Further evidence of macro-pru illusion

Back to blogging after two weeks travelling (though still busy until Christmas!).

Over the past few weeks I read a number of articles suggesting that the outcomes of real-life macro-prudential experiments were rather poor, to say the least. Those complement the various academic studies I had already commented on since the start of this year (see here and here).

The Economist reported that the Hong Kong housing market jumped by 21% over just…a single year, and has doubled over the past five years. And this happened despite the fact that local regulators have progressively introduced harsher and harsher macro-prudential measures: it raised the LTV constraints on new mortgages exactly seven times over the period. Any effect? None.

The Economist again reported that another sort of macro-prudential measure was being used in Sweden, with little effect. Swedish regulators required at least a 15% down payment for mortgages (i.e. max 85% LTV) in 2010, then raised the capital requirements that banks need to hold against mortgages in 2013, and then again raised an aggregate capital requirement earlier this year. But the property market has still boomed. Moreover, the newspaper says that even when tools targeting specific types of credit are put in place, the financial sector (and demand) responds by extending other types of credit:

the allure of cheap loans is so great that households in Sweden and beyond will find ways around the restrictions that remain in place. When the Slovakian government put limits on housing loans, banks boosted other forms of lending to bridge the gap. In Sweden, so-called “blanco-loans”, more expensive unsecured loans, can be used for that purpose. All told, credit is still growing and asset prices climbing, despite regulators’ efforts.

Earlier this summer, two IMF researchers published a paper listing and analysing the macro-pru policies and their effects in five different countries over the past decade or so, including Sweden and HK (the other ones being the Netherlands, New Zealand and Singapore). While in a few instances it might be a little early to judge the results of those implementations, it is clear that macro-pru has had only very minor impacts on only one of the markets they looked at. The only (small) positive impacts they found involved potentially enhanced resilience of the banking sector in some countries; which is even arguable as a percentage point more capital is unlikely to represent enough of a buffer to significantly absorb losses emanating from a collapsing NGDP driven by a housing market free-fall.

Let’s see what this paper has to say (I modified some of their charts below on purpose).

Hong Kong:

The impact of tightening macroprudential policy on property prices is less clear; property prices leveled off briefly following the measures but resumed their upward trend in mid-2014.

Also, remember this chart from a previous post (original paper here). Red dots represent tightening, and blue dots loosening, over a longer time frame. Effectiveness? Close to zero.

The Netherlands: No impact so far and no conclusion, but the housing market was already falling following the financial crisis anyway.

New Zealand:

Following the imposition of the caps there was a sharp fall in loans with high LTVs. Housing loans with high LTVs made up 5.2 percent of total new commitments in February 2014 compared with 25.1 percent in September 2013. In addition, the slowdown was accompanied by lower house sales and a lower growth in house prices.

Here, macro-pru had some minor effects (of course that LTV fell as they were capped), but what the paper doesn’t mention is that total lending growth has resumed and is concentrated in the lower than 80% LTV bracket. Moreover, house prices growth has also resumed. So, some positive effects but temporary and minor.

Singapore:

The combination of macroprudential and fiscal measures was effective in building buffers and moderating price appreciation in Singapore. The recent macroprudential measures lowered the average LTV ratio on new housing loans, and increased the share of borrowers with single mortgages. […] The rise in housing prices has abated. The HDB Resale Price Index declined eight percent from its peak in mid-2013 to the end of 2014 following a rise of almost 50 percent since end-2008. Similarly, the Private Residential Property Price Index declined by five percent from its peak in the third quarter of 2013 to the end of 2014. The decline in housing prices was accompanied by a sharp drop in transaction volumes. Annual new home sales in the private residential market declined by ⅓ in 2013 and by 50 percent in 2014

Singapore is probably one of the rare successes of macro-pru. But even there, disentangling the effects of macro-pru from those of Singapore economic difficulties and housing oversupply (leading to a natural correction) is not as straightforward as the IMF paper seems to believe. In particular as most of the fall in house prices occurred before the harshest constraints were put in place.

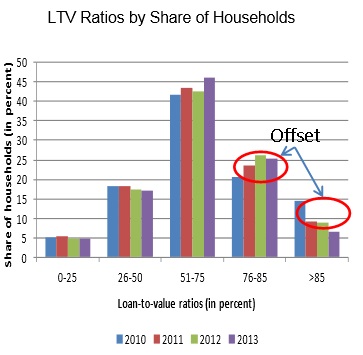

Sweden: Some shifts from the 85%+ LTV bracket to the 75-85%, but overall no effect on the housing market.

Overall, the paper concludes that

While there is some early evidence that the measures taken have enhanced banking system resilience, it is still early to determine their full impact.

Translation: macro-prudential measures’ effectiveness is very limited.

Of course domestic restrictions on housing supply still weigh on those countries’ property prices. But that’s not the whole story. As I have repeatedly said on this blog, housing booms have become a common occurrence throughout the world since the introduction of the Basel framework at the end of the 1980s (the parallel introduction of inflation targeting by central banks may well have amplified the trend). All countries with and without building restrictions have been affected, albeit at varying degrees.

What about the counterfactual? Some could argue that without the implementation of those measures, the situation if all those countries would have got even worse. But merely limiting a crisis or a the inflation of a bubble is not the goal, is it? Macro-pru is being sold to the public as an effective anti-crisis micro-management tool.

But what’s really scary is the absolute faith that most central bankers and regulators have in macro-prudential tools. Virtually all their speeches (see this search on the BIS website), presentations and publications praise macro-pru effects in taming the financial sector, while rejecting the idea that monetary policy is the right tool to do so (unsurprising as they keep trying to justify maintaining interest rates at their lowest levels in history).

As The Economist (itself a fan of macro-prudential policies 50% of the time, go figure) rightly sums up:

Ask a central banker what regulators should do when rock-bottom rates cause house prices to soar, and the reply will almost always be “macropru”. Raising rates to burst house-price bubbles is a bad idea, the logic runs, since the needs of the broader economy may not square with those of the property market. Instead, “macroprudential” measures, meaning restrictions on mortgage lending and borrowing, are seen as the answer. But this medicine is hard to administer, as Sweden’s housing market vividly illustrates.

In fact, it is very misleading to think of the needs of the broader economy that would in some ways be disconnected from those of the property market. The economy is organic and resources move from one area to another, where they are needed, or where incentives make them more profitable. As resources are scarce, there simply can’t be a disconnect between the various sectors of the economy. If an ‘imbalance’ appears somewhere, it must mean that there is an equal imbalance of the opposite sign somewhere else. As a result, trying to boost or tame particular sectors is counterproductive. Resources will still mostly flow towards the areas of least resistance.

The Basel banking framework introduced less resistance in the property sector (as well as in the sovereign and structured financial product spaces), and higher resistance in most of the rest of the economy. The ‘imbalances’ that lead to the apparently differing ‘needs’ of the property sector and of the broader economy are mere reflections of a more fundamental and deeper and bigger imbalance.

Macro-prudential policies merely represent an illusion of effective central planning. Not only its effectiveness is close to zero but it can only become effective when its effects are so harsh that they risk paralysing economic activity without fixing the underlying distortions in the economy.

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

Trackbacks / Pingbacks