Intragroup funding: don’t build the wall

Three years ago, I wrote about the importance of intragroup funding, liquidity and capital flows within a banking group composed of multiple entities – often cross-border, as it is common nowadays. This series of posts started by outlining recent empirical evidence, which suggested that intragroup funding – or, as academics called it, ‘internal capital markets’ – benefited banking groups by allowing the efficient transfer of liquidity where and when it was needed within the multinational bank’s legal entity structure, thereby averting crises or at least dampening its effects, and solidifying the group as a whole.

Follow-up posts described historical experiences and compared the relative stability of the US and Canadian 19th century branching systems: Canadian banks demonstrated a much higher level of financial resilience thanks to their ability to open branches nationwide, compared to the great instability and recurrent crises experienced by large US state banks – whose ability to open branches in other states or districts was severely constrained by law – and later ‘unit’ banks, which were not allowed to open branches altogether. The series also included the example of a modern banking model that combined characteristics of both the fragmented 19th century US and great resilience, thanks to its peculiar liability-sharing, funds transfer mechanism and cross-control structure: the German Sparkassen Finanzgruppe (saving banks group; see post here).

Of course, throughout this series I kept pointing out that all empirical and historical evidence actually went against the current regulatory mindset of fragmenting and siloing banking. Since the financial crisis, regulators have fallen into a very damaging fallacy of composition: their belief that making each separate entity of larger integrated banking groups stronger and raising barriers between them will strengthen the system as whole is deeply flawed.

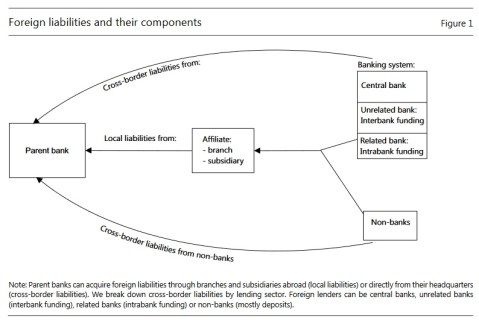

Last month, a new paper confirming the critical aspect of intragroup liquidity transfers for financial stability was published (Changing business model in international funding, by Gambacorta, van Rixtel and Schiaffi). This paper investigates whether banks altered their funding profile when the financial crisis struck and money markets froze. More specifically, they looked at changes in the nature (retail, wholesale, intragroup…) and origins (domestic, foreign) of the liabilities at holding and parent company level, as well as at branches and subsidiary levels. And unsurprisingly:

Our main conclusions are as follows. Following the first episodes of turbulence in the interbank market (after 2007:Q2), globally active banks increased their reliance on funding from branches and subsidiaries abroad, and cut back on funding obtained directly by headquarters (cross-border funding). In particular, banks reduced cross-border funding from unrelated banks – eg those that are not part of the same banking group – and from non-bank entities. At the same time, they increased intragroup cross-border liabilities in an attempt to make more efficient use of their internal capital markets.

The authors make a great job at summarising the current literature on the topic: there is overwhelming evidence that banks rely on ‘internal capital markets’ to absorb external liquidity shocks. Yet, the authors also highlight that there have been a few drivers of declining intragroup flows, of which the siloing of liquidity and capital by new regulation has been the main one:

Of these drivers, regulatory reform has been the main catalyst of the profound changes observed in global banking and its funding structures in recent years. This includes most prominently Basel III and structural banking reforms, such as the “ringfencing” of domestic operations and “subsidiarisation”, which requires banks to operate as subsidiaries overseas, with their own capital and liquidity buffers, and funding dedicated to different entities. Moreover, several jurisdictions have implemented enhanced oversight and prudential measures, including local capital, liquidity and funding requirements and restrictions on intragroup financial transfers, promoting “self-sufficiency” and effectively reducing the scope of global banking groups’ internal capital markets (Goldberg and Gupta, 2013). In effect, these regulations restrict the foreign activities of domestic banks and the local activities of foreign banks (“localisation”; Morgan Stanley and Oliver Wyman, 2013).

They point out that

“ring-fencing” and “subsidiarisation” may constrain the efficient allocation of capital and liquidity within a globally active banking group and the functioning of its internal capital markets; in fact, these proposals have led to concerns that structural banking reforms may potentially trap capital and liquidity in local pools.

As I mentioned several years ago in my previous series on the topic, this is a real concern. Driven by their fallacy of composition, and with no empirical evidence to justify their reforms, regulators are weakening the system as a whole, repeating the mistakes of the US of the past. Moreover, disjointed discretionary regulatory actions are likely to make things worse when the next crisis strikes: domestically-focused regulators are likely to attempt to protect their own national banking system, preventing domestic subsidiaries from transferring much-needed liquidity to their parents abroad, resulting in a weakened international financial system.

The long-term consequences of trapping capital and liquidity where they are not of any need is unknown. But, constrained by the new rules, the profit-maximising private enterprises that banks are may well decide that putting those funds to use is better than leaving them idle, even if they would have been even more profitably used elsewhere. In turn, this would distort the allocation of capital in the economy, with potentially dramatic economic outcomes.

Worryingly, it has been recently reported that regulatory agencies had in mind an even more drastic idea: the elimination through subsidiarisation of most, if not all, international branches, trapping further capital and funding within entities that never needed to hold such funds in the past. Whether this measure is implemented in the end remains to be seen but one thing is certain: political agendas lead to the total disregard of empirical and historical evidence. In banking as in politics, the new ideological fracture seems to be ‘open’ vs. ‘closed’.

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

Trackbacks / Pingbacks