Lars Christensen on Yellen and bubbles, and UK regulators at full speed

Lars Christensen published a sarcastic post on his blog, which coincidentally treats the monetary policy and bubbles problem as the same time as my previous post. I fully agree with him that Yellen’s comments are ridiculous.

This is Lars:

it seems to part of a growing tendency among central bankers globally to be obsessing about “financial stability” and “bubbles”, while at the same time increasingly pushing their primary nominal targets in the background.

While I agree with Lars that central banks should provide ‘nominal stability’, I don’t think inflation targeting provides such framework (and I believe Lars agrees). Inflation is very hard to measure, let alone to define, and can be very misleading (Scott Sumner believes that inflation indicators are meaningless). According to a Wicksellian framework, it does look like something’s wrong with interest rates at the moment. Banking regulation, due to its roles in ‘channelling’ interest rates, surely also plays a big role that monetary policy cannot influence. In the end, maintaining inflation right on target is in no way insurance of actual nominal (and financial) stability.

David Beckworth, in a new paper published a few days ago, also criticised inflation targeting on the ground that it contributes to financial instability. I agree with Market Monetarists that a policy stabilising NGDP growth would provide a more robust economy and financial system, though it is in my view still imperfect (I’ll come back to that in another post).

Totally unrelated: in the UK, regulators are working at full speed. Here is a summary of some of the latest regulatory announcements:

- Regulators believe that asset managers ‘waste’ too much client money on sell-side analysts research and want to regulate the process, risking to transform the market into an oligopoly as smaller research providers may not be able to cope with the reduced fee-generation (see here and here)

- HMRC wants to get the power to access your bank account and check your spending habits without going through court to make sure that you are able to pay the taxes they claim you owe them (even if they are wrong). I have personally dealt many times with HMRC (I didn’t owe them money, they did) and the least I can say is that it wasn’t necessarily a pleasant experience: waiting 45min on the phone to end up speaking to someone who sounds very suspicious that you are trying to trick tax authorities… (to be fair, I also ended up speaking to competent and pleasant people) HMRC makes mistakes all the time and I would be very cautious in granting them such powers… (see here and here)

- New rules capping the fees payday lenders can charge are effectively about to kill a large number of them… It probably won’t help much (see here)

- Bank account holders aren’t taking advantage of the best offers available to them and don’t spend their time constantly changing bank to get the best pricing and as a result earn poor returns? The regulator also wants to change that, though I submit that it should tell his boss (the BoE) that, if savers indeed earn poor returns, it possibly is because rates aren’t very high… (see here)

- The BoE and PRA want global banking regulators to reduce RWAs or capital requirements for small banks. Not saying this is a bad thing, but this sounds kind of contradictory to me, given everything we’ve been hearing for years from the same regulators… (see here)

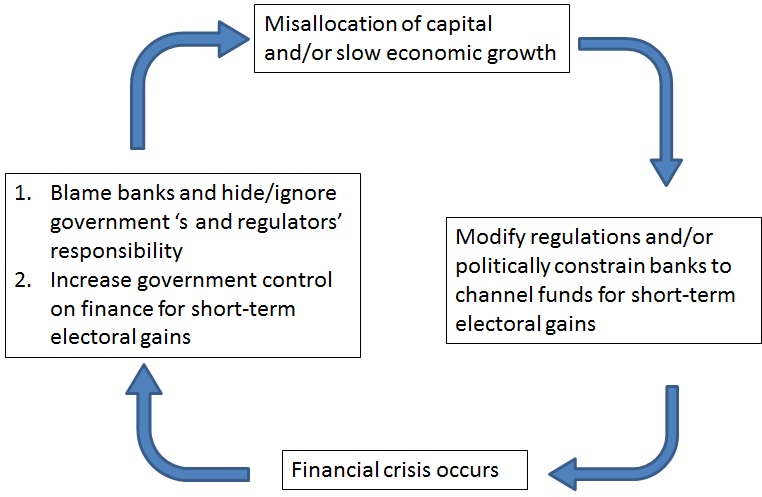

The political banking cycle

A couple of weeks ago, The Economist reported that Mel Watt, the new regulator of the US federal housing agencies Fannie Mae and Freddie Mac, wanted those two agencies to stop shrinking and continue purchasing mortgage loans from banks in order to help homeowners and the housing market (also see the WSJ here). To twist the system further, the compensation of the agencies’ executives will be linked to those political goals. Mr Watt used to be one of the main proponents of more accessible house lending for poor households through Fannie and Freddie before the crisis.

As The Economist asks, “what could go wrong?”…

Lars Christensen and Scott Sumner also find this ridiculously misguided government intervention horrifying. I find myself in complete agreement (and this is an understatement). Who could still honestly say that we are (or were) in a laissez-faire environment?

This, along with UK’s FLS and Help to Buy schemes, made me think that there has been a ‘political banking cycle’ throughout the 20th century. Why 20th century? From all the banking history I’ve read so far, populations seemed to better understand banking before the introduction of safety net measures such as central banks, deposit insurances or systematic government bail-outs. When financial crashes occurred, blame was usually shared between governments and banks, if not governments only. This is why many crises triggered deregulation processes rather than reregulation ones. This contrasts with the mainstream view our society has had since the Great Depression: when a financial crash happens, whatever the government’s responsibility is, banks and free market capitalism are the ones to blame.

This political cycle looks like that:

The worst is: it works. Politicians escaped pretty much unscathed from the financial crisis despite the huge role they played in triggering it*. The majority of the population now sincerely believes that the crisis was caused by greedy bankers (see here, here, here and here). This is as far from the truth as it can be (I don’t deny ‘greed’ played a role though, but channelled through and exacerbated by a combination of other factors, i.e. moral hazard etc.). Unfortunately, it is undeniable: politicians won. And not only politicians won, but they also managed to self-convince that they played no role in the crisis, as the example of Mr Watt shows (he either truly believes that government intervention in the US housing market was a good thing, or he has an incredibly cynical short-term political view).

The crucial question is: why did 19th century populations seem more educated about banking? The answer is that the lack of state paternalism through various protection schemes forced bank depositors and investors to oversee and monitor their banks. Once protection is implemented, there is no incentive or reason anymore to maintain any of those skills.

Who is easier to manipulate: a knowledgeable electorate or an ignorant one?

PS: This chart is mostly accurate for democracies that have a populist tendency. Not all countries seem to be prone to such cycle (this can be due to cultural or institutional arrangements).

* I won’t get into the details here, but if you’re interested, just read Engineering the Financial Crisis, Fragile by Design or Alchemists of Loss……. or simply this NYT article from 1999.

The BoE’s FLS delusion

The Bank of England reported yesterday the latest statistics of one of its flagship measures, the Funding for Lending Scheme. Unsurprisingly, they are disappointing. No, more than that actually: the FLS has been pretty much useless.

When launched mid-2012, the FLS was supposed to offer cheap funding to British banks in exchange for increased business and mortgage lending (though originally, authorities strongly emphasised SMEs in their PR as you can imagine) in order to ‘stimulate the economy’. The only effect of the scheme was to boost… mortgage lending.

The BoE, unhappy, decided to refocus the scheme on businesses (including SMEs) only, in November last year. Well, as I predicted, it was evidently a great success: in Q114, net lending to businesses was –GBP2.7bn and net lending to SMEs was –GBP700m. Since the inception of the scheme, business lending has pretty much constantly fallen (see chart below).

According to the FT:

Figures from the British Bankers’ Association showed net lending to companies fell by £2.3bn in April to £275bn, the biggest monthly decline since last July.

The BoE argues that we don’t know what would have happened without the scheme. Perhaps lending would have fallen even more? That’s a poor argument for a scheme that was supposed to boost lending, not merely reduce its fall. Not even all large UK banks participated in the scheme (HSBC and Santander didn’t). Moreover, some banks withdrew only modest amounts because they could already access cheaper financial markets by issuing covered bonds and other secured funding instruments, or, if they couldn’t, used the FLS to pay off existing wholesale funding rather than increase lending… The FLS funding that did end up being used to lend was effective in boosting… the mortgage lending supply.

The UK government has also ‘urged’ banks to extend more credit to SMEs. Still, nothing is happening and nobody seems to understand why. For sure, low demand for credit plays a role as businesses rebuild their balance sheet following the pre-crisis binge. Still, nobody seems to understand the role played by current regulatory measures. Central bankers are supposed to understand the banking system. The fact that they seem so oblivious to such concepts is worrying.

On the one hand, you have politicians, regulators and central bankers trying to push bankers to lend to SMEs, which often represent relatively high credit risk. On the other hand, the same politicians, regulators and central bankers are asking the banks to… derisk their business model and increase their capitalisation. You can’t be more contradictory.

The problem is: regulation reflects the derisking point of view. Basel rules require banks to increase their capital buffer relatively to the riskiness of their loan book; riskiness measures (= risk-weighted assets) which are also derived from criteria defined by Basel (and ‘validated’ by local regulators when banks are on an IRB basis, i.e. use their own internal models).

Those criteria require banks to hold much more capital against SME exposures than against mortgage ones. Banks that focus on SMEs end up squeezed: risk-adjusted SME lending return is not enough to generate the RoE that covers the cost of capital on a thicker equity base. Banks’ best option is to reduce interest income but reduce proportionally more their capital base to generate higher RoEs. Apart from lending to sovereigns and sovereign-linked entities, the main way they can currently do that is to lend… secured on retail properties…

(I have already described here how this process creates misallocation of capital and possibly business cycles)

As such, it is unsurprising that mortgage lending never turned negative in the UK (even a single month) throughout the crisis. Even credit card exposures haven’t been cut by banks, as their risk-adjusted returns were more beneficial for their RoE than SMEs’. Furthermore, alternative lenders, who are not subject to those capital requirements, actually see demand for credit by SMEs increase (see also here).

Let’s get back to the 29th of November 2013. At that time, after it was announced that the FLS would be modified, I declared:

RWAs are still in place! Mortgage and household lending will still attract most of lending volume as it is more profitable from a capital point of view.

Well…

As long as those Basel rules, which have been at the root of most real estate cycles around the world since the 1980s, aren’t changed, SMEs are in for a hard time. And economic growth too in turn. Secular stagnation they said?

PS: this topic could easily be linked to my previous one on intragroup funding and regulators “killing banking for nothing”. Speaking of the ‘death of banking’, Izabella Kaminska managed to launch a new series on this very subject without ever saying a word about regulation, which is the single largest driver behind financial innovations and reshaped business models. I sincerely applaud the feat.

PPS: The FT reported how far regulators (here the FCA) are willing to go to reshape banking according to their ideal: equity research in the UK is in for a pretty hard time. This is silly. Let investors decide which researchers they wish to remunerate. Oversight of the financial sector is transforming into paternalism, if not outright regulatory threats and uncertainty.

PPS: I wish to thank Lars Christensen who mentioned my blog yesterday and had some very nice comments about it.

Inside regulator trading

While some people keep praising the virtues of regulation on anything and everything (see Izabella Kaminska here on Bitcoin), a brand new study seems to picture a slightly less rosy view of regulators…

(This research was originally pointed by Lars Christensen on his blog and Facebook account. Thank you again Lars)

The abstract is telling:

We use a new data set obtained via a Freedom of Information Act request to investigate the trading strategies of the employees of the Securities and Exchange Commission (SEC). We find that a hedge portfolio that goes long on SEC employees’ buys and short on SEC employees’ sells earns positive and economically significant abnormal returns of (i) about 4 % per year for all securities in general; and (ii) about 8.5% in U.S. common stocks in particular. The abnormal returns stem not from the buys but from the sale of stock ahead of a decline in stock prices. We find that at least some of these SEC employee trading profits are information based, as they tend to divest (i) in the run-up to SEC enforcement actions; and (ii) in the interim period between a corporate insider’s paper-based filing of the sale of restricted stock with the SEC and the appearance of the electronic record of such sale online on EDGAR. These results raise questions about potential rent seeking activities of the regulator’s employees.

Wait. Do you mean that Securities and Exchange Commission employees are humans like anybody else, driven by their own sense of greed? Amazing.

A few absolutely striking facts were listed in this paper. The SEC lacked a system to monitor employees’ trades until… 2009. Despite the system implemented early 2009, employees seem to be able to avoid large losses by selling their holdings just before a negative SEC decision is announced. Moreover, previous research also found that politicians and congressmen benefited from insider trading… A law was passed in… 2012 to prevent them from trading on privileged information. 2012! They must be kidding. How late is that?! The logic seems to be: impose red tape on corporations ASAP but please do not affect rent-seeking and other benefits of government officials! The effectiveness of the law still has to be researched…

For sure there are some limitations to this paper and its methodology: the authors only effectively analysed 7,200 transactions out of a total of 29,081. This is because many transactions had invalid tickers (some were mutual funds but… how is even this possible for other securities?), were not traded on American exchanges or had very limited data due to illiquidity. Moreover, they couldn’t identify individual employees and as a result worked on an aggregate portfolio. It is also fair to admit that the ‘abnormal return on short positions’ actually didn’t generate any profit but only prevented losses, as they were not short sales but outright ones.

Still, independently of our view of insider trading (many people argue that it isn’t such a bad thing after all), such results are significant and should be further researched. Regulators like to portray themselves as being on a moral high ground, shaming those guilty of insider trading and other frauds. So the news that they may well succumb to the same temptation as those vulgar and immoral capitalist insiders not only sounds very ironic but also reaches extreme levels of cynicism.

As Lars said:

Who is regulating the regulators?

A UK housing bubble? Sam Bowman doubts it

On the Adam Smith Institute’s blog, Sam Bowman had a couple of posts (here and a follow-up here, and mentioned by Lars Christensen here) attempting to explain that there might not have been any house price bubble in the UK. He essentially says that there was no oversupply of housing in the 1990s and 2000s. Here’s Sam:

These charts show that housing construction was actually well below historical levels in the 1990s and 2000s, both in absolute terms and relative to population. It is difficult to see how someone could claim that the 2008 bust was caused by too many resources flowing toward housing and subsequently needing time to reallocate if there was no bubble in housing to begin with.

What this suggests is that the Austrian story about the crisis may be wrong in the UK (and, if Nunes’s graphs are right, the US as well). The Hayek-Mises story of boom and bust is not just about rises in the price of housing: it is about malinvestments, or distortions to the structure of production, that come about when relative prices are distorted by credit expansion.

Well, I think this is not that simple. Let me explain.

First, the Hayek/Mises theory does not apply directly to housing. In the UK, there are tons of reasons, both physical and legal, why housing supply is restricted. As a result, increased demand does not automatically translate into increased supply, unlike in Spain, which seems to have lower restrictions as shown by the housing start chart below:

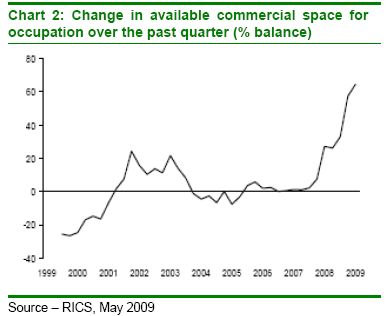

Second, Sam overlooks what happened to commercial real estate. There was indeed a CRE boom in the UK and CRE was the main cause of losses for many banks during the crisis (unlike residential property, whose losses remained relatively limited).

Third, the UK is also characterised by a lot of foreign buyers, who do not live in the UK and hence not included in the population figures. Low rates on mortgages help them purchase properties, pushing up prices, triggering a reinforcing trend while supply in the demanded areas often cannot catch up.

Fourth, the impact of Basel regulations seems to be slightly downplayed. Coincidence or not, the first ‘bubble’ (in the 1980s) appeared right when Basel’s Risk Weighted Assets were introduced. And it is ‘curious’, to say the least, that many countries experienced the same trend at around the same time. Would house lending and house prices have increased that much if those rules had never been implemented? I guess not, as I have explained many times. I have yet to write posts on what happened in several countries. I’ll do it as soon as I find some time.

I recommend you to take a look at my RWA-based Austrian Business Cycle Theory, which seems to show that, while there should indeed be long-term real estate projects started (depending on local constraints of course), there is also an indirect distortion of the capital structure of the non-real estate sector.

While there may well be ‘real’ factors pushing up real estate prices in the UK, there also seems to be regulatory and monetary policy factors exacerbating the rise.

- Chart 1: Spanish Property Insight

- Chart 2: FT Alphaville

- Chart 3: Guardian

Macro(un)prudential regulation

From a free-market perspective, one can only be against macroprudential regulation. Macroprudential regulation is the new fashion among regulators and other policy-makers. It’s trendy, and I understand why: it sounds clever enough to impress friends during a night out. It aims at monitoring a few macroeconomic indicators in order to try to ‘cool’ the system if it seems to be overheating. Those tools are supposed to be countercyclicals: if the economic environment is good, regulators can force the whole banking system to start accumulating extra equity or liquid assets for example, or decide to cap the amount that all banks can lend to mortgage borrowers. As you can guess, it is not the kind of self-regulating financial system I particularly appreciate.

This is once again a typical example of trying to fix the symptoms created by the system’s defects, without touching those defects. Wrong monetary policy? Bad government policies and subsidies? Of course not, the financial system is inherently bad and fragile, regulators and politicians said. Well, to be fair, this is their job and how they make money.

Lars Christensen, chief analyst at Danske Bank and author of The Market Monetarist blog, had a couple of niece pieces against macroprudential regulation recently. In the first one, he quotes and agrees with a recent WSJ article by John Cochrane, financial economist at the University of Chicago (also available on his blog):

This is Cochrane:

Interest rates make the headlines, but the Federal Reserve’s most important role is going to be the gargantuan systemic financial regulator. The really big question is whether and how the Fed will pursue a “macroprudential” policy. This is the emerging notion that central banks should intensively monitor the whole financial system and actively intervene in a broad range of markets toward a wide range of goals including financial and economic stability.

For example, the Fed is urged to spot developing “bubbles,” “speculative excesses” and “overheated” markets, and then stop them—as Fed Governor Sarah Bloom Raskin explained in a speech last month, by “restraining financial institutions from excessively extending credit.” How? “Some of the significant regulatory tools for addressing asset bubbles—both those in widespread use and those on the frontier of regulatory thought—are capital regulation, liquidity regulation, regulation of margins and haircuts in securities funding transactions, and restrictions on credit underwriting.”

This is not traditional regulation—stable, predictable rules that financial institutions live by to reduce the chance and severity of financial crises. It is active, discretionary micromanagement of the whole financial system. A firm’s managers may follow all the rules but still be told how to conduct their business, whenever the Fed thinks the firm’s customers are contributing to booms or busts the Fed disapproves of.

I completely agree with Cochrane.

And I completely agree with both of them. Christensen argues that the central bank’s goal is to provide nominal stability – to have a single target and stick to it, but that macroprudential regulation would involve manipulating many different tools having opposite effects, with likely unintended consequences. He then goes on to argue that if “markets are often wrong”, central banks are even worse and “have a lousy track record” at spotting bubbles.

Another important point made by Cochrane in my opinion is:

Third lesson: Limited power is the price of political independence. Once the Fed manipulates prices and credit flows throughout the financial system, it will be whipsawed by interest groups and their representatives.

= crony capitalism. This has plagued all corners of our capitalist system for ages, and when things turn bad, free markets/laissez-faire capitalism/liberalism/neoliberalism/ultra turboliberalism/add the one you want is blamed… Go figure.

Christensen’s second post, published a few days ago, refers to a Bloomberg article on the so-called ability of a new Finnish model to ‘forecast’ all cyclical up and downswings in the US over the past 140 years… He helpfully remembers that nobody is ever able to constantly beat the market. While this sounds like a rational expectations/efficient market hypothesis point of view (I don’t know what Lars actually believes in), I do agree with him (and no I don’t believe in rational expectations, but constantly beating the market requires non-human skills and information-gathering abilities). He then goes on to say that while this is relatively basic economics, “nowadays central bankers increasingly think they can beat the markets. This is at the core of macroprudential thinking.”

Obviously, the whole thing rests on the myth that the financial system is fragile and must be ‘safeguarded’ or ‘protected’ (see this IMF article) by ‘benevolent dictators’, in Christensen’s words. I would also add that macroprudential ideas are now new and have been already tried one way or another since the early 19th century (but how many regulators and economists remember that? See an example here).

This is how I see things: no central body can ever have perfect knowledge of what’s happening in the economy and what the various plans, wishes and wants of the millions of actors in the system are (I am obviously not the first one to say this. See Mises, Hayek, Friedman and so many others). As a result, any central intervention is bound to fail or create distortions in the economic landscape.

Central banks are a monopoly: they define nominal interest rates and base money supply unilaterally and can only adjust their policies with a time lag, after they have already affected the economy. A distorting monetary policy can easily kickstart asset bubbles: an increasing supply of ‘high-powered’ money (base money) not matched by an increase in the demand for money can easily lead to excess credit creation. If real estate prices boom due to the flow of credit towards the sector, is it reasonable to try to stop it? The flow of credit is already here, and if it cannot go where it wanted in the first place, it will find another place to go to. China and its wealth management products is a good example of this process.

Let’s consider a current example in the UK. Due to a combination of interest rates maintained too low for too long, misguided government schemes such as Funding for Lending and Help to Buy, compounded by Basel regulations that favour mortgage lending and local restrictions on housing supply, if ever a housing bubble appears, the solution will be to… blame the banks and artificially restrict LTVs or cap lending??? Right…

Finance is a spontaneous process: people can be very innovative at finding ways of bypassing restrictions to achieve their desired financing and saving goals. Macroprudential controls would only move the problem from one sector to another, without correcting its very source. Macroprudential regulation would also introduce an unwelcome dose of discretionary rules and micromanagement, which have destabilising effects on trust, markets and economic actors.

Photograph: Wikipedia

Recent Comments