The ‘great search for yield’ update, Taleb on bank disintermediation and Coeuré on Wicksell

This is a quick update on my post of last week on the rush for yield among private investors and what it meant in terms of interest rate disequilibrium.

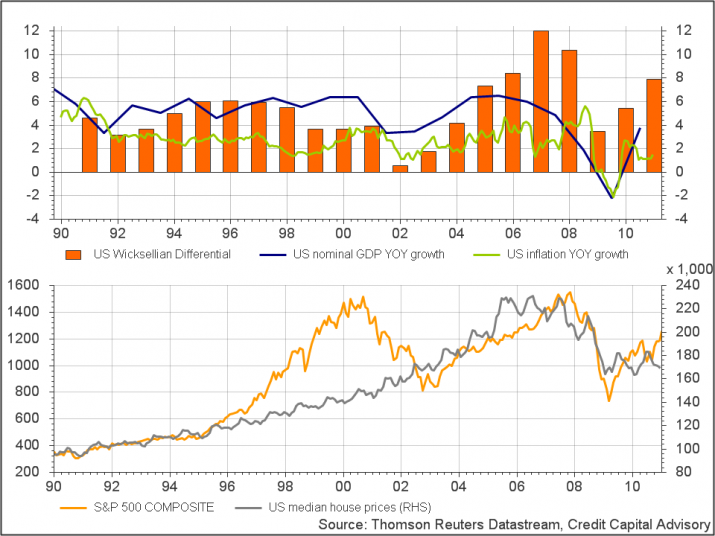

Following my post, Thomas Aubrey from Credit Capital Advisory kindly provided me with an update of his ‘Wicksellian differential’ chart. You can also find it here.

As you can see the differential between the estimated natural rate and the money rate of interest in the US have kept increasing and almost reached pre-crisis peak. According to his calculation, the potential differential now reaches………10%. It’s indeed huge. Try for a second to imagine the Fed all of a sudden increasing their target interest rate by 10%…… No you’re right, we just can’t imagine it. Frankly, I hope his calculation is wrong but…I wouldn’t bet my life on it. Consequently, Thomas Aubrey believes that it backs up my claim about malinvestments.

As you can see the differential between the estimated natural rate and the money rate of interest in the US have kept increasing and almost reached pre-crisis peak. According to his calculation, the potential differential now reaches………10%. It’s indeed huge. Try for a second to imagine the Fed all of a sudden increasing their target interest rate by 10%…… No you’re right, we just can’t imagine it. Frankly, I hope his calculation is wrong but…I wouldn’t bet my life on it. Consequently, Thomas Aubrey believes that it backs up my claim about malinvestments.

Meanwhile, in a speech called ‘The economic consequences of low interest rates’ at the International Center for Monetary and Banking Studies on the 9 October, Benoit Coeuré, member of the Executive Board of the European Central Bank, misunderstood Wicksell and inflation, justifying very low interest rates. Not only Mr Coeuré seems to believe that CPI adequately reflects inflation, but also, according to him, inflation is always zero when the money rate of interest equals the natural rate. This is not true: real shocks can temporarily push inflation one way or another, but over the longer term productivity becomes the main driver behind inflation and deflation. In a world of productivity increases (and increasing output), deflation should be the norm (as it was the case at the end of the 19th century and early 20th). A zero level of inflation in this context would actually mean that there is hidden inflation. George Selgin has written a lot on this. See his Less than Zero book or this video.

Last Friday, FT’s Henny Sender discussed the Fed’s impact on markets. According to a Hong Kong-based hedge fund “the Fed is always there. It is clear that it will not tolerate a decline in asset values. If you sell in the face of QE, you look like an idiot.” Sounds like the best way to completely distort markets. Free markets you said?

Today, John Authers, in another FT piece, says that “Western economy is overcentralised, creating extra risk”. I obviously won’t disagree with him. He cites Nicholas Taleb (reminding me of Larry White). But one thing particularly struck me: Taleb seems to think that hedge funds “are developing strategies that aim to disintermediate the banks, such as loan funds.” This is very, very close to my own opinion, which I haven’t mentioned yet on this blog: technological developments will enable shadow banking to grow under one form or another to desintermediate credit creation. This is something big, and it will require many blog posts and possibly a research paper…and some time.

The investors’ great search for yield (and the likely collapse?)

Quite a long post… Here I’m going to have to get to the heart of my theoretical economic beliefs. I’ll try to keep it simple and as short as I can though. I will argue that there are many risks to investors going forward due to distortions in interest rates.

I wasn’t surprised yesterday when I read the two following FT articles. The first one tells how leveraged buyouts (LBOs) in the US have boomed recently, with leverage reaching the height of the pre-crisis boom of 5.3 times EBITDA, some even reaching 7.5 times EBITDA. This means that the private equity funds that acquired those firms used debt equivalent to 5 times earnings before depreciation, interest and taxes of the targets to fund the acquisitions. It is a lot. What is usually considered a highly leveraged LBO is around 4 times EBITDA and higher.

The second FT article talks about the fact that hedge funds are struggling to achieve high returns due to the size of the industry. Institutional investors have piled in hedge funds expecting higher returns than what traditional investments yield at the moment.

Earlier this year, we have seen many investors also piling in junk bonds, offering some of the lowest non-investment grade yields on record (despite the economy still not being in great shape and spreads over US treasuries not being at their lowest level ever). What’s going on?

Many people won’t agree with that, but to me, it looks like central banks’ monetary policies (low interest rates, quantitative easing, LTRO, OMT…) are lowering interest rates below their so-called ‘natural rates’. What is the natural rate of interest? It was the Swedish economist Knut Wicksell who came up with this term, highlighting to him the equivalent of the equilibrium free-market rate of interest in a barter world. Wicksell defined the natural rate in those terms in his 1898 book Interest and Prices, chapter 8:

“There is a certain rate of interest on loans which is neutral in respect to commodity prices, and tends neither to raise nor to lower them. This is necessarily the same as the rate of interest which would be determined by supply and demand if no use were made of money and all lending were effected in the form of real capital goods. It comes to much the same thing to describe it as the current value of the natural rate of interest on capital.” (emphasis his)

We can interpret it as the equilibrium interest rate that would exist under free market conditions, with no external interferences such as central banks’ monetary policies and governments’ interest-lowering schemes. In such conditions, intertemporal preferences between savers and borrowers are matched. This natural rate is in opposition to the ‘money rate of interest’, or the actual interest rate prevalent in a money and credit economy. The system is near equilibrium when the natural and the money rates coincide.

At the moment, some people such as Scott Sumner would argue that the natural rate of interest is below zero, justifying massive cash injection in the economy in order to lower the money rate of interest (= nominal interest rate). For him, the evidence is that nominal GDP has been allowed to fall below trend during the crisis and hasn’t recovered since then. While I agree that there was a case for an increase in the quantity of money to counteract a higher demand for money in the earlier stages of the crisis, I don’t believe this is now necessary. (I also believe that ‘trend’ is a very imperfect indicator on which to base policies. NGDP growth trend changed several times since World War 2 and can also be impacted over fairly long periods by unsustainable booms).

But it does continue. There have now been several rounds of QE in the US and monetary easing in Europe, Japan and China, to name a few. So the current situation looks like a sign that the money rate of interest has been pushed below the natural rate for quite some time. While nominal interest rates have been low for a while, real interest rates are now even lower (or even negative). And real interest rates are what investors care about, as it represents the actual gain over cost of life inflation. This has the consequence of pushing investors toward higher-yielding asset classes (hedge funds, private equity, junk bonds, emerging market equities…), in order to generate the returns they normally get on lower-risk assets.

But there is no inflation, you’re going to tell me. True, inflation as measured by CPI has also been relatively low for a while. Is CPI the right measure though? Asset prices (from real estate to equities and bonds) are not reflected in it despite arguably representing a form of inflation. Remember what Wicksell said: “There is a certain rate of interest on loans which is neutral in respect to commodity prices, and tends neither to raise nor to lower them.” Well… It’s clearly not what’s happening now. Even excluding asset classes, CPI may even not accurately reflect goods’ prices inflation. Would investors really need to search for yield if the cost of life actually declined or remained stable?

Does it mean that asset prices should always remain stable at the natural rate? Not at all, and there can be good reasons why asset prices move (real supply shocks for example). But what we can now witness in financial markets look more like malinvestments than anything else. Malinvestments represent bad allocation of capital to investments that would not be profitable under natural rate of interest conditions. As the discount rate on those investments decline in line with the nominal interest rate, they suddenly look attractive from a risk-reward point of view. But what if the discount rate is wrong in the first place? And what if future cash flows are also artificially boosted by low rates? This is a variation of the original Austrian business cycle theory, first developed by Ludwig von Mises and F.A. Hayek early 20th century, and which originally focused on the effects of a distorted interest rate on the structure of production.

Another indication – more scientific than my previous observation – that the money rate may well be below the natural rate, has been devised by a former colleague of mine. Thomas Aubrey published a very interesting book in 2012, Profiting from Monetary Policy, in which he underlines his own calculation of what he calls the ‘Wicksellian differential’ (the difference between the natural and the money rates of interest). He uses estimates of the return on capital and the cost of capital in order to calculate the differential (according to neoclassical economic theory, the real interest rate should equal the marginal product of capital in equilibrium conditions – not everybody agrees though). Using those assumptions, it does look like we have been in a new credit boom since 2010 as you can see from the charts here:

Where does this lead us? Every unsustainable boom has to end at some point. It is likely that as soon as nominal interest rates start rising above a certain level, mark to market losses and worse, outright defaults, will force investors to mark down their holdings of malinvestments. We’ve already recently seen the impact on emerging markets of a mere talk of reducing the pace of quantitative easing.

What could be the consequences? Banks don’t place their liquidity in such risky assets, but might well be exposed to clients that do (many banks provide so-called leveraged loans for instance). Such impact on banks should be relatively limited though, given current regulatory constraints and deleveraging. In turn, this should limit the damage to credit creation and reduce the risk of another monetary contraction through the money multiplier. However, and it is a big question mark, banks might be exposed to companies (and households) under life support from low interest rates. This is more likely to be the case in some countries than others (I’ll let you guess which ones). When rates rise, loan impairment charges may rise quite a lot in those countries.

Private losses (through various types of investment funds and not subject to the money multiplier) may well be large though, negatively affecting private investments for some time afterwards. If you were thinking that the economy was naturally recovering at the moment, you might give it a second thought… Investors, beware, timing will be crucial.

First chart: Wall Street Journal; Second chart: Credit Capital Advisory

Recent Comments