Quick update on recent news: John Kay, hedge funds and house prices control

John Kay wrote an interesting piece in the FT yesterday saying that finance should be treated like fast food to secure stability. I can’t agree more. A nice quote:

Still, would it not be better if proper supervision ensured that no financial institution could ever get into a mess like Northern Rock or Lehman – or Royal Bank of Scotland or Citigroup or AIG? No, it would not. Just replace “financial institution” with “fast-food outlet” or “supermarket” or “carmaker” in that sentence to see how peculiar is the suggestion.

I know what you’re going to say: “but banks are different!” To which I would reply: no, they aren’t. It is treating them as different that makes them different.

Another nice one:

We have experience of structures in which committees in Moscow or Washington take the place of the market in determining the criteria by which a well-run organisation should be judged, and that experience is not encouraging. The truth is that in a constantly changing environment nobody really knows how organisations should best be run, and it is through trial and error that we find out.

I am a little surprised though, as I have the impression that John Kay is kind of contradicting himself (see his post from June in which he seems to say that banking reforms are going the right direction).

Another piece highlighted how much regulation is changing the hedge fund industry. What’s going on is that regulation is now limiting new entrants in the market as they can’t cope with booming compliance costs. This results in the largest hedge funds experiencing most of new money inflow from investors. Is this a problem? Yes. First, small hedge funds have traditionally outperformed large and established ones on average. So preventing them from entering the market reduces market and economic efficiency: proper allocation of capital to where it would be the most profitable does not happen as a result (and consequently, returns to investors are lower). Second, and more worrying, is that regulation is now replicating what has happened in the banking industry: it’s creating too big to fail hedge funds (and nobody seems to remember LTCM). Well done guys.

Finally for today, echoing my earlier post, a BoE member thinks that it is not the role of the central bank to control house prices. I certainly agree.

Spontaneous finance at work

The FT reported today that non-bank lending to SMEs was at its highest level since 2008 in the UK, whereas bank lending had been declining constantly since the start of the crisis, despite politicians’ and central bankers’ actions to revive it (such as the BoE’s Funding for Lending Scheme).

What kind of non-bank lending are we talking about? Personally, I would call this ‘shadow banks lending’, even though some other economists and analysts may have a different definition of shadow banking. To me, it comprises the less-regulated non-bank entities, from hedge funds to peer-to-peer lending platforms.

This is spontaneous finance at work: while the bloated, politically connected and over-regulated banking system does not seem to be able to channel resources (private savings) to smaller-than-large corporations, private actors, from investment funds to private individuals, step in to respond to their funding needs. This phenomenon has two sources: banks’ lending rates are often too high (blame regulatory capital requirements) and banks’ offered savings rate too low (blame too high inflation vs. BoE rate). And blame banks’ too high operating costs for both. As a result, there is a mismatch between what savers expect and what companies expect.

The solution? Bypass banks. Various investment companies (from hedge funds to more traditional mutual funds) are now setting up funds to gather savings and lend directly to companies that need them. Peer-to-peer and crowdfunding platforms basically act the same way by disintermediating all financial institutions: individuals directly lend to other individuals or firms. We also now see funds investing through P2P platforms (reversing the disintermediation process). Through those shadow banking channels, both savers and borrowers get better rates than they would do at a bank. At the time of my writing, savers can earn from 4% to 7% on their savings (even some hedge funds would love to get such steady returns). Rates vary for borrowers, but are on average lower than that of banks.

Lending volume is still pretty small as the wider public isn’t yet aware of those funding opportunities. In the UK, Funding Circle has only lent slightly less than GBP170m so far to small businesses (this compares to banks’ SME lending which stands at around GBP170…bn). But it’s growing quickly: it was only launched in 2010. Moreover, other shadow banks had lent around GBP17bn as of June (yes, a lot of 17 something, just a coincidence).

As this City AM article highlighted today, as usual, the main risk to those financial innovations is over-regulation, preventing their development and potentially leading to the creation of much riskier and opaque financial products. Regulators wish to ‘protect’ savers. I argue that savers do not need to be protected: they need to learn to invest responsibly and to understand the risks involved. Protection distorts risk-taking and capital allocation.

More worrying is the fact that some peer-to-peer industry actors are now even lobbying to be regulated… They claim that regulation will reassure potential investors. I claim that regulation will mainly protect the established firms by making it more difficult for new competitors to enter the market and offer competitive products to savers and borrowers. A brand new financial system is building before our eyes. It is important not to repeat mistakes that led to our current ineffective banking system.

Photograph: govopps.co.uk

Financial bloggers beware

The French financial regulator AMF may end up fining two bloggers (one retired French economics professor and one American investment advisor) who might possibly perhaps maybe hypothetically have influenced financial markets in 2011, when they declared that Societe Generale’s leverage was higher than what the bank officially reported.

This would be a dangerous precedent. Bloggers, financial analysts, journalists and other people are here to independently (or not) analyse news, data and information and express an opinion, whether it is right or wrong. The first question that comes out of this is: could only two bloggers influence markets in such a way? It sounds quite unlikely. Markets are formed by millions of individuals, who can (and do) also come up with their own views. When top-ranked analysts at top banks downgrade companies, markets react negatively, but nowhere near what happened to SocGen at that time (the bank’s share price fell 42% within just 20 days).

Moreover, they also have the right to be wrong. If nobody believes them, their opinion won’t matter. In case people do believe them, it might well mean that there is at least some truth in their arguments.

All this once again looks like witch-hunting. No news here. Throughout the crisis, regulators tried to blame hedge funds, speculators, short-selling, rating agencies and other market participants as soon as a country’s credit spread was jumping or the share price of a bank collapsing. A classic case of ‘shoot the messenger’.

The eventual result of this is that information might become scarcer as analysts fear getting sued even if they are actually right. This is evidently the wrong solution. More analyses and opinions the better, as it would reduce the reliance on and impact of a handful of analysts and commentators. We need more competition in financial commentary, not less.

PS: The original links are here and here. The fines are likely to be around EUR10,000. Not too high, but still way too much.

Chart Source: Yahoo Finance

French entrepreneurs open a 100% reserve bank

Alright, I wasn’t planning to blog today but I suddenly got overexcited… I don’t know how I missed this news, as it’s been in the French media since June at least, but, well, I did miss it.

While the French government doesn’t like financial innovation, two French entrepreneurs just launched a 100% reserve bank… And this isn’t a tiny event. It’s reported everywhere in the media, for a simple reason: the bank’s cash and dealing machine will be located at the local…….tobacconist.

Yep, that’s right. We all knew that French people liked to smoke, but now, they will even be able to bank while buying cigarettes. A new revolution, I’m telling you.

This new bank is called ‘Compte Nickel’ and will open on the 1st of January 2014, pushed by the national tobacconist federation. The website was launched today. How does it work? Well, it simply works like any 100% reserve bank: it’s some kind of safe in which you deposit your money. Tobacconists open for you a payment account and provide you with an associated debit card. You can transfer money, pay your bills, withdraw money all around Europe and get your salary paid in the account. It’s virtually like a normal bank current account/demand deposit.

What’s the difference then? A (fractional reserve) bank lends out the money deposited in it by its current account customers or invests it in liquid securities to generate interest income. It then often pays an interest on the account as a result and there is no or little charge to maintain the account. Interest rate is usually very low on demand deposits, and virtually non-existent in France. Compte Nickel on the other hand really acts like a safe: the money is not lent out nor invested anywhere. It is simply deposited in Compte Nickel’s Banque de France account.

Consequently, Compte Nickel does not lend. There is no overdraft allowed, no credit card and no credit facilities available. As I said, it is an electronic safe. As the bank still has operating expenses, customers will be charged to maintain the account. This cost is expected to be around EUR34 per year.

It will be a pretty interesting experience to see how people react to that new type of banking, especially given the well-developed anti-bank sentiment in France. 100000 people are expected to sign up during the first year.

If ever this is a successful experience that leads to full reserve banking becoming more widespread, it will raise other questions though: what happens to lending volume in a 100% reserve banking world? It would necessarily decline. I am not saying that this is necessarily a bad thing, and many authors, including Friedman, Rothbard and Fisher have considered the benefits of such a system. On the other hand, other authors (I’m mainly thinking about the so-called ‘Free Bankers’ here), have argued that every time a 100% reserve bank was set up, it always eventually became a fractional reserve one… They also argued that, given the choice between the two models, people would go for a fractional reserve bank. How would the monetary system respond to an increase in money demand? What happens to central banks’ monetary policy? Central banks aren’t required in a full-reserve world…

Banking theorists and historians, get ready!

Update: There might be a few reasons why such an account could indeed attract French customers. As I said above, anti-bank sentiment is one. Many French people think that banks are casinos playing with their money. A second one is that French people already pay a lot of banking charges. French law actually prevented banks to pay interest on current accounts until 2005. There have traditionally been a lot of charges to maintain a current account as a result, which have not disappeared. Yes, once again another regulatory distortion… Therefore, it might not bother customers to be charged for a full reserve bank account (and it does look like normal banks charge more than Compte Nickel!). A simple reason why such a bank might take a while to take off is…. that French customers are often quite conservative and want proven business models.

Photograph: PFG/SIPA

The ‘great search for yield’ update, Taleb on bank disintermediation and Coeuré on Wicksell

This is a quick update on my post of last week on the rush for yield among private investors and what it meant in terms of interest rate disequilibrium.

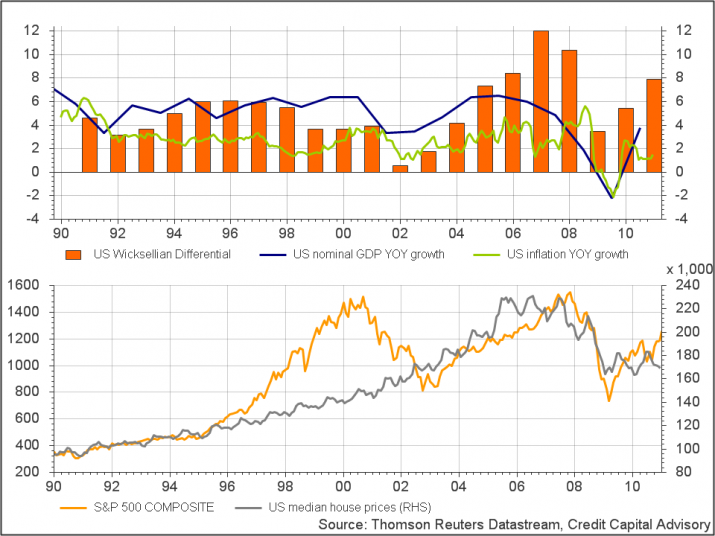

Following my post, Thomas Aubrey from Credit Capital Advisory kindly provided me with an update of his ‘Wicksellian differential’ chart. You can also find it here.

As you can see the differential between the estimated natural rate and the money rate of interest in the US have kept increasing and almost reached pre-crisis peak. According to his calculation, the potential differential now reaches………10%. It’s indeed huge. Try for a second to imagine the Fed all of a sudden increasing their target interest rate by 10%…… No you’re right, we just can’t imagine it. Frankly, I hope his calculation is wrong but…I wouldn’t bet my life on it. Consequently, Thomas Aubrey believes that it backs up my claim about malinvestments.

As you can see the differential between the estimated natural rate and the money rate of interest in the US have kept increasing and almost reached pre-crisis peak. According to his calculation, the potential differential now reaches………10%. It’s indeed huge. Try for a second to imagine the Fed all of a sudden increasing their target interest rate by 10%…… No you’re right, we just can’t imagine it. Frankly, I hope his calculation is wrong but…I wouldn’t bet my life on it. Consequently, Thomas Aubrey believes that it backs up my claim about malinvestments.

Meanwhile, in a speech called ‘The economic consequences of low interest rates’ at the International Center for Monetary and Banking Studies on the 9 October, Benoit Coeuré, member of the Executive Board of the European Central Bank, misunderstood Wicksell and inflation, justifying very low interest rates. Not only Mr Coeuré seems to believe that CPI adequately reflects inflation, but also, according to him, inflation is always zero when the money rate of interest equals the natural rate. This is not true: real shocks can temporarily push inflation one way or another, but over the longer term productivity becomes the main driver behind inflation and deflation. In a world of productivity increases (and increasing output), deflation should be the norm (as it was the case at the end of the 19th century and early 20th). A zero level of inflation in this context would actually mean that there is hidden inflation. George Selgin has written a lot on this. See his Less than Zero book or this video.

Last Friday, FT’s Henny Sender discussed the Fed’s impact on markets. According to a Hong Kong-based hedge fund “the Fed is always there. It is clear that it will not tolerate a decline in asset values. If you sell in the face of QE, you look like an idiot.” Sounds like the best way to completely distort markets. Free markets you said?

Today, John Authers, in another FT piece, says that “Western economy is overcentralised, creating extra risk”. I obviously won’t disagree with him. He cites Nicholas Taleb (reminding me of Larry White). But one thing particularly struck me: Taleb seems to think that hedge funds “are developing strategies that aim to disintermediate the banks, such as loan funds.” This is very, very close to my own opinion, which I haven’t mentioned yet on this blog: technological developments will enable shadow banking to grow under one form or another to desintermediate credit creation. This is something big, and it will require many blog posts and possibly a research paper…and some time.

Nobel Prize in Economics

Today Eugene Fama, Lars Peter Hansen and Robert Shiller share the 2013 The Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel.

While I do not share some of their beliefs (Fama’s efficient market hypothesis based on rational expectations or Shiller’s irrational exuberance are a few examples), I can only but welcome the award of the prize to pro-free markets academics.

Congratulations!

Andy Haldane has a few lessons to teach Adair Turner

Andy Haldane, the Executive Director of Financial Stability at the Bank of England, is possibly one of the most knowledgeable top regulators around. Not only knowledgeable actually. Also modest. What I like in him is that he knows what he doesn’t know. He is the representative of common sense among regulators; it’s almost a pleasure to listen to him. To me, the contrast is sharp between Haldane and Lord Adair Turner, who should probably learn a thing or two from him.

In another (long) remarkable speech given at the Kansas City Fed on 31 August (sorry, I’m only catching up with that now) called ‘The dog and the frisbee‘, he demonstrates again his immense knowledge and modesty. He argues that, often, simple and straightforward rules are much more effective than complex and adaptive rules. Of course, what he targets here is the increasingly large Basel regulatory framework and the risk-weighted assets-based regulatory capital ratios. He many times cites research highlighting how unweighted measures performed better in spotting institutions at risk of collapse.

He based his opinion on his economic beliefs. He and I both disagree with the rational expectations hypothesis, which underlines most modern mainstream economic and finance theory. Financial theory is dominated by the ‘modern portfolio theory’, from which is derived some of the most basic financial tools (Capital Asset Pricing Model for example). I’ll get back to this in another post but the assumptions underlying CAPM/cost of capital and modern portfolio theory in general are highly unrealistic. Yet, few practitioners seem to care. Mathematics has taken over as the only way to describe the world and invest. It looks scientific. So it looks good and must be real.

A crucial point he mentions is that economic agents’ knowledge is limited and imperfect, and that the marginal cost of gathering further data may well outweigh the marginal benefit we get from this supplementary data. Even if all possible information could be gathered, cognitive abilities are limited and we may not be able to accurately process it. Finally, even if we could process it, data changes all the time and our conclusion could already be invalidated when released. This reminds me of some of the arguments developed by Mises and Hayek in the economic calculation problem in a socialist society. Indeed, central regulation of the banking sector effectively equates to partial central planning of the economic system.

Haldane also describes how modern risk-management models have to deal with several million parameters in order to assess various banking and trading risks and accordingly apply risk-weights to calculate regulatory capital ratios. The problem, he says, is that the pre-crisis way of thinking (both from a regulatory and an economic points of view) hasn’t changed: mathematical models have failed so what is needed is even more complex mathematics…

I don’t agree with everything Haldane says though. I don’t see the need to tax complexity or the even simple need for a regulatory leverage ratio for example. Moreover, Haldane himself admitted that both during the Great Depression and during the Great Recession, “the market was leading where regulators had feared to tread”, as banks took corrective measures to reassure investors. So if markets take the necessary measure by themselves and regulators can’t spot crises, why even have them in the first place?

Here are a few selected quotes:

- “No regulator had the foresight to predict the financial crisis, although some have since exhibited supernatural powers of hindsight.”

- “For what this paper explores is why the type of complex regulation developed over recent decades might not just be costly and cumbersome but sub-optimal for crisis control. In financial regulation, less may be more.”

- “Take decision-making in a complex environment. With risk and rational expectations, the optimal response to complexity is typically a fully state-contingent rule. Under risk, policy should respond to every raindrop; it is fine-tuned. Under uncertainty, that logic is reversed. Complex environments often instead call for simple decision rules. That is because these rules are more robust to ignorance. Under uncertainty, policy may only respond to every thunderstorm; it is coarse-tuned.”

- “The general message here is that the more complex the environment, the greater the perils of complex control. The optimal response to a complex environment is often not a fully state-contingent rule. Rather, it is to simplify and streamline.”

- “Strategies that simplify, or perhaps even ignore, statistical weights may be preferable. The simplest imaginable such scheme would be equal-weighting or “tallying”. In complex environments, tallying strategies have been found to be superior to risk-weighted alternatives. “

- “Complex rules may cause people to manage to the rules, for fear of falling foul of them. They may induce people to act defensively, focussing on the small print at the expense of the bigger picture.”

- “Of course, simple rules are not costless. They place a heavy reliance on the judgement of the decision-maker, on picking appropriate heuristics. Here, a key ingredient is the decision-maker’s level of experience, since heuristics are learned behaviours honed by experience.”

- “As of July this year, two years after the enactment of Dodd-Frank, a third of the required rules had been finalised. Those completed have added a further 8,843 pages to the rulebook. At this rate, once completed Dodd-Frank could comprise 30,000 pages of rulemaking. That is roughly a thousand times larger than its closest legislative cousin, Glass-Steagall. Dodd-Frank makes Glass-Steagall look like throat-clearing. The situation in Europe, while different in detail, is similar in substance. Since the crisis, more than a dozen European regulatory directives or regulations have been initiated, or reviewed, covering capital requirements, crisis management, deposit guarantees, short-selling, market abuse, investment funds, alternative investments, venture capital, OTC derivatives, markets in financial instruments, insurance, auditing and credit ratings.These are at various stages of completion. So far, they cover over 2000 pages. That total is set to increase dramatically as primary legislation is translated into detailed rule-writing. For example, were that rule-making to occur on a US scale, Europe’s regulatory blanket would cover over 60,000 pages. It would make Dodd-Frank look like a warm-up Act.”

- “Einstein wrote that: “The problems that exist in the world today cannot be solved by the level of thinking that created them”. Yet the regulatory response to the crisis has largely been based on the level of thinking that created it. The Tower of Basel, like its near-namesake the Tower of Babel, continues to rise.”

The two following quotes highlight how wrong are those who blame the crisis on ‘deregulation’:

- “Today, regulatory reporting is on an altogether different scale. Since 1978, the Federal Reserve has required quarterly reporting by bank holding companies. In 1986, this covered 547 columns in Excel, by 1999, 1,208 columns. By 2011, it had reached 2,271 columns. Fortunately, over this period the column capacity of Excel had expanded sufficiently to capture the increase.”

- “As numbers of regulators have risen, so too have regulatory reporting requirements. In the UK, regulatory reporting was introduced in 1974. Returns could have around 150 entries. […] Today, UK banks are required to fill in more than 7,500 separate cells of data – a fifty-fold rise. Forthcoming European legislation will cause a further multiplication. Banks across Europe could in future be required to fill in 30-50,000 data cells spread across 60 different regulatory forms.”

Photograph: The Times/Chris Harris

The investors’ great search for yield (and the likely collapse?)

Quite a long post… Here I’m going to have to get to the heart of my theoretical economic beliefs. I’ll try to keep it simple and as short as I can though. I will argue that there are many risks to investors going forward due to distortions in interest rates.

I wasn’t surprised yesterday when I read the two following FT articles. The first one tells how leveraged buyouts (LBOs) in the US have boomed recently, with leverage reaching the height of the pre-crisis boom of 5.3 times EBITDA, some even reaching 7.5 times EBITDA. This means that the private equity funds that acquired those firms used debt equivalent to 5 times earnings before depreciation, interest and taxes of the targets to fund the acquisitions. It is a lot. What is usually considered a highly leveraged LBO is around 4 times EBITDA and higher.

The second FT article talks about the fact that hedge funds are struggling to achieve high returns due to the size of the industry. Institutional investors have piled in hedge funds expecting higher returns than what traditional investments yield at the moment.

Earlier this year, we have seen many investors also piling in junk bonds, offering some of the lowest non-investment grade yields on record (despite the economy still not being in great shape and spreads over US treasuries not being at their lowest level ever). What’s going on?

Many people won’t agree with that, but to me, it looks like central banks’ monetary policies (low interest rates, quantitative easing, LTRO, OMT…) are lowering interest rates below their so-called ‘natural rates’. What is the natural rate of interest? It was the Swedish economist Knut Wicksell who came up with this term, highlighting to him the equivalent of the equilibrium free-market rate of interest in a barter world. Wicksell defined the natural rate in those terms in his 1898 book Interest and Prices, chapter 8:

“There is a certain rate of interest on loans which is neutral in respect to commodity prices, and tends neither to raise nor to lower them. This is necessarily the same as the rate of interest which would be determined by supply and demand if no use were made of money and all lending were effected in the form of real capital goods. It comes to much the same thing to describe it as the current value of the natural rate of interest on capital.” (emphasis his)

We can interpret it as the equilibrium interest rate that would exist under free market conditions, with no external interferences such as central banks’ monetary policies and governments’ interest-lowering schemes. In such conditions, intertemporal preferences between savers and borrowers are matched. This natural rate is in opposition to the ‘money rate of interest’, or the actual interest rate prevalent in a money and credit economy. The system is near equilibrium when the natural and the money rates coincide.

At the moment, some people such as Scott Sumner would argue that the natural rate of interest is below zero, justifying massive cash injection in the economy in order to lower the money rate of interest (= nominal interest rate). For him, the evidence is that nominal GDP has been allowed to fall below trend during the crisis and hasn’t recovered since then. While I agree that there was a case for an increase in the quantity of money to counteract a higher demand for money in the earlier stages of the crisis, I don’t believe this is now necessary. (I also believe that ‘trend’ is a very imperfect indicator on which to base policies. NGDP growth trend changed several times since World War 2 and can also be impacted over fairly long periods by unsustainable booms).

But it does continue. There have now been several rounds of QE in the US and monetary easing in Europe, Japan and China, to name a few. So the current situation looks like a sign that the money rate of interest has been pushed below the natural rate for quite some time. While nominal interest rates have been low for a while, real interest rates are now even lower (or even negative). And real interest rates are what investors care about, as it represents the actual gain over cost of life inflation. This has the consequence of pushing investors toward higher-yielding asset classes (hedge funds, private equity, junk bonds, emerging market equities…), in order to generate the returns they normally get on lower-risk assets.

But there is no inflation, you’re going to tell me. True, inflation as measured by CPI has also been relatively low for a while. Is CPI the right measure though? Asset prices (from real estate to equities and bonds) are not reflected in it despite arguably representing a form of inflation. Remember what Wicksell said: “There is a certain rate of interest on loans which is neutral in respect to commodity prices, and tends neither to raise nor to lower them.” Well… It’s clearly not what’s happening now. Even excluding asset classes, CPI may even not accurately reflect goods’ prices inflation. Would investors really need to search for yield if the cost of life actually declined or remained stable?

Does it mean that asset prices should always remain stable at the natural rate? Not at all, and there can be good reasons why asset prices move (real supply shocks for example). But what we can now witness in financial markets look more like malinvestments than anything else. Malinvestments represent bad allocation of capital to investments that would not be profitable under natural rate of interest conditions. As the discount rate on those investments decline in line with the nominal interest rate, they suddenly look attractive from a risk-reward point of view. But what if the discount rate is wrong in the first place? And what if future cash flows are also artificially boosted by low rates? This is a variation of the original Austrian business cycle theory, first developed by Ludwig von Mises and F.A. Hayek early 20th century, and which originally focused on the effects of a distorted interest rate on the structure of production.

Another indication – more scientific than my previous observation – that the money rate may well be below the natural rate, has been devised by a former colleague of mine. Thomas Aubrey published a very interesting book in 2012, Profiting from Monetary Policy, in which he underlines his own calculation of what he calls the ‘Wicksellian differential’ (the difference between the natural and the money rates of interest). He uses estimates of the return on capital and the cost of capital in order to calculate the differential (according to neoclassical economic theory, the real interest rate should equal the marginal product of capital in equilibrium conditions – not everybody agrees though). Using those assumptions, it does look like we have been in a new credit boom since 2010 as you can see from the charts here:

Where does this lead us? Every unsustainable boom has to end at some point. It is likely that as soon as nominal interest rates start rising above a certain level, mark to market losses and worse, outright defaults, will force investors to mark down their holdings of malinvestments. We’ve already recently seen the impact on emerging markets of a mere talk of reducing the pace of quantitative easing.

What could be the consequences? Banks don’t place their liquidity in such risky assets, but might well be exposed to clients that do (many banks provide so-called leveraged loans for instance). Such impact on banks should be relatively limited though, given current regulatory constraints and deleveraging. In turn, this should limit the damage to credit creation and reduce the risk of another monetary contraction through the money multiplier. However, and it is a big question mark, banks might be exposed to companies (and households) under life support from low interest rates. This is more likely to be the case in some countries than others (I’ll let you guess which ones). When rates rise, loan impairment charges may rise quite a lot in those countries.

Private losses (through various types of investment funds and not subject to the money multiplier) may well be large though, negatively affecting private investments for some time afterwards. If you were thinking that the economy was naturally recovering at the moment, you might give it a second thought… Investors, beware, timing will be crucial.

First chart: Wall Street Journal; Second chart: Credit Capital Advisory

Ludwig von Mises’ death

Today is the 40th anniversary of Austrian economist Ludwig von Mises’ death.

I can’t emphasize enough how much Mises has been influential on my way of looking at both economic and social interactions. When I compared his writings to my day to day life as a banks analyst, everything made so much sense… I’ve read several of his books, of which Human Action is one of my favourite. I found myself in agreement with 99% of what I read in it. Believe me, this usually never happens.

He was a true believer in freedom, and was mocked during several decades for predicting the fall of the Soviet Union. A great economist.

Thank you Ludwig.

PS: You can read more about Mises on Free Banking and on the Mises Institute website (also here).

Payday lenders are the new usurers (apparently)

It scares me when I read this: “Today I’m putting payday lenders on notice: tougher regulation is coming and I expect them all to make changes so that consumers get a fair outcome. The clock is ticking.”

It sounds more like an extract from the speech of a populist politician than from the head of the UK-based Financial Conduct Authority.

The FCA is now about to implement ever more intrusive regulation: those bad payday lenders, modern times loan sharks, must be reined in. As a result, we are now witnessing the return of middle-ages usury laws, which sound logical from a moral (or religious) point of view but not much from an economic one.

Under the new proposal, payday lenders will not be able to roll over loans more than twice, cannot try to get their money back more than twice, the FCA can ‘order’ lenders to drop products that are “not in the best interest of consumers”, and borrowers will need to ‘prove’ they can repay the loan.

Most (if not all) those points don’t make much sense. But let me address one particular point: regulators are (as usual?) trying to fix the problem created by other regulations.

I don’t really see the problem with payday lenders. If they exist, it is because there is a market demand for them. If there is a market demand for them, it is because some people are excluded from the traditional financial system as their credit profile is too risky. From this, we can conclude two things: 1. banning or reining in payday lenders will have the only effect or excluding entirely some people from the credit system and 2. asking those people to prove that they can repay is nonsense, as otherwise they wouldn’t have come to a payday lender in the first place as banks would have welcomed that risk-free interest income…

But let’s go back one step. How can there be such a market demand originally? Because banks don’t want to take the risk with those customers anymore. Why don’t they want to take the risk, even if awesomely rewarded? Because they are under pressure from regulation/regulators to de-risk their balance sheet and it has become way too costly as a result… We have another typical example of a morally good action (to make banks safer) that has unintended consequences. Now regulators and politicians are trying to regulate the problems created by the first layer of regulation. I guess in a few years time they will have to add another layer to re-regulate the shortcomings of the current layer… A never-ending story.

Recent Comments