Risk-weighted assets and capital manipulations

As some of you might have noticed, the Bank of International Settlements published yesterday the final version of the Basel III leverage ratio (official report can be found here). This ratio is a measure of the capitalisation of a bank for regulatory purposes. I have already mentioned a few times those capital ratios. Since the first Basel regulations were introduced, capital ratios were based on risk-weighted assets (RWAs). Some of you might already be aware of my ‘love’ of RWAs… The leverage ratio, on the other hand, gets rid of RWAs.

I am not going to speak about the leverage ratio here. But about other two other related BIS studies that, in a way, legitimate the use of unweighted capital ratios. In January 2013, the BIS published a first analysis of market RWAs. They tried to estimate the variability of risk-weights associated to equivalent securities across banks. The BIS provided 26 portfolios of financial securities to 16 different banks and asked them to risk-weigh them according to their internal models. The results were shocking (but not surprising).

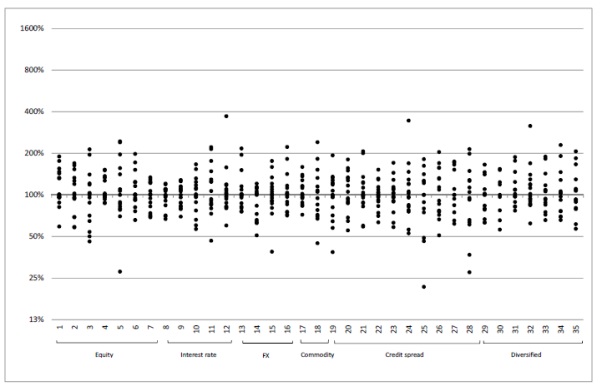

Banks mostly assess market risks using statistical Value-at-Risk models. The graph below shows the dispersion of the results provided by the banks’ VaR models. The results are normalised so that the median result is centred on 100%.

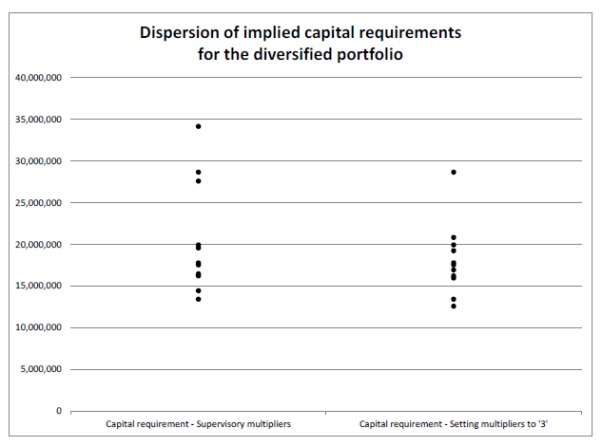

The dispersion is huge. Some banks judged portfolio 14 as being around 1000% riskier than the median bank’s perception of it (and I am not even talking about the most conservative one). Some comfort could be taken from the diversified portfolios (25 and 26), which are closer to real life portfolios. Nonetheless, even in those, variations are large enough to undermine the credibility of the risk-weights applied to them. The chart below demonstrates the capital requirements (in Euros) implied from the VaR results above for portfolio 25. Some banks would put aside more than twice the amount of capital than others would, for the same portfolio of securities.

The BIS believed at that time that different local regulatory requirements were partially responsible for the results (such as some banks following Basel 2.5 and others Basel 2. I’m going to skip the details but Basel 2.5 pushes market RWAs up).

The BIS eventually published its final study on market RWA at the end of December. This time, all banks had implemented Basel 2.5. So most of the observed variation could only come from the banks’ internal model differences. What did they find?

Not much difference. Variations were still huge. The resulting implied capital requirements (in thousands of Euros) for portfolios 29 and 30 were as follows:

Clearly, RWAs are unreliable. This questions the very utility of RWA-based regulatory capital ratios. How can one actually trust two different banks both reporting 10% Tier 1 ratios? One of them might in reality hold twice as little capital as the other one for what is actually the same risk level. Banks can easily game the system. Moreover, the FT was reporting yesterday that some banks were starting to report RoRWA (return on RWAs) instead of more traditional return on equity or return on assets. But those measures suffer from the exact same defects. While an unweighted leverage ratio is clearly not perfect, RWAs introduce far too much information distortion and even potentially exacerbate the business cycle. Time to get rid of them.

Banks’ RWAs as a source of malinvestments – Some recent empirical evidence

A recent study by academics from the Southern Methodist University and the Wharton School of the University of Pennsylvania had very interesting findings (the actual full paper can be found here): banks based near booming housing markets charged higher interest rates and reduced loan amounts to companies, which ended up investing less than companies borrowing from banks located in stable (or falling) housing markets. They called this the “crowding-out effect of house-price appreciation”. The study gathered data from 1988 to 2006 in the US, during the Basel period. It would have been interesting to compare with the pre-Basel era and replicate it with European markets.

Conventional economic knowledge seemed to think that “to the extent that home prices begin to rise, consumers will feel wealthier; they’ll feel more disposed to spend…that’s going to provide the demand that firms need in order to be willing to hire and to invest.” (This is Ben Bernanke as quoted by The Economist, which mentioned this study a few weeks ago)

But our academics instead found an inverse relationship:

We estimate that a one standard-deviation increase in housing prices (about $79,700 in year 2000 dollars) that a bank is exposed to decreases investment by firms related to that bank by almost 6.3 percentage points, which is approximately 12% of a standard deviation for firm investment. Banks also increase the interest rate charged by 9 basis points, reduce outstanding loans by approximately 9%, and reduce loan size by approximately 4.5%. These results are consistent with banks reducing the supply of capital to firms in response to increased housing prices.

So much for the Keynesianism of housing bubbles…

Their findings was summarised in an easier to read single chart by The Economist:

I think they are spot on in identifying this crowding out effect but overlook the underlying importance of Basel’s risk-weighted assets in triggering the boom and forcing the reallocation of capital towards housing. In their paper, there is not a single reference to Basel, banks’ capital requirements (apart from one related to MBS) and RWAs. But their story matches almost perfectly the RWA-based ABCT model I described in my previous post on the topic.

What did my model say? That the supply of loanable funds would be reduced to businesses and increased to real estate as a result of capital-optimising choices made by banks (because of RWAs capital constraints). That consequently, interest rates would increase for businesses and be reduced for real estate. This is exactly what they found.

But it doesn’t stop here. The model also said that an increase in interest rates to businesses would shorten their structure of production as interest-sensitive long-term investments become unprofitable. What did they find? That businesses reduced investments despite the temporary boost in consumption due to the well-referenced wealth effects (which they also mentioned)…

However, they missed the deeper implications of banking regulation on the reallocation of capital from businesses to real estate. To them, house price increases seems to be the only factor diverting capital towards housing. I don’t deny that increasing house prices would bring about self-reinforcing house lending, even in a free market: as house prices increase, lending gets facilitated and speculators are attracted, pushing prices up even further. But my point is that regulation and RWAs can both trigger and exacerbate the process way beyond the self-correcting point at which it would normally stop (and collapse) in a free market environment.

There is catch though… If RWAs do indeed trigger a boom in house lending, how could they find some areas in the US within which the process actually wasn’t triggered (no increase in house prices/lending) despite being subject to the same regulatory framework? Well, there are possibly a few answers to that question. Some local banks could actually be in an area experiencing falling house prices for some reason (even though they increase nationally) and low mortgage demand. This would automatically limit the amount they lend and push RWAs on real estate up, making housing less attractive from a capital-optimisation point of view. Another possibility would be that those local banks are actually subsidiaries of other banks that try to optimise capital usage on an aggregate (national) basis. However, it is hard to say as the criteria used to build the sample of banks are not clear.

There is another, simpler, possible explanation: even in falling housing prices areas, local banks’ business lending was still constrained and mortgage lending still supported! Meaning that, in a RWA-free world (and excluding a recessionary environment), a decline in housing prices would have triggered an even sharper decrease/increase in mortgage/business lending. This cannot be proved with this study however. There could also be other explanations that haven’t come to my mind yet.

Overall, I remain slightly sceptical of statistical/regression/correlation-based economic studies and I’ll take this one with a pinch of salt, especially as they use various assumptions and proxies that could easily distort the outcome. Nonetheless, the results they obtained were quite significant. And they provide some empirical evidences to my very theoretical model.

Meanwhile, Nouriel Roubini on Friday, in a piece called Back to Housing Bubbles, listed all the markets in which there are signs of bubbles:

[…] signs of frothiness, if not outright bubbles, are reappearing in housing markets in Switzerland, Sweden, Norway, Finland, France, Germany, Canada, Australia, New Zealand, and, back for an encore, the UK (well, London). In emerging markets, bubbles are appearing in Hong Kong, Singapore, China, and Israel, and in major urban centers in Turkey, India, Indonesia, and Brazil.

Real estate bubbles existed before Basel introduced risk-weighted assets, but nothing on that scale and in so many countries at the same time. Time for policy-makers to wake up.

RWA-based ABCT Series:

- Banks’ risk-weighted assets as a source of malinvestments, booms and busts

- Banks’ RWAs as a source of malinvestments – Update

- Banks’ RWAs as a source of malinvestments – A graphical experiment

- Banks’ RWAs as a source of malinvestments – Some recent empirical evidence

- A new regulatory-driven housing bubble?

Cato Institute’s 31st Monetary Conference – Was the Fed a good idea?

About two weeks ago, the US-based think tank Cato organised its annual monetary conference. Great panels and very interesting speeches.

Three panels were of particular interest to me: panel 1 (“100 Years of the Fed: What Have We Learned?”), panel 2 (“Alternatives to Discretionary Government Fiat Money”), panel 3 (“The Fed vs. the Market as Bank Regulator”).

In panel 1, George Selgin destroys the Federal Reserve’s distorted monetary history. Nothing much new in what he says for those who know him but it just never gets boring anyway. He covers: some of the lies that the Federal Reserve tells the general public to justify its existence, pre-WW2 Canada and its better performing monetary system despite not having a central bank, the lack of real Fed independence from political influence and……the Fed not respecting Bagehot’s principles despite claiming to do so. In this panel, the speech of Jerry Jordan, former President of the Federal Reserve Bank of Cleveland, is also very interesting.

In panel 2, Larry White speaks about alternatives to government fiat money, counterfeiting laws and state laws making it illegal to issue private money. Scott Sumner describes NGDP level targeting. Here again, nothing really new for those who follow his blog, but interesting nonetheless (even though I don’t agree with everything) and a must see for those who don’t.

In panel 3, John Allison provides an insider view of regulators’ intervention in banking (he used to be CEO of BB&T, an American bank). He argues that mathematical risk management models provide unhelpful information to bankers. He would completely deregulate banking but increase capital requirements, which is an original position to say the least. Kevin Dowd’s speech is also interesting: he covers regulatory and accounting arbitrage (SPEs, rehypothecation…) and various banking regulations including Basel’s.

Overall, great stuff and you should watch the whole of it (I know, it’s long… you can probably skip most Q&As).

PS: Scott Sumner also commented on the Pope’s speech on “evil incarnate”. Reminds me of the vocabulary I used…

Banks’ RWAs as a source of malinvestments – A graphical experiment

Today is going to be experimental and theoretical. I have already outlined the principles behind the RWA-based variation of the Austrian Business Cycle Theory (ABCT), which was followed by a quick clarification. I am now attempting to come up with a graphical representation to illustrate its mechanism. In order to do that, I am going to use Roger Garrison’s capital structure-based macroeconomics representations used in his book Time and Money: The Macroeconomics of Capital Structure. I am not saying that what I am about to describe is 100% right. Remember that this remains an experiment that I just wrote down over those last few days and that needs a lot more development. There may well also be other ways of depicting the impacts that Basel regulation’s RWAs have on the capital structure and malinvestments. Completely different analytical frameworks might also do. Comments and suggestions are welcome.

This is what Garrison’s representation of the macroeconomics of capital structure looks like:

It is composed of three elements:

- Bottom right: this is the traditional market for loanable funds, where the supply and demand for loanable funds cross at the natural rate of interest. It represents economic agents’ intertemporal preferences: the higher they value future goods over present goods, the more they save and the lower the interest rate. The x-axis represents the quantity of savings supplied (and investments) and the y-axis represents the interest rate.

- Top right: this is the production-possibility frontier (PPF). In Garrison’s chart, it represents the sustainable trade-off between consumption and gross investment. Only movements along the frontier are sustainable and supposed to reflect economic agents’ preferences. Positive net investments and technological shocks expand the frontier as the economy becomes more productive.

- Top left: this is the Hayekian triangle. It represents the various stages of production (each adding to output) within an industry. See details below:

I don’t have time to come back to the original ABCT and those willing to find out more about it can find plenty of examples online. Today I wish only to try to understand the impact of regulatory-defined risk-weighted assets on this structure. Ironically, it becomes necessary to disaggregate the Austrian capital-based framework to understand the mechanics and distortions leading to a likely banking crisis. In everything that follows, and unlike in the original Austrian theory, we exclude central banks from the picture (i.e. no monetary injection). We instead focus only on monetary redistribution. The story outlined below does not explain the financial crisis by itself. Rather, it outlines a regulatory mechanism that exacerbated the crisis.

I don’t have time to come back to the original ABCT and those willing to find out more about it can find plenty of examples online. Today I wish only to try to understand the impact of regulatory-defined risk-weighted assets on this structure. Ironically, it becomes necessary to disaggregate the Austrian capital-based framework to understand the mechanics and distortions leading to a likely banking crisis. In everything that follows, and unlike in the original Austrian theory, we exclude central banks from the picture (i.e. no monetary injection). We instead focus only on monetary redistribution. The story outlined below does not explain the financial crisis by itself. Rather, it outlines a regulatory mechanism that exacerbated the crisis.

Let’s take a simple example that I have already used earlier. Only two types of lending exist: SME lending and mortgage/real estate lending. Basel regulations force banks to use more capital when lending to SME and as a result, bankers are incentivised to maximise ROE through artificially increasing mortgage lending and artificially restricting SME lending, as described in my first post on the topic.

In equilibrium and in a completely free-market world with no positive net investment, the economy looks like Garrison’s chart above. However, bankers don’t charge the Wicksellian natural rate of interest to all customers: they add a risk premium to the natural rate (effectively a ‘risk-free’ rate) to reflect the risk inherent to each asset class and customer. Those various rates of interest do reflect an equilibrium (‘natural’) state, which factors in the free markets’ perception of risk. Because lending to SME is riskier than mortgage lending, we end up with:

natural (risk free) rate < mortgage rate (natural rate + mortgage risk premium) < SME rate (natural rate + SME risk premium)

What RWAs do is to impose a certain perception of risk for accounting purposes, distorting the normal channelling of loanable funds and therefore each asset class’ respective ‘natural’ rate of interest. Unfortunately, depicting all demand and supply curves, their respective interest rates and the changes when Basel-defined RWAs are applied would be extremely messy in a single chart. We’re going to illustrate each asset class separately with their respective demand and supply curve. Let’s start with mortgage (real estate) lending:

Given the incentives they have to channel lending towards capital-optimising asset classes, bankers artificially increase the supply of loanable funds to all real estate activities, pushing the rate of interest below the natural rate of the sector. As the actual total supply of loanable funds does not change, returns on savings remain the same. In our PPF, this pushes resources towards real estate. Any other industry would interpret the lowered rate of interest as a shift in people’s intertemporal preferences towards the future and increase long-term investments at the expense of short-term production. Indeed, long-term housing projects are started. This is represented by the thin dotted red triangle.

Given the incentives they have to channel lending towards capital-optimising asset classes, bankers artificially increase the supply of loanable funds to all real estate activities, pushing the rate of interest below the natural rate of the sector. As the actual total supply of loanable funds does not change, returns on savings remain the same. In our PPF, this pushes resources towards real estate. Any other industry would interpret the lowered rate of interest as a shift in people’s intertemporal preferences towards the future and increase long-term investments at the expense of short-term production. Indeed, long-term housing projects are started. This is represented by the thin dotted red triangle.

However, the short-term housing supply is inelastic and cannot be reduced. The resulting real estate structure of production is the plain red triangle. Nonetheless, real estate developers have been tricked by the reduced interest rate and the long-term housing projects they started do not match economic agents’ future demand. Meanwhile, savers, adequately rewarded for their savings, do not draw down on them (or don’t have to), but are instead incentivised to leverage as they (indirectly) see profit opportunities from the differential between the natural and the artificially reduced rate. Leverage effectively becomes a function of the interest rate differential:

The increased leverage boosts the demand for existing real estate, bidding up prices, starting a self-reinforcing trend based on expected further price increases. We end up in a temporary situation of both short-term ‘overconsumption’ of real estate and its associated goods, and long-term overinvestments (malinvestments). This situation is depicted by the thick dotted red triangle and represents an unsustainable state beyond the PPF.

On the other hand, bankers artificially restrict the supply of loanable funds to SME, pushing the rate of interest above the natural rate. Tricked by a higher rate of interest, SMEs are led to believe that consumers now value more highly present goods over future goods (as they ‘apparently’ now save less of their income). They temporarily reduce interest rate-sensitive long-term investments to increase the production of late stages consumer goods. This results in an overproduction of consumer goods relative to economic agents’ underlying present demand. Nonetheless, wealth effects from the real estate boom temporarily boost consumption, maintaining prices level. Overconsumption of present goods could also eventually appear if and when savers start leveraging their consumption through low-rate mortgages, as house prices seem to keep increasing. In the long-run, SMEs’ investments aren’t sufficient to satisfy economic agents’ future demand of consumer goods.

With leverage increasing and the economy producing beyond its PPF, the situation is unsustainable. As increasingly more people pile in real estate, demand for real estate loanable funds increases, pushing up the interest rate of the sector. Interest payments – which had taken an increasingly large share of disposable income in line with growing leverage – rise, putting pressure on households’ finances. The economy reaches a Minsky moment and real estate prices start coming down. Real estate developers, who had launched long-term housing projects tricked by the low rates, find out that these are malinvestments that either cannot find buyers or are lacking the financial resources to be completed. Bankruptcies increase among over-leveraged households and companies. Banks start experiencing losses, contract lending and money supply as a result, whereas savers’ demand for money increases. The economy is in monetary disequilibrium. Welcome to the financial crisis designed in the Swiss city of Basel.

This all remains very theoretical and I’ll try to dig up some empirical evidences in another post. Nonetheless, the story seems to match relatively well what happened in some countries during the crisis. Soon after Basel regulations were implemented, household leverage in Spain or Ireland took off and came along with increasing house prices and retail sales, which both collapsed once the crisis struck. Under this framework, the artificially restricted supply of loanable funds to SME and the consequent reduction in long-term investments could also partly explain the rich world manufacturing problems. However, I presented a very simple template. As I mentioned in a previous post, securitisation and other banking regulations (liquidity…) blur the whole picture, and central banks can remain the primary channel through which interest rates are distorted.

RWA-based ABCT Series:

- Banks’ risk-weighted assets as a source of malinvestments, booms and busts

- Banks’ RWAs as a source of malinvestments – Update

- Banks’ RWAs as a source of malinvestments – A graphical experiment

- Banks’ RWAs as a source of malinvestments – Some recent empirical evidence

- A new regulatory-driven housing bubble?

Banks’ risk-weighted assets as a source of malinvestments, booms and busts

Here I’m going to argue that Basel-defined risk-weighted assets, a key component of banking regulation, may be partly responsible for recent business cycles.

Readers might have already noticed my aversion to risk-weighted assets (RWAs), which I view as abominations for various reasons. They are defined by Basel accords and used in regulatory capital ratios. Basel I (published in 1988 and enforced from 1992) had fixed weights by asset class. For example, corporate loans and mortgages would be weighted respectively 100% and 50%, whereas OECD sovereign debt would be weighted 0%. If a bank had USD100bn of total assets, applying risk-weights could, depending on the lending mix of the bank, lead to total RWAs of anything between USD20bn to USD90bn. Regulators would then take the capital of the bank as defined by Basel (‘Tier 1’ capital, total capital…) and calculate the regulatory capital ratio of the bank: Tier 1 capital/RWAs. Basel regulation required this ratio to be above 4%.

Basel II (published in 2004 and progressively implemented afterwards) introduced some flexibility: the ‘Standardised method’ was similar to Basel I’s fixed weights with more granularity (due to the reliance on external credit ratings), while the various ‘Internal Ratings Based’ methods allowed banks to calculate their own risk-weight based on their internal risk management models (‘certified’ by regulators…).

This system is perverse. Banks are profit-maximising institutions that answer to their shareholders. Shareholders on the other hand have a minimal threshold under which they would not invest in a company: the cost of capital, or required return on capital. As a result, return on equity (ROE) has to at least cover the cost of capital. If it doesn’t, economic losses ensue and investors would have been better off investing in lower yielding but lower risk assets in the first place. But Basel accords basically dictate banks how much capital they need to hold. Therefore banks have an incentive in trying to ‘manage’ capital in order to boost ROE. Under Basel, this means pilling in some particular asset classes.

Let’s make very rough calculations to illustrate the point under a Basel II Standardised approach: a pure commercial bank (i.e. no trading activity) has a choice between lending to SMEs (option 1) or to individuals purchasing homes (option 2). The bank has EUR1bn in Tier 1 capital available and wishes to maximise returns while keeping to the minimum of 4% Tier 1 ratio. We also assume that external funding (deposits, wholesale…) is available and that the marginal increase in interest expense is always lower than the marginal increase in interest income.

- Option 1: Given the 100% risk-weight on SME lending, the bank could lend EUR25bn (25bn x 100% x 4% = 1bn), at an interest rate of 7% (say), equalling EUR1.75bn in interest income.

- Option 2: Mortgage lending, at a 35% risk-weight, allows the same bank to lend a total of EUR71.4bn (71.4bn x 35% x 4% = 1bn) for EUR1bn in capital, at an interest rate of 3% (say), equalling EUR2.14bn in interest income.

The bank is clearly incentivised to invest its funding base in mortgages to maximise returns. In practice, large banks that are under the IRB method can push mortgage risk-weights to as low as barely above 10%, and corporate risk-weights to below 50%. As a result, banks are involuntarily pushed by regulators to game RWAs. The lower RWAs, the lower capital the bank needs, the higher its ROE and the happier the regulators. Banks call this ‘capital optimisation’.

Consequently, does it come as a surprise that low-risk weighted asset classes were exactly the ones experiencing bubbles in pre-crisis years? Oh sorry, you don’t know which asset classes were lowly rated… Here they are: real estate, securitisation, OECD sovereign debt. Yep, that’s right. Regulatory incentives that create crises. And the new Basel III regime does pretty much nothing to change the incentivised economic distortions introduced by its predecessors.

Yesterday, Fitch, the rating agency, published a study of lending and RWAs among Europe’s largest banks (press release is available here, full report here but requires free subscription). And, what a surprise, corporate lending is going…down, while mortgage lending and credit exposures to sovereigns are going…up (see charts below). The trend is even exacerbated as banks are under pressure from regulators to boost regulatory capitalisation and from shareholders to improve ROE. And this study only covers IRB banks. My guess is that the situation is even more extreme for Standardised method banks that cannot lower their RWAs.

The ‘funny’ thing is: not a single regulator or central banker seems to get it. As a result, we keep seeing ill-founded central banks schemes aiming at giving SME lending a boost, like the Funding for Lending Scheme launched by the Bank of England in 2012, which provided banks with cheap funding. Yes, you guessed it: SME lending continued its downward trend and the scheme provided mortgage lending a boost.

Should the situation ‘only’ prevent corporates to borrow funds, bad economic consequences would follow but remain limited. Economic growth would suffer but no particular crisis would ensue. The problem is: Basel and RWAs force a massive misallocation of capital towards a few asset classes, resulting in bubbles and large economic crises when the crash occurs.

The Mises and Hayek Austrian business cycle theory emphasises the distortion in the structure of relative prices that emanates from central banks lowering the nominal interest rate below the natural rate of interest as represented by economic agents’ intertemporal preferences, resulting in monetary disequilibrium (excess supply of money). The consequent increase in money supply flows in the economy through one (or a few) entry points, increasing the demand in those sectors, pushing up their prices and artificially (and unsustainably) increasing their return on investment.

I argue here that due to Basel’s RWAs distortions, central banks could even be excluded from the picture altogether: banks are naturally incentivised to channel funds towards particular sectors at the expense of others. Correspondingly, the supply of loanable funds increases above equilibrium in the favoured sectors (hence lowering the nominal interest rate and bringing about an unsustainable boom) but reduces in the disfavoured ones. There can be no aggregate overinvestment during the process, but bad investments (i.e. malinvestments) are undertaken: the investment mix changes as a result of an incentivised flow of lending, rather than as a result of economic agents’ present and future demand. Eventually, the mismatch between expected demand and actual demand appears, malinvestments are revealed, losses materialise and the economy crashes. Central banks inflation worsen the process through the mechanism described by the Austrians.

I am not sure that regulators had in mind a process to facilitate boom and bust cycles when they designed Basel rules. The result is quite ‘ironic’ though: regulations developed to enhance the stability of the financial sector end up being one of the very sources of its instability.

RWA-based ABCT Series:

- Banks’ risk-weighted assets as a source of malinvestments, booms and busts

- Banks’ RWAs as a source of malinvestments – Update

- Banks’ RWAs as a source of malinvestments – A graphical experiment

- Banks’ RWAs as a source of malinvestments – Some recent empirical evidence

- A new regulatory-driven housing bubble?

The EBA banks’ balance sheets assessment and the standardisation problem

About two weeks ago, the European Banking Authority announced their standard definitions of impaired loans (i.e. non-performing loans) and other asset quality standards, which aim at harmonising the various definitions in place throughout Europe for their upcoming asset quality review. Today, I won’t even be mentioning the odd fact to see a regulator getting in a bank for a few days and basically telling the bank that it knows its loan book better than the bankers themselves. No, today I will only speak about the harmonisation issue.

![]()

Banks have different ways of classifying past-due loans, impaired loans, loans in forbearance and so on, not only in between countries but also within countries. For instance, in the UK, I know some banks that will classify all loans in forbearance as impaired, artificially pushing up their headline bad loans ratio, while others do not, looking better as a result to the untrained eye. Most British banks will automatically classify loans 90 days and more in arrears as impaired, whereas most French banks will only apply the impaired definition when loans are 180 days and more in arrears.

So a standardisation seems to be a good thing as data becomes comparable. Well, it is, and it isn’t. To be fair, standardisation within a country is probably a good thing, although shareholders, investors and auditors – rather than regulators – should force management to report financial data the way they deem necessary. However, it makes a lot less sense on an international basis. Why? Countries have different cultural backgrounds and legal frameworks, meaning that certain financial ratios should not be interpreted the same way from one country to another.

Let’s take a few examples. In the US, people are much more likely than Europeans on average to walk away from their home if they can’t pay off their mortgage. Most Europeans, on the other hand, will consider mortgage repayment as priority number 1. As a result, impaired mortgage ratios could well end-up higher in the US. But US banks know that and adapt their loan loss reserves in consequence. Within Europe, legal frameworks and judiciary efficiency are also key: UK banks often set aside fewer funds against mortgage losses as the legal system allows them to foreclose and sell homes relatively quickly and with minimal losses. In France on the other hand, the process is much longer with many regulatory and legal hurdles. Consequently, UK-based mortgage banks seem to have lower loan loss reserves compared with some of their continental Europe peers. Does it mean they are riskier? Not really.

Another (abstract) example: in country A, the local culture pushes people to pay off their debt at all costs, whereas in country B, most people, once they stop paying back when they run into short-term trouble, never resume payment. In country A, banks consider it safe to classify a loan as impaired only after 180 days without payment. In country B though, banks know that the loan will never be paid off as soon as it is 30 days past due. Standardisation would make both countries use the same classification. Why not, but it doesn’t bring much: analysts will still have to take into account local variations (just in a different way). However, it might spark an unnecessary panic in country A when figures suddenly look much worse to the untrained public.

This is the issue with harmonising. Some standardisation may be welcome, but most analysts and investors already know the differences in reporting between countries and don’t take headline figures at par value, making the EBA exercise relatively pointless. For the less-well informed individuals, the EBA harmonisation could also bring a false sense of safety: figures look comparable, but in reality, they’re not entirely. In the end, harmonised reporting or not, adjustments always have to be made…

The same apply to most internationally-applied regulations. Basel rules, for example, effectively apply standardised capital and liquidity requirements throughout the world (with some local implementation differences). Banks in higher-risk countries have to comply with the same capital ratios as banks in lower-risk countries, the adjustment being made through risk-weighted assets…which are easily gamed. But analysts know well enough that a 17% regulatory Tier 1 ratio (a key bank capital safety ratio) is actually poor for an African bank, despite looking high by Western standards and way above official requirements.

In the end, standardisation makes particular sense in geographical areas where both culture and legal frameworks present only minor differences, such as the US. Europe is still a pretty fragmented continent, and it doesn’t look like things are going to change overnight. The EBA hasn’t been very clear about the exact implementation of its criteria. Let’s just hope they keep the issues discussed in this post in mind.

News of Regulatory Capital importance

The European Banking Authority today published its new Basel 3 monitoring exercise of European Banks. For those of you who don’t know what Basel 3 is, it is the latest iteration of the global banking guidelines defined in Basel, Switzerland, which roughly covers minimum capital, liquidity and funding requirements that banks have to achieve by 2019. I’ll come back to the details in another post.

![]()

There is some partially good news. European banks seem to become more capitalised and more liquid. I have doubts regarding the process though, and I am not even questioning the centralised decision-taking in Basel, which I am evidently against. I am also against undercapitalised banks, but for other reasons.

No, what ‘worries’ me is the method that regulators used to push banks to recapitalise. The Basel accord asked banks to achieve balance sheet targets by 2019. Then came the EBA and other national regulators, who ‘stress-tested’ banks and almost publicly shamed them if they failed the tests. Now, the EBA proudly announces that pretty much all European banks will achieve capital and liquidity targets (“fully loaded Core Equity Tier 1 capital ratio”, “Liquidity Coverage ratio”…) five years ahead of schedule.

Hold on… Why even come up with a 2019 deadline in the first place then? The consequence of this is that banks have been under massive pressure to quickly ‘recapitalise’ in the middle of a European economic crisis, instead of doing it more progressively. This certainly did not help economic recovery, and we can also question the quality of the capital ratios achieved as a result.

Why? Many banks have tried to bolster their regulatory capital ratio and their liquidity by… reducing their balance sheet. Meaning? They decided to reduce lending, maintaining their capital base stable (or even declining!). Moreover, many banks are also playing with risk-weighted assets (RWAs). RWAs allow banks to apply a “weight” on a specific asset class according to the perceived risk of this class. For example, US debt is judged as risk-free and hence will carry a 0% weight, thereby allowing the bank to hold no capital against it to absorb potential losses.

Regulatory capital ratios are calculated this way: regulatory capital/RWAs. Regulatory capital comprises equity and “supplementary hybrid capital”, which lies in between equity and debt. The ratio is flawed: hybrid capital often does not adequately absorb losses and banks have an incentive to ‘arrange’ RWAs (lowering them to artificially increase the ratio). It happens frequently and I’ll get back to that another day. A clue to the fact that banks’ capitalisation might not be that good is the Basel 3 Leverage ratio. While we can criticise this leverage ratio on methodological grounds, it uses total assets and not RWAs on the denominator. Well, guess what? This ratio has not changed since the latest EBA review…

Another ‘good’ news, HSBC will hire 3000 more compliance staff this year, following a similar move by JPMorgan. Surely this is good news as it creates jobs? Not really. HSBC already employs 2000 compliance officers. Hiring so many people to deal with red tape instead of working in more productive activities represents a big economic loss.

Recent Comments