Flawed models + history ignorance = disastrous policy-making

Ben Southwood pointed to new research on banking which I thought would beautifully complement the point I was trying to make in my previous post on the ignorance of history.

The author designs a model that leads him to conclude that

contrary to conventional wisdom, competition can make banks more reluctant to take excessive risks: As competition intensifies and margins decline, banks face more-binding threats of failure, to which they may respond by reducing their risk-taking. Yet, at the same time, banks become riskier. This is because the direct, destabilizing effect of lower margins outweighs the disciplining effect of competition; moreover, a substantial rise in competition reduces banks’ incentive to build precautionary capital buffers. A key implication is that the effects of competition on risk-taking and on failure risk can move in opposite directions.

The paper declares that “a decline in margins caused by heightened competition [would lead to] a more conservative stance and less aggressive risk-taking” and that “high profits that can be reaped in less-competitive environment [would allow] for more risk-taking”. The author describes the literature as generally believing that… the opposite is true.

The paper declares that “a decline in margins caused by heightened competition [would lead to] a more conservative stance and less aggressive risk-taking” and that “high profits that can be reaped in less-competitive environment [would allow] for more risk-taking”. The author describes the literature as generally believing that… the opposite is true.

My first reaction is: it is so much more complex than that. Banks have different cultures and risk-aversions within the same context. This is why some fail why others remain strong throughout a given period. There is no pre-programmed behaviour that would push banks to act in a certain way. Within a given banking system and at a given point in time, banks offer investors a range of RoE and volatility of returns: investors can then diversify their banking investment portfolio according to their need and risk appetite. Some will prefer a high return/high volatility of earnings/high risk bank and require a higher cost of capital; others will go for stability and lower returns*. Banks are not trying to maximise RoE. Banks are trying to maximise RoE on a risk-adjusted basis**.

According to the author, historical experience demonstrates that competition makes banks riskier, and that this prediction is consistent with empirical evidence. Wait… Really? What kind of ‘competition’? In what context? Under what sort of banking, political and economic framework? Historical experiences of as close as possible to pure competition show the exact opposite of this claim. Indeed, the empirical evidence the author refers to is this 2009 paper, which statistically analysed current data from the Bankscope database. There is no reference to historical events, political circumstances, banking design and restrictive regulations. All types of banks, from the US granular unit banks to the Chinese giant government-controlled oligopoly banks are aggregated and ‘conclusion’ on competition is reached. This is bad research.

The paper is full of dubious claims, such as this one:

In our model, highly profitable banks optimally build equity capital buffers to guard against failure, whereas banks operating in more-competitive environments seek to minimize their capital.

Once again, this conclusion is so far from historical reality as to be meaningless. There are examples of oligopoly-type banks operating on thin capital buffers and free banking experiences in Scotland showed that competition led banks to accumulate large capital buffers. We also find examples of banks with local monopolies operating on a small equity base due to a particular banking structure. Banking system design and risk culture are key. Research pieces such as this one are over-simplistic and provide policy-makers with the wrong diagnoses.

But looking at the model’s assumptions, it becomes clear that the analysis was made in a vacuum. The banking system consists of one bank (no lending competition…), owned and run by infinitely lived shareholders, whose competitors are money market funds. Economics and finance is a matter of time-constrained resources management, and infinitely lived owners/bankers have different incentives and priorities from those whose life is finite and uncertain… Other unrealistic assumptions that skew the models include: money market funds that effectively compete with the (only) bank’s deposit rate for depositors’ funds, or very granular time periods during which the bank has no flexibility to raise capital or deal with its balance sheet issues, resulting in very binary outcomes at the end of each period. And, of course, this ‘competitive’ system includes deposit insurance and capital requirements.

In the end, we can reasonably question what this model proves, if anything. This exemplifies the problems I have with financial and economic models in general: they are not reliable. And this is an understatement.

For instance, the conclusions reached by this model are precisely the opposite of those reached by other models built for previous similar studies. What does this mean? Which ones are right (if any)? Which ones are wrong (if any)?

I used to be a scientist and have a Master’s degree in engineering. I also used to believe that everything could be modelled. I was wrong. Economic systems do not benefit from universal physical constants.

When I started my career in financial services, I tended to use mathematical and statistical tools (trends, correlations) to forecast some financial information. A senior analyst warned me: “it never works.” He was right, but I didn’t believe him to start with and continued experimenting nonetheless, until I noticed that ‘intuition’, ‘knowledge’ and ‘wisdom’ would serve me more than mathematics. What was I trying to forecast? Revenues of a listed firm. Nothing really complex.

Unfortunately, most economists and central bankers still believe they can model the whole economy – or, as seen above, the whole banking system – using maths. Given the inaccuracy of quarterly revenue and profit per share estimates, modelling something infinitely more complex (the whole economy), which involves an infinite number of ever-changing, erratic and poorly-rational variables (i.e. humans), sounds like an enormous, if not impossible, project. Still, this is what academic DSGE models have been trying to do for a few decades. With great success as we have been witnessing since 2007.

I agree (for once) with this post by Noah Smith, who rightly asks:

So why doesn’t anyone in the finance industry use them? Maybe industry is just slow to catch on. But with so many billions upon billions of dollars on the line, and so many DSGE models to choose from, you would think someone at some big bank or macro hedge fund somewhere would be running a DSGE model. And yet after asking around pretty extensively, I can’t find anybody who is.

One unsettling possibility is that the academic macroeconomists of the ’70s and ’80s simply bit off more than they could chew. Modeling a big thing (like the economy) as the outcome of a bunch of little things (like the decisions of consumers and companies) is a difficult task. Maybe no DSGE is going to do the job. And maybe finance industry people simply realize this.

Of course, many people working in finance still try to forecast the future. But their forecasts are in competition with each other and none of them has the power to make the decision that central banks or policy-makers can make for the whole economy, with potentially disastrous consequences. The Fed’s, ECB’s and BoE’s forecasts have constantly been way off the mark throughout the crisis. I also know from certain sources that some of central banks’ models are less elaborate than rating agencies’. I’ll let the reader conclude.

The example above clearly demonstrates why economics should avoid relying on mathematics and simplified assumptions. Time to stop ignoring history.

* In a banking system with no deposit insurance, the same applies: depositors have the choice between higher deposit rates/higher risk or lower and safer ones.

** This is where moral hazard and bad regulatory incentives applies: by distorting risk-aversion and assessment.

Continuously ignoring and misinterpreting history

This recent speech by the Vice President of the ECB, Vítor Constâncio, is in my opinion one of the foremost examples of how a partial reading or misinterpretation of history that becomes accepted as mainstream can lead to bad policy-making.

This speech is typical. Constâncio argues that

the build-up of systemic risk over the financial cycle is an endogenous outcome – a man-made construct – and the job of macro-prudential policy is to try to smoothen this cycle as much as possible. […]

The […] most important source of systemic risk is the risk of the unravelling of financial imbalances. These imbalances may build up gradually, mostly endogenously, and can then unravel abruptly. They form part of the inherent pro-cyclicality of the financial system.

It is crucial to recognise that the financial cycle has an important endogenous component which arises because banks take too much solvency and liquidity risk. The aim of macro-prudential policy should be to temper the financial cycle rather than to merely enhance the resilience of the financial sector ahead of crises.

While Constâncio is right that there is some truth in the pro-cyclicality of financial systems as a long economic boom impairs risk perception, risk assessment and risk premiums, he never highlights why such booms and busts occur in the first place. Outside of negative supply shocks, are they a ‘natural’ consequence of the activity of the economic system? Or are they exogenously triggered by bad government or monetary policies?

Several economic schools of thought have different explanations and theories. Yet, there is one thing that cannot be denied: historical experiences of financial stability.

This is where the flaw of Constâncio’s (and of most central bankers’ and mainstream economists’) thinking resides: history proves that, when the banking sector is left to itself, systemic endogenous accumulation of financial imbalances is minimal, if not non-existent…

According to Larry White in a recent article summing up the history of thought and historical occurrences of free banking, Kurt Schuler identified sixty banking episodes to some extent akin to free banking. White’s paper describes 11 of them, many of which had very few institutional and regulatory restrictions on banking. He quotes Kevin Dowd:

As Kevin Dowd fairly summarizes the record of these historical free banking systems, “most if not all can be considered as reasonably successful, sometimes quite remarkably so.” In particular, he notes that they “were not prone to inflation,” did not show signs of natural monopoly, and boosted economic growth by delivering efficiency in payment practices and in intermediation between savers and borrowers. Those systems of plural note-issue that were panic-prone, like the pre-1913 United States and pre-1832 England, were not so because of competition but because of legal restrictions that significantly weakened banks.

Yet, there is no trace of such events in conventional/mainstream financial history. Central bankers seem to be completely oblivious to those facts (this is surely self-serving) and economists only partially aware of the causes of financial crises. Moreover, free banking episodes also proved that banks were not inherently prone to take “too much solvency and liquidity risk”: indeed, historical records show that banks in such periods were actually well capitalised and rarely suffered liquidity crises. In short, laissez-faire banking’s robustness was far superior to our overly-designed ones’. Consequently we keep making the same mistakes over and over again in believing that a crisis occurred because the previous round of regulation was inadequate…

What we end up with is a banking system shaped by layers and layers of regulations and central banks’ policies. Every financial product, every financial activity, was awarded its own regulation as well as multiple ‘corrective’ rules and patches, was influenced by regulators’ ‘recommendations’, was limited by macro-prudential tools and manipulated through various interest rates under the control by a small central authority. On top of such regulatory intervention, short-term political interference compounds the problem by purposely designing and adjusting financial systems for short-term electoral gains. Markets are distorted in all possible ways as the price system ceases to work adequately, defeating their capital allocation purposes and creating bubbles after bubbles.

Studying banking and financial history demonstrates that it is quite ludicrous to pretend that banking systems are inherently subject to failure through endogenous accumulation of risk. In the quest for an explanation of the crisis, better look at the intersection of moral hazard, political incentives, and the regulatory-originated risk opacity. It might turn out that imbalances are, well, mostly… exogenous.

Please let finance organise itself spontaneously.

Photo: José Carlos Pratas

Calomiris and Haber are pretty much spot on

I recently finished reading Fragile by Design, the latest book of Charles Calomiris and Stephen Haber.

Let’s get to the point: it’s one of the best books of banking I’ve had the occasion to read. It is a masterpiece of banking and political history and theory.

Calomiris and Haber describe the stability and efficiency of banking systems in terms of local political arrangements and institutions, which contrasts with most of nowadays’ theories that don’t distinguish between banking systems in various countries and way too often seem to draw conclusions on banking from the US experience only.

They describe banks’ stability in terms of a ‘Game of Banks Bargains’: the tendency for populists and bankers to form coalitions that aren’t favourable for society as a whole but favourable for politicians’ short-term political gains and bankers’ short-term profits. Needless to say, this alliance is built at the expense of long-term stability and efficiency. Only countries that have built political institutions to counteract the effects of populist policy proposals have experienced a stable financial environment since the early 19th century.

This thesis is extremely convincing and, while I find it unsurprising, it is so well documented that it is sometimes almost shocking. It clearly goes against mainstream Keynesian and Post-Keynesian theories, which consider financial collapses as a result of the normal process of human ignorance and panics. According to those theories, banks will fail at some point, hence the need for regulation and intervention early on. From most Keynesian books and articles I’ve read so far, collapses just happen. I’ve always been bewildered by the lack of underlying explanation: “that’s just the way it is”. Hyman Minsky’s Stabilizing an Unstable Economy is the perfect example: it draws general conclusions about the banking sector and the economy from a period of a couple of decades in the US… Knowledge of financial history quickly proves those arguments wrong.

The book isn’t without flaws however. It describes and compares the history of banking systems in England, the US, Canada, Mexico and Brazil. I found that either Brazil or Mexico could have been skipped (as covering both didn’t bring that much more to the thesis) in order to study more in depth another European (French, German, Italian) and/or Asian (Japanese, Indian…) banking system.

Also, while the (long) description of the political ramifications that led to the US subprime crisis is stunning, I believe the authors’ thesis is incomplete. There is no doubt that the populists/housing agencies/bankers alliance (or forced alliance) amplified the crisis by generating way too many low-quality housing loans through declining underwriting standards. However, this cannot be the only reason behind the crash. As I have described in many posts, properties have boomed and crashed all around the world in a coordinated fashion during the same period due to regulations incentivising house lending (and securitized products based on housing loans), as well as low interest rates. It is hard to argue that the Irish or the Spanish housing markets were the victims of US populists and US subprime lending…

Finally, what Calomiris and Haber describe is that free-market banking systems are less prone to systemic failures. From their work, it is clear that: 1. the fewer rules the banking system is subject to and 2. the less government intervention in the finance industry, the more stable the financial system. They demonstrate that the more lightly regulated Canadian system and the Scottish free-banking system were seen as almost ideal. Nevertheless, they seem to refrain from explicitly argue in favour of free-banking systems for some reason. I found this a little odd.

I certainly disagree with their view that banks can only exist when the state exists and charter them because of their interrelationship (i.e. states can raise financing through banks and banks get competitive advantages in return). Their arguments are really unconvincing: 1. it isn’t because such occurrences are rare in recent history that they cannot happen and 2. we have consistently witnessed throughout history, and in particular over the past decades, the spontaneous emergence of unchartered financial institutions (from money market funds to P2P lending firms) that respond to a private need for financial services. I do not think those are ‘utopian fantasies’ as this is happening right in front of us right now… States started to select, allow, charter and regulate those institutions when they needed finance. This does not imply that a limited and pacifistic state necessarily needs to use the same constraining tools.

In the end, those flaws remain minor and the book is easily one of my favourites. It deserves much more attention than what the media have given them so far (indeed, they go against the traditional ‘banking is inherently unstable’ tenet…). Unfortunately, the media are more interested in bank-bashing stories, putting in the spotlight much weaker books such as The Bankers’ New Clothes (by Admati and Hellwig)…

PS: FT’s John Kay also talks about the book here.

The political banking cycle

A couple of weeks ago, The Economist reported that Mel Watt, the new regulator of the US federal housing agencies Fannie Mae and Freddie Mac, wanted those two agencies to stop shrinking and continue purchasing mortgage loans from banks in order to help homeowners and the housing market (also see the WSJ here). To twist the system further, the compensation of the agencies’ executives will be linked to those political goals. Mr Watt used to be one of the main proponents of more accessible house lending for poor households through Fannie and Freddie before the crisis.

As The Economist asks, “what could go wrong?”…

Lars Christensen and Scott Sumner also find this ridiculously misguided government intervention horrifying. I find myself in complete agreement (and this is an understatement). Who could still honestly say that we are (or were) in a laissez-faire environment?

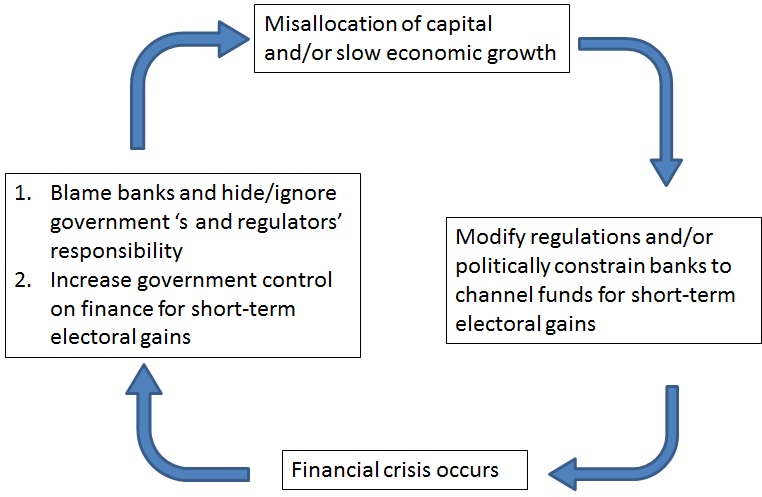

This, along with UK’s FLS and Help to Buy schemes, made me think that there has been a ‘political banking cycle’ throughout the 20th century. Why 20th century? From all the banking history I’ve read so far, populations seemed to better understand banking before the introduction of safety net measures such as central banks, deposit insurances or systematic government bail-outs. When financial crashes occurred, blame was usually shared between governments and banks, if not governments only. This is why many crises triggered deregulation processes rather than reregulation ones. This contrasts with the mainstream view our society has had since the Great Depression: when a financial crash happens, whatever the government’s responsibility is, banks and free market capitalism are the ones to blame.

This political cycle looks like that:

The worst is: it works. Politicians escaped pretty much unscathed from the financial crisis despite the huge role they played in triggering it*. The majority of the population now sincerely believes that the crisis was caused by greedy bankers (see here, here, here and here). This is as far from the truth as it can be (I don’t deny ‘greed’ played a role though, but channelled through and exacerbated by a combination of other factors, i.e. moral hazard etc.). Unfortunately, it is undeniable: politicians won. And not only politicians won, but they also managed to self-convince that they played no role in the crisis, as the example of Mr Watt shows (he either truly believes that government intervention in the US housing market was a good thing, or he has an incredibly cynical short-term political view).

The crucial question is: why did 19th century populations seem more educated about banking? The answer is that the lack of state paternalism through various protection schemes forced bank depositors and investors to oversee and monitor their banks. Once protection is implemented, there is no incentive or reason anymore to maintain any of those skills.

Who is easier to manipulate: a knowledgeable electorate or an ignorant one?

PS: This chart is mostly accurate for democracies that have a populist tendency. Not all countries seem to be prone to such cycle (this can be due to cultural or institutional arrangements).

* I won’t get into the details here, but if you’re interested, just read Engineering the Financial Crisis, Fragile by Design or Alchemists of Loss……. or simply this NYT article from 1999.

The importance of intragroup funding – 19th century Canada

This is a quick follow-up post on intragroup funding, as promised in the one focusing on the US experience during the 19th century.

The Canadian case is interesting, because Canada is also a ‘recent’ country that experienced its own banking development at the same time as its close, also ‘recent’, neighbour, the US. Though the contrast cannot be starker; while the US was prone to recurrent financial crises during the 19th century, Canada’s financial system remained pretty stable throughout the period, and continued to do so until today.

The main difference between the Canadian and the US banking systems was their fragmentation and regulation. The US, as described earlier, had a very fragmented and highly regulated (though much less than today…) banking system, whereas Canada had a lightly regulated and quite concentrated one (some could argue that it was pretty much an oligopoly). In the US, a multitude of unit banks with no branches and local monopolies prevailed. In Canada, large nationwide banks with multitude of branches prevailed. This was due to the specific political and institutional arrangements in Canada: unlike in the US, where states had most of the powers to charter banks, the Canadian government was the one who decided whether or not to grant a bank charter, not the provinces. In 1890, there were 38 chartered banks in Canada and around 8000 in the US.

It is easy to understand why the Canadian banking system was more stable: nationwide branch network allowed banks to move liquidity around and continue to accept each others’ notes at par, and loan books were much more diversified and less prone to local asset quality deterioration. When branches in the West of the country were experiencing a liquidity shortage, it was easy to provide them with extra liquidity from their cousin in the East in order to avoid contagion as banks tried to protect their name and reputation. Moreover, the fact that only a few banks had large market shares in the country made it a lot easier to coordinate a response in times of financial tension, pretty much like the US clearinghouse system, but on a much larger scale.

The consequences of this design were that banks operated on thinner liquidity and capital buffers than banks in the US, as credit and liquidity risks could be consolidated and diversified away. Furthermore, credit was as available in Canada as in the US and deposit rates were higher, while banks were nonetheless more profitable thanks to centralised back office functions on a nationwide basis (i.e. economies of scale).

In the end, Canada experienced not a single bank failure during the Great Depression, despite having no central bank nor deposit insurance, the two tenets of current banking regulatory ‘good practices’.

What is striking from my series of posts on intragroup funding is that history is crystal clear: it is large, diversified, banking groups that represent a more stable ideal than insulated, but reinforced, smaller local banks. Unfortunately, most regulators and economists don’t seem to know much banking history…

The importance of intragroup funding – 19th century US vs. modern Germany

I recently explained the importance of intragroup liquidity and capital flows to prevent or help solve financial crises and why new regulations are weakening banks, and showed the inherent weakness in the design of the 19th century US banking system. Today I wish to highlight the similarities, and more importantly, the differences, between the 19th century US banking system and the modern German banking system.

As previously described, the peculiar US banking system had a multitude of tiny unit banks that were not allowed to branch, with very little financial flows and support behind them (at least until they started setting up local clearinghouses). By 1880, there were about 3,500 banks in the US, meaning about 1 bank for 14,000 people. Nowadays, there are about 1,800 banks in Germany, meaning one bank for 45,000 people. Germany’s banking system isn’t as fragmented as the 19th century US one, but it is still very fragmented by developed economies’ standards.

By comparison, in the UK, there is one bank for 410,000 people, though most banks have no retail banking market share, meaning this figure is probably way overestimated (my guess is that there is actually one bank for about 3m people). In Germany though, most banks have a retail banking market share: the banking system is divided between the large private banks (which actually don’t account for much of the local retail market share and focus mostly on corporate lending and investment banking), the cooperative banks group (the Volksbanken and Raiffeisenbanken, representing around 1,200 small retail banks), and the savings banks group, the largest banking group in Germany (the Sparkassen-Finanzgruppe, representing slightly less than 450 retail banks).

![]()

Those Sparkassen, for instance, cannot compete with each other and cannot branch out of their local area, making both their loan books and funding structures highly undiversified, with restrictions very similar to those that applied to 19th century US banks. Moreover, many of those banks have relatively small capital and liquidity buffers, at least compared to the US banks. Nevertheless, the Sparkassen have demonstrated remarkable resilience over time, experiencing very few failures (all have been bailed out). How to explain this?

First, all Sparkassen depend on local Landesbanks, which, quite similarly to clearinghouses in 19th century US, play the role of local central banks, moving liquidity around according to the needs of their Sparkassen members. This process alleviates acute liquidity crises. But this isn’t enough to avert regional crises or national, systemic ones.

Second, the Sparkassen rely on another mechanism: several regional and interregional support funds that allow healthy banks to recapitalise or provide liquidity to endangered sister Sparkassen. Those support funds can be complemented by extra contributions from healthy Sparkassen if ever needed. This mechanism is akin to some sort of intragroup funds flows*.

Here we go: instead of insulating each bank, raising barriers to allegedly make them more resilient, the Sparkassen allow funds to circulate when needed. They understand that the actual failure of one of their members would have catastrophic ramifications for the rest of the group (and for their shared credit rating). It is in their best interest to mutually support each other. But guess what? Some Sparkassen now fear that European regulators will take action to make such intragroup mutual support flows illegal…

* The Volksbanken have a relatively similar structure and intragroup support mechanism, though there are differences. Both groups are also actively involved in intragroup peer monitoring, which is important to limit moral hazard.

The importance of intragroup funding – The 19th century US experience

This is a follow-up post to my previous one on banks’ intragroup funding.

Financial and banking historians have known for a long time what the BoE believes it has ‘discovered’. A prime example of the importance of being able to move funds around (whether under the form of capital or liquidity) is the experience of US banking in the 19th century.

In the 19th century, the US was plagued by recurrent banking crises. This was mostly due to strict limitations on the development and growth of banks that basically isolated banks from each other. The result was known as ‘unit banking’. I am not going to enter into all the details (and this post mainly refers to the North of the US) but I strongly advise you to check the references at the bottom of this post.

The US’ political arrangements made it very difficult for the federal government to charter banks on a national basis, as the experiments of the First and the Second Banks of the United States demonstrate. States, on the other hand, could charter banks of issue within their borders to help finance the states’ expenditures. They also tended to forbid interstate branching in order not to leak out sources of funds to other states and artificially limit competition within their borders, as banking monopoly rents led to more abundant funding resources for the states (taxes could account for close to a quarter or even a third of total state financing). Many large cities ended up having a single bank at the very beginning of the 19th century.

The race for financing led states to charter increasingly more banks. However, new laws divided states into districts and allowed only a very limited number of banks to be chartered within each of them. Banks also did not have the right to open branches throughout the states. In the end, the whole banking system was completely fragmented in a myriad of small banks that enjoyed local monopolies.

From the 1830s, ‘free banks’ started to appear, a trend that accelerated following the 1837 banking crisis during which many banks failed throughout the country. This prompted a movement to increase competition in banking and access to credit for those who could not access the traditional, restricted, banking system. Free banks could be opened without any approval by state regulators. They still came to the funding need of state governments as the free banking laws required the full-backing of banknotes with high-quality securities, mostly government debt. Crucially, free banks were not allowed to branch. The previous system of larger banks that were constrained in their growth by their inability to open branch in other states, or simply in other districts, was progressively replaced by a system of a multitude of tiny ‘unit’ banks. In the end, the number of banks massively grew but unit banks often retained local monopolies. The federal government eventually tried to find ways to increase the number of nationally-chartered banks, but in the end those banks faced the same legal constraints that prevented free banks to branch.

There was political power behind those unit banks: because they couldn’t expand, unit banks were incentivised to lend to their local community even when times were tough (if they didn’t, they wouldn’t make any money and would fail anyway…). Banks were numerous (there were more than 27,000 banks in the US early-20th century, 95% of which had no branches…) but geographically isolated. As a result, they suffered from high levels of concentration in their loan books and deposit base, and were particularly badly hit by local economic problems. Liquidity risk was high and banks could hardly get hold of extra funds to face bank runs when they occurred.

Some banks tried to organise themselves into holding companies, owning several unit banks. However, the law prevented any financial or operational integration between various banks. The only thing they ended up sharing was a common ownership structure. A partial solution came up with the setup of clearinghouses, which basically settled interbank transactions, but also played the role of coordinator during local crises.

As a result of this poorly-designed banking structure, financial crises were recurrent: there were 11 of them between 1800 and 1914. Post-clearinghouses crises were nonetheless milder as clearinghouses allowed some liquidity to circulate.

Where does this lead us?

I described in my previous post how intragroup funding allows banking systems to remain more stable by allowing liquidity to circulate from stronger entities to weaker ones (this also applies to capital).

The 19th century US is an extreme example of what happens when you prevent this free movement of funds: a few banks fail and indirect contagion weakens even the stronger banks, leading to a systemic collapse. When banking groups are larger and free to move funds around, on the other hand, they have an incentive to reinforce their weaker links. Think about those 19th century ‘bank holdings’, which could not operationally integrate their various unit banks: the collapse of one of their ‘unit bank subsidiaries’ could potentially endanger the existence of all unit banks owned by that holding company through economic and financial contagion. Wouldn’t it be simpler to allow the transfer of funds from one unit bank to another to prevent any failure in the first place and actually reassure depositors that their banks are solid?

Unfortunately, current regulations aims at fragmenting and isolating national banking systems (and types of banks). This is likely to transform our globalised banking system into a mild version of what happened in the US, rather than into the stronger and more resilient systems that regulators hope to build. In the US, each unit bank had to maintain relatively high levels of capital and liquidity given their inherent weakness and lack of diversification. Was it enough to prevent crises? Not at all. This is in contrast with the Canadian experience, whose banking system comprised a few, very large, lightly regulated, branching banks. The Canadian banking system remained very stable throughout the period (and later).

More on 19th century Canada in a subsequent post.

Recommended readings:

- Charles A. Conant, A History of Modern Banks of Issue

- Charles Calomiris and Stephen Haber, Fragile by Design

- Christopher Whalen, Inflated: How Money and Debt Built the American Dream

- Milton Friedman and Anna Schwartz, A Monetary History of the United States

Update: I added one very important and great book to the list…

Felix Martin and the credit theory of money

I just finished reading a book that had been on my shelves for a few months, Money: The Unauthorised Biography, by Felix Martin (the book has only just been released in the US). Martin argues that our conventional view of money is wrong. Money isn’t a commodity used as a medium of exchange that evolved from the inconvenience of barter, but a system of mutual credit. Martin is not the first one to articulate this view, called the credit theory of money.

While overall Martin’s book is interesting, particularly for its historic descriptions and for bringing an ‘original’ view of the origins of money, it is plagued by a few problems and misinterpretations. Throughout the book, it feels like money, at least in its modern sense, is a ‘bad’ thing that is at the root of most of our current excesses, from inequality to financial crises. Perhaps, but the book never really discusses monetary calculation and economic efficiency. Money might have cons, but it also has pros. The fact that some ancient, very hierarchical – or even totally backward, societies were not using such ‘money’ is in no way something to be worried about…

Throughout his book, Martin seems to misinterpret former authors’ writings. Take Bagehot, whom Martin believes understood money and trust a lot better than most academic economists since then. Martin incorrectly reports Bagehot as saying that central banks should lend to insolvent banks. More importantly, he also didn’t seem to notice that Bagehot had never been a fan of the central banking system. In fact, Bagehot thought that system was not natural and even dangerous. This becomes a serious flaw of the book when Martin justifies his economic and reform ideas on a system that Bagehot himself saw as far from perfect.

Martin also seems to praise inflation without ever mentioning its downsides and the potential economic disruptions it can bring about. In turn, this leads him to praise… John Law. While John Law is most of the times seen as a model of economic mismanagement, Martin sees in him a ‘genius’, whose only faults was to have lived too early and to have believed in benevolent dictators:

Law’s system was ingenious, innovative and centuries ahead of his time.

To Martin, John Law’s system mainly failed because of… the vested interests of the old financial establishment! As with most other topics the book cover, I found this was a very selective reading of the historical facts.

This is the book’s main issue: it draws the wrong conclusions from a very superficial reading of history (including our latest financial crisis).

The book’s main thesis (admittedly, it’s also other people’s) suffers from the same problem. Why opposing credit theory of money and metalism? To me money can be both credit and commodity. This is not irreconcilable. Let’s suppose you provide me with a service or a product. The consequence of this transaction is that I am in credit to you. From there, what can you do? To settle the transaction, you can either accept one of my products or services. This is barter. Or you could use my ‘debt’ to you (my IOU) to purchase another product from someone else. However, in order to accept the ‘debt transfer’, the other person needs to make sure that my credit is good (i.e. that I will close the transaction at some point) in order to reduce the probability of losses (i.e. credit risk). This other person can further transfer my IOU, which ends up serving as money in a chain of transactions. Nevertheless, settlement (i.e. debt cancellation) is still expected at some point, and with no generally accepted medium of exchange, this settlement is similar to barter. This system still suffers from lack of granularity and from the double coincidence of wants problem.

Enter commodities. Excluding its barter-like issues, the process described above works, but involves credit risk. Developed societies discovered a way to reduce this credit risk to a minimum: a direct settlement of the IOU against what we view as the same value of a granular, easily transferable and measurable commodity. Think about it: you can either take the risk that my IOU will not be transferable any further or that I will fail to close the transaction, or you can settle the transaction directly by accepting some sort of commodity in exchange, which makes credit risk entirely disappear. But the system remains a system of credit: the only difference now is that IOU transfer chains end directly after the first transaction. This is still valid nowadays: everybody still says “how much do I owe you?” in order to pay for a good in store*.

(Note: of course if my credit is good, my IOU could still be transferred and ‘used’ as a medium of exchange, but would still merely remain a claim on the same easily transferable commodity.)

Strangely, Martin seems to downplay the settlement issue. He takes the Yap islands as an example of a pure system of credit money. But this is not accurate: Martin himself says that locals eventually settle their mutual debt using stone money (the fei/rai)!

I ended up quite confused about the book. It is hard to figure out what Martin really believes. Some of his proposals, such as money that would be some sort of state equity, look unworkable and closer to statist dreams than economic freedom; although this shouldn’t be surprising, as Martin never really questions the state, regulators and central bankers, and blindly accepts the Keynesian criticism of Say’s law. Money is more a history book than an economics book, but whether this is financial history or monetary theory you’re looking for, there is already a lot more comprehensive out there.

*The story I just described is essentially similar to Carl Menger’s theory of the origins of money. However, I added in a new factor: credit risk.

The Economist declares that financial crises are due to…

The Economist surprised me this week. In a good way.

Over the past few years, the newspaper’s main rhetoric has been that the financial system needed to be more regulated. From time to time, the ancient roots of the venerable newspaper seemed to make a comeback to denounce the increasing red tape that financial businesses were now subject to. But overall, The Economist seemed to have been partly taken over by statist fever and the general editorial line was: regulation and inflation will be the saviours of our capitalist system. Unsurprisingly, I tended to disagree (euphemism spotted).

When this week The Economist decided to publish two articles under the umbrella title of A History of Finance in Five Crises, and How the Next One Could be Prevented (see here and here), I was very sceptical. I was indeed expecting the usual arguments that bankers try to abuse the system, that regulation is necessary to prevent those abuses, that more central bank control of the financial system is a good thing, that financial innovations should be regulated out of existence.

I was plain, delightfully, wrong.

This is The Economist:

Whatever was wrong with the American housing market, it was not lack of government: far from a free market, it was one of the most regulated industries in the world, funded by taxpayer subsidies and with lending decisions taken by the state.

Amen.

In a very timely and remarkable echo to my very recent post on the obsession of financial stability, the newspaper also pointed out the risk of too much protection:

The more the state protected the system, the more likely it was that people in it would take risks with impunity.

[…] In many cases the rationale for the rules and the rescues has been to protect ordinary investors from the evils of finance. Yet the overall effect is to add ever more layers of state padding and distort risk-taking.

This fits an historical pattern. As our essay this week shows, regulation has responded to each crisis by protecting ever more of finance. Five disasters, from 1792 to 1929, explain the origins of the modern financial system. This includes hugely successful innovations, from joint-stock banks to the Federal Reserve and the New York Stock Exchange. But it has also meant a corrosive trend: a gradual increase in state involvement.

The newspaper even attacked… deposit insurance! Blasphemy! To tell you the truth, I still find it hard to believe:

The numbers would amaze Bagehot. In America a citizen can now deposit up to $250,000 in any bank blindly, because that sum is insured by a government scheme: what incentive is there to check that the bank is any good?

[…] Today America is an extreme case, but insurance of over $100,000 is common in the West. This protects wealth, and income, and means investors ignore creditworthiness, worrying only about the interest-rate offer, sending deposits flocking to flimsy Icelandic banks and others with pitiful equity buffers.

[…] How can the zombie-like shuffle of the state into finance be stopped? Deposit insurance should be gradually trimmed until it protects no more than a year’s pay, around $50,000 in America. That is plenty to keep the payments system intact. Bank bosses might start advertising their capital ratios, as happened before deposit insurance was introduced.

Those are two brilliant articles. Personally, I find that very encouraging. It means that my blog, as well as the work of the very few people who think like me, aren’t pointless.

Dear Economist, welcome back.

(and please stay with us this time)

Bundesbank’s Dombret has strange free market principles

Andreas Dombret, member of the executive board of the Bundesbank, made two very similar speeches last week (The State as a Banker? and Striving to achieve stability – regulations and markets in the light of the crisis). When I started to read them, I was delighted. Take a look:

If one were to ask the question whether or not the market economy merits our trust, another question has to be added immediately: “Does the state merit our trust?”

[…]

Sometimes it seems as if we are witnessing a transformation of values and a redefinition of fundamental concepts. The close connection between risk-taking and liability, which is an important element of a market economy, has weakened.

Conservative and risk-averse business models have become somewhat old-fashioned. If the state is bearing a significant part of the losses in the case of a default of a bank, banks are encouraged to take on more risks.

[…]

[High bonuses and short-termism] are the result of violated market principles and blurred lines between the state and the banks. They are not the result of a well-designed market economy but rather indicative of deformed economies. However, the market economy stands accused of these faults.

Brilliant. I was just about to become a Dombret fan when…I read the rest:

In my view, the solution is to be found in returning the state to its role of providing a framework in which the private sector can operate. This means a return to the role the founding fathers of the social market economy had in mind.

They knew that good banking regulation is a key element of a well-designed framework for a well-functioning banking industry and a proper market economy in general.

[…]

This is where good bank capitalisation comes into play. It is the other side of the coin. Good regulation should directly address the key problem. If the system is too fragile, an important and direct measure to reduce fragility is to have enough capital.

[…]

Good capitalisation will have the positive side effect of reducing many of the wrong incentives and distortions created by taxpayers’ implicit guarantees and therefore making the bail-in threat more credible ex ante.

And from the second article:

In view of all this, I believe that two elements will be especially important in making banks more stable: capital and liquidity. Deficits in both of these things were factors which contributed significantly to the financial crisis. The state can bring in regulation to address these deficits, and has done so very successfully.

And on shadow banking:

In terms of financial stability, the crux of the matter is that these entities can cause similar risks to banks but are not subject to bank regulation.And the shadow banking system can certainly generate systemic risks which pose a threat to the entire financial system.

Much the same applies to insurance companies. Although they aren’t a direct component of the shadow banking system, they can also be a source of systemic risk. All of this makes it appropriate to extend the reach of regulation.

Sorry but I will postpone joining the fan club…

Mr. Dombret correctly identifies the issue with the financial system: too much state involvement. What is his solution? More state involvement. It is hard to believe that one person could come up with the exact same solution that had not worked in the past. Were the banks not already subject to capital requirements before the crisis? Even if not ‘high’ enough they were still higher than no capital requirement at all. So in theory they should have at least mitigated the crisis. But the crisis was the worst one since 1929, and much worse than previous ones during which there were no capital requirements. Efficient regulation indeed…

Like 95% of regulators, he makes such mistakes because of his (voluntary?) ignorance of banking history. A quick look at a few books or papers such as this one, comparing US and Canadian banking systems historically, would have shown him that Canadian banks were more leveraged than US banks on average since the early 19th century, yet experienced a lot fewer bank failures. There is clearly so much more at play than capital buffers in banking crises…

Moreover, he views formerly ‘low’ capital requirements as a justification for bankers to take on more risks to generate high return on equity. This doesn’t make sense. For one thing, the higher the capital requirements the higher the risks that need to be taken on to generate the same RoE. It also encourages gaming the rules. This is what is currently happening, as banks are magically managing to reduce their risk-weighted assets so that their regulatory-defined capital ratios look healthier without having to increase their capital.

Mr. Dombret starts by seriously questioning the state’s ability to manage the system and highlights the very harmful and distortive effects of state regulation to eventually… back further and deeper state regulation.

A question Mr. Dombret: what are we going to do following the next crisis? Continue down the same road?

Can please someone remind Mr. Dombret of what a free market economy, which he seems to cherish, means?

Picture: Marius Becker

Recent Comments