A clarification on mortgage rates for ASI’s Ben Southwood

Ben Southwood from the Adam Smith Institute replied to my previous post here. I am still confused about Ben’s claim that the spread varied “widely”. As the following chart demonstrates, the margins of SVR, tracker and total floating lending over the BoE base rate remained remarkably stable between 1998 and 2008, despite the BoE rate varying from a high 7.5% in 1998 to a low of 3.5% in 2003:

Everything changed in 2009 when the BoE rate collapsed to the zero lower bound. Following his comments, I think I need to address a couple of things. Two particular points attracted my attention. Ben said:

If other Bank schemes, like Funding for Lending or quantitative easing were overwhelming the market then we’d expect the spread to be lower than usual, not much higher.

His second big point, that the spread between the Bank Rate and the rates banks charged on markets couldn’t narrow any further 2009 onwards perplexes me. On the one hand, it is effectively an illustration of my general principle that markets set rates—rates are being determined by banks’ considerations about their bottom line, not Bank Rate moves. On the other hand, it seems internally inconsistent. If banks make money (i.e. the money they need to cover the fixed costs Julien mentions) on the spread between Bank Rate and mortgage rates (i.e. if Bank Rate is important in determining rates, rather than market moves) then the absolute levels of the numbers is irrelevant. It’s the spread that counts.

It looks to me that we are both misunderstanding each other here. It is indeed the spread that counts. But the spread over funding (deposit) cost, not BoE rate! (Which seems to me to be consistent with my posts on MMT/endogenous money.) Let me clarify my argument with a simple model.

Assumptions:

- A medium-size bank’s only assets are floating rate mortgages (loan book of GBP1bn). Its only source of revenues is interest income. The bank maintains a fixed margin of 1% above the BoE rate but keeps the right to change it if need be.

- The bank’s funding structure is composed only of demand deposits, for which the bank does not pay any interest. As a result, the bank has no interest expense.

- The bank has a 100% loan/deposit ratio (i.e. the bank has ‘lent out’ the whole of its deposit base and therefore does not hold any liquid reserve).

- The bank has an operational cost base of GBP20m that is inflexible in the short-term (not in the long-term though there are upwards and downwards limits) and no loan impairment charge.

Of course this situation is unrealistic. A 100% loan/deposit bank would necessarily have some sort of wholesale funding as it needs to maintain some liquidity. It would also very likely have a more expensive saving deposit base and some loan impairment charges. But the mechanism remains the same therefore those details don’t matter.

In order to remain profitable, the bank’s interest income has to be superior to its cost base. Moreover, the bank’s interest income is a direct, linear function, of the BoE rate. The higher the rate, the higher the income and the higher the profitability. As a result, the bank’s profitability obeys the following equation:

Net Profit = Interest Income – Costs = f(BoE rate) – Costs,

with f(BoE rate) = BoE rate + margin = BoE rate + 1%.

Consequently, in order for Net Profit > 0, we need f(BoE rate) > Costs.

Now, we know that the bank’s cost base is GBP20m. The bank must hence earn more than GBP20m on its loan book to remain profitable (which does not mean that it is enough to cover its cost of capital).

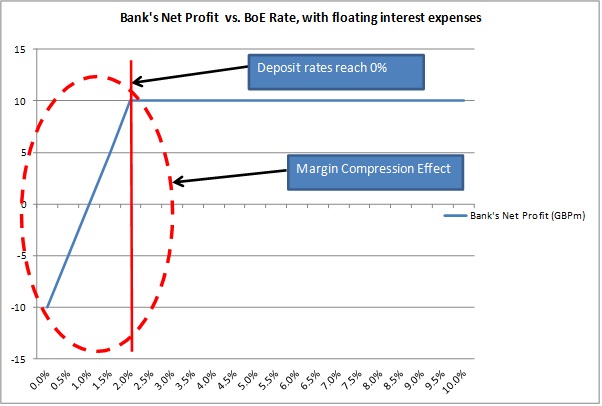

The BoE rate is 2%, making the rate on the mortgage book of the bank 3%, leading to a GBP30m income and a GBP10m net profit. Almost overnight, the BoE lowers its rate to 0.5%. The bank’s loan book’s average rate is now 1.5%, and generates GBP15m of income. The bank is now making a GBP5m loss. Having inflexible short-term costs, it’s only way of getting back to profitability is to increase its margin by at least 0.5%. The bank’s net profit profile is summarised by the following chart:

However, a more realistic bank would pay interest on its deposit base (its funding). Let’s now modify our assumptions and make that same bank entirely demand deposit-funded, remunerated at a variable rate. The bank pays BoE rate minus a fixed 2% margin on its deposit base. As a result, what needs to cover the banks operational costs isn’t interest income but net interest income. The bank’s net profit equation is now altered in the following way:

Net Profit = Net Interest Income – Costs

Net Profit = Interest Income – Interest Expense – Costs

Net Profit = f1(BoE rate) – f2(BoE rate) – Costs

with f1(BoE rate) = BoE rate + margin = BoE rate + 1%,

and f2(BoE rate) = BoE rate – margin = BoE rate – 2%.

The equation can be reduced to: Net Profit = 3% (of its loan book) – Costs, as long as BoE rate >= 2% (see below).

Let’s illustrate the net profit profile of the bank with the below chart:

What happens is clear. Independently of its effects on the demand for credit and loan defaults, the BoE rate level has no effect on the bank’s profitability. Everything changes when deposit rates reach the zero lower bound (i.e. there is no negative nominal rate on deposits), which occurs before the BoE rate reaches it. From this point on, the bank’s interest income decreases despite its funding cost unable to go any lower. This is the margin compression effect that I described in my first post. In reality, things obviously aren’t that linear but follow the same pattern nevertheless.

Realistic banks are also funded with saving deposits and senior and subordinated debt, on which interest expenses are higher. This is when schemes such as the Funding for Lending Scheme kicks in, by providing cheaper-than-market funding for banks, in order to reduce the margin compression effect. The other way to do it is to reflect a rate rise in borrowers’ cost, while not increasing deposit rates. This is highly likely to happen, although I guess that banks would only partially transfer a rate hike in order not to scare off customers.

Overall, we could say that markets determine mortgage rates to an extent. But this is only due to the fact that banks have natural (short-term) limits under which they cannot go. It would make no sense for banks not to earn a single penny on their loan book (and they would go bust anyway). Beyond those limits, the BoE still determines mortgage rates.

Although I am going to qualify this assertion: the BoE roughly determines the rate and markets determine the margin. At a disaggregated level, banks still compete for funding and lending. They determine the margins above and below the BoE rate in order to maximise profitability. They, for instance, also have to take into account the fact that an increase in the BoE rate might reduce the demand for credit, thereby not reflecting the whole increase/decrease to customers as long as it still boosts their profitability. Those are some of the non-linear factors I mentioned above. But they remain relatively marginal and the aggregate, competitively-determined, near-equilibrium margin remains pretty stable over time as demonstrated with the first chart above.

With this post I hope to have clarified the mechanism I relied on in my previous post, but feel free to send me any question you may have!

Mortgage rates are still determined by the BoE

Ben Southwood from the Adam Smith Institute wrote an interesting piece this week. I have an objection to his title and the conclusion he reached. Ben wrote:

However, it was recently pointed out to me that since a high fraction of UK mortgages track the Bank of England’s base rate, a jump in rates, something we’d expect as soon as UK economic growth is back on track, could make mortgages much less affordable, clamping down on the demand for housing.

This didn’t chime with my instincts—it would be extremely costly for lenders to vary mortgage rates with Bank Rate so exactly while giving few benefits to consumers—so I set out to check the Bank of England’s data to see if it was in fact the case. What I found was illuminating: despite the prevalence of tracker mortgages the spread between the average rate on both new and existing mortgage loans and Bank Rate varies drastically.

Wait. I really don’t reach the same conclusion from the same dataset. This is what I extracted from the BoE website (using the BoE’s old reporting format, as the new one only started in 2011):

Banks and building societies offer two main types of floating rate mortgages: standard variable rate (SVR) and trackers. Trackers usually follow the BoE rate closely. SVR are slightly different: margins above the BoE rate are more flexible. Banks vary them to manage their revenues but usually fix them for an extended period of time before reviewing them again. During the crisis, some banks that had vowed to maintain their SVR at a certain spread angered their customers when this situation became unsustainable due to low base rates. Some banks and building societies made losses on their SVR portfolio as a result and had to break their promise and increase their SVR.

What we can notice from the chart above is clear: since the mid-1990s, it is the BoE that determine both mortgage and deposit rates. Not the market. All rates moved in tandem with the BoE base rate. Still, the linkage was broken when the BoE rate collapsed to the zero lower bound in 2009. And this is probably why Ben declared that

but what is clear is that tracker mortgages be damned, interest rates are set in the marketplace.

I think this is widely exaggerated. Ben missed something crucial here: banks have fixed operational costs. Banks generate income by earning a margin between their interest income (from loans) and interest expense (from deposits and other sources of funding). They usually pay demand deposits below the BoE rate and saving/time deposits at around the BoE rate, and make money by lending at higher rates. From this net interest income, banks have to deduce their fixed costs (salaries and other administrative expenses) and bad debt provisions.

There is a problem though. Setting the BoE rate near zero involves margin compression. Banks’ back books (lending made over the previous years) on variable rates see their interest income collapse. Banks’ deposit base is stickier: many saving accounts are not on variable rates. Therefore, there is a time lag before the deposit base reprice (we can see this on the chart above: whereas lending reprices instantaneously when the BoE rate moves, deposits show a lag). Moreover, near the zero bound, the spread between demand deposit rates and the BoE rates all but disappears. The two following charts clearly illustrate this margin compression phenomenon:

It is clear that banks started to make losses when the BoE rate fell, as the margin on the floating rate back book (stock) became negative. Using the new BoE reporting would make those margins look even worse*. To offset those losses, banks started to increase the spread on new lending, leading to a spike on the interest margin of the front book (green line above). Banks can potentially reprice their whole loan book at a higher margin, but this takes time, especially with 15 to 30-year mortgages. Consequently, banks not only increased the spread on new lending, but also decided to break their SVR promises and increase their back book SVR rates (see black line in charts). This usually did not go down well with their customers, but some banks had no choice, having entered the crisis with too low SVRs.

What happens to a bank whose net interest income is negative (assuming it has no other income source)? It reports net accounting losses as it still has fixed operational expenses… Continuously depressed margins explain why banks’ RoE remains low. For banks to report net profits, their net interest income must cover (at least) both operational expenses and loan impairment charges. What Ben identified as ‘market-defined interest rates’ or the ‘spread over BoE’s rate’ from 2009 onwards is simply the floor representing banks’ operational costs, under which banks cannot go… The only other (and faster) way to rebuild banks’ bottom line would be to increase the BoE rate.

A mystery though: why didn’t banks decrease their time deposit rates further? I am unsure to have an answer to that question. A possibility is that the spread between demand and time deposits remained the same. Another possibility is that banks’ time deposit rates remained historically roughly in line with UK gilts rates. Decreasing time deposit rates much below those of gilts would provide savers with incentives to invest their money in gilts rather than in banks’ saving accounts.

What would a rate hike mean? Ben thinks it would have little impact, probably because the spread over BoE seems to show quite a lot of breathing space before the base rate impacts lending rates. I don’t think this is the case. A rate increase would likely push lending rates upwards on bank’s back book (i.e. banks are not going to reduce the spread in order to maintain stable mortgage rates). Why? Banks’ net interest margin and return on equity are still very depressed. Moreover, new Basel III regulations are forcing banks to hold more equity, further reducing RoE. Consequently, banks will seek to rebuild their margin and profitability, making customers pay higher rates to compensate for years of low rates and newly-introduced regulatory measures.

* I am unsure why the BoE changed its reporting and what the differences are, but reported lending rates are much lower than with the old reporting standards. Tracker mortgage rates even seem to be lower than time deposit rates. See below and compare with my first chart. If anybody has an explanation, please enlighten me:

Update: I replaced ‘ceiling’ with ‘floor’ in the post as it makes a lot more sense!

Update 2: Ben Southwood replies here…

Update 3: …and I replied there!

A UK housing bubble? Sam Bowman doubts it

On the Adam Smith Institute’s blog, Sam Bowman had a couple of posts (here and a follow-up here, and mentioned by Lars Christensen here) attempting to explain that there might not have been any house price bubble in the UK. He essentially says that there was no oversupply of housing in the 1990s and 2000s. Here’s Sam:

These charts show that housing construction was actually well below historical levels in the 1990s and 2000s, both in absolute terms and relative to population. It is difficult to see how someone could claim that the 2008 bust was caused by too many resources flowing toward housing and subsequently needing time to reallocate if there was no bubble in housing to begin with.

What this suggests is that the Austrian story about the crisis may be wrong in the UK (and, if Nunes’s graphs are right, the US as well). The Hayek-Mises story of boom and bust is not just about rises in the price of housing: it is about malinvestments, or distortions to the structure of production, that come about when relative prices are distorted by credit expansion.

Well, I think this is not that simple. Let me explain.

First, the Hayek/Mises theory does not apply directly to housing. In the UK, there are tons of reasons, both physical and legal, why housing supply is restricted. As a result, increased demand does not automatically translate into increased supply, unlike in Spain, which seems to have lower restrictions as shown by the housing start chart below:

Second, Sam overlooks what happened to commercial real estate. There was indeed a CRE boom in the UK and CRE was the main cause of losses for many banks during the crisis (unlike residential property, whose losses remained relatively limited).

Third, the UK is also characterised by a lot of foreign buyers, who do not live in the UK and hence not included in the population figures. Low rates on mortgages help them purchase properties, pushing up prices, triggering a reinforcing trend while supply in the demanded areas often cannot catch up.

Fourth, the impact of Basel regulations seems to be slightly downplayed. Coincidence or not, the first ‘bubble’ (in the 1980s) appeared right when Basel’s Risk Weighted Assets were introduced. And it is ‘curious’, to say the least, that many countries experienced the same trend at around the same time. Would house lending and house prices have increased that much if those rules had never been implemented? I guess not, as I have explained many times. I have yet to write posts on what happened in several countries. I’ll do it as soon as I find some time.

I recommend you to take a look at my RWA-based Austrian Business Cycle Theory, which seems to show that, while there should indeed be long-term real estate projects started (depending on local constraints of course), there is also an indirect distortion of the capital structure of the non-real estate sector.

While there may well be ‘real’ factors pushing up real estate prices in the UK, there also seems to be regulatory and monetary policy factors exacerbating the rise.

- Chart 1: Spanish Property Insight

- Chart 2: FT Alphaville

- Chart 3: Guardian

Blame the rich for the next asset bubble. Or not.

First of all, happy new year to all of you! Fingers crossed we don’t witness another market crash this year! 🙂

Indeed, credit markets are hot. Equity markets are also hot. The FT published an article yesterday with some striking facts about the ‘improvements’ in credit markets over the past couple of years. Some would say that it’s encouraging. I am not convinced…

Most credit indicators are close to or above their pre-credit crisis high. Sales of leveraged loans and high-yield bonds are above their pre-crisis peak. The average leverage level of US LBOs is back to 2006 level. Issuance of collateralised loan obligations is close to its pre-crisis peak. Even CCC-rated junk bonds are way above their previous peak. I’ve already mentioned some of those facts a few months ago.

In a relatively recent presentation, Citi’s strategist Hans Lorenzen confirmed the trend: central banks are indirectly suppressing most risky investments’ risk premia. Most investors expect junk bonds’ spreads to tighten further or at least to stabilise at those narrow levels and emerging markets bonds and equities, as well as junk bonds are now among investors’ top asset classes .

My ‘theory’ at the time was that (see also here), if investors were piling in increasingly riskier asset classes, bringing their yield down to record low levels in the process, and nonetheless accepting this level of risk for such low returns, it was because current central bank-defined nominal interest rates were below the Wicksellian natural rate of interest. Inflation, as felt by investors rather than the one reported by national statistics agencies, was higher than most real rates of return on relatively safe assets. In order to see their capital growing (or at least to prevent it from declining), they were forced to pick riskier assets, such as high-yield bonds, which were not really high-yield anymore as a result but remained junk nonetheless. This would result in capital misallocation as, under ‘natural’ interest rate conditions, those investments would have never taken place. Thomas Aubrey’s Wicksellian differential, an indicator of the likely gap between the nominal and the natural rates of interest, was, in line with credit markets, reaching its pre-crisis high and seemed to confirm that ‘theory’.

Well, I now think that not all investors are responsible for what we are witnessing today. The (very) rich are.

This came to my mind some time ago while reading that FT piece by John Authers. This was revealing.

“Their wealth gives them scope to try imaginative investments, but they are terrified of inflation, even as deflation is emerging as a greater risk. That is in part because inflation for the goods and services bought by the very rich is running about 2 percentage points faster than retail inflation as a whole in the UK.” (my emphasis)

In the UK, real gilts’ yields were already in negative territory: adjusted by the (potentially underestimated) consumer price index, gilts were yielding around -1% early 2013. Savers were effectively losing money by investing in those bonds. Now think about the rich: by investing in such bonds, they would get a real return of around -3% instead.

Moreover, “71 per cent of respondents said they were more worried now about a steep rise in inflation than they were five years ago.”

Does it start to make sense? The cost of living I was mentioning earlier is increasing particularly quickly for the rich. And… they are the ones who own most financial assets. In order to offset those rising living costs, they naturally look for higher-yielding investments. And it is exactly what the FT reports:

“Their favourite asset classes for the next three decades are emerging markets equities, developed equities and agricultural land, in that order. Private equity comes close after farmland, while art and collectables were also a more popular asset class than any kind of bonds. […]

Hedge funds, as a group, have not fared well since the crisis. But wealthy investors preoccupied by inflation, and robbed of the easy option of bonds, are evidently disposed to give them a try, with an average projected allocation for the next three decades of 25 per cent. Meanwhile, the chance of a bubble in agricultural land prices, or in art, looks very real.”

Are the rich responsible for our current frothy markets then? Obviously not. They are acting rationally in response to central banks’ policies. Nonetheless, this raises an interesting question. Mainstream economics only considers a high aggregate inflation rate as dangerous. What about ‘class warfare’-type inflation? It does look like inflation experienced by one socioeconomic class could inadvertently lead to asset bubbles and bursts, despite aggregate inflation remaining subdued. This may be another destabilising effect of monetary injections on relative prices.

Granted, central banks possibly are on a Keynesian’s ‘euthanasia of the rentier’-type scheme in order to try to alleviate the pain of over-indebted borrowers (and/or to encourage further lending). But financial repression avoidance might well end-up coming back with a vengeance if savers’ reactions, and in particular, rich savers’, make financial markets bubble and crash.

Charts: FT (link above), Citi and Societé Générale

Banks’ RWAs as a source of malinvestments – Some recent empirical evidence

A recent study by academics from the Southern Methodist University and the Wharton School of the University of Pennsylvania had very interesting findings (the actual full paper can be found here): banks based near booming housing markets charged higher interest rates and reduced loan amounts to companies, which ended up investing less than companies borrowing from banks located in stable (or falling) housing markets. They called this the “crowding-out effect of house-price appreciation”. The study gathered data from 1988 to 2006 in the US, during the Basel period. It would have been interesting to compare with the pre-Basel era and replicate it with European markets.

Conventional economic knowledge seemed to think that “to the extent that home prices begin to rise, consumers will feel wealthier; they’ll feel more disposed to spend…that’s going to provide the demand that firms need in order to be willing to hire and to invest.” (This is Ben Bernanke as quoted by The Economist, which mentioned this study a few weeks ago)

But our academics instead found an inverse relationship:

We estimate that a one standard-deviation increase in housing prices (about $79,700 in year 2000 dollars) that a bank is exposed to decreases investment by firms related to that bank by almost 6.3 percentage points, which is approximately 12% of a standard deviation for firm investment. Banks also increase the interest rate charged by 9 basis points, reduce outstanding loans by approximately 9%, and reduce loan size by approximately 4.5%. These results are consistent with banks reducing the supply of capital to firms in response to increased housing prices.

So much for the Keynesianism of housing bubbles…

Their findings was summarised in an easier to read single chart by The Economist:

I think they are spot on in identifying this crowding out effect but overlook the underlying importance of Basel’s risk-weighted assets in triggering the boom and forcing the reallocation of capital towards housing. In their paper, there is not a single reference to Basel, banks’ capital requirements (apart from one related to MBS) and RWAs. But their story matches almost perfectly the RWA-based ABCT model I described in my previous post on the topic.

What did my model say? That the supply of loanable funds would be reduced to businesses and increased to real estate as a result of capital-optimising choices made by banks (because of RWAs capital constraints). That consequently, interest rates would increase for businesses and be reduced for real estate. This is exactly what they found.

But it doesn’t stop here. The model also said that an increase in interest rates to businesses would shorten their structure of production as interest-sensitive long-term investments become unprofitable. What did they find? That businesses reduced investments despite the temporary boost in consumption due to the well-referenced wealth effects (which they also mentioned)…

However, they missed the deeper implications of banking regulation on the reallocation of capital from businesses to real estate. To them, house price increases seems to be the only factor diverting capital towards housing. I don’t deny that increasing house prices would bring about self-reinforcing house lending, even in a free market: as house prices increase, lending gets facilitated and speculators are attracted, pushing prices up even further. But my point is that regulation and RWAs can both trigger and exacerbate the process way beyond the self-correcting point at which it would normally stop (and collapse) in a free market environment.

There is catch though… If RWAs do indeed trigger a boom in house lending, how could they find some areas in the US within which the process actually wasn’t triggered (no increase in house prices/lending) despite being subject to the same regulatory framework? Well, there are possibly a few answers to that question. Some local banks could actually be in an area experiencing falling house prices for some reason (even though they increase nationally) and low mortgage demand. This would automatically limit the amount they lend and push RWAs on real estate up, making housing less attractive from a capital-optimisation point of view. Another possibility would be that those local banks are actually subsidiaries of other banks that try to optimise capital usage on an aggregate (national) basis. However, it is hard to say as the criteria used to build the sample of banks are not clear.

There is another, simpler, possible explanation: even in falling housing prices areas, local banks’ business lending was still constrained and mortgage lending still supported! Meaning that, in a RWA-free world (and excluding a recessionary environment), a decline in housing prices would have triggered an even sharper decrease/increase in mortgage/business lending. This cannot be proved with this study however. There could also be other explanations that haven’t come to my mind yet.

Overall, I remain slightly sceptical of statistical/regression/correlation-based economic studies and I’ll take this one with a pinch of salt, especially as they use various assumptions and proxies that could easily distort the outcome. Nonetheless, the results they obtained were quite significant. And they provide some empirical evidences to my very theoretical model.

Meanwhile, Nouriel Roubini on Friday, in a piece called Back to Housing Bubbles, listed all the markets in which there are signs of bubbles:

[…] signs of frothiness, if not outright bubbles, are reappearing in housing markets in Switzerland, Sweden, Norway, Finland, France, Germany, Canada, Australia, New Zealand, and, back for an encore, the UK (well, London). In emerging markets, bubbles are appearing in Hong Kong, Singapore, China, and Israel, and in major urban centers in Turkey, India, Indonesia, and Brazil.

Real estate bubbles existed before Basel introduced risk-weighted assets, but nothing on that scale and in so many countries at the same time. Time for policy-makers to wake up.

RWA-based ABCT Series:

- Banks’ risk-weighted assets as a source of malinvestments, booms and busts

- Banks’ RWAs as a source of malinvestments – Update

- Banks’ RWAs as a source of malinvestments – A graphical experiment

- Banks’ RWAs as a source of malinvestments – Some recent empirical evidence

- A new regulatory-driven housing bubble?

Cato Institute’s 31st Monetary Conference – Was the Fed a good idea?

About two weeks ago, the US-based think tank Cato organised its annual monetary conference. Great panels and very interesting speeches.

Three panels were of particular interest to me: panel 1 (“100 Years of the Fed: What Have We Learned?”), panel 2 (“Alternatives to Discretionary Government Fiat Money”), panel 3 (“The Fed vs. the Market as Bank Regulator”).

In panel 1, George Selgin destroys the Federal Reserve’s distorted monetary history. Nothing much new in what he says for those who know him but it just never gets boring anyway. He covers: some of the lies that the Federal Reserve tells the general public to justify its existence, pre-WW2 Canada and its better performing monetary system despite not having a central bank, the lack of real Fed independence from political influence and……the Fed not respecting Bagehot’s principles despite claiming to do so. In this panel, the speech of Jerry Jordan, former President of the Federal Reserve Bank of Cleveland, is also very interesting.

In panel 2, Larry White speaks about alternatives to government fiat money, counterfeiting laws and state laws making it illegal to issue private money. Scott Sumner describes NGDP level targeting. Here again, nothing really new for those who follow his blog, but interesting nonetheless (even though I don’t agree with everything) and a must see for those who don’t.

In panel 3, John Allison provides an insider view of regulators’ intervention in banking (he used to be CEO of BB&T, an American bank). He argues that mathematical risk management models provide unhelpful information to bankers. He would completely deregulate banking but increase capital requirements, which is an original position to say the least. Kevin Dowd’s speech is also interesting: he covers regulatory and accounting arbitrage (SPEs, rehypothecation…) and various banking regulations including Basel’s.

Overall, great stuff and you should watch the whole of it (I know, it’s long… you can probably skip most Q&As).

PS: Scott Sumner also commented on the Pope’s speech on “evil incarnate”. Reminds me of the vocabulary I used…

Banks’ RWAs as a source of malinvestments – A graphical experiment

Today is going to be experimental and theoretical. I have already outlined the principles behind the RWA-based variation of the Austrian Business Cycle Theory (ABCT), which was followed by a quick clarification. I am now attempting to come up with a graphical representation to illustrate its mechanism. In order to do that, I am going to use Roger Garrison’s capital structure-based macroeconomics representations used in his book Time and Money: The Macroeconomics of Capital Structure. I am not saying that what I am about to describe is 100% right. Remember that this remains an experiment that I just wrote down over those last few days and that needs a lot more development. There may well also be other ways of depicting the impacts that Basel regulation’s RWAs have on the capital structure and malinvestments. Completely different analytical frameworks might also do. Comments and suggestions are welcome.

This is what Garrison’s representation of the macroeconomics of capital structure looks like:

It is composed of three elements:

- Bottom right: this is the traditional market for loanable funds, where the supply and demand for loanable funds cross at the natural rate of interest. It represents economic agents’ intertemporal preferences: the higher they value future goods over present goods, the more they save and the lower the interest rate. The x-axis represents the quantity of savings supplied (and investments) and the y-axis represents the interest rate.

- Top right: this is the production-possibility frontier (PPF). In Garrison’s chart, it represents the sustainable trade-off between consumption and gross investment. Only movements along the frontier are sustainable and supposed to reflect economic agents’ preferences. Positive net investments and technological shocks expand the frontier as the economy becomes more productive.

- Top left: this is the Hayekian triangle. It represents the various stages of production (each adding to output) within an industry. See details below:

I don’t have time to come back to the original ABCT and those willing to find out more about it can find plenty of examples online. Today I wish only to try to understand the impact of regulatory-defined risk-weighted assets on this structure. Ironically, it becomes necessary to disaggregate the Austrian capital-based framework to understand the mechanics and distortions leading to a likely banking crisis. In everything that follows, and unlike in the original Austrian theory, we exclude central banks from the picture (i.e. no monetary injection). We instead focus only on monetary redistribution. The story outlined below does not explain the financial crisis by itself. Rather, it outlines a regulatory mechanism that exacerbated the crisis.

I don’t have time to come back to the original ABCT and those willing to find out more about it can find plenty of examples online. Today I wish only to try to understand the impact of regulatory-defined risk-weighted assets on this structure. Ironically, it becomes necessary to disaggregate the Austrian capital-based framework to understand the mechanics and distortions leading to a likely banking crisis. In everything that follows, and unlike in the original Austrian theory, we exclude central banks from the picture (i.e. no monetary injection). We instead focus only on monetary redistribution. The story outlined below does not explain the financial crisis by itself. Rather, it outlines a regulatory mechanism that exacerbated the crisis.

Let’s take a simple example that I have already used earlier. Only two types of lending exist: SME lending and mortgage/real estate lending. Basel regulations force banks to use more capital when lending to SME and as a result, bankers are incentivised to maximise ROE through artificially increasing mortgage lending and artificially restricting SME lending, as described in my first post on the topic.

In equilibrium and in a completely free-market world with no positive net investment, the economy looks like Garrison’s chart above. However, bankers don’t charge the Wicksellian natural rate of interest to all customers: they add a risk premium to the natural rate (effectively a ‘risk-free’ rate) to reflect the risk inherent to each asset class and customer. Those various rates of interest do reflect an equilibrium (‘natural’) state, which factors in the free markets’ perception of risk. Because lending to SME is riskier than mortgage lending, we end up with:

natural (risk free) rate < mortgage rate (natural rate + mortgage risk premium) < SME rate (natural rate + SME risk premium)

What RWAs do is to impose a certain perception of risk for accounting purposes, distorting the normal channelling of loanable funds and therefore each asset class’ respective ‘natural’ rate of interest. Unfortunately, depicting all demand and supply curves, their respective interest rates and the changes when Basel-defined RWAs are applied would be extremely messy in a single chart. We’re going to illustrate each asset class separately with their respective demand and supply curve. Let’s start with mortgage (real estate) lending:

Given the incentives they have to channel lending towards capital-optimising asset classes, bankers artificially increase the supply of loanable funds to all real estate activities, pushing the rate of interest below the natural rate of the sector. As the actual total supply of loanable funds does not change, returns on savings remain the same. In our PPF, this pushes resources towards real estate. Any other industry would interpret the lowered rate of interest as a shift in people’s intertemporal preferences towards the future and increase long-term investments at the expense of short-term production. Indeed, long-term housing projects are started. This is represented by the thin dotted red triangle.

Given the incentives they have to channel lending towards capital-optimising asset classes, bankers artificially increase the supply of loanable funds to all real estate activities, pushing the rate of interest below the natural rate of the sector. As the actual total supply of loanable funds does not change, returns on savings remain the same. In our PPF, this pushes resources towards real estate. Any other industry would interpret the lowered rate of interest as a shift in people’s intertemporal preferences towards the future and increase long-term investments at the expense of short-term production. Indeed, long-term housing projects are started. This is represented by the thin dotted red triangle.

However, the short-term housing supply is inelastic and cannot be reduced. The resulting real estate structure of production is the plain red triangle. Nonetheless, real estate developers have been tricked by the reduced interest rate and the long-term housing projects they started do not match economic agents’ future demand. Meanwhile, savers, adequately rewarded for their savings, do not draw down on them (or don’t have to), but are instead incentivised to leverage as they (indirectly) see profit opportunities from the differential between the natural and the artificially reduced rate. Leverage effectively becomes a function of the interest rate differential:

The increased leverage boosts the demand for existing real estate, bidding up prices, starting a self-reinforcing trend based on expected further price increases. We end up in a temporary situation of both short-term ‘overconsumption’ of real estate and its associated goods, and long-term overinvestments (malinvestments). This situation is depicted by the thick dotted red triangle and represents an unsustainable state beyond the PPF.

On the other hand, bankers artificially restrict the supply of loanable funds to SME, pushing the rate of interest above the natural rate. Tricked by a higher rate of interest, SMEs are led to believe that consumers now value more highly present goods over future goods (as they ‘apparently’ now save less of their income). They temporarily reduce interest rate-sensitive long-term investments to increase the production of late stages consumer goods. This results in an overproduction of consumer goods relative to economic agents’ underlying present demand. Nonetheless, wealth effects from the real estate boom temporarily boost consumption, maintaining prices level. Overconsumption of present goods could also eventually appear if and when savers start leveraging their consumption through low-rate mortgages, as house prices seem to keep increasing. In the long-run, SMEs’ investments aren’t sufficient to satisfy economic agents’ future demand of consumer goods.

With leverage increasing and the economy producing beyond its PPF, the situation is unsustainable. As increasingly more people pile in real estate, demand for real estate loanable funds increases, pushing up the interest rate of the sector. Interest payments – which had taken an increasingly large share of disposable income in line with growing leverage – rise, putting pressure on households’ finances. The economy reaches a Minsky moment and real estate prices start coming down. Real estate developers, who had launched long-term housing projects tricked by the low rates, find out that these are malinvestments that either cannot find buyers or are lacking the financial resources to be completed. Bankruptcies increase among over-leveraged households and companies. Banks start experiencing losses, contract lending and money supply as a result, whereas savers’ demand for money increases. The economy is in monetary disequilibrium. Welcome to the financial crisis designed in the Swiss city of Basel.

This all remains very theoretical and I’ll try to dig up some empirical evidences in another post. Nonetheless, the story seems to match relatively well what happened in some countries during the crisis. Soon after Basel regulations were implemented, household leverage in Spain or Ireland took off and came along with increasing house prices and retail sales, which both collapsed once the crisis struck. Under this framework, the artificially restricted supply of loanable funds to SME and the consequent reduction in long-term investments could also partly explain the rich world manufacturing problems. However, I presented a very simple template. As I mentioned in a previous post, securitisation and other banking regulations (liquidity…) blur the whole picture, and central banks can remain the primary channel through which interest rates are distorted.

RWA-based ABCT Series:

- Banks’ risk-weighted assets as a source of malinvestments, booms and busts

- Banks’ RWAs as a source of malinvestments – Update

- Banks’ RWAs as a source of malinvestments – A graphical experiment

- Banks’ RWAs as a source of malinvestments – Some recent empirical evidence

- A new regulatory-driven housing bubble?

Banks’ RWAs as a source of malinvestments – Update

Following a couple of comments I received on my RWA-based Austrian business cycle theory (ABCT) post, I’d like to clarify a few points:

- In the original ABCT, one cannot figure out where malinvestments will appear following an increase in the money supply not matched by an increase in the demand for money, apart from the fact that they are likely to be in producer goods industries rather than in consumer goods industries, due to the artificial lengthening of the structure of production. The mechanism involved is the Cantillon effect: the first firms to receive the new money will see their purchasing/investing power increase at the expense of the rest. We cannot really foresee where the new spending/investments will be directed though but what is certain is that the original structure of relative prices between goods in the economy will be modified as a result.

- In the RWA-based theory the Cantillon effect is ‘limited’: new funds are effectively channelled towards a few specific sectors that benefit from regulatory advantages (lower capital requirements for banks). It is thus possible to foresee which sectors could boom first and where some of the malinvestments could emerge. This does not mean that all malinvestments will show up in those sectors. Other related sectors could also boom as a result. And the increasing wealth effects of the people concerned could also reflect on unrelated sectors…

- Securitisation also makes it a lot more difficult to follow the channelling effect: asset-backed securities were lowly weighted under Basel 2 (under both Standardised and IRB methods) if they obtained a good credit rating. As a result, some corporate lending got a boost from the measure and this would typically replicate the exact process of the original ABCT. Risk-weights were tightened under latest Basel rules though.

- In the RWA-based ABCT, there is no increase in the money supply as assumption. Interest rates are lowered for some sectors (increasing related prices) and raised for others (depressing related prices) as a result of funding rebalancing through banks’ optimisation of capital. Consequences could be less catastrophic than an actual increase in money supply though (although I have no evidence of that). But there is always increase in the money supply at the same time anyway! 🙂

Today in an SNL article (membership required), I found out that the UK government is becoming increasingly frustrated about the lack of SME lending in the country. Hold your breath:

After years of frustration in its attempts to induce banks to extend more credit to small and medium-sized enterprises, the U.K. government has reached the perhaps surprising conclusion that bankers may simply lack the skills they need to lend.

RWAs? Capital requirements guys? No? It must be the skills! To be so clueless is both sad and hilarious.

RWA-based ABCT Series:

- Banks’ risk-weighted assets as a source of malinvestments, booms and busts

- Banks’ RWAs as a source of malinvestments – Update

- Banks’ RWAs as a source of malinvestments – A graphical experiment

- Banks’ RWAs as a source of malinvestments – Some recent empirical evidence

- A new regulatory-driven housing bubble?

The Economist struggles with Wicksell

Looks like Wicksell is back in fashion. After years (decades?) with barely any mention of this distinguished Swedish economist outside of work from some heterodox economic schools academics (like the Austrians), he is now everywhere and has unleashed a great debate among academics and financial practitioners. This is the outcome of both the financial crisis (preceded by interest rates that were below their ‘natural’ level according to Wicksellian-based theories) and the current unconventional policies undertaken by central banks all over the world (that risk repeating the same mistakes according to those same theories).

This week’s Economist’s column Free Exchange tries to identify whether or not current interest rates are too low based on a Wicksellian framework (A natural long-term rate). The article is complemented by a Free Exchange blog post on the newspaper’s website.

I won’t get back to the definitions of Wicksell’s money and natural rates of interest as I’ve done it in two recent posts (here and here). I only wish today to comment on The Economist’s interpretation (and misconceptions) of the Wicksellian rate.

A few of things shocked me in this week’s column. First, the assertions that “the natural rate prevails when the economy is at full employment” and that “the natural interest rate is often assumed to be constant.” I’m sorry…what? Putting aside the fact that ‘full employment’ is hard to define, there can be full employment with interest rates below or above their natural level, and interest rates can be at their natural level with the economy not at full employment. Many other ‘real’ factors have effects on ‘full employment’. Using full employment as a basis for spotting the equilibrium rate is dangerous.

Second, where did they get that the natural interest rate was constant? This doesn’t make sense. The natural interest rate rises and decreases following a few variables (various economic schools of thought will have differing opinions) such as time preference (i.e. whether or not people prefer to use income for immediate or future consumption), marginal product of capital (demand for loanable funds by entrepreneurs would increase as long as they can make a profit on the marginal increase in capital stock, driving up the interest rate in the process), liquidity preference (i.e. whether or not people desire to hold money as cash rather than some other less liquid form of wealth – pretty much the only important factor driving the interest rate for Keynesians –)… As you can imagine, all those factors vary constantly, impacting the demand for money and the demand for credit and in turn the rate of interest. It clearly does not remain constant…

The Economist also dismisses the possibility that real interest rates are too low by the fact that sovereign bonds’ yields are low, not only in the US (where the Fed is engaged in massive bonds purchases), but also in other economies whose central banks are less active in purchasing sovereign debt. But it overlooks the fact that natural rates aren’t uniform and may well be lower in other countries (for example, the natural rate was probably lower in Germany than in Spain and Ireland before the crisis, despite having a common central bank). It also overlooks that ‘risk-free’ rates used as a basis of most financial calculations internationally are US Treasuries, not sovereign bonds of other countries.

Finally, in support of its point, the column argues that expected future low rates could also reflect investors’ expectations of sluggish future growth and that “despite profit margins near record levels and rock-bottom interest rates, business investment has been sluggish, recently peaking at just above 12% of GDP; it topped 14% in the late 1990s.” Once again, this is misinterpreting the natural rate: the level of the natural rate of interest does not necessarily depend on expected future economic growth as I described above. Sluggish business investments also are more likely to reflect current regulatory ‘regime uncertainty’ than entrepreneurs’ doubts about the future state of the economy. On top of that, using the dotcom bubble as a reference for business investment is intellectually dishonest. Moreover, the article contradicts itself starting with “central banks ignore this century-old observation at their peril” only to conclude that “all this suggests that policy rates, low as they seem, are not out of line with their natural level.” Hhhmmm, ok.

The Free Exchange blog post by Greg Ip is a little better but still overall quite confused and confusing. Interestingly, it cites a paper by Bill White (http://dallasfed.org/assets/documents/institute/wpapers/2012/0126.pdf) who argues that the sort of yield-chasing that we can witness in financial markets today is a symptom of nominal rates being lower than natural rates. Doesn’t this remind you of anything? That’s right; it was exactly my point in this post. But it then cites Brad de Long, who can be added to the list of people who don’t understand what regulatory uncertainty is, and who tries as a result to convince us that the natural rate is below zero. Theoretically, a below zero natural rate if possible in period of deflation. But it does not make much sense to have a natural rate below zero when inflation is above zero.

It is definitely a hard task to identify the natural rate of interest. Nonetheless, a few rules of thumb are sometimes better than overly-complex reasoning. Investors would be perfectly happy with negative nominal yields if cost of life was declining even faster. This is obviously not the case at the moment.

Spontaneous finance at work

The FT reported today that non-bank lending to SMEs was at its highest level since 2008 in the UK, whereas bank lending had been declining constantly since the start of the crisis, despite politicians’ and central bankers’ actions to revive it (such as the BoE’s Funding for Lending Scheme).

What kind of non-bank lending are we talking about? Personally, I would call this ‘shadow banks lending’, even though some other economists and analysts may have a different definition of shadow banking. To me, it comprises the less-regulated non-bank entities, from hedge funds to peer-to-peer lending platforms.

This is spontaneous finance at work: while the bloated, politically connected and over-regulated banking system does not seem to be able to channel resources (private savings) to smaller-than-large corporations, private actors, from investment funds to private individuals, step in to respond to their funding needs. This phenomenon has two sources: banks’ lending rates are often too high (blame regulatory capital requirements) and banks’ offered savings rate too low (blame too high inflation vs. BoE rate). And blame banks’ too high operating costs for both. As a result, there is a mismatch between what savers expect and what companies expect.

The solution? Bypass banks. Various investment companies (from hedge funds to more traditional mutual funds) are now setting up funds to gather savings and lend directly to companies that need them. Peer-to-peer and crowdfunding platforms basically act the same way by disintermediating all financial institutions: individuals directly lend to other individuals or firms. We also now see funds investing through P2P platforms (reversing the disintermediation process). Through those shadow banking channels, both savers and borrowers get better rates than they would do at a bank. At the time of my writing, savers can earn from 4% to 7% on their savings (even some hedge funds would love to get such steady returns). Rates vary for borrowers, but are on average lower than that of banks.

Lending volume is still pretty small as the wider public isn’t yet aware of those funding opportunities. In the UK, Funding Circle has only lent slightly less than GBP170m so far to small businesses (this compares to banks’ SME lending which stands at around GBP170…bn). But it’s growing quickly: it was only launched in 2010. Moreover, other shadow banks had lent around GBP17bn as of June (yes, a lot of 17 something, just a coincidence).

As this City AM article highlighted today, as usual, the main risk to those financial innovations is over-regulation, preventing their development and potentially leading to the creation of much riskier and opaque financial products. Regulators wish to ‘protect’ savers. I argue that savers do not need to be protected: they need to learn to invest responsibly and to understand the risks involved. Protection distorts risk-taking and capital allocation.

More worrying is the fact that some peer-to-peer industry actors are now even lobbying to be regulated… They claim that regulation will reassure potential investors. I claim that regulation will mainly protect the established firms by making it more difficult for new competitors to enter the market and offer competitive products to savers and borrowers. A brand new financial system is building before our eyes. It is important not to repeat mistakes that led to our current ineffective banking system.

Photograph: govopps.co.uk

Recent Comments