The end of banking? Not like this please

I recently read Jonathan McMillan’s The End of Banking, which I first heard of through FT Alphaville here (McMillan is actually a pseudonym to cover it two authors: an academic and a banker). I have mixed feelings about this book. I really wanted to agree with it. And I do, to some extent. But I simply cannot agree with a number of other points they make.

Their proposal to reform banking is as follows (see the book for details): lending can be disintermediated through P2P lending platforms (and equivalent), which both monitor potential borrowers through credit scoring and allocate savers’ funds to minimise the probability of losses. Marketplaces set up by platforms would enable savers to sell their investments to generate cash if needed. What about the payment system? Their solution is for non-bank FIs to continuously provide market liquidity a number of financial instruments using algorithmic trading. Current accounts would in fact be invested like mutual funds, which would instantly convert those investments into cash when required for payment. They also propose accounting rule changes to prevent corporations from creating money-like instruments.

As such, they propose to end banks’ inside money and have a financial system exclusively based on digital outside money controlled by a monetary authority. While they don’t classify it this way, it does seem to me to be some sort of 100%-reserve banking proposal: the money supply is fixed in the very-short term and exogenously-defined by the monetary authority.

What I agree with:

- The main thesis of the book is completely valid and is something I have also argued for a little while: technological disruptions are now allowing us to go beyond banking and disintermediate it. P2P lending, non-banking payment systems, decentralised payment frameworks and currencies, algorithm-driven credit scoring… In many areas, banks have almost become redundant. I totally adhere to the authors’ thesis (although credit scoring does have real limitations).

- Technological developments have facilitated regulatory arbitrage, if not enabled it. Computing power now allow banks to optimise their capital requirements through the use of complex models which, it is important to point out, are validated by regulators.

What I disagree with:

- The authors seem to believe that banking regulation is usually a good thing and cannot seem to understand the various distortions, bubbles and inefficiencies those regulations create. According to them, if only technology hadn’t boomed over the past three decades, the banking system would be more stable. I strongly disagree.

- I dislike the top-down banking reform approach taken by their thesis. Free markets, driven by technology, should decide under what form the next iteration of banking should arise.

- I also see weaknesses in their proposal. First, I cannot agree with their view that money belongs to the public sphere, and that IOUs must benefit from a state guarantee to qualify as money. This has been disproved by history over and over again. Second, I see their proposal to have algorithmic trading manage the payment system as not only unworkable, but also dangerous. As already witnessed, algorithmic trading is imperfect and can amplify crashes rather than prevent them. How their payment system would react during a crisis, when everyone tries to exit most investments and pile into a few others, is anyone’s guess. Mine is that the payment system would suddenly be down, paralysing the entire economy. To be fair, their treatment of cash is unclear: could we maintain a custody account comprising only digital cash in their framework?

- Their 100%-reserve banking reform does not address fluctuations in the demand for money. Centralised monetary authorities do neither have access to the right information, nor within the right timeframe, to accurately provide extra media of exchange when needed by the public. Private entities, in direct contact with the public, can.

- Finally, though this is a minor point, I disagree with their monetary policy stance. It is inaccurate to present price stability as ideal to avoid economic distortions: productivity increases should lead to mild deflation in a growing economy (see Selgin’s Less than Zero or any market monetarist or Austrian blog and research paper). I also reject their physical cash ban, from a libertarian standpoint: people should be able to withdraw cash if ever they wish to*. This would seriously limit their negative interest rates policy proposal.

Overall, it is a thought-provoking and interesting book, which also quite accurately describes our current banking system in its first part (mostly aimed at people who don’t know that much about banking). Its two authors are also right to point out the defects of regulation in an IT-intensive era. But, in my opinion, they draw the wrong conclusions and the wrong reform proposals from their original assessment.

* Here again, their treatment of cash is unclear: can cash be withdrawn in a digital form and maintain in a digital wallet outside the financial system? I doesn’t look so from their book but I cannot say for sure.

Martin Wolf’s not so shocking shocks

Martin Wolf, FT’s chief economist, recently published a new book, The Shifts and the Shocks. The book reads like a massive Financial Times article. The style is quite ‘heavy’ and not always easy to read: Wolf throws at us numbers and numbers within sentences rather than displaying them in tables. This format is more adapted to newspaper articles.

Overall, it’s typical Martin Wolf, and FT readers surely already know most of the content of the book. I won’t come back to his economic policy advices here, as I wish to focus on a topic more adapted to my blog: his views on banking.

And unfortunately his arguments in this area are rather poor. And poorly researched.

Wolf is a fervent admirer of Hyman Minsky. As a result, he believes that the financial system is inherently unstable and that financial imbalances are endogenously generated. In Minsky’s opinion, crises happen. It’s just the way it is. There is no underlying factor/trigger. This belief is both cynical and wrong, as proved by the stability of both the numerous periods of free banking throughout history (see the track record here) and of the least regulated modern banking systems (which don’t even have lenders of last resort or deposit insurance). But it doesn’t fit Wolf’s story so let’s just forget about it: banking systems are unstable; it’s just the way it is.

Wolf identifies several points that led to the 2000s banking failure. In particular, liberalisation stands out (as you would have guessed) as the main culprit. According to him “by the 1980s and 1990s, a veritable bonfire of regulations was under way, along with a general culture of laissez-faire.” What’s interesting is that Wolf never ever bothers actually providing any evidence of his claims throughout the book (which is surprising given the number of figures included in the 350+ pages). What/how many regulations were scrapped and where? He merely repeats the convenient myth that the banking system was liberalised since the 1980s. We know this is wrong as, while high profile and almost useless rules like Glass-Steagall or the prohibition of interest payment on demand deposits were repealed in the US, the whole banking sector has been re-regulated since Basel 1 by numerous much more subtle and insidious rules, which now govern most banking activities. On a net basis, banking has been more regulated since the 1980s. But it doesn’t fit Wolf’s story so let’s just forget about it: banking systems were liberalised; it’s just the way it is.

Financial innovation was also to blame. Nevermind that those innovations, among them shadow banking, mostly arose from or grew because of Basel incentives. Basel rules provided lower risk-weight on securitized products, helping banks improve their return on regulatory capital. But it doesn’t fit Wolf’s story so let’s just forget about it: greedy bankers always come up with innovations; it’s just the way it is.

The worst is: Wolf does come close to understanding the issue. He rightly blames Basel risk-weights for underweighting sovereign debt. He also rightly blames banks’ risk management models (which are based on Basel guidance and validated by regulators). Still, he never makes the link between real estate booms throughout the world and low RE lending/RE securitized risk-weights (and US housing agencies)*. Housing booms happened as a consequence of inequality and savings gluts; it’s just the way it is.

All this leads Wolf to attack the new classical assumptions of efficient (and self-correcting) markets and rational expectations. While he may have a point, the reasoning that led to this conclusion couldn’t be further from the truth: markets have never been free in the pre-crisis era. Rational expectations indeed deserve to be questioned, but in no way does this cast doubt on the free market dynamic price-researching process. He also rightly criticises inflation targeting, but his remedy, higher inflation targets and government deficits financed through money printing, entirely miss the point.

What are Wolf other solutions? He first discusses alternative economic theoretical frameworks. He discusses the view of Austrians and agrees with them about banking but dismisses them outright as ‘liquidationists’ (the usual straw man argument being something like ‘look what happened when Hoover’s Treasury Secretary Mellon recommended liquidations during the Depression: a catastrophe’; sorry Martin, but Hoover never implemented Mellon’s measures…). He also only relies on a certain Rothbardian view of the Austrian tradition and quotes Jesus Huerta de Soto. It would have been interesting to discuss other Austrian schools of thought and writers, such as Selgin, White and Horwitz, who have an entirely different perception of what to do during a crisis. But he probably has never heard of them. He once again completely misunderstands Austrian arguments when he wonders how business people could so easily be misled by wrong monetary policy (and he, incredibly, believes this questions the very Austrian belief in laissez-faire), and when he cannot see that Austrians’ goals is to prevent the boom phase of the cycle, not ‘liquidate’ once the bust strikes…

Unsurprisingly, post-Keynesian Minsky is his school of choice. But he also partly endorses Modern Monetary Theory, and in particular its banking view:

banks do not lend out their reserves at the central bank. Banks create loans on their own, as already explained above. They do not need reserves to do so and, indeed, in most periods, their holdings of reserves are negligible.

I have already written at length why this view (the ‘endogenous money’ theory) is inaccurate (see here, here, here, here and here).

He then takes on finance and banking reform. He doubts of the effectiveness of Basel 3 (which he judges ‘astonishingly complex’) and macro-prudential measures, and I won’t disagree with him. But what he proposes is unclear. He seems to endorse a form of 100% reserve banking (the so-called Chicago Plan). As I have written on this blog before, I am really unsure that such form of banking, which cannot respond to fluctuations in the demand for money and potentially create monetary disequilibrium, would work well. Alternatively, he suggests almost getting rid of risk-weighted assets and hybrid capital instruments (he doesn’t understand their use… shareholder dilution anyone?) and force banks to build thicker equity buffers and report a simple leverage ratio. He dismisses the fact that higher capital requirements would impact economic activity by saying:

Nobody knows whether higher equity would mean a (or even any) significant loss of economic opportunities, though lobbyists for banks suggest that much higher equity ratios would mean the end of our economy. This is widely exaggerated. After all, banks are for the most part not funding new business activities, but rather the purchase of existing assets. The economic value of that is open to question.

Apart from the fact that he exaggerates banking lobbyists’ claims to in turn accuse them of… exaggerating, he here again demonstrates his ignorance of banking history. Before Basel rules, banks’ lending flows were mostly oriented towards productive commercial activities (strikingly, real estate lending only represented 3 to 8% of US banks’ balance sheets before the Great Depression). ‘Unproductive’ real estate lending only took over after the Basel ruleset was passed.

The case for higher capital requirements is not very convincing and primarily depends on the way rules are enforced. Moreover, there is too much focus on ‘equity’. Wolf got part of his inspiration from Admati and Hellwig’s book, The Bankers’ New Clothes. But after a rather awkward exchange I had with Admati on Twitter, I question their actual understanding of bank accounting:

While his discussion of the Eurozone problems is quite interesting, his description of the Eurozone crisis still partly rests on false assumptions about the banking system. Unfortunately, it is sad to see that an experienced economist such as Martin Wolf can write a whole book attacking a straw man.

* In a rather comical moment, Wolf finds ‘unconvincing’ that US government housing policy could seriously inflate a housing bubble. To justify his opinion, he quotes three US Republican politicians who said that this view “largely ignores the credit bubble beyond housing. Credit spreads declined not just for housing, but also for other asset classes like commercial real estate.” Let’s just not tell them that ‘Real Estate’ comprises both residential housing and CRE…

A couple of comments on ‘House of Debt’

I just read House of Debt, the latest book by Mian and Sufi, which got a relatively wide coverage in the media, so I thought I should write a quick post about it.

Overall, it’s a good book, accessible for those who do not have a background in economics or finance. What I particularly liked about the book is its emphasis on leverage. The boom in household and business leverage over the past two decades inevitably fuelled an unsustainable boom in aggregate spending. Bringing indebtedness back to more ‘normal’ values also inevitably reduces spending power*. Yet, too many economists seem to take this pre-crisis trend as normal.

They are also right to advocate letting banks fail, as well as question the non-monetary banking intermediation channel (as proposed by Bernanke in his famous article Non-Monetary Effects of the Financial Crisis in the Propagation of the Great Depression) and the effectiveness of monetary policy following a debt boom.

However, the authors never explain the underlying causes of the leverage boom and the crisis. It seems to be assumed that financial innovations (i.e. securitization mostly) appear all of a sudden, enabling an unsustainable boom to take place. What role did monetary policy play during the period? Or banking regulation? Those questions remain unanswered. Yet, as I’ve been explaining for now close to a year, the combination of those two factors was critical in triggering the boom in financial innovation, leverage, and malinvestments. I wish Mian and Sufi had provided their thoughts on that topic in their book.

They provide evidence that house prices increased the most in counties with inelastic housing supply. Still, they also strongly increased in those with elastic housing supply… They focus on the Asian ‘savings glut’, which would have flowed into the US. Perhaps, but it doesn’t mean that the Fed rate wasn’t too low, and many countries all around the world also experienced booming housing markets. Moreover, mortgage delinquencies started when the Fed increased its base rate… Despite being a US-centric book, there is also no discussion of the particular populist political framework at play in designing both the peculiar US banking system and the crisis, as described by Calomiris and Haber.

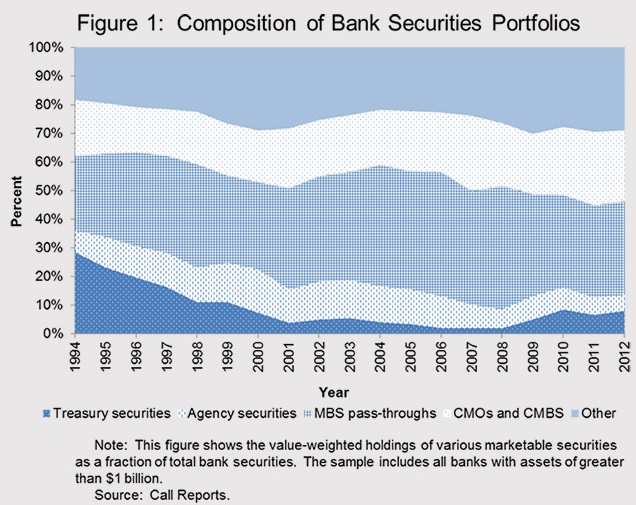

As a result, they seem to identify the rise in securitization as a fraud. I believe this is not the case. Banks started holding securitized assets on their balance sheet because of their beneficial capital treatment. There is little sign that they tried to originate bad assets to defraud naïve investors. Indeed, take a look at the chart below (from a recent post): banks also invested in such products and self-retained tranches of those they had originated throughout the boom period, and continue to do so. This points to ignorance of the risks. Not fraud.

I encourage you to read the book for its very good data gathering. Despite some of its (relatively minor) flaws, the book does much to debunk some myths through the appropriate use of empirical evidence.

* This doesn’t mean that there wasn’t also an excess demand for money at that time. Just that a decreased money supply through debt deflation exacerbated the problem.

Calomiris and Haber are pretty much spot on

I recently finished reading Fragile by Design, the latest book of Charles Calomiris and Stephen Haber.

Let’s get to the point: it’s one of the best books of banking I’ve had the occasion to read. It is a masterpiece of banking and political history and theory.

Calomiris and Haber describe the stability and efficiency of banking systems in terms of local political arrangements and institutions, which contrasts with most of nowadays’ theories that don’t distinguish between banking systems in various countries and way too often seem to draw conclusions on banking from the US experience only.

They describe banks’ stability in terms of a ‘Game of Banks Bargains’: the tendency for populists and bankers to form coalitions that aren’t favourable for society as a whole but favourable for politicians’ short-term political gains and bankers’ short-term profits. Needless to say, this alliance is built at the expense of long-term stability and efficiency. Only countries that have built political institutions to counteract the effects of populist policy proposals have experienced a stable financial environment since the early 19th century.

This thesis is extremely convincing and, while I find it unsurprising, it is so well documented that it is sometimes almost shocking. It clearly goes against mainstream Keynesian and Post-Keynesian theories, which consider financial collapses as a result of the normal process of human ignorance and panics. According to those theories, banks will fail at some point, hence the need for regulation and intervention early on. From most Keynesian books and articles I’ve read so far, collapses just happen. I’ve always been bewildered by the lack of underlying explanation: “that’s just the way it is”. Hyman Minsky’s Stabilizing an Unstable Economy is the perfect example: it draws general conclusions about the banking sector and the economy from a period of a couple of decades in the US… Knowledge of financial history quickly proves those arguments wrong.

The book isn’t without flaws however. It describes and compares the history of banking systems in England, the US, Canada, Mexico and Brazil. I found that either Brazil or Mexico could have been skipped (as covering both didn’t bring that much more to the thesis) in order to study more in depth another European (French, German, Italian) and/or Asian (Japanese, Indian…) banking system.

Also, while the (long) description of the political ramifications that led to the US subprime crisis is stunning, I believe the authors’ thesis is incomplete. There is no doubt that the populists/housing agencies/bankers alliance (or forced alliance) amplified the crisis by generating way too many low-quality housing loans through declining underwriting standards. However, this cannot be the only reason behind the crash. As I have described in many posts, properties have boomed and crashed all around the world in a coordinated fashion during the same period due to regulations incentivising house lending (and securitized products based on housing loans), as well as low interest rates. It is hard to argue that the Irish or the Spanish housing markets were the victims of US populists and US subprime lending…

Finally, what Calomiris and Haber describe is that free-market banking systems are less prone to systemic failures. From their work, it is clear that: 1. the fewer rules the banking system is subject to and 2. the less government intervention in the finance industry, the more stable the financial system. They demonstrate that the more lightly regulated Canadian system and the Scottish free-banking system were seen as almost ideal. Nevertheless, they seem to refrain from explicitly argue in favour of free-banking systems for some reason. I found this a little odd.

I certainly disagree with their view that banks can only exist when the state exists and charter them because of their interrelationship (i.e. states can raise financing through banks and banks get competitive advantages in return). Their arguments are really unconvincing: 1. it isn’t because such occurrences are rare in recent history that they cannot happen and 2. we have consistently witnessed throughout history, and in particular over the past decades, the spontaneous emergence of unchartered financial institutions (from money market funds to P2P lending firms) that respond to a private need for financial services. I do not think those are ‘utopian fantasies’ as this is happening right in front of us right now… States started to select, allow, charter and regulate those institutions when they needed finance. This does not imply that a limited and pacifistic state necessarily needs to use the same constraining tools.

In the end, those flaws remain minor and the book is easily one of my favourites. It deserves much more attention than what the media have given them so far (indeed, they go against the traditional ‘banking is inherently unstable’ tenet…). Unfortunately, the media are more interested in bank-bashing stories, putting in the spotlight much weaker books such as The Bankers’ New Clothes (by Admati and Hellwig)…

PS: FT’s John Kay also talks about the book here.

Felix Martin and the credit theory of money

I just finished reading a book that had been on my shelves for a few months, Money: The Unauthorised Biography, by Felix Martin (the book has only just been released in the US). Martin argues that our conventional view of money is wrong. Money isn’t a commodity used as a medium of exchange that evolved from the inconvenience of barter, but a system of mutual credit. Martin is not the first one to articulate this view, called the credit theory of money.

While overall Martin’s book is interesting, particularly for its historic descriptions and for bringing an ‘original’ view of the origins of money, it is plagued by a few problems and misinterpretations. Throughout the book, it feels like money, at least in its modern sense, is a ‘bad’ thing that is at the root of most of our current excesses, from inequality to financial crises. Perhaps, but the book never really discusses monetary calculation and economic efficiency. Money might have cons, but it also has pros. The fact that some ancient, very hierarchical – or even totally backward, societies were not using such ‘money’ is in no way something to be worried about…

Throughout his book, Martin seems to misinterpret former authors’ writings. Take Bagehot, whom Martin believes understood money and trust a lot better than most academic economists since then. Martin incorrectly reports Bagehot as saying that central banks should lend to insolvent banks. More importantly, he also didn’t seem to notice that Bagehot had never been a fan of the central banking system. In fact, Bagehot thought that system was not natural and even dangerous. This becomes a serious flaw of the book when Martin justifies his economic and reform ideas on a system that Bagehot himself saw as far from perfect.

Martin also seems to praise inflation without ever mentioning its downsides and the potential economic disruptions it can bring about. In turn, this leads him to praise… John Law. While John Law is most of the times seen as a model of economic mismanagement, Martin sees in him a ‘genius’, whose only faults was to have lived too early and to have believed in benevolent dictators:

Law’s system was ingenious, innovative and centuries ahead of his time.

To Martin, John Law’s system mainly failed because of… the vested interests of the old financial establishment! As with most other topics the book cover, I found this was a very selective reading of the historical facts.

This is the book’s main issue: it draws the wrong conclusions from a very superficial reading of history (including our latest financial crisis).

The book’s main thesis (admittedly, it’s also other people’s) suffers from the same problem. Why opposing credit theory of money and metalism? To me money can be both credit and commodity. This is not irreconcilable. Let’s suppose you provide me with a service or a product. The consequence of this transaction is that I am in credit to you. From there, what can you do? To settle the transaction, you can either accept one of my products or services. This is barter. Or you could use my ‘debt’ to you (my IOU) to purchase another product from someone else. However, in order to accept the ‘debt transfer’, the other person needs to make sure that my credit is good (i.e. that I will close the transaction at some point) in order to reduce the probability of losses (i.e. credit risk). This other person can further transfer my IOU, which ends up serving as money in a chain of transactions. Nevertheless, settlement (i.e. debt cancellation) is still expected at some point, and with no generally accepted medium of exchange, this settlement is similar to barter. This system still suffers from lack of granularity and from the double coincidence of wants problem.

Enter commodities. Excluding its barter-like issues, the process described above works, but involves credit risk. Developed societies discovered a way to reduce this credit risk to a minimum: a direct settlement of the IOU against what we view as the same value of a granular, easily transferable and measurable commodity. Think about it: you can either take the risk that my IOU will not be transferable any further or that I will fail to close the transaction, or you can settle the transaction directly by accepting some sort of commodity in exchange, which makes credit risk entirely disappear. But the system remains a system of credit: the only difference now is that IOU transfer chains end directly after the first transaction. This is still valid nowadays: everybody still says “how much do I owe you?” in order to pay for a good in store*.

(Note: of course if my credit is good, my IOU could still be transferred and ‘used’ as a medium of exchange, but would still merely remain a claim on the same easily transferable commodity.)

Strangely, Martin seems to downplay the settlement issue. He takes the Yap islands as an example of a pure system of credit money. But this is not accurate: Martin himself says that locals eventually settle their mutual debt using stone money (the fei/rai)!

I ended up quite confused about the book. It is hard to figure out what Martin really believes. Some of his proposals, such as money that would be some sort of state equity, look unworkable and closer to statist dreams than economic freedom; although this shouldn’t be surprising, as Martin never really questions the state, regulators and central bankers, and blindly accepts the Keynesian criticism of Say’s law. Money is more a history book than an economics book, but whether this is financial history or monetary theory you’re looking for, there is already a lot more comprehensive out there.

*The story I just described is essentially similar to Carl Menger’s theory of the origins of money. However, I added in a new factor: credit risk.

Recent Comments