Regulatory study says regulators were right

Some regulators seem to be ready to publish the most idiotic arguments to justify their earlier work. A new flawed study about an ill-conceived measure for small firms lending (SME) by the European Banking Authority did just that.

Despite continuously denying that capital requirements have anything to do with SME and other corporate lending, authorities have decided to experiment in 2014 by allowing banks to hold less capital against such lending (a measure called ‘SME Supporting Factor’). In order to find out whether or not this measure had any effect on SME lending, the EBA launched a study that concluded that there was (in the words of Reuters):

“no sufficient evidence” that lower capital charges provided additional stimulus for lending to SMEs compared to large corporates

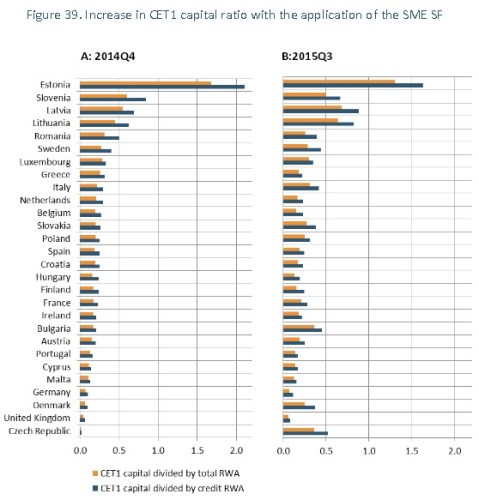

First, let’s notice the very small timeframe of the study: less than 18 months. Banks are unlikely to be able to grow their loan book by much in a safe fashion in such short timeframe. Second, the demand side seems not to be factored in (but I believe it to be a minor point). Third, SME SF only applied to tiny loans (not more than EUR1.5m, which is too small for medium sized firms). And indeed, the EBA report highlights that “SMEs subject to SF represent 4% of the aggregate corporate portfolios, 11% of the aggregate retail portfolios, and, in case of SA banks only, 6% of the aggregate exposures secured by immovable property.” In other word, they represent a very small share of banks’ loan books.

But the main issue with this measure, and indeed with this study, is that this SME SF has barely tightened the differential between risk-weights applied to SME/corporate exposures and risk-weights applied to real estate/sovereign exposures. SME SF only introduces a 24% capital discount to that form of lending (see table below for Basel’s ‘Standardised Approach’ for SME lending). The result, as the EBA shows, is that total risk-weighted assets (RWA, the denominator used to calculate regulatory capital ratios) only declined by…1.2%. This has effectively zero impact on banks’ RoEs.

Let’s make a quick calculation. A bank has total assets of $2,500 to which an average of risk-weight of 40% is applied, giving $1,000 RWAs. The bank also has $100 in regulatory capital (in order to simplify, let’s assume it only consists of plain vanilla shareholder equity), leading to a 10% regulatory capital ratio. The bank also makes $10 net profit, implying a 10% RoE.

A 1.2% decline in RWAs would lead to RWAs falling by a mere $12, making the capital ratio 10.1%*. Assuming the bank decides to maintain a 10% ratio, the newly-freed capital would allow RoE to improve by…0.1 percentage point. Impressive effect, to say the least.

Irony aside, SME SF was a very ill-conceived measure: its scope was too narrow (targeting firms that are too small), and the incentives it gave banks were very superficial given the remaining differential between the risk-weights applied to SME and other types of exposures (Standardised Approach risk-weight on mortgages remain way below at 35% – and median risk-weight is 17% on an IRB basis** – see upcoming post – UPDATE: here). The mini-gains that banks’ could have expected would have possibly been more than offset by the risk of rapidly growing an SME loan book in an uncertain economic environment.

The study also found that current capital requirements for small and large corporates were adequate, and that applying SME SF would lead to those exposures being undercapitalised. This is in complete opposition with the (mostly independent, that is, not published by EU regulators) papers I reported on a few weeks ago.

In the end, this research undertook by a regulatory body succeeded to prove what it wanted to prove: regulatory measures were right from the start. If only it were not completely wrong.

*This is in line with the EBA’s findings:

**Standardised method refers to a RWA calculation method that applies to relatively small banks, which use fixed risk-weights provided by Basel rules. IRB (Internal Rating Based) refers to more flexible (but validated by regulators) risk-weights calculated internally by large banks using complex models.

Recent Comments