Is the BIS on the Dark Side of macroeconomics?

The BIS has got a hobby: to annoy other economists and central bankers. It’s a good thing. It published its annual report about two weeks ago, and the least we can say is that it didn’t please many.

Gavin Davies wrote a very good piece in the FT last week, summarising current opposite views: “Keynesian Yellen versus Wicksellian BIS”. What’s interesting is that Davies views the BIS as representing the ‘Wicksellian’ view of interest rates: that current interest rates are lower than their natural level (i.e. monetary policy is ‘loose’ or ‘easy’). On the other hand, Scott Sumner and Ryan Avent seem to precisely believe the opposite: that current rates are higher than their natural level and that the BIS is mistaken in believing that low nominal rates mean easy money. This is hard to reconcile both views.

Neither is the BIS particularly explicit. Why does it believe that interest rates are low? Because their headline nominal level is low? Because their real level is low? Or because its own natural rates estimates show that central banks’ rates are low?

It is hard to estimate the Wicksellian ‘natural rate’ of interest. Some people, such as Thomas Aubrey, attempt to estimate the natural rate using the marginal product of capital theory. There are many theories of the rate of interest. Fisher (described by Milton Friedman as America’s best ever economist), Bohm-Bawerk, and Mises would argue that the natural interest rate is defined by time preference (even though they differ on details), and Keynes liquidity preference. Some economists, such as Miles Kimball, currently argue that the natural rate of interest is negative. This view is hard to reconcile with any of the theories listed above. Fisher himself declared in The Rate of Interest that interest rates in money terms cannot be negative (they can in commodity terms).

Unfortunately, and as I have been witnessing for a while now, Wicksell is very often misinterpreted, even by senior economists. The latest example is Paul Krugman, evidently not a BIS fan. Apart from his misinterpretation of Wicksell (see below), he shot himself in the foot by declaring (my emphasis):

Now, what about the BIS? It is arguing that central banks have consistently kept rates too low for the past couple of decades. But this is not a statement about the Wicksellian natural rate. After all, inflation is lower now than it was 20 years ago.

Given that we indeed got two decades of asset bubbles and crashes, it looks to me that the BIS view was vindicated…

Furthermore, in a very good post, Thomas Aubrey corrects some of those misconceptions:

The second issue to note is that when the natural rate is higher than the money rate there is no necessary impact on the general price level. As the Swedish economist Bertie Ohlin pointed in the 1930s, excess liquidity created during a Wicksellian cumulative process can flow into financial assets instead of the real economy. Hence a Wicksellian cumulative process can have almost no discernible impact on the general price level as was seen during the 1920s in the US, the 1980s in Japan and more recently in the credit bubble between 2002-2007.

(Bob Murphy also wrote a very good post here on Krugman vs. Wicksell)

But there are other problematic issues. First, inflation (as defined by CPI/RPI/general increase in the price level) itself is hard to measure, and can be misleading. Second, as I highlighted in an earlier post, wealthy people, who are the ones who own most investible assets, experience higher inflation rates. In order to protect their wealth from declining through negative real returns (what Keynes called the ‘euthanasia of the rentiers’), they have to invest it in higher-yielding (and higher-risk) assets, causing bubbles is some asset classes (while expectations that central bank support to asset prices will remain and allow them to earn a free lunch, effectively suppressing risk-aversion).

If natural rates were negative – or at least very low – and the environment deflationary, it is unlikely that we would witness such hunt for yield: people care about real rates, not nominal ones (though in the short-run, money illusion can indeed prevail). But this is not only an ultra-rich problem: there are plenty of stories of less well-off savers complaining of reduced purchasing power.

Meanwhile, the rest of the population and overleveraged companies, supposedly helped by lower interest rates, seem not to deleverage much: overall debt levels either stagnate or even increase in most economies, as the BIS pointed out.

Banks also suffer from the combination of low rates* and higher regulatory requirements that continue to pressurise their bottom line, and have ceased to pass lower rates on to their customers.

In this context, the BIS seems to have a point: rates may well be too low. Current interest rate levels seem to only prevent the reallocation of capital towards more economically efficient uses, while struggling banks are not able to channel funds to productive companies.

Critics of the BIS point to their call to rise rates to counter inflation back in 2011. Inflation, as conventionally measured, indeed hasn’t stricken in many countries. In the UK and some other European countries though, complaints about quickly rising prices and falling purchasing power have been more than common (and I’m not even referring to house price inflation). This mismatch between aggregate inflation indicators and widespread perception is a big issue, which underlies financial risk-taking.

In the end, Keynes’ euthanasia of the rentiers only seem to prop up dying overleveraged businesses and promote asset bubbles (and financial instability) as those rentiers pile in the same asset classes. I side with the BIS in believing this is not a good and sustainable policy.

I also side with the BIS and with Mohamed El-Erian in believing in the poor forecasting ability of most central bankers, who seem to constantly display a dovish view of the economy, which apparently experiences never-ending ‘slack’, as well as the very uncertain effect of macro-prudential policies, which cannot and will not get in all the cracks. Nevertheless, many mainstream economists and economic publications seem to be overconfident in the effectiveness of macro-prudential policies (see The Economist here, Yellen here, Haldane here, who calls macropru policies “targeted lightning strikes”…).

While central banks’ rates should probably already have risen in several countries (and remain low in others, hence the absurdity of having a single monetary policy for the whole Eurozone), everybody should keep the BIS warnings in mind: after all, they were already warning us before the financial crisis, yet few people listened and many laughed at them.

Unfortunately, politicians and regulators have repeated some of the mistakes made during the Great Depression: they increased regulation of business and banking while the economy was struggling. I have many times referred to the concept of regulatory uncertainty, as well as the over-regulation that most businesses are now subject to (in the US at least, though this is also valid in most European countries). Businesses complaints have been increasing and The Economist reported on that issue last week.

In the meantime, while monetary policy has done (almost) everything it could to boost credit growth and to prevent the money supply from collapsing, harsher banking regulation has been telling banks to do the exact opposite: raise capital, deleverage, and don’t take too much risk.

In the end, monetary policy cannot fix those micro-level issues. It is time to admit that we do not live in the same microeconomic environment as before the crisis. What about cutting red tape to unleash growth rather than risk another financial crisis?

* Yes, for banks, rates are low, whichever way you look at them. Banks can simply not function by earning zero income on their interest-earning assets (loan book and securities portfolio).

PS: Noah Smith, another member of the anti-BIS crowd, has a nonsense ‘let’s keep interest rate low forever’-type article here: raising interest rates would lead to an asset price crash, so we should keep them low to have a crash later. Thanks Noah. The way he describes a speculative bubble is also wrong (my emphasis):

The theory of speculation tells us that bubbles form when people think they can find some greater fool to sell to. But when practically everyone is convinced that asset prices are relatively high, like now, it’s pretty obvious that there aren’t many greater fools out there.

Really? No, speculation involved buying as long as you believe you can get the right timing to exit the position. Even if everyone believed that asset prices were overvalued, as long as investors expect prices to continue to increase, speculation would continue: profits can still be made by exiting on time, even if you join the party late.

PPS: A particularly interesting chart from the BIS report was the one below:

It is interesting to see how coordinated financial cycles have become. Yet the BIS seems not to be able to figure out that its own work (i.e. Basel banking rules) could well be the common denominator of those cycles (which were rarely that synchronised in the past).

It is interesting to see how coordinated financial cycles have become. Yet the BIS seems not to be able to figure out that its own work (i.e. Basel banking rules) could well be the common denominator of those cycles (which were rarely that synchronised in the past).

Blame the rich for the next asset bubble. Or not.

First of all, happy new year to all of you! Fingers crossed we don’t witness another market crash this year! 🙂

Indeed, credit markets are hot. Equity markets are also hot. The FT published an article yesterday with some striking facts about the ‘improvements’ in credit markets over the past couple of years. Some would say that it’s encouraging. I am not convinced…

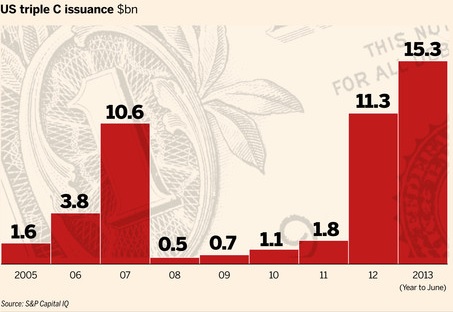

Most credit indicators are close to or above their pre-credit crisis high. Sales of leveraged loans and high-yield bonds are above their pre-crisis peak. The average leverage level of US LBOs is back to 2006 level. Issuance of collateralised loan obligations is close to its pre-crisis peak. Even CCC-rated junk bonds are way above their previous peak. I’ve already mentioned some of those facts a few months ago.

In a relatively recent presentation, Citi’s strategist Hans Lorenzen confirmed the trend: central banks are indirectly suppressing most risky investments’ risk premia. Most investors expect junk bonds’ spreads to tighten further or at least to stabilise at those narrow levels and emerging markets bonds and equities, as well as junk bonds are now among investors’ top asset classes .

My ‘theory’ at the time was that (see also here), if investors were piling in increasingly riskier asset classes, bringing their yield down to record low levels in the process, and nonetheless accepting this level of risk for such low returns, it was because current central bank-defined nominal interest rates were below the Wicksellian natural rate of interest. Inflation, as felt by investors rather than the one reported by national statistics agencies, was higher than most real rates of return on relatively safe assets. In order to see their capital growing (or at least to prevent it from declining), they were forced to pick riskier assets, such as high-yield bonds, which were not really high-yield anymore as a result but remained junk nonetheless. This would result in capital misallocation as, under ‘natural’ interest rate conditions, those investments would have never taken place. Thomas Aubrey’s Wicksellian differential, an indicator of the likely gap between the nominal and the natural rates of interest, was, in line with credit markets, reaching its pre-crisis high and seemed to confirm that ‘theory’.

Well, I now think that not all investors are responsible for what we are witnessing today. The (very) rich are.

This came to my mind some time ago while reading that FT piece by John Authers. This was revealing.

“Their wealth gives them scope to try imaginative investments, but they are terrified of inflation, even as deflation is emerging as a greater risk. That is in part because inflation for the goods and services bought by the very rich is running about 2 percentage points faster than retail inflation as a whole in the UK.” (my emphasis)

In the UK, real gilts’ yields were already in negative territory: adjusted by the (potentially underestimated) consumer price index, gilts were yielding around -1% early 2013. Savers were effectively losing money by investing in those bonds. Now think about the rich: by investing in such bonds, they would get a real return of around -3% instead.

Moreover, “71 per cent of respondents said they were more worried now about a steep rise in inflation than they were five years ago.”

Does it start to make sense? The cost of living I was mentioning earlier is increasing particularly quickly for the rich. And… they are the ones who own most financial assets. In order to offset those rising living costs, they naturally look for higher-yielding investments. And it is exactly what the FT reports:

“Their favourite asset classes for the next three decades are emerging markets equities, developed equities and agricultural land, in that order. Private equity comes close after farmland, while art and collectables were also a more popular asset class than any kind of bonds. […]

Hedge funds, as a group, have not fared well since the crisis. But wealthy investors preoccupied by inflation, and robbed of the easy option of bonds, are evidently disposed to give them a try, with an average projected allocation for the next three decades of 25 per cent. Meanwhile, the chance of a bubble in agricultural land prices, or in art, looks very real.”

Are the rich responsible for our current frothy markets then? Obviously not. They are acting rationally in response to central banks’ policies. Nonetheless, this raises an interesting question. Mainstream economics only considers a high aggregate inflation rate as dangerous. What about ‘class warfare’-type inflation? It does look like inflation experienced by one socioeconomic class could inadvertently lead to asset bubbles and bursts, despite aggregate inflation remaining subdued. This may be another destabilising effect of monetary injections on relative prices.

Granted, central banks possibly are on a Keynesian’s ‘euthanasia of the rentier’-type scheme in order to try to alleviate the pain of over-indebted borrowers (and/or to encourage further lending). But financial repression avoidance might well end-up coming back with a vengeance if savers’ reactions, and in particular, rich savers’, make financial markets bubble and crash.

Charts: FT (link above), Citi and Societé Générale

Cato Institute’s 31st Monetary Conference – Was the Fed a good idea?

About two weeks ago, the US-based think tank Cato organised its annual monetary conference. Great panels and very interesting speeches.

Three panels were of particular interest to me: panel 1 (“100 Years of the Fed: What Have We Learned?”), panel 2 (“Alternatives to Discretionary Government Fiat Money”), panel 3 (“The Fed vs. the Market as Bank Regulator”).

In panel 1, George Selgin destroys the Federal Reserve’s distorted monetary history. Nothing much new in what he says for those who know him but it just never gets boring anyway. He covers: some of the lies that the Federal Reserve tells the general public to justify its existence, pre-WW2 Canada and its better performing monetary system despite not having a central bank, the lack of real Fed independence from political influence and……the Fed not respecting Bagehot’s principles despite claiming to do so. In this panel, the speech of Jerry Jordan, former President of the Federal Reserve Bank of Cleveland, is also very interesting.

In panel 2, Larry White speaks about alternatives to government fiat money, counterfeiting laws and state laws making it illegal to issue private money. Scott Sumner describes NGDP level targeting. Here again, nothing really new for those who follow his blog, but interesting nonetheless (even though I don’t agree with everything) and a must see for those who don’t.

In panel 3, John Allison provides an insider view of regulators’ intervention in banking (he used to be CEO of BB&T, an American bank). He argues that mathematical risk management models provide unhelpful information to bankers. He would completely deregulate banking but increase capital requirements, which is an original position to say the least. Kevin Dowd’s speech is also interesting: he covers regulatory and accounting arbitrage (SPEs, rehypothecation…) and various banking regulations including Basel’s.

Overall, great stuff and you should watch the whole of it (I know, it’s long… you can probably skip most Q&As).

PS: Scott Sumner also commented on the Pope’s speech on “evil incarnate”. Reminds me of the vocabulary I used…

The ivory tower economist syndrome

Here we go. Academic economists are lost. Lawrence Summers just made a striking announcement in a speech a few days ago: we are likely to be in a secularly stagnating economy that needs recurrent bubbles to achieve full employment, as its natural rate of interest has been constantly below zero for a while. Evidently, Krugman, Sumner, Cowen, Wolf and many other economists started to discuss the issue. Some agree, some don’t. However, most seem to miss the main problem. I call that the ivory tower economist syndrome. Abstractly thinking in terms of aggregated economic figures locked in a university or government office won’t be of much help. Zerohedge rightly makes fun of Summers and Krugman, as the satiric newspaper The Onion made the same economic advices a few years ago:

Congress is currently considering an emergency economic-stimulus measure, tentatively called the Bubble Act, which would order the Federal Reserve to† begin encouraging massive private investment in some fantastical financial scheme in order to get the nation’s false economy back on track.

Who said that was fiction?

Many of them are backing their ideas using wrong arguments. For instance, Summers and Krugman don’t believe interest rates were too low before the crisis as… there was no inflation! Sure, but, how do you know that? CPI? RPI? GDP deflator? There are many problems with inflation figures. Let’s list some of them:

- They don’t accurately reflect inflation. You can change the calculation and the result changes dramatically. Moreover, the goods picked to calculate them and the weights applied to them are quite arbitrary. This is supposed to reflect the ‘average’ household basket. Well, I am not the average household apparently as my own inflation rate has been way higher than headline inflation over the past few years.

- 0% CPI increase does not mean that there is no inflation. Productivity increase drives inflation down. As a result, reasoning in terms of headline inflation is a mistake. Real inflation is hidden. The fastest economic growth in the history of the Western world (late 19th and early 20th century) occurred during a long period of secular deflation…

- Most asset prices aren’t reflected in inflation figures. Newly created money now mostly go to investments, a lot of which being speculation. Most of banks’ lending is mortgage lending. So newly-created money goes to housing, pushing up prices… which aren’t reflected in inflation figures. Sure, one can argue that, at some point, there will be inflationary pressure on consumer goods. But productivity increases reducing the price of domestically-produced goods (IT revolution anyone?) and cheap goods from developing countries mask that process. Moreover, when asset bubbles burst (which they eventually do), the wealth effect from asset price increases that could lead to inflation all but disappears. Lending was also different 50 or 100 years ago: much lending did not go directly to investments in financial or real assets. Consequently consumer goods inflation appeared a lot faster after new monetary injection (considering stable productivity).

So justifying the fact that nominal interest rates defined by central banks were not low because there was no inflation is in itself wrong, or at best inaccurate. In reality, low interest rates are very likely to have caused, or at least participated, in the recent credit bubble. Regarding the so-called ‘savings glut’, Cowen agrees with Kling on the fact that, if we really had ‘too much’ savings chasing ‘too few’ investment opportunities, we would not need central banks’ actions to push interest rates lower. The supply and demand of loanable funds would automatically drive the interest rate to a very low level.

But, most importantly, all those economists forget a fundamental fact that I have been mentioning a hundred times recently: regime uncertainty (yes, again…). For economists to speak in terms of monetary and spending aggregates alone and to not pay attention to the broader context surrounding businesses is a major mistake. I’ve kept repeating and giving many evidences recently (like here, here, and here) that businesses currently delay investments due to the uncertain regulatory and economic decisions taken by governments and regulators all around the world. This is now the major issue for SMEs and banks at least. Again today, Euromoney published an interesting short article on ‘renewed regulatory uncertainty’ for banks:

For all the populist fervor then about perceived policy inaction to address systemic risk, many banks see it differently: investor flight from banks’ equity and bond products has taken root over the years, amid fears that new rules will render business models uneconomic.

Take a look at that SEB and Deloitte chart summarising current regulatory reforms. It looks slightly messy doesn’t it? And look how it is named…

A bank analyst told Euromoney that:

Changes in regulations, changes in what other stakeholders consider to be acceptable, the risk that the behaviours of certain employees become associated with the institution as a whole – those are indeed much more expensive for banks these days than credit [risk].

As I have already highlighted in an earlier post, more than the number of rules, it is the fact that rules change that is crucial to business planning. You can’t play a certain game if the rules of the game constantly change. Yet none of those ‘great’ economists ever mentioned regulation, uncertainty, rules or anything related. Looks like abstract economic aggregates are a lot more interesting to manipulate…

Get out of your tower guys!

The ‘great search for yield’ update, Taleb on bank disintermediation and Coeuré on Wicksell

This is a quick update on my post of last week on the rush for yield among private investors and what it meant in terms of interest rate disequilibrium.

Following my post, Thomas Aubrey from Credit Capital Advisory kindly provided me with an update of his ‘Wicksellian differential’ chart. You can also find it here.

As you can see the differential between the estimated natural rate and the money rate of interest in the US have kept increasing and almost reached pre-crisis peak. According to his calculation, the potential differential now reaches………10%. It’s indeed huge. Try for a second to imagine the Fed all of a sudden increasing their target interest rate by 10%…… No you’re right, we just can’t imagine it. Frankly, I hope his calculation is wrong but…I wouldn’t bet my life on it. Consequently, Thomas Aubrey believes that it backs up my claim about malinvestments.

As you can see the differential between the estimated natural rate and the money rate of interest in the US have kept increasing and almost reached pre-crisis peak. According to his calculation, the potential differential now reaches………10%. It’s indeed huge. Try for a second to imagine the Fed all of a sudden increasing their target interest rate by 10%…… No you’re right, we just can’t imagine it. Frankly, I hope his calculation is wrong but…I wouldn’t bet my life on it. Consequently, Thomas Aubrey believes that it backs up my claim about malinvestments.

Meanwhile, in a speech called ‘The economic consequences of low interest rates’ at the International Center for Monetary and Banking Studies on the 9 October, Benoit Coeuré, member of the Executive Board of the European Central Bank, misunderstood Wicksell and inflation, justifying very low interest rates. Not only Mr Coeuré seems to believe that CPI adequately reflects inflation, but also, according to him, inflation is always zero when the money rate of interest equals the natural rate. This is not true: real shocks can temporarily push inflation one way or another, but over the longer term productivity becomes the main driver behind inflation and deflation. In a world of productivity increases (and increasing output), deflation should be the norm (as it was the case at the end of the 19th century and early 20th). A zero level of inflation in this context would actually mean that there is hidden inflation. George Selgin has written a lot on this. See his Less than Zero book or this video.

Last Friday, FT’s Henny Sender discussed the Fed’s impact on markets. According to a Hong Kong-based hedge fund “the Fed is always there. It is clear that it will not tolerate a decline in asset values. If you sell in the face of QE, you look like an idiot.” Sounds like the best way to completely distort markets. Free markets you said?

Today, John Authers, in another FT piece, says that “Western economy is overcentralised, creating extra risk”. I obviously won’t disagree with him. He cites Nicholas Taleb (reminding me of Larry White). But one thing particularly struck me: Taleb seems to think that hedge funds “are developing strategies that aim to disintermediate the banks, such as loan funds.” This is very, very close to my own opinion, which I haven’t mentioned yet on this blog: technological developments will enable shadow banking to grow under one form or another to desintermediate credit creation. This is something big, and it will require many blog posts and possibly a research paper…and some time.

Matthew Klein is drawing the wrong lessons on private currencies

Matthew C. Klein is a columnist for Bloomberg. He used to write on The Economist’s economic blog, Free Exchange. Despite not agreeing with him most of the times, I found that he had some of the most provocative and interesting pieces among the usually quite dull Economist posts. And I used to comment on those pieces. A lot.

He today published a new piece on the Bloomberg website, arguing that the ‘devaluation’ of US-based Southwest Airlines’ frequent flier reward points explains why private currencies (including free banking, Bitcoin and equivalents) have never taken off: they have unstable and unpredictable purchasing power.

His argument is really misguided. Let me explain why.

- First, I would not really call reward points currency. They are media of exchange of very limited use. They are definitely not generally accepted media of exchange (to be honest, Bitcoins aren’t either, as George Selgin explains).

- Bitcoins cannot even lose purchasing power unpredictably: its algorithm has been defined so that new Bitcoins are created following a very steady pattern. So I don’t see why Klein even mentions them…

- Matthew Klein seems to have limited knowledge of banking history: free banking systems have been very stable where and when they existed (White, Selgin, Dowd, Horwitz, and others have published enough on the topic). It is the state that monopolised currency issuance for its own benefits which very often led to financial crises. Currency depreciation has also been much more acute under government’s fiat currency systems.

- Finally – and this is where Klein’s argument really breaks down, the Southwest frequent-flier points devaluation is linked to the devaluation of the dollar! How? Like free banks’ private currency issuance is based on outside money reserve (usually gold or some other commodities), frequent-flier points are also based on another type of outside money (here, the US Dollar) although the analogy is not exact. Basically, every time a customer pays X USD to Southwest, Southwest generates Y reward points. As a result, there is an ex-ante Y/X exchange rate, which is supposed to remain constant over time. Issuing those points is a cost for the company, but which is offset by the potential profit of keeping loyal customers, at this specific exchange rate. When enough reward points have been accumulated, they can then be exchanged for a flight (which are priced in terms of both USD and reward points separately). While Southwest does control the reward points supply, it does not control the outside money supply. And unfortunately, the USD is slowly depreciating thanks to the Fed, thereby increasing the ex-post Y/X exchange rate and the relative purchasing power of the reward points… Like any price, reward points-based prices are sticky, and have to be revaluated over time to reflect the change in the medium of account (which is also USD) that Southwest uses to report its profits. It looks like in this case that reward points-based prices are stickier than USD-based prices, making devaluations both less frequent and sharper in order to catch up with the depreciation of their underlying outside money.

This phenomenon isn’t isolated. My internet monthly bill was recently increased by….25%! I was shocked for a few minutes when I found out. But it is easily explained: internet bills aren’t revaluated every month or even every year, despite the fact that inflation depreciates the currency’s purchasing power every month. At some point, internet firms have to readjust the prices that they charge in order to respond to the increase in their own supply costs and maintain their margins. And when it happens, increases are usually big. This is also valid for many other goods.

So Matt, you’re going to have to find another argument to justify government-controlled currencies!

Recent Comments