Andy Haldane has a few lessons to teach Adair Turner

Andy Haldane, the Executive Director of Financial Stability at the Bank of England, is possibly one of the most knowledgeable top regulators around. Not only knowledgeable actually. Also modest. What I like in him is that he knows what he doesn’t know. He is the representative of common sense among regulators; it’s almost a pleasure to listen to him. To me, the contrast is sharp between Haldane and Lord Adair Turner, who should probably learn a thing or two from him.

In another (long) remarkable speech given at the Kansas City Fed on 31 August (sorry, I’m only catching up with that now) called ‘The dog and the frisbee‘, he demonstrates again his immense knowledge and modesty. He argues that, often, simple and straightforward rules are much more effective than complex and adaptive rules. Of course, what he targets here is the increasingly large Basel regulatory framework and the risk-weighted assets-based regulatory capital ratios. He many times cites research highlighting how unweighted measures performed better in spotting institutions at risk of collapse.

He based his opinion on his economic beliefs. He and I both disagree with the rational expectations hypothesis, which underlines most modern mainstream economic and finance theory. Financial theory is dominated by the ‘modern portfolio theory’, from which is derived some of the most basic financial tools (Capital Asset Pricing Model for example). I’ll get back to this in another post but the assumptions underlying CAPM/cost of capital and modern portfolio theory in general are highly unrealistic. Yet, few practitioners seem to care. Mathematics has taken over as the only way to describe the world and invest. It looks scientific. So it looks good and must be real.

A crucial point he mentions is that economic agents’ knowledge is limited and imperfect, and that the marginal cost of gathering further data may well outweigh the marginal benefit we get from this supplementary data. Even if all possible information could be gathered, cognitive abilities are limited and we may not be able to accurately process it. Finally, even if we could process it, data changes all the time and our conclusion could already be invalidated when released. This reminds me of some of the arguments developed by Mises and Hayek in the economic calculation problem in a socialist society. Indeed, central regulation of the banking sector effectively equates to partial central planning of the economic system.

Haldane also describes how modern risk-management models have to deal with several million parameters in order to assess various banking and trading risks and accordingly apply risk-weights to calculate regulatory capital ratios. The problem, he says, is that the pre-crisis way of thinking (both from a regulatory and an economic points of view) hasn’t changed: mathematical models have failed so what is needed is even more complex mathematics…

I don’t agree with everything Haldane says though. I don’t see the need to tax complexity or the even simple need for a regulatory leverage ratio for example. Moreover, Haldane himself admitted that both during the Great Depression and during the Great Recession, “the market was leading where regulators had feared to tread”, as banks took corrective measures to reassure investors. So if markets take the necessary measure by themselves and regulators can’t spot crises, why even have them in the first place?

Here are a few selected quotes:

- “No regulator had the foresight to predict the financial crisis, although some have since exhibited supernatural powers of hindsight.”

- “For what this paper explores is why the type of complex regulation developed over recent decades might not just be costly and cumbersome but sub-optimal for crisis control. In financial regulation, less may be more.”

- “Take decision-making in a complex environment. With risk and rational expectations, the optimal response to complexity is typically a fully state-contingent rule. Under risk, policy should respond to every raindrop; it is fine-tuned. Under uncertainty, that logic is reversed. Complex environments often instead call for simple decision rules. That is because these rules are more robust to ignorance. Under uncertainty, policy may only respond to every thunderstorm; it is coarse-tuned.”

- “The general message here is that the more complex the environment, the greater the perils of complex control. The optimal response to a complex environment is often not a fully state-contingent rule. Rather, it is to simplify and streamline.”

- “Strategies that simplify, or perhaps even ignore, statistical weights may be preferable. The simplest imaginable such scheme would be equal-weighting or “tallying”. In complex environments, tallying strategies have been found to be superior to risk-weighted alternatives. “

- “Complex rules may cause people to manage to the rules, for fear of falling foul of them. They may induce people to act defensively, focussing on the small print at the expense of the bigger picture.”

- “Of course, simple rules are not costless. They place a heavy reliance on the judgement of the decision-maker, on picking appropriate heuristics. Here, a key ingredient is the decision-maker’s level of experience, since heuristics are learned behaviours honed by experience.”

- “As of July this year, two years after the enactment of Dodd-Frank, a third of the required rules had been finalised. Those completed have added a further 8,843 pages to the rulebook. At this rate, once completed Dodd-Frank could comprise 30,000 pages of rulemaking. That is roughly a thousand times larger than its closest legislative cousin, Glass-Steagall. Dodd-Frank makes Glass-Steagall look like throat-clearing. The situation in Europe, while different in detail, is similar in substance. Since the crisis, more than a dozen European regulatory directives or regulations have been initiated, or reviewed, covering capital requirements, crisis management, deposit guarantees, short-selling, market abuse, investment funds, alternative investments, venture capital, OTC derivatives, markets in financial instruments, insurance, auditing and credit ratings.These are at various stages of completion. So far, they cover over 2000 pages. That total is set to increase dramatically as primary legislation is translated into detailed rule-writing. For example, were that rule-making to occur on a US scale, Europe’s regulatory blanket would cover over 60,000 pages. It would make Dodd-Frank look like a warm-up Act.”

- “Einstein wrote that: “The problems that exist in the world today cannot be solved by the level of thinking that created them”. Yet the regulatory response to the crisis has largely been based on the level of thinking that created it. The Tower of Basel, like its near-namesake the Tower of Babel, continues to rise.”

The two following quotes highlight how wrong are those who blame the crisis on ‘deregulation’:

- “Today, regulatory reporting is on an altogether different scale. Since 1978, the Federal Reserve has required quarterly reporting by bank holding companies. In 1986, this covered 547 columns in Excel, by 1999, 1,208 columns. By 2011, it had reached 2,271 columns. Fortunately, over this period the column capacity of Excel had expanded sufficiently to capture the increase.”

- “As numbers of regulators have risen, so too have regulatory reporting requirements. In the UK, regulatory reporting was introduced in 1974. Returns could have around 150 entries. […] Today, UK banks are required to fill in more than 7,500 separate cells of data – a fifty-fold rise. Forthcoming European legislation will cause a further multiplication. Banks across Europe could in future be required to fill in 30-50,000 data cells spread across 60 different regulatory forms.”

Photograph: The Times/Chris Harris

The investors’ great search for yield (and the likely collapse?)

Quite a long post… Here I’m going to have to get to the heart of my theoretical economic beliefs. I’ll try to keep it simple and as short as I can though. I will argue that there are many risks to investors going forward due to distortions in interest rates.

I wasn’t surprised yesterday when I read the two following FT articles. The first one tells how leveraged buyouts (LBOs) in the US have boomed recently, with leverage reaching the height of the pre-crisis boom of 5.3 times EBITDA, some even reaching 7.5 times EBITDA. This means that the private equity funds that acquired those firms used debt equivalent to 5 times earnings before depreciation, interest and taxes of the targets to fund the acquisitions. It is a lot. What is usually considered a highly leveraged LBO is around 4 times EBITDA and higher.

The second FT article talks about the fact that hedge funds are struggling to achieve high returns due to the size of the industry. Institutional investors have piled in hedge funds expecting higher returns than what traditional investments yield at the moment.

Earlier this year, we have seen many investors also piling in junk bonds, offering some of the lowest non-investment grade yields on record (despite the economy still not being in great shape and spreads over US treasuries not being at their lowest level ever). What’s going on?

Many people won’t agree with that, but to me, it looks like central banks’ monetary policies (low interest rates, quantitative easing, LTRO, OMT…) are lowering interest rates below their so-called ‘natural rates’. What is the natural rate of interest? It was the Swedish economist Knut Wicksell who came up with this term, highlighting to him the equivalent of the equilibrium free-market rate of interest in a barter world. Wicksell defined the natural rate in those terms in his 1898 book Interest and Prices, chapter 8:

“There is a certain rate of interest on loans which is neutral in respect to commodity prices, and tends neither to raise nor to lower them. This is necessarily the same as the rate of interest which would be determined by supply and demand if no use were made of money and all lending were effected in the form of real capital goods. It comes to much the same thing to describe it as the current value of the natural rate of interest on capital.” (emphasis his)

We can interpret it as the equilibrium interest rate that would exist under free market conditions, with no external interferences such as central banks’ monetary policies and governments’ interest-lowering schemes. In such conditions, intertemporal preferences between savers and borrowers are matched. This natural rate is in opposition to the ‘money rate of interest’, or the actual interest rate prevalent in a money and credit economy. The system is near equilibrium when the natural and the money rates coincide.

At the moment, some people such as Scott Sumner would argue that the natural rate of interest is below zero, justifying massive cash injection in the economy in order to lower the money rate of interest (= nominal interest rate). For him, the evidence is that nominal GDP has been allowed to fall below trend during the crisis and hasn’t recovered since then. While I agree that there was a case for an increase in the quantity of money to counteract a higher demand for money in the earlier stages of the crisis, I don’t believe this is now necessary. (I also believe that ‘trend’ is a very imperfect indicator on which to base policies. NGDP growth trend changed several times since World War 2 and can also be impacted over fairly long periods by unsustainable booms).

But it does continue. There have now been several rounds of QE in the US and monetary easing in Europe, Japan and China, to name a few. So the current situation looks like a sign that the money rate of interest has been pushed below the natural rate for quite some time. While nominal interest rates have been low for a while, real interest rates are now even lower (or even negative). And real interest rates are what investors care about, as it represents the actual gain over cost of life inflation. This has the consequence of pushing investors toward higher-yielding asset classes (hedge funds, private equity, junk bonds, emerging market equities…), in order to generate the returns they normally get on lower-risk assets.

But there is no inflation, you’re going to tell me. True, inflation as measured by CPI has also been relatively low for a while. Is CPI the right measure though? Asset prices (from real estate to equities and bonds) are not reflected in it despite arguably representing a form of inflation. Remember what Wicksell said: “There is a certain rate of interest on loans which is neutral in respect to commodity prices, and tends neither to raise nor to lower them.” Well… It’s clearly not what’s happening now. Even excluding asset classes, CPI may even not accurately reflect goods’ prices inflation. Would investors really need to search for yield if the cost of life actually declined or remained stable?

Does it mean that asset prices should always remain stable at the natural rate? Not at all, and there can be good reasons why asset prices move (real supply shocks for example). But what we can now witness in financial markets look more like malinvestments than anything else. Malinvestments represent bad allocation of capital to investments that would not be profitable under natural rate of interest conditions. As the discount rate on those investments decline in line with the nominal interest rate, they suddenly look attractive from a risk-reward point of view. But what if the discount rate is wrong in the first place? And what if future cash flows are also artificially boosted by low rates? This is a variation of the original Austrian business cycle theory, first developed by Ludwig von Mises and F.A. Hayek early 20th century, and which originally focused on the effects of a distorted interest rate on the structure of production.

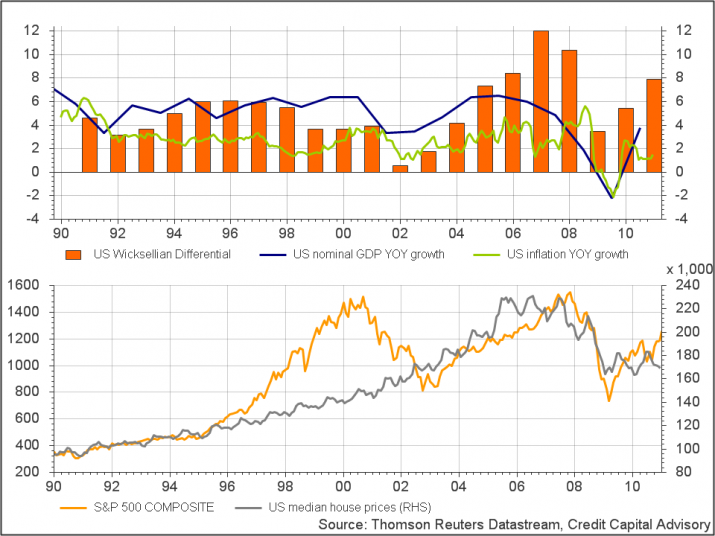

Another indication – more scientific than my previous observation – that the money rate may well be below the natural rate, has been devised by a former colleague of mine. Thomas Aubrey published a very interesting book in 2012, Profiting from Monetary Policy, in which he underlines his own calculation of what he calls the ‘Wicksellian differential’ (the difference between the natural and the money rates of interest). He uses estimates of the return on capital and the cost of capital in order to calculate the differential (according to neoclassical economic theory, the real interest rate should equal the marginal product of capital in equilibrium conditions – not everybody agrees though). Using those assumptions, it does look like we have been in a new credit boom since 2010 as you can see from the charts here:

Where does this lead us? Every unsustainable boom has to end at some point. It is likely that as soon as nominal interest rates start rising above a certain level, mark to market losses and worse, outright defaults, will force investors to mark down their holdings of malinvestments. We’ve already recently seen the impact on emerging markets of a mere talk of reducing the pace of quantitative easing.

What could be the consequences? Banks don’t place their liquidity in such risky assets, but might well be exposed to clients that do (many banks provide so-called leveraged loans for instance). Such impact on banks should be relatively limited though, given current regulatory constraints and deleveraging. In turn, this should limit the damage to credit creation and reduce the risk of another monetary contraction through the money multiplier. However, and it is a big question mark, banks might be exposed to companies (and households) under life support from low interest rates. This is more likely to be the case in some countries than others (I’ll let you guess which ones). When rates rise, loan impairment charges may rise quite a lot in those countries.

Private losses (through various types of investment funds and not subject to the money multiplier) may well be large though, negatively affecting private investments for some time afterwards. If you were thinking that the economy was naturally recovering at the moment, you might give it a second thought… Investors, beware, timing will be crucial.

First chart: Wall Street Journal; Second chart: Credit Capital Advisory

Ludwig von Mises’ death

Today is the 40th anniversary of Austrian economist Ludwig von Mises’ death.

I can’t emphasize enough how much Mises has been influential on my way of looking at both economic and social interactions. When I compared his writings to my day to day life as a banks analyst, everything made so much sense… I’ve read several of his books, of which Human Action is one of my favourite. I found myself in agreement with 99% of what I read in it. Believe me, this usually never happens.

He was a true believer in freedom, and was mocked during several decades for predicting the fall of the Soviet Union. A great economist.

Thank you Ludwig.

PS: You can read more about Mises on Free Banking and on the Mises Institute website (also here).

Payday lenders are the new usurers (apparently)

It scares me when I read this: “Today I’m putting payday lenders on notice: tougher regulation is coming and I expect them all to make changes so that consumers get a fair outcome. The clock is ticking.”

It sounds more like an extract from the speech of a populist politician than from the head of the UK-based Financial Conduct Authority.

The FCA is now about to implement ever more intrusive regulation: those bad payday lenders, modern times loan sharks, must be reined in. As a result, we are now witnessing the return of middle-ages usury laws, which sound logical from a moral (or religious) point of view but not much from an economic one.

Under the new proposal, payday lenders will not be able to roll over loans more than twice, cannot try to get their money back more than twice, the FCA can ‘order’ lenders to drop products that are “not in the best interest of consumers”, and borrowers will need to ‘prove’ they can repay the loan.

Most (if not all) those points don’t make much sense. But let me address one particular point: regulators are (as usual?) trying to fix the problem created by other regulations.

I don’t really see the problem with payday lenders. If they exist, it is because there is a market demand for them. If there is a market demand for them, it is because some people are excluded from the traditional financial system as their credit profile is too risky. From this, we can conclude two things: 1. banning or reining in payday lenders will have the only effect or excluding entirely some people from the credit system and 2. asking those people to prove that they can repay is nonsense, as otherwise they wouldn’t have come to a payday lender in the first place as banks would have welcomed that risk-free interest income…

But let’s go back one step. How can there be such a market demand originally? Because banks don’t want to take the risk with those customers anymore. Why don’t they want to take the risk, even if awesomely rewarded? Because they are under pressure from regulation/regulators to de-risk their balance sheet and it has become way too costly as a result… We have another typical example of a morally good action (to make banks safer) that has unintended consequences. Now regulators and politicians are trying to regulate the problems created by the first layer of regulation. I guess in a few years time they will have to add another layer to re-regulate the shortcomings of the current layer… A never-ending story.

Bitcoin, Silk Road, and weird stuff going on at City AM

Alright… I have to catch up with a lot of things after a long and very busy weekend…

First thing, I’d like that all of you who mention the Silk Road story as a ‘defeat’ for the classical liberal/libertarian ideals and for the possibility of a laissez-faire monetary system to stop right now. This Silk Road story and illegal trade have nothing to do with free-markets. Nothing. Illegal trade, and crazy people, and murders, and crime, existed before any alternative currency appeared. Liberalism does not advocate some kind of Mad Max anarchism, but voluntary cooperation.

Bitcoin has its faults (and apparently some of them might involve loss of anonymity), and if it does not satisfy the requirements of its users, it will disappear and be replaced by another medium of exchange. People will learn, new media of exchange will perform better. It’s the essence of evolution under free-markets.

Following my last-week’s post, I found it ‘funny’ to find out that the British financial newspaper City AM had two days in row published comments that reminded mine… See here and here. Coincidence?

The case for stable rules

I argued in a previous post about macroprudential regulation that discretionary regulation (as well as monetary and any other policy) was not recommended. Let me elaborate on that.

Stable rules are a fundamental feature of intertemporal coordination between savers and borrowers, between investors and entrepreneurs. In order for economic agents to (more or less) accurately plan for the future, for entrepreneurs to develop their business ideas and anticipate future demand, for savers to invest their money and know that their property rights are not going to disappear overnight and accordingly plan their own delayed consumption and provide entrepreneurs with directly available funds, the economic system needs a stable and predictable rule framework. Production and investments take time and as a result involve uncertainty, which should not be exacerbated by an instable rule set. The rule of law is part of this framework. Monetary policy, financial regulation and government policies should follow the same pattern, instead of being discretionary.

Let’s take an example: most of you have probably played Monopoly. You know in advance what the rules, possibilities and limitations of the game are and you plan your strategy accordingly. Imagine that, from time to time, the rules changed, making most of your elaborated and well-developed strategy suddenly worthless. You had purchased a number of tactically-placed hotels and had only a couple more to buy for your strategy to succeed. All of a sudden, a newly-introduced rule not only prevents you from buying other hotels (jeopardising your strategy), but also implements a tax on all hotels in order to promote investment in smaller houses and railway stations. You are now at risk of bankruptcy. I guess you would then think twice (or three times, or four times) before investing in a new hotel (or anything else) next time you play. It is the same thing in real life.

But, you’re going to tell me that there are also unexpected events in real life, whether they are wars or natural disasters, which require exceptional micromanagement. It is indeed arguable that some micromanagement would help. But I would also answer that there are also unexpected events in Monopoly: the Chance and Community Chest cards. So both in the game and in life, economic agents then face a choice: they can plan for the future, taking into account unexpected events and keep aside some resources as an economic buffer for bad times, or they can try to maximise potential profits, hoping that no disaster will strike but taking on more risk. Society represents a combination of people whose behaviours are somewhere on this spectrum.

The fact that those unexpected events exist does not imply that policymakers should introduce even more uncertainty into the system. Unfortunately, most of them are over-confident in their ability to understand, control, foresee and anticipate events. What they don’t see is the unintended consequences of their actions, which can often worsen rather than alleviate a given situation.

It can be argued that bad rules are better than constantly changing ones. Of course, good and stable rules are even better. Don’t get me wrong though. I am not saying that rules are good per se. Rules often distort, disturb or prevent economic activity and freedom. But some rules and legal systems are necessary, to facilitate the enforcement of private contracts. Whether this system must be set up through government monopoly or through private cooperation is another topic. What I am saying is that all else being equal, stable rules are the way to go.

The concept of ‘regime uncertainty’, invented by Robert Higgs, illustrates remarkably well what I am trying to show. It also particularly applies to nowadays’ financial regulation. Multiple constantly-changing rules across many jurisdictions affect financial institutions’ behaviour: risk is to be avoided as much as possible.

The world is uncertain enough as it is. A stable institutional framework is necessary for trust to build up within the system. And trust is the foundation of prosperity.

Photograph: Intermonk

The French government does not like crowdfunding

While most of the world is trying to move forward and away from the traditional banking sector, France tries its best to prevent financial innovation from annoying its politically-connected large banks. This is not welcome. But this follows a particular historical pattern. France has always been late in the race for financial innovation. This is originally due to the story of John Law and the Mississippi Company (later Compagnie d’Occident, later Compagnie Perpetuelle des Indes), which made anything financial-related suspicious and delayed the country’s financial development by around a 100 years.

Today, most countries, and in particular the US, the UK and emerging markets in Africa or Asia are trying to give a boost to the latest financial innovations around: crowdfunding, peer-to-peer lending, mobile banking… They hope that it would bolster lending to offset the effects of a depressed banking system (insolvency, regulation, regulation, regulation, regulation…).

Not in France. While BarcampBank (an ‘unconference’ for financial innovators) attendees have been talking about the difficulties of creating anything financial in France for a while, it recently looked like things were improving.

It looked too good to be true. The French government now wants to limit the amount invested to….. EUR250 per person per project. Yes. 250 euros. This is very likely to attract investors as you can guess… Projects will also be limited to EUR300k. It’s obviously not very big, especially in light of the projects available on some American and British platforms. The French government justifies this move by preventing individuals from taking on too much risk. Thank you dad.

Another, unofficial reason is that this type of financing will increasingly challenge banks’ savings and lending offers, probably within the next 15 years. French banks’ executives and French politicians are very connected: they often studied together, and many former civil servants work for French banks (and vice-versa). Crony capitalism is still the norm in the country.

Meanwhile, in the US, peer-to-peer lenders keep developing their business by now issuing securitisation…with the support of all large Wall Street banks. Another world, I’m telling you.

RWAs and Scott Sumner on banks

The FT yesterday published a new article on ‘manic regulation’. It comes as a relatively nice surprise given the tone of most of the articles recently. The FT reminds us that in 1980 there was one regulator for 11000 financial workers in the UK, in 2011, one for 300, that Basel 1 was 30 pages-long, and Basel 3 1000. It pleasantly questions whether the excessive regulation put in place at the moment would prevent another financial crisis. Its answer: “History suggests not”.

Something I particularly liked: “The worst thing about the new regime is that the whole system of risk-weights is a nonsense.” I really have to get back to RWAs in a post soon. In my opinion, it is an abomination of financial regulation that needs to be scrapped.

Scott Sumner reiterated his “banks don’t matter” claim. For those who don’t know him, he is the Market Monetarism guru, a new school of thought insisting that a central bank stabilising the growth of nominal GDP by monetary policy would prevent or reduce most crises. Business Insider called him “the blogger who may have just saved the American economy”… Scott and I are both pretty close and pretty far ideologically speaking. He is a classical liberal disliking most government interventions. And while we agree on most subjects, we won’t really agree on monetary policy and banking ones as we have differing economic worldviews. I do agree with him that NGDP targeting would be an improvement on our current monetary policy framework though.

So here Scott claims (in line with his worldview and what he already declared) that the banking system doesn’t matter in order to maintain the economy stable. He doesn’t want to include banks in macro-economic models (I think they are often quite useless anyway…). I don’t agree with him, as you can see from my comments, and from my exchange with two other economic bloggers, Nick Rowe and JP Koning. My point of view is that, in the real world, banks play the role of intermediaries without which the central bank would struggle to influence anything through monetary policy.

The regulatory regime runs against the concept of individual responsibility

Is it from me? No, it’s from the president of the Bundesbank! He wrote a nice piece for the FT. And, what a surprise, he’s basically saying the same thing about risk-weighted assets and regulation as I do. Ok, in a different way. He criticises the fact that some banks over-invest in government bonds because of…favourable regulatory treatment, including very low (or nil) RWAs, possibly leading to instability. Reminds me of something…

Recent Comments