Clarifying confusions on capital requirements

As the Trump administration is considering scrapping parts of the enormous Dodd-Frank act, a number of media and economists look alarmed: Dodd-Frank made the American banking system safer, the argument goes, and getting rid of it would lead to another financial crisis.

While long-time readers of this blog know that Dodd-Frank, and the Basel 3 international accords it is based on, merely continue the mistakes of three decades of regulatory overreach that have brought about the largest financial crisis in decades, I thought it was necessary to clarify a couple of points regarding capital requirements.

In this week’s Economist, two articles seem to admit that, while the act indeed represented an unclear regulatory monster of thousands of pages that mostly penalised smaller financial institutions, it also made the system safer by reinforcing banks’ capitalisation.

In an editorial, the newspaper asserts that:

Onerous though it is, however, the act also achieved a lot. Measures to beef up banks’ equity funding have made America’s financial system more secure. The six largest bank-holding companies in America had equity funding of less than 8% in 2007; since 2010 that figure has stood at 12-14%.

In another article, it adds:

Thanks in part to Dodd-Frank, America’s banks are far safer than they were: the ratio of the six largest banks’ tier-1 capital (chiefly equity) to risk-weighted assets, the main gauge of their strength, was a threadbare 8-9% before the crisis; since 2010 it has been 12-14%.

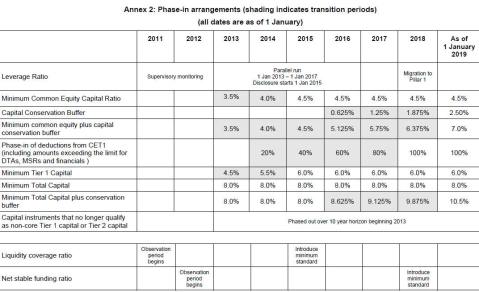

But it is far from clear that Basel requirements are behind banks’ post-crisis thicker capital buffers. See Basel 3 minimum capital requirements below:

Minimum Tier-1 capital requirements are 7.875% (Tier 1 + capital conservation buffer). This is around 2008 level for large US banks. Hardly an improvement at first glance then.

However, let’s also add the recent SIFI capital surcharge, published by the FSB last November: only two institutions qualified for a 2.5% surcharge (only one of them US-based), but let’s add it this figure to our minimum above. We get to a SIFI minimum Tier 1 requirement of 10.375%. This is still an almost 2 to 4% gap with the 12% to 14% average referred to by The Economist above.

Therefore the only conclusion is that there are other parameters and considerations influencing the level of capital ratios upward. One of those parameters is indeed regulatory-related, but is discretionary at bank-level: it is bankers’ own view about the capital buffer they believe they need above the regulatory minimum in order to avoid breaching it in case of sudden large losses. This shows some of the perverse side-effects of strict minima, and I described some time ago that the ‘effective’ capital ratio was actually the differential between the level maintained by the bank and the regulatory minimum. And this ‘effective’ buffer tends to narrow rather than thicken as minima are raised.

The second is exogenous to bank’s decision making-process: the financial crisis has taught a number of investors not to get fooled by headline regulatory capital ratios. Consequently, investors now ask for higher levels of capital in order to compensate for the lack of clarity regarding the quality of capital*. Given that risk-weights (another regulatory construct) have a considerable influence on the level of capital ratios, investors also ask for extra capital buffers to compensate for the distortions they inevitably introduce in the headline figures.

Consequently, had minimal requirements stayed the same, investors would have been highly likely to demand extra protection against the uncertainty introduced by…..those same regulatory requirements.

In the end, the assumption that banks are much better capitalised and that regulation/Dodd-Frank is responsible for this is questionable.

*While Basel 3 and Dodd-Frank have indeed also touched upon the issue of capital quality, it remains unclear how a number of so-called hybrid, or ‘complementary Tier 1’, instruments will perform under stress and legal challenges.

PS: this blog post could have entered into a lot more details about the parameters driving the thickness of capital buffers, but it would then have to be split into 3 or 4 different posts. At least. So please read some of my other posts on the topic to get the bigger picture as this is a complex issue.

Recent Comments