News digest (Libor 1.7bn fine, banks’ poor IT systems, banking, telco, IT, retailing convergence…)

Again this week, so many things happening that I can’t spend much time commenting on each and I have to make choices!

George Osborne, UK’s Chancellor of the Exchequer, is about to announce a tax-free treatment for P2P lending, which could be included in individual Isa accounts. This is a good thing. Nothing much more to say…

The Bank of England is thinking of asking UK-based banks to provide regulatory capital ratios calculated using standard risk-weights as defined by Basel’s Standardised method. These ratios would not replace those banks’ main capital ratios as currently calculated (under the IRB method) but would ‘complement’ them. It’s a good idea and we may well end up having a few surprises…

The EU has fined some of the large global banks as part of the Libor rate-rigging. Banks will have to pay EUR1.7bn. This isn’t that significant given what JPMorgan has paid so far in fines in the US… I stopped counting and I may well be wrong but I think they paid around USD$15bn so far this year. Surely this should make me doubt about the ability of laissez-faire to regulate banks? Not really. First, we are not in a laissez-faire environment. Second, laissez-faire does not mean laissez-faire fraudulent activities. It means laissez-faire people to negotiate their own contracts and agreements. When those contracts are not respected, when there is fraud, punishment should ensue. Laissez-faire is completely in favour of the rule of law. Moreover in a real free-market environment, it is likely that most fraudulent banks would already be out of business…

Something I know from experience: many banks have really poor IT systems and poorly-designed databases. This week, Royal Bank of Scotland’s customers could not access their accounts anymore for a whole day (and pretty busy shopping day on top of that). Its CEO acknowledged that the bank will have to invest… GBP1bn in its IT systems. That’s a massive bill. It shows how outdated its IT systems must have been. It is scary to see that some banks (nop, no name), whether small, medium-sized or massively massive have such poorly-designed systems that they cannot adequately track simple data such as their exposures and the level of provisioning against them by industrial sector or geographical area for example. This is the result of years, if not decades, of underinvestment in IT. This is also why start-up banks are usually much more efficient: they have top-notch IT. For large banks, no surprise, trading systems have been upgraded at a much faster pace than commercial and retail banking ones. Banks are currently plagued by their high cost base. But more efficient IT systems would have helped maintain their costs lower while improving internal productivity.

Moreover, banks are also under threat from new financial actors, and possibly future data-heavy entrants such as Google and Amazon. Those firms have great IT systems: it is their core business. What if they entered the banking business? It’s what Spain’s BBVA’s CEO asked in the FT this week. Indeed, banks are now closing branches one by one as customers move online or mobile. It also means that new entrants possibly wouldn’t need any branch network altogether and could offer more efficient services to customers, using their huge data centres and cloud computing capabilities. A quick visit to the annual Barcamp Bank ‘unconference’ shows how many people are currently working on new customer-friendly and efficient banking API and other systems. We’ve already seen the ‘convergence’ of IT, telecoms and media. Are we about to witness a banking, IT, telecom, retailing, online search and payment convergence?

Are synthetic CDOs making a comeback? Well, issuance volume is still pretty low… Unless low interest rates start over-boosting this market too?

Finally, Columbia University’s Charles Calomiris has his own take on Admati and Hellwig’s recommendations and rejects some of their claims (such as the fact that higher equity levels would not impair lending, a claim that I have already made here, although my reasoning was different). He also favours rising banks’ equity requirements though.

What Walter Bagehot really said in Lombard Street (and it’s not nice for central bankers and regulators)

(Warning: this is quite a long post as I reproduce some parts of Bagehot’s writings)

As I promised in a post a few days ago, I am today getting back to the common ancestor of all of today’s central bankers, Walter Bagehot.

Bagehot is probably one of the most misquoted economist/businessmen of all times. Most people seem to think they can just cherry pick some of his claims to justify their own beliefs or policies, and leave aside the other ones. Sorry guys, it doesn’t work like that. Bagehot’s recommendations work as a whole. Here I am going to summarise what Bagehot really said about banking and regulation in his famous book Lombard Street: A description of the Money Market.

Let’s start with central banking. As I’ve already highlighted a few days ago, Bagehot said that the institution that holds bank reserves (i.e. a central bank) should:

- Lend freely to solvent banks and companies

- Lend at a punitive rate of interest

- Lend only against good quality collateral

I can’t recall how many times I’ve heard central bankers, regulators and journalists repeating again and again that “according to Bagehot” central banks had to lend freely. Period. Nothing else? Nop, nothing else. Sometimes, a better informed person will add that Bagehot said that central banks had to lend to solvent banks only or against good collateral. Very high interest rates? No way. Take a look at what Mark Carney said in his speech last week: “140 years ago in Lombard Street, Walter Bagehot expounded the duty of the Bank of England to lend freely to stem a panic and to make loans on “everything which in common times is good ‘banking security’.”” Typical.

Now hold your breath. What Bagehot said did not only involve central banking in itself but also the banking system in general, as well as its regulation. Bagehot attacked…regulatory ratios. Check this out (chapter 8, emphasis mine):

But possibly it may be suggested that I ought to explain why the American system, or some modification, would not or might not be suitable to us. The American law says that each national bank shall have a fixed proportion of cash to its liabilities (there are two classes of banks, and two different proportions; but that is not to the present purpose), and it ascertains by inspectors, who inspect at their own times, whether the required amount of cash is in the bank or not. It may be asked, could nothing like this be attempted in England? could not it, or some modification, help us out of our difficulties? As far as the American banking system is one of many reserves, I have said why I think it is of no use considering whether we should adopt it or not. We cannot adopt it if we would. The one-reserve system is fixed upon us.

Here Bagehot refers to reserve requirements, and pointed out that banks in the US had to keep a minimum amount of reserves (i.e. today’s equivalent would be base fiat currency) as a percentage of their liabilities (= customer deposits) but that it did not apply to Britain as all reserves were located at the Bank of England and not at individual banks (the US didn’t have a central bank at that time). He then follows:

The only practical imitation of the American system would be to enact that the Banking department of the Bank of England should always keep a fixed proportion—say one-third of its liabilities—in reserve. But, as we have seen before, a fixed proportion of the liabilities, even when that proportion is voluntarily chosen by the directors, and not imposed by law, is not the proper standard for a bank reserve. Liabilities may be imminent or distant, and a fixed rule which imposes the same reserve for both will sometimes err by excess, and sometimes by defect. It will waste profits by over-provision against ordinary danger, and yet it may not always save the bank; for this provision is often likely enough to be insufficient against rare and unusual dangers.

Bagehot thought that ‘fixed’ reserve ratios would not be flexible enough to cope with the needs of day-to-day banking activities and economic cycles: in good times, profits would be wasted; in bad times, the ratio is likely not to be sufficient. Then it gets particularly interesting:

But bad as is this system when voluntarily chosen, it becomes far worse when legally and compulsorily imposed. In a sensitive state of the English money market the near approach to the legal limit of reserve would be a sure incentive to panic; if one-third were fixed by law, the moment the banks were close to one-third, alarm would begin, and would run like magic. And the fear would be worse because it would not be unfounded—at least, not wholly. If you say that the Bank shall always hold one-third of its liabilities as a reserve, you say in fact that this one-third shall always be useless, for out of it the Bank cannot make advances, cannot give extra help, cannot do what we have seen the holders of the ultimate reserve ought to do and must do. There is no help for us in the American system; its very essence and principle are faulty.

To Bagehot, requirements defined by regulatory authorities were evidently even worse, whether for individual banks or applied to a central bank. I bet he would say the exact same thing of today’s regulatory liquidity and capital ratios, which are essentially the same: they can potentially become a threshold around which panic may occur. As soon as a bank reaches the regulatory limit (for whatever reason), alarm would ring and creditors and depositors would start reducing their lending and withdrawing their money, draining the bank’s reserves and either creating a panic, or worsening it. This reasoning could also be applied to all stress tests and public shaming of banks by regulators over the past few years: they can only make things worse.

Even more surprising: the spiritual leader of all of today’s central bankers was actually…against central banking. That’s right. Time and time again in Lombard Street he claimed that Britain’s central banking system was ‘unnatural’ and only due to special privileges granted by the state. In chapter 2, he said:

I shall have failed in my purpose if I have not proved that the system of entrusting all our reserve to a single board, like that of the Bank directors, is very anomalous; that it is very dangerous; that its bad consequences, though much felt, have not been fully seen; that they have been obscured by traditional arguments and hidden in the dust of ancient controversies.

But it will be said—What would be better? What other system could there be? We are so accustomed to a system of banking, dependent for its cardinal function on a single bank, that we can hardly conceive of any other. But the natural system—that which would have sprung up if Government had let banking alone—is that of many banks of equal or not altogether unequal size. In all other trades competition brings the traders to a rough approximate equality. In cotton spinning, no single firm far and permanently outstrips the others. There is no tendency to a monarchy in the cotton world; nor, where banking has been left free, is there any tendency to a monarchy in banking either. In Manchester, in Liverpool, and all through England, we have a great number of banks, each with a business more or less good, but we have no single bank with any sort of predominance; nor is there any such bank in Scotland. In the new world of Joint Stock Banks outside the Bank of England, we see much the same phenomenon. One or more get for a time a better business than the others, but no single bank permanently obtains an unquestioned predominance. None of them gets so much before the others that the others voluntarily place their reserves in its keeping. A republic with many competitors of a size or sizes suitable to the business, is the constitution of every trade if left to itself, and of banking as much as any other. A monarchy in any trade is a sign of some anomalous advantage, and of some intervention from without.

As reflected in those writings, Bagehot judged that the banking system had not evolved the right way due to government intervention (I can’t paste the whole quote here as it would double the size of my post…), and that other systems would have been more efficient. This reminded me of Mervyn King’s famous quote: “Of all the many ways of organising banking, the worst is the one we have today.” Another very interesting passage will surely remind my readers of a few recent events (chapter 4):

And this system has plain and grave evils.

1st. Because being created by state aid, it is more likely than a natural system to require state help.

[…]

3rdly. Because, our one reserve is, by the necessity of its nature, given over to one board of directors, and we are therefore dependent on the wisdom of that one only, and cannot, as in most trades, strike an average of the wisdom and the folly, the discretion and the indiscretion, of many competitors.

Granted, the first point referred to the Bank of England. But we can easily apply it to our current banking system, whose growth since Bagehot’s time was partly based on political connections and state protection. Our financial system has been so distorted by regulations over time than it has arguably been built by the state. As a result, when crisis strikes, it requires state help, exactly as Bagehot predicted. The second point is also interesting given that central bankers are accused all around the world of continuously controlling and distorting financial markets through various (misguided or not) monetary policies.

For all the system ills, however, he argued against proposing a fundamental reform of the system:

I shall be at once asked—Do you propose a revolution? Do you propose to abandon the one-reserve system, and create anew a many-reserve system? My plain answer is that I do not propose it. I know it would be childish. Credit in business is like loyalty in Government. You must take what you can find of it, and work with it if possible.

Bagehot admitted that it was not reasonable to try to shake the system, that it was (unfortunately) there to stay. The only pragmatic thing to do was to try to make it more efficient given the circumstances.

But what did he think was a good system then? (chapter 4):

Under a good system of banking, a great collapse, except from rebellion or invasion, would probably not happen. A large number of banks, each feeling that their credit was at stake in keeping a good reserve, probably would keep one; if any one did not, it would be criticised constantly, and would soon lose its standing, and in the end disappear. And such banks would meet an incipient panic freely, and generously; they would advance out of their reserve boldly and largely, for each individual bank would fear suspicion, and know that at such periods it must ‘show strength,’ if at such times it wishes to be thought to have strength. Such a system reduces to a minimum the risk that is caused by the deposit. If the national money can safely be deposited in banks in any way, this is the way to make it safe.

What Bagehot described is a ‘free banking’ system. This is a laissez faire-type banking system that involves no more regulatory constraints than those applicable to other industries, no central bank centralising reserves or dictating monetary policy, no government control and competitive currency issuance. No regulation? No central bank to adequately control the currency and the money supply and act as a lender of last resort? No government control? Surely this is a recipe for disaster! Well…no. There have been a few free banking systems in history, in particular in Scotland and Sweden in the 19th century, to a slightly lesser extent in Canada in the 19th and early 20th, and in some other locations around the world as well. Curiously (or not), all those banking systems were very stable and much less prone to crises than the central banking ones we currently live in. Selgin and White are experts in the field if you want to learn more. If free banking was so effective, why did it disappear? There are very good reasons for that, which I’ll cover in a subsequent post on the history of central banking.

I am not claiming that Bagehot held those views for his entire life though. A younger Bagehot actually favoured monopolised-currency issuance and the one-reserve system he decried in his later life. I am not even claiming that everything he said was necessarily right. But Bagehot as a defender of free banking and against regulatory requirements of all sort is a far cry from what most academics and regulators would like us to believe today. Personally, I find that, well, very ironic.

BoE’s Mark Carney is burying Walter Bagehot a second time

Banks were partying on Thursday. Mark Carney, the new governor of the Bank of England, decided to ‘relax’ rules that had been put in place by its predecessor, Mervyn King. From now on, the BoE will lend to banks (as well as non-bank financial institutions) for longer maturities, accept less quality collateral in exchange, and lower the interest rate on/cost off those facilities. Mervin King was worried about ‘moral hazard’. Mark Carney has no idea what that means.

According to the FT, Barclays quickly figured out what this move implied: “it reduces the need for, and the cost of, holding large liquidity buffers.” Just wow. So, while we’ve just experienced a crisis during which some banks collapsed because they didn’t hold enough liquid assets on their balance sheet as they expected central banks and governments to step in if required, Carney’s move is expected to make the banks hold……even less liquidity.

It’s obviously nothing to say that this goes against every possible piece of regulation devised over the last few years. While the regulators were right in thinking that banks needed to hold more liquid assets, they took on the wrong problem: it was government and central bank support that brought about low liquidity holdings, and not free-markets recklessness. Anyway, Carney’s move kind of undermines that effort and risks rewarding mismanaged banks at the expense of safer ones.

Carney’s decision also goes against all the principles devised by the ‘father’ of central banking: Walter Bagehot. I guess it is time to decipher Bagehot, as he has been constantly misquoted since the start of the crisis by people who have apparently never read him. As a result he was used to justify what were actually anti-Bagehot policies. Bagehot’s principles are underlined in his famous book Lombard Street, written in 1873. What should a central bank do during a banking crisis? According to Bagehot (as described in chapters 2, 4 and 7), it should:

- Lend freely to solvent banks and companies

- Lend at a punitive rate of interest

- Only accept good quality collateral in exchange

For instance, in chapter 2:

The holders of the cash reserve must be ready not only to keep it for their own liabilities, but to advance it most freely for the liabilities of others. They must lend to merchants, to minor bankers, to ‘this man and that man,’ whenever the security is good.

In chapter 7:

First. That these loans should only be made at a very high rate of interest. This will operate as a heavy fine on unreasonable timidity, and will prevent the greatest number of applications by persons who do not require it. The rate should be raised early in the panic, so that the fine may be paid early; that no one may borrow out of idle precaution without paying well for it; that the Banking reserve may be protected as far as possible.

Secondly. That at this rate these advances should be made on all good banking securities, and as largely as the public ask for them. The reason is plain. The object is to stay alarm, and nothing therefore should be done to cause alarm. But the way to cause alarm is to refuse some one who has good security to offer… No advances indeed need be made by which the Bank will ultimately lose.

No central bank applied Bagehot’s recommendations during the financial crisis. Granted, given the organisation of today’s financial system, it is difficult for central bank to lend to non-financial firms. Nonetheless, it took them a little while to start lending freely and lent to insolvent banks as well. They also started to accept worse quality collateral than what they used to (think about the Fed now purchasing mortgage/asset-backed securities for example). Finally, central banks have never charged a punitive rate on their various facilities. Quite the contrary: interest rates were pushed down as much as humanly possible on all normal and exceptional refinancing facilities.

While the ECB and the Fed have made clear that some of those were temporary measures, Carney now seems to imply that, not only are they here to stay, but they also will be extended in non-crisis times. He calls that being “open for business”. Poor Bagehot must be turning in his grave right now.

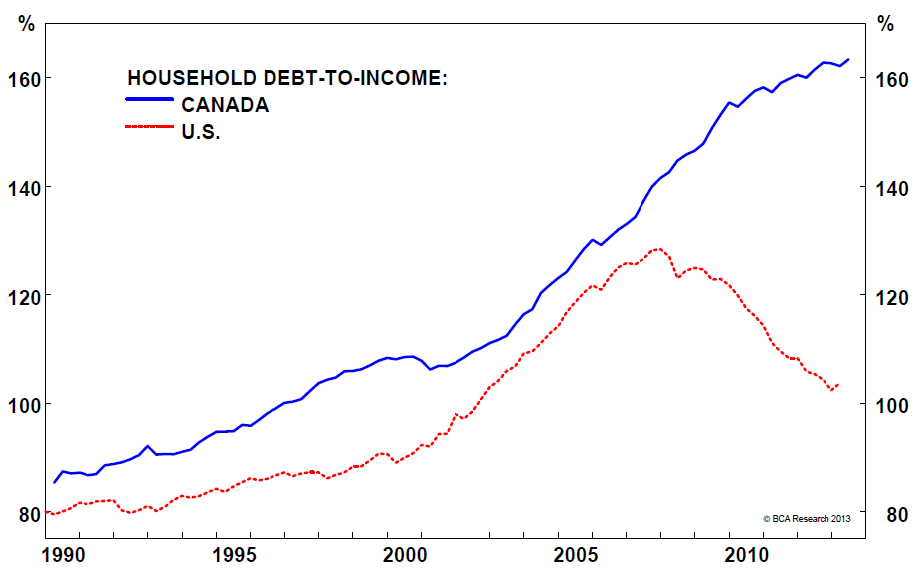

According to Carney, those measures will reinforce financial stability. Really? So no moral hazard involved? no bank taking unnecessary risks because it knows that the BoE has its back? If Mervyn King didn’t do everything perfectly while in charge, at least he had a point. Carney, after overseeing a large credit bubble in Canada over the past few years (he first joined the Bank of Canada in 2003, then rejoined it as Governor in 2008), is now applying his brilliant recipe to the UK.

I think that Carney’s decisions introduce considerable incentive distortions in the banking system. This is clearly not what a free-market should look like. In any case, if a new crisis strikes as a result, I am pretty sure that laissez-faire will be blamed again. It is ironic to see that some of those central bankers destroy faith in free-markets while trying to protect them.

Bagehot also said other things that go against the principles driving our current banking and regulatory system. More details in another post!

Photograph: Reuters/Bloomberg

Chart: The Big Picture

Quick update on recent news: John Kay, hedge funds and house prices control

John Kay wrote an interesting piece in the FT yesterday saying that finance should be treated like fast food to secure stability. I can’t agree more. A nice quote:

Still, would it not be better if proper supervision ensured that no financial institution could ever get into a mess like Northern Rock or Lehman – or Royal Bank of Scotland or Citigroup or AIG? No, it would not. Just replace “financial institution” with “fast-food outlet” or “supermarket” or “carmaker” in that sentence to see how peculiar is the suggestion.

I know what you’re going to say: “but banks are different!” To which I would reply: no, they aren’t. It is treating them as different that makes them different.

Another nice one:

We have experience of structures in which committees in Moscow or Washington take the place of the market in determining the criteria by which a well-run organisation should be judged, and that experience is not encouraging. The truth is that in a constantly changing environment nobody really knows how organisations should best be run, and it is through trial and error that we find out.

I am a little surprised though, as I have the impression that John Kay is kind of contradicting himself (see his post from June in which he seems to say that banking reforms are going the right direction).

Another piece highlighted how much regulation is changing the hedge fund industry. What’s going on is that regulation is now limiting new entrants in the market as they can’t cope with booming compliance costs. This results in the largest hedge funds experiencing most of new money inflow from investors. Is this a problem? Yes. First, small hedge funds have traditionally outperformed large and established ones on average. So preventing them from entering the market reduces market and economic efficiency: proper allocation of capital to where it would be the most profitable does not happen as a result (and consequently, returns to investors are lower). Second, and more worrying, is that regulation is now replicating what has happened in the banking industry: it’s creating too big to fail hedge funds (and nobody seems to remember LTCM). Well done guys.

Finally for today, echoing my earlier post, a BoE member thinks that it is not the role of the central bank to control house prices. I certainly agree.

Spontaneous finance at work

The FT reported today that non-bank lending to SMEs was at its highest level since 2008 in the UK, whereas bank lending had been declining constantly since the start of the crisis, despite politicians’ and central bankers’ actions to revive it (such as the BoE’s Funding for Lending Scheme).

What kind of non-bank lending are we talking about? Personally, I would call this ‘shadow banks lending’, even though some other economists and analysts may have a different definition of shadow banking. To me, it comprises the less-regulated non-bank entities, from hedge funds to peer-to-peer lending platforms.

This is spontaneous finance at work: while the bloated, politically connected and over-regulated banking system does not seem to be able to channel resources (private savings) to smaller-than-large corporations, private actors, from investment funds to private individuals, step in to respond to their funding needs. This phenomenon has two sources: banks’ lending rates are often too high (blame regulatory capital requirements) and banks’ offered savings rate too low (blame too high inflation vs. BoE rate). And blame banks’ too high operating costs for both. As a result, there is a mismatch between what savers expect and what companies expect.

The solution? Bypass banks. Various investment companies (from hedge funds to more traditional mutual funds) are now setting up funds to gather savings and lend directly to companies that need them. Peer-to-peer and crowdfunding platforms basically act the same way by disintermediating all financial institutions: individuals directly lend to other individuals or firms. We also now see funds investing through P2P platforms (reversing the disintermediation process). Through those shadow banking channels, both savers and borrowers get better rates than they would do at a bank. At the time of my writing, savers can earn from 4% to 7% on their savings (even some hedge funds would love to get such steady returns). Rates vary for borrowers, but are on average lower than that of banks.

Lending volume is still pretty small as the wider public isn’t yet aware of those funding opportunities. In the UK, Funding Circle has only lent slightly less than GBP170m so far to small businesses (this compares to banks’ SME lending which stands at around GBP170…bn). But it’s growing quickly: it was only launched in 2010. Moreover, other shadow banks had lent around GBP17bn as of June (yes, a lot of 17 something, just a coincidence).

As this City AM article highlighted today, as usual, the main risk to those financial innovations is over-regulation, preventing their development and potentially leading to the creation of much riskier and opaque financial products. Regulators wish to ‘protect’ savers. I argue that savers do not need to be protected: they need to learn to invest responsibly and to understand the risks involved. Protection distorts risk-taking and capital allocation.

More worrying is the fact that some peer-to-peer industry actors are now even lobbying to be regulated… They claim that regulation will reassure potential investors. I claim that regulation will mainly protect the established firms by making it more difficult for new competitors to enter the market and offer competitive products to savers and borrowers. A brand new financial system is building before our eyes. It is important not to repeat mistakes that led to our current ineffective banking system.

Photograph: govopps.co.uk

Should the Bank of England have tools to prick property bubbles?

The answer is no. (but not according to this FT article)

Wait… Actually, it already has tools: it’s called monetary policy. Place the interest rate at the right level and stop massively injecting cash in the economy and, perhaps, you won’t witness real estate bubbles?

There are other hugely distorting UK government policies at the moment: the Funding-for-Lending scheme and the more recent Help-to-Buy, which both push demand for property up through artificially low interest rates. I’ll explain that in details in another post.

So the question becomes: why adding other distorting tools (whether ‘macroprudential‘ or ‘microprudential‘) and policies, such as maximum loan-to-value or loan-to-income ratios, on top of already deficient tools and policies? I have another suggestion: why not trying to correct the failings of the first layer of policies? Just saying.

PS: Lord Turner is obviously mentioned in this FT article.

Recent Comments