Chairman of the Fed, famously declared that the ATM was the only useful financial innovation since the 1980s. Harsh.

True, some financial innovations are better than others. In particular, those used to bypass regulatory restrictions are more dangerous, not because they are intrinsically evil or anything, but simply because their often complex legal structure makes them opaque and difficult for external analysts and investors to analyse. This famous 2010 Fed paper attempted to map the shadow banking system (see picture), and usefully stated that not all shadow banking (and financial innovations) activities were dangerous (but those specifically designed to avoid regulations were). Ironically (and typically…) one of the first innovations to ever appear within the shadow banking system was money market funds. What was the rationale behind their creation? In the 1960s and 1970s in the US, interest payment on bank demand deposits was prohibited and capped on other types of deposits. The resulting financial repression through high inflation pushed financial innovators to come up with a way of bypassing the rule: money market funds became a deposit-equivalent that paid higher interests. Today we blame money market funds for being responsible for a quiet run on banks during the crisis, precipitating their fall. It would just be good to remember that without such stupid regulation in the first place, money market funds might have never existed…

The last decade has seen the growth of two particularly interesting innovations within the shadow banking system: one was relatively hidden (securitisation) while the other one grew in the spotlight (crowdfunding/peer-to-peer lending). One was deemed dangerous. The other one was more than welcome (ok, not in France). What had to happen happened: they are now combining their strength.

Various types of crowdfunding exist: equity crowdfunding, P2P lending, project financing… Today I’m going to focus on P2P lending only. What started as platforms enabling individuals to lend to other individuals are now turning into massive gates for complex institutional investors to lend to individuals and SMEs. Given the retreat of banks from the SME market (thank you Basel), various institutional investors (mutual and hedge funds, insurance firms) thought about diversifying their investments (and maximising their returns) by starting to offer loans to individuals and companies they normally can’t reach.

Basically, those funds had a few options: developing the capabilities to directly lend to those customers, investing in securitised portfolios of bank loans, or investing in securitised portfolios of P2P loans. The first option was very complex to implement and the required infrastructure would take a long time to develop. The second option had already existed for a little while, but was dependent on banks lending to customers, which current regulations limit due to higher capital requirements on such loans. The third option, on the other hand, allowed funds to maximise returns and attract more potential borrowers thanks to the reduction of the cost of borrowing by disintermediating banks. And funds could also strike deals with those still tiny online platforms that would have never happened with massive banks.

While securitisation sounds scary, it is actually only a simpler way of investing in loans of small sizes (the alternative being to invest in every single loan, some of them amounting to only USD500… Not only many funds don’t have the capability of doing such things, but many have also restrictions about the types of asset class and amounts they can invest in). Securitisation also bypasses Wall Street investment banks: funds directly invest in P2P loans, package them and sell them on to other investors while retaining a ‘tranche’ in the deal, which absorbs losses first. Now some entrepreneurs are even talking of setting up secondary markets to trade investments in loans, pretty much like a smaller version of the bond market.

Is this a welcome evolution for the P2P industry? I would say that it is a necessary evolution. It is once again a spontaneous development that merely reflects the need for funding of the P2P industry, which small retail investors cannot fulfil (unless all investment funds’ customers start withdrawing their money to directly invest in P2P, which is highly unlikely). Many start to think that large institutional investors will end up crowding out small retail investors. Possibly, but as long as regulation remains light, keeping barriers to entry low, new platforms only accepting retail investors could well appear if the demand is present.

All this is fascinating. Not only because technology and the internet enables new ways of channelling funds from savers to borrowers, but also because this is the growth of a parallel 100%-reserve banking system. The shadow banking system is effectively some version of a 100%-reserve banking. And it keeps growing through those various innovations. As I argued in a previous post, this may well have implications for monetary policy that current central banks and economists don’t take into account. A 100%-reserve banking system does not have a deposit multiplier and consequently does not have an elastic currency to respond to a sudden increase or decrease in the demand for money. However, such a system perfectly matches savers’ and borrowers’ intertemporal preferences, limiting malinvestments. Nonetheless, we for now remain in a mix system of 100% reserve (most of shadow banking) and fractional reserves (traditional banking). It would still be interesting to study the possible policy implications of a growth in the 100%-reserve part of the economy.

Co-operative Bank’s new ownership ‘tragedy’ is rather a good thing

For those of you who don’t live in the UK, the Co-operative Bank has been struggling with a large GBP1.5bn capital shortfall (vs. a capital base of GBP1.6bn) since early summer due to losses on its loan book (most of them emanating from the takeover of Britannia Building Society in 2009, a struggling mutual mortgage bank). Moody’s, the rating agency, even downgraded it by six notches all of a sudden. The Co-operative Bank was a subsidiary of the Co-operative Group, a mutual company that owns multiple businesses.

I said ‘was’ because…it won’t be anymore. And it’s apparently causing some headaches.

Mutual companies are owned by their members (who are some of their customers), and not by external shareholders. This was the case of both Britannia’s and Co-op’s equity capital (indirectly through the Co-op Group). However, due to their very nature, mutuals’ ability to raise capital is limited. Consequently, they raise complementary capital from external investors in order to grow. In the case of Co-op, its equity capital was complemented by some sort of hybrid capital: GBP60m of preference shares owned by retail investors and around GBP1.1bn of subordinated debt, which happened to be partly held by…hedge funds. Both counted towards the total regulatory capital ratio of the bank, as defined by Basel accords. Ranking of the capital structure in case of bankruptcy of the bank was as follows: after depositors and other senior creditors, subordinated creditors had the second claims on the liquidated assets of the bank, followed by preference shares-holders and members.

Following several months of negotiations that saw creditors threatening to block a deal under which they would take a loss on their investments, a deal was finally reached a few days ago: a conversion of their bonds into new equity. As a result, 70% of the capital of the bank will be owned by institutional investors, among which several hedge funds (representing around 30/40%). The Co-op Group (and hence members) will retain a 30% stake in the bank. It obviously sounds quite ironic to see a mutual company owned by vulture capitalists… It also looks quite ironic to see the failure of the now all-powerful UK regulators: they never spotted the problems at Co-op Bank, all their proposed solutions collapsed once after the other, and the agreed deal was reached in a perfect free-market type agreement without their intervention…

Many people around me and in the media have raised concerns that the new hedge funds ownership was a bad thing due to the short-term view of their investment strategy. Those fears are misplaced. Hedge funds and private equity firms indeed invest for the short-term. As far as I’m aware, there aren’t many studies analysing the impacts of hedge funds on the performance of the firms in which they own a stake. This recent one found that activist hedge funds actually improved future performances! There are many more studies on the long-term effects of short-term private equity investments. It was actually the topic of my Masters’ research dissertation. The academic research was clear: private equity-owned firms suffered over the short-term through tough restructuring processes (involving job losses and pressure on salaries), but over the longer-term performed better than their peers and actually even hired more people…

Is this surprising? No. We really need to keep emotions aside and think about the underlying reasons for all this. What is the hedge fund’s goal? To maximise profits. What is the time frame? Usually quite short-term (= a few years). How can the fund exit the investment? By selling the company to external investors. Here we go. This is key. Do you think that funds would be able to maximise the selling price if external investors viewed the company as unlikely to perform well over time? Of course not. Prices are derived from future discounted cash flows. The more likely the company is to perform well after the sale, the higher the price the hedge (or private equity) fund can extract from it. As a result, it is not in the interest of the fund to seek “short-term gains at the expense of the future”.

Of course, this does not mean that no failure ever happens. Some funds also acquire companies to dismantle them. Which does not necessarily imply that they are evil. Some companies actually represent net economic losses to society with no prospect of improvements. Those companies should disappear and capital reallocated to more efficient ones. Funds that dismantle companies usually do it as there is no other way to realise profits. Some funds also fail in restructuring firms, or overload them with debt. But when the companies fail, funds also make massive losses that threaten their own existence. It is in the interest of both to succeed.

Co-op Bank’s former CEO declared that the restructuring process was a ‘tragedy’, that hedge funds were ‘maximising profits’ and were ‘unethical’. I would like to ask: what is actually a tragedy? Is mismanaging an institution leading to bankruptcy and potential losses for ordinary individuals that ethical? What about mis-selling financial products to naïve customers on top of that? Wouldn’t it be better to have a well-performing bank that generates economic profits? Are low profits, losses and waste of capital a way of proving that a company is behaving well? Or is a company more useful for human and social advancement if it actually delivers economic benefit and creates additional capital? Some people have serious rethinking to do.

There is no real need to worry about hedge funds owning a large stake in Co-operative Bank. Co-op may well at last become an asset to society instead of a liability. Its new hedge fund owners also seem to understand that to maximise the value of the brand, ethics must remain a focus, whatever that means. But if eventually Co-op does not survive, it may also well be because it couldn’t be saved in the first place.

Update: I don’t know how I originally missed the senior creditors but I did… Depositors aren’t the only senior creditors and this is now corrected

Quick update on recent news: John Kay, hedge funds and house prices control

John Kay wrote an interesting piece in the FT yesterday saying that finance should be treated like fast food to secure stability. I can’t agree more. A nice quote:

Still, would it not be better if proper supervision ensured that no financial institution could ever get into a mess like Northern Rock or Lehman – or Royal Bank of Scotland or Citigroup or AIG? No, it would not. Just replace “financial institution” with “fast-food outlet” or “supermarket” or “carmaker” in that sentence to see how peculiar is the suggestion.

I know what you’re going to say: “but banks are different!” To which I would reply: no, they aren’t. It is treating them as different that makes them different.

Another nice one:

We have experience of structures in which committees in Moscow or Washington take the place of the market in determining the criteria by which a well-run organisation should be judged, and that experience is not encouraging. The truth is that in a constantly changing environment nobody really knows how organisations should best be run, and it is through trial and error that we find out.

I am a little surprised though, as I have the impression that John Kay is kind of contradicting himself (see his post from June in which he seems to say that banking reforms are going the right direction).

Another piece highlighted how much regulation is changing the hedge fund industry. What’s going on is that regulation is now limiting new entrants in the market as they can’t cope with booming compliance costs. This results in the largest hedge funds experiencing most of new money inflow from investors. Is this a problem? Yes. First, small hedge funds have traditionally outperformed large and established ones on average. So preventing them from entering the market reduces market and economic efficiency: proper allocation of capital to where it would be the most profitable does not happen as a result (and consequently, returns to investors are lower). Second, and more worrying, is that regulation is now replicating what has happened in the banking industry: it’s creating too big to fail hedge funds (and nobody seems to remember LTCM). Well done guys.

Finally for today, echoing my earlier post, a BoE member thinks that it is not the role of the central bank to control house prices. I certainly agree.

Spontaneous finance at work

The FT reported today that non-bank lending to SMEs was at its highest level since 2008 in the UK, whereas bank lending had been declining constantly since the start of the crisis, despite politicians’ and central bankers’ actions to revive it (such as the BoE’s Funding for Lending Scheme).

What kind of non-bank lending are we talking about? Personally, I would call this ‘shadow banks lending’, even though some other economists and analysts may have a different definition of shadow banking. To me, it comprises the less-regulated non-bank entities, from hedge funds to peer-to-peer lending platforms.

This is spontaneous finance at work: while the bloated, politically connected and over-regulated banking system does not seem to be able to channel resources (private savings) to smaller-than-large corporations, private actors, from investment funds to private individuals, step in to respond to their funding needs. This phenomenon has two sources: banks’ lending rates are often too high (blame regulatory capital requirements) and banks’ offered savings rate too low (blame too high inflation vs. BoE rate). And blame banks’ too high operating costs for both. As a result, there is a mismatch between what savers expect and what companies expect.

The solution? Bypass banks. Various investment companies (from hedge funds to more traditional mutual funds) are now setting up funds to gather savings and lend directly to companies that need them. Peer-to-peer and crowdfunding platforms basically act the same way by disintermediating all financial institutions: individuals directly lend to other individuals or firms. We also now see funds investing through P2P platforms (reversing the disintermediation process). Through those shadow banking channels, both savers and borrowers get better rates than they would do at a bank. At the time of my writing, savers can earn from 4% to 7% on their savings (even some hedge funds would love to get such steady returns). Rates vary for borrowers, but are on average lower than that of banks.

Lending volume is still pretty small as the wider public isn’t yet aware of those funding opportunities. In the UK, Funding Circle has only lent slightly less than GBP170m so far to small businesses (this compares to banks’ SME lending which stands at around GBP170…bn). But it’s growing quickly: it was only launched in 2010. Moreover, other shadow banks had lent around GBP17bn as of June (yes, a lot of 17 something, just a coincidence).

As this City AM article highlighted today, as usual, the main risk to those financial innovations is over-regulation, preventing their development and potentially leading to the creation of much riskier and opaque financial products. Regulators wish to ‘protect’ savers. I argue that savers do not need to be protected: they need to learn to invest responsibly and to understand the risks involved. Protection distorts risk-taking and capital allocation.

More worrying is the fact that some peer-to-peer industry actors are now even lobbying to be regulated… They claim that regulation will reassure potential investors. I claim that regulation will mainly protect the established firms by making it more difficult for new competitors to enter the market and offer competitive products to savers and borrowers. A brand new financial system is building before our eyes. It is important not to repeat mistakes that led to our current ineffective banking system.

Photograph: govopps.co.uk

Recent Comments