Why the Austrian business cycle theory needs an update

I have been thinking about this topic for a little while, even though it might be controversial in some circles. By providing me with a recent paper empirically testing the ABCT, Ben Southwood, from ASI, unconsciously forced my hand.

I really do believe that a lot more work must be done on the ABCT to convince the broader public of its validity. This does not necessarily mean proving it empirically, which is always going to be hard given the lack of appropriate disaggregated data and the difficulty of disentangling other variables.

However, what it does mean is that the theoretical foundations of the ABCT must be complemented. The ABCT is an old theory, originally devised by Mises a century ago and to which Hayek provided a major update around two decades later. The ABCT explains how an ‘unnatural’ expansion of credit (and hence the money supply) by the banking system brings about unsustainable distortions in the intertemporal structure of production by lowering the interest rate below its Wicksellian natural level. As a result, the theory is fully reliant on the mechanics of the banking sector.

The theory is fundamentally sound, but its current narrative describes what would happen in a relatively free market with a relatively free banking system. At the time of Mises and Hayek, the banking system indeed was subject to much lighter regulations than it is now and operated differently: banks’ primary credit channel was commercial loans to corporations. The Mises/Hayek narrative of the ABCT perfectly illustrates what happens to the economy in such circumstances. Following WW2, the channel changed: initiative to encourage home building and ownership resulted in banks’ lending approximately split between retail/mortgage lending and commercial lending. Over time, retail lending developed further to include an increasingly larger share of consumer and credit card loans.

Then came Basel. When Basel 1 banking regulations were passed in 1988, lending channels completely changed (see the chart below, which I have now used several times given its significance). Basel encouraged banks’ real estate lending activities and discouraged banks’ commercial lending ones. This has obvious impacts on the flow of loanable funds and on the interest rate charged to various types of customers.

In the meantime, banking regulations have multiplied, affecting almost all sort of banking activities, sometimes fundamentally altering banks’ behaviour. Yet the ABCT narrative has roughly remained the same. Some economists, such as Garrison, have come up with extra details on the traditional ABCT story. Others, such as Horwitz, have mixed the ABCT with Yeager’s monetary disequilibrium theory (which is rejected by some other Austrian economists).

While those pieces of academic work, which make the ABCT a more comprehensive theory, are welcome, I argue here that this is not enough, and that, if the ABCT is to convince outside of Austrian circles, it also needs more practical, down to Earth-type descriptions. Indeed, what happens to the distortions in the structures of production when lending channels are influenced by regulations? This requires one to get their hands dirty in order to tweak the original narrative of the theory to apply it to temporary conditions. Yet this is necessary.

Take the paper mentioned at the beginning of this post. The authors find “little empirical support for the Austrian business cycle theory.” The paper is interesting but misguided and doesn’t disprove anything. Putting aside its other weaknesses (see a critique at the bottom of this post*), the paper observes changes in prices and industrial production following changes in the differential between the market rate of interest and their estimate of the natural rate. The authors find no statistically significant relationship.

Wait a minute. What did we just describe above? That lending channels had been altered by regulation and political incentives over the past decades. What data does the paper rely on? 1972 to 2011 aggregate data. As a result, the paper applies the wrong ABCT narrative to its dataset. Given that lending to corporations has been depressed since the introduction of Basel, it is evident that widening Wicksellian differentials won’t affect industrial structures of production that much. Since regulation favour a mortgage channel of credit and money creation, this is where they should have looked.

But if they did use the traditional ABCT narrative, it is because no real alternative was available. I have tried to introduce an RWA-based ABCT to account for the effects of regulatory capital regulation on the economy. My approach might be flawed or incomplete, but I think it goes in the right direction. Now that the ABCT benefits from a solid story in a mostly unhampered market, one of the current challenges for Austrian academics is to tweak it to account for temporary regulatory-incentivised banking behaviour, from capital and liquidity regulations to collateral rules. This is dirty work. But imperative.

Major update here: new research seems to confirm much of what I’ve been saying about RWAs and the changing nature of financial intermediation.

* I have already described above the issue with the traditional description of the ABCT in this paper, as well as the dataset used. But there are other mistakes (which also concern the paper they rely on, available here):

– It still uses aggregate prices and production data (albeit more granular): the ABCT talks about malinvestments, not necessarily of overinvestment. The (traditional) ABCT does not imply a general increase in demand across all sectors and products. Meaning some lines of production could see demand surge whereas other could see demand fall. Those movements can offset each other and are not necessarily reflected in the data used by this study.

– It seems to consider that aggregate price increases are a necessary feature of the ABCT. But inflation can be hidden. The ABCT relies on changes in relative prices. Moreover, as the structure of production becomes more productive, price per unit should fall, not increase.

New research on finance and Austrian capital theories

Two brand new pieces of academic research have been published last month, directly or indirectly related to the Austrian theory of the business cycle (some readers might already know my RWA-based ABCT: here, here, here and here).

The first one, called Roundaboutness is Not a Mysterious Concept: A Financial Application to Capital Theory (Cachanosky and Lewin) attempts to start merging ABCT (or rather, Austrian capital theory) with corporate finance theory. The authors use the finance concepts of economic value added (EVA), modified duration, Macaulay duration and convexity in order to represent the Austrian concepts of ‘roundaboutness’ and ‘average period of production’. The paper provides a welcome and well-defined corporate finance background to the ABCT.

However, finance practitioners still don’t have the option to use a ‘full-Austrian’ alternative financial framework, as this paper still relies on some mainstream concepts. For instance, the EVA calculation for a given period t is as follows:

where ROIC is the return on invested capital, WACC the weighted average cost of capital and K the financial capital invested.

In order to compute the project’s market value added (MVA, i.e. whether or not the project has added value), it is then necessary to discount the expected future EVAs of each period t1, t2…, T, by the WACC of the project:

The WACC represents the minimum return demanded by investors to compensate for the risk of such a project (i.e. the opportunity cost), and is dependent on the interest rate level. The problem arises in the way it is calculated in modern mainstream finance. While the cost of debt capital is relatively straightforward to extract, the cost of equity capital is commonly computed using the capital asset pricing model (CAPM). Unfortunately, the CAPM is based on the Modern Portfolio Theory, itself based on new-classical economics and rational expectations/efficient market hypothesis premises, which are at odds with Austrian approaches.

(And I am not even mentioning some of the very dubious assumptions of the theory, such as “all investors can lend and borrow unlimited amounts at the risk-free rate of interest”…)

While it is easy for researchers to define a cost of equity for a theoretical paper, practitioners do need a method to estimate it from real life data. This is how the CAPM comes in handy, whereas the Austrian approach still has no real alternative to suggest (as far as I know).

Nevertheless, putting the cost of equity problem aside, the authors view the MVA as perfectly adapted to capital theory:

Note that the MVA representation captures the desired characteristics of capital-theory; (1) it is forward looking, (2) it focuses on the length of the EVA cash-flow, and (3) it captures the notion of capital-intensity.

Using the corporate finance framework outlined above, the authors easily show that the more capital intensive investments are the more they are sensitive to variations in interest rates (i.e. they have a larger ‘convexity’). They also show that more ‘roundabout’/longer projects benefit proportionally more from a decline in interest rates than shorter projects. Unsurprisingly, those projects are also the first ones to suffer when interest rates start going up.

The following chart demonstrates the trajectory of the MVA of both long time horizon (high roundabout – HR) and short time horizon (low roundabout – LR) projects as a function of WACC.

Overall, this is a very interesting paper that contains a lot more than what I just described. I wish more research was undertaken on that topic though.

The second paper, pointed by Tyler Cowen, while not directly related to the ABCT, nonetheless has several links to it (I am unsure why Cowen thinks this piece of research actually reflects the ABCT). What’s interesting in this paper is that it seems to confirm the link between credit expansion, financial instability and banks stock prices, as well as the ‘irrationality’ of bank shareholders, who do not demand a higher equity premium when credit expansion occurs (which doesn’t seem to fit the rational expectations framework very well…).

The obsession of stability

One of the outcomes of the financial crisis has been that regulators are now obsessed with instability. Or stability. Or both.

They have been on a crusade to eliminate the evil risks to ‘financial stability’, and nothing seems to be able to stop them (ok, not entirely true). Banks, shadow banking, peer-to-peer lending, crowdfunding, private equity, payday lenders, credit cards…

Their latest target is asset managers. In a new speech at London Business School, Andrew Haldane, a usually ‘wise’ regulator, seems to have now succumbed to the belief that regulators know better and have the powers to control and regulate the whole financial industry (see also here). This is worrying.

Haldane now views every large asset manager as dangerous and many investment strategies as potentially amplifying upward or downward spiral in asset prices, representing ‘flaws’ in financial markets that regulators ought to fix. I believe this is strongly misguided.

In their quest to cure markets from any instability, regulators are annihilating the market process itself. I would argue that some level of instability is not only necessary, but is also desirable.

First, instability reflects human action; the allocation of resources by investors and entrepreneurs. Some succeed, some fail, prices go up, prices go down, everybody adapts. Sometimes many, too many, investors believe that a new trend is emerging, indeed amplifying a market movement and subsequently leading to a crash. But crashes and failures are part of the learning process that is inherent to any capitalist and market-based society. Suppress or postpone this process and don’t be surprised when very large crashes occur. On the other hand, an unhampered market would naturally limit the size of bubbles and their subsequent crashes as market actors continuously learn from their mistakes.

Second, instability enhances risk management. Instability is necessary because it induces fear in markets participants’ behaviour, who then take risks more seriously. By suppressing instability, regulators would suppress risk assessment and encourage risky behaviours: “there is nothing to fear; regulators are making sure markets are stable.” The illusion of safety is one of the most potent risks there is.

Nevertheless, regulators, on their quest for the Holy Grail of stability, want to regulate again and again. On the back of flawed instability or paternalistic consumer protection arguments, and despite seemingly showing poor understanding of financial industries, they are trying to implement regulations that would at best limit, at worst dictate, market actors’ capital allocation decisions. Adam Smith would turn in his grave (along with his invisible hand, who is now buried next to him).

In the end, regulators’ obsession for stability and protection creates even stronger systemic risks. In fact, the only ‘stable’ society is what Mises called the evenly-rotating economy, the one that never experiments. Nothing really attractive.

Funny enough, in his speech, Haldane even acknowledged regulation as one of the reasons underlying some of the current instability:

Risk-based regulatory rules can contribute further to these pro-cyclical tendencies. […]

There have been several incidences over recent years of regulators loosening regulatory constraints to forestall concerns about pro-cyclical behaviour in a downswing. […]

In particular, regulation and accounting appear to have played a significant role.

I guess he didn’t get the irony.

Banks’ RWAs as a source of malinvestments – A graphical experiment

Today is going to be experimental and theoretical. I have already outlined the principles behind the RWA-based variation of the Austrian Business Cycle Theory (ABCT), which was followed by a quick clarification. I am now attempting to come up with a graphical representation to illustrate its mechanism. In order to do that, I am going to use Roger Garrison’s capital structure-based macroeconomics representations used in his book Time and Money: The Macroeconomics of Capital Structure. I am not saying that what I am about to describe is 100% right. Remember that this remains an experiment that I just wrote down over those last few days and that needs a lot more development. There may well also be other ways of depicting the impacts that Basel regulation’s RWAs have on the capital structure and malinvestments. Completely different analytical frameworks might also do. Comments and suggestions are welcome.

This is what Garrison’s representation of the macroeconomics of capital structure looks like:

It is composed of three elements:

- Bottom right: this is the traditional market for loanable funds, where the supply and demand for loanable funds cross at the natural rate of interest. It represents economic agents’ intertemporal preferences: the higher they value future goods over present goods, the more they save and the lower the interest rate. The x-axis represents the quantity of savings supplied (and investments) and the y-axis represents the interest rate.

- Top right: this is the production-possibility frontier (PPF). In Garrison’s chart, it represents the sustainable trade-off between consumption and gross investment. Only movements along the frontier are sustainable and supposed to reflect economic agents’ preferences. Positive net investments and technological shocks expand the frontier as the economy becomes more productive.

- Top left: this is the Hayekian triangle. It represents the various stages of production (each adding to output) within an industry. See details below:

I don’t have time to come back to the original ABCT and those willing to find out more about it can find plenty of examples online. Today I wish only to try to understand the impact of regulatory-defined risk-weighted assets on this structure. Ironically, it becomes necessary to disaggregate the Austrian capital-based framework to understand the mechanics and distortions leading to a likely banking crisis. In everything that follows, and unlike in the original Austrian theory, we exclude central banks from the picture (i.e. no monetary injection). We instead focus only on monetary redistribution. The story outlined below does not explain the financial crisis by itself. Rather, it outlines a regulatory mechanism that exacerbated the crisis.

I don’t have time to come back to the original ABCT and those willing to find out more about it can find plenty of examples online. Today I wish only to try to understand the impact of regulatory-defined risk-weighted assets on this structure. Ironically, it becomes necessary to disaggregate the Austrian capital-based framework to understand the mechanics and distortions leading to a likely banking crisis. In everything that follows, and unlike in the original Austrian theory, we exclude central banks from the picture (i.e. no monetary injection). We instead focus only on monetary redistribution. The story outlined below does not explain the financial crisis by itself. Rather, it outlines a regulatory mechanism that exacerbated the crisis.

Let’s take a simple example that I have already used earlier. Only two types of lending exist: SME lending and mortgage/real estate lending. Basel regulations force banks to use more capital when lending to SME and as a result, bankers are incentivised to maximise ROE through artificially increasing mortgage lending and artificially restricting SME lending, as described in my first post on the topic.

In equilibrium and in a completely free-market world with no positive net investment, the economy looks like Garrison’s chart above. However, bankers don’t charge the Wicksellian natural rate of interest to all customers: they add a risk premium to the natural rate (effectively a ‘risk-free’ rate) to reflect the risk inherent to each asset class and customer. Those various rates of interest do reflect an equilibrium (‘natural’) state, which factors in the free markets’ perception of risk. Because lending to SME is riskier than mortgage lending, we end up with:

natural (risk free) rate < mortgage rate (natural rate + mortgage risk premium) < SME rate (natural rate + SME risk premium)

What RWAs do is to impose a certain perception of risk for accounting purposes, distorting the normal channelling of loanable funds and therefore each asset class’ respective ‘natural’ rate of interest. Unfortunately, depicting all demand and supply curves, their respective interest rates and the changes when Basel-defined RWAs are applied would be extremely messy in a single chart. We’re going to illustrate each asset class separately with their respective demand and supply curve. Let’s start with mortgage (real estate) lending:

Given the incentives they have to channel lending towards capital-optimising asset classes, bankers artificially increase the supply of loanable funds to all real estate activities, pushing the rate of interest below the natural rate of the sector. As the actual total supply of loanable funds does not change, returns on savings remain the same. In our PPF, this pushes resources towards real estate. Any other industry would interpret the lowered rate of interest as a shift in people’s intertemporal preferences towards the future and increase long-term investments at the expense of short-term production. Indeed, long-term housing projects are started. This is represented by the thin dotted red triangle.

Given the incentives they have to channel lending towards capital-optimising asset classes, bankers artificially increase the supply of loanable funds to all real estate activities, pushing the rate of interest below the natural rate of the sector. As the actual total supply of loanable funds does not change, returns on savings remain the same. In our PPF, this pushes resources towards real estate. Any other industry would interpret the lowered rate of interest as a shift in people’s intertemporal preferences towards the future and increase long-term investments at the expense of short-term production. Indeed, long-term housing projects are started. This is represented by the thin dotted red triangle.

However, the short-term housing supply is inelastic and cannot be reduced. The resulting real estate structure of production is the plain red triangle. Nonetheless, real estate developers have been tricked by the reduced interest rate and the long-term housing projects they started do not match economic agents’ future demand. Meanwhile, savers, adequately rewarded for their savings, do not draw down on them (or don’t have to), but are instead incentivised to leverage as they (indirectly) see profit opportunities from the differential between the natural and the artificially reduced rate. Leverage effectively becomes a function of the interest rate differential:

The increased leverage boosts the demand for existing real estate, bidding up prices, starting a self-reinforcing trend based on expected further price increases. We end up in a temporary situation of both short-term ‘overconsumption’ of real estate and its associated goods, and long-term overinvestments (malinvestments). This situation is depicted by the thick dotted red triangle and represents an unsustainable state beyond the PPF.

On the other hand, bankers artificially restrict the supply of loanable funds to SME, pushing the rate of interest above the natural rate. Tricked by a higher rate of interest, SMEs are led to believe that consumers now value more highly present goods over future goods (as they ‘apparently’ now save less of their income). They temporarily reduce interest rate-sensitive long-term investments to increase the production of late stages consumer goods. This results in an overproduction of consumer goods relative to economic agents’ underlying present demand. Nonetheless, wealth effects from the real estate boom temporarily boost consumption, maintaining prices level. Overconsumption of present goods could also eventually appear if and when savers start leveraging their consumption through low-rate mortgages, as house prices seem to keep increasing. In the long-run, SMEs’ investments aren’t sufficient to satisfy economic agents’ future demand of consumer goods.

With leverage increasing and the economy producing beyond its PPF, the situation is unsustainable. As increasingly more people pile in real estate, demand for real estate loanable funds increases, pushing up the interest rate of the sector. Interest payments – which had taken an increasingly large share of disposable income in line with growing leverage – rise, putting pressure on households’ finances. The economy reaches a Minsky moment and real estate prices start coming down. Real estate developers, who had launched long-term housing projects tricked by the low rates, find out that these are malinvestments that either cannot find buyers or are lacking the financial resources to be completed. Bankruptcies increase among over-leveraged households and companies. Banks start experiencing losses, contract lending and money supply as a result, whereas savers’ demand for money increases. The economy is in monetary disequilibrium. Welcome to the financial crisis designed in the Swiss city of Basel.

This all remains very theoretical and I’ll try to dig up some empirical evidences in another post. Nonetheless, the story seems to match relatively well what happened in some countries during the crisis. Soon after Basel regulations were implemented, household leverage in Spain or Ireland took off and came along with increasing house prices and retail sales, which both collapsed once the crisis struck. Under this framework, the artificially restricted supply of loanable funds to SME and the consequent reduction in long-term investments could also partly explain the rich world manufacturing problems. However, I presented a very simple template. As I mentioned in a previous post, securitisation and other banking regulations (liquidity…) blur the whole picture, and central banks can remain the primary channel through which interest rates are distorted.

RWA-based ABCT Series:

- Banks’ risk-weighted assets as a source of malinvestments, booms and busts

- Banks’ RWAs as a source of malinvestments – Update

- Banks’ RWAs as a source of malinvestments – A graphical experiment

- Banks’ RWAs as a source of malinvestments – Some recent empirical evidence

- A new regulatory-driven housing bubble?

Banks’ risk-weighted assets as a source of malinvestments, booms and busts

Here I’m going to argue that Basel-defined risk-weighted assets, a key component of banking regulation, may be partly responsible for recent business cycles.

Readers might have already noticed my aversion to risk-weighted assets (RWAs), which I view as abominations for various reasons. They are defined by Basel accords and used in regulatory capital ratios. Basel I (published in 1988 and enforced from 1992) had fixed weights by asset class. For example, corporate loans and mortgages would be weighted respectively 100% and 50%, whereas OECD sovereign debt would be weighted 0%. If a bank had USD100bn of total assets, applying risk-weights could, depending on the lending mix of the bank, lead to total RWAs of anything between USD20bn to USD90bn. Regulators would then take the capital of the bank as defined by Basel (‘Tier 1’ capital, total capital…) and calculate the regulatory capital ratio of the bank: Tier 1 capital/RWAs. Basel regulation required this ratio to be above 4%.

Basel II (published in 2004 and progressively implemented afterwards) introduced some flexibility: the ‘Standardised method’ was similar to Basel I’s fixed weights with more granularity (due to the reliance on external credit ratings), while the various ‘Internal Ratings Based’ methods allowed banks to calculate their own risk-weight based on their internal risk management models (‘certified’ by regulators…).

This system is perverse. Banks are profit-maximising institutions that answer to their shareholders. Shareholders on the other hand have a minimal threshold under which they would not invest in a company: the cost of capital, or required return on capital. As a result, return on equity (ROE) has to at least cover the cost of capital. If it doesn’t, economic losses ensue and investors would have been better off investing in lower yielding but lower risk assets in the first place. But Basel accords basically dictate banks how much capital they need to hold. Therefore banks have an incentive in trying to ‘manage’ capital in order to boost ROE. Under Basel, this means pilling in some particular asset classes.

Let’s make very rough calculations to illustrate the point under a Basel II Standardised approach: a pure commercial bank (i.e. no trading activity) has a choice between lending to SMEs (option 1) or to individuals purchasing homes (option 2). The bank has EUR1bn in Tier 1 capital available and wishes to maximise returns while keeping to the minimum of 4% Tier 1 ratio. We also assume that external funding (deposits, wholesale…) is available and that the marginal increase in interest expense is always lower than the marginal increase in interest income.

- Option 1: Given the 100% risk-weight on SME lending, the bank could lend EUR25bn (25bn x 100% x 4% = 1bn), at an interest rate of 7% (say), equalling EUR1.75bn in interest income.

- Option 2: Mortgage lending, at a 35% risk-weight, allows the same bank to lend a total of EUR71.4bn (71.4bn x 35% x 4% = 1bn) for EUR1bn in capital, at an interest rate of 3% (say), equalling EUR2.14bn in interest income.

The bank is clearly incentivised to invest its funding base in mortgages to maximise returns. In practice, large banks that are under the IRB method can push mortgage risk-weights to as low as barely above 10%, and corporate risk-weights to below 50%. As a result, banks are involuntarily pushed by regulators to game RWAs. The lower RWAs, the lower capital the bank needs, the higher its ROE and the happier the regulators. Banks call this ‘capital optimisation’.

Consequently, does it come as a surprise that low-risk weighted asset classes were exactly the ones experiencing bubbles in pre-crisis years? Oh sorry, you don’t know which asset classes were lowly rated… Here they are: real estate, securitisation, OECD sovereign debt. Yep, that’s right. Regulatory incentives that create crises. And the new Basel III regime does pretty much nothing to change the incentivised economic distortions introduced by its predecessors.

Yesterday, Fitch, the rating agency, published a study of lending and RWAs among Europe’s largest banks (press release is available here, full report here but requires free subscription). And, what a surprise, corporate lending is going…down, while mortgage lending and credit exposures to sovereigns are going…up (see charts below). The trend is even exacerbated as banks are under pressure from regulators to boost regulatory capitalisation and from shareholders to improve ROE. And this study only covers IRB banks. My guess is that the situation is even more extreme for Standardised method banks that cannot lower their RWAs.

The ‘funny’ thing is: not a single regulator or central banker seems to get it. As a result, we keep seeing ill-founded central banks schemes aiming at giving SME lending a boost, like the Funding for Lending Scheme launched by the Bank of England in 2012, which provided banks with cheap funding. Yes, you guessed it: SME lending continued its downward trend and the scheme provided mortgage lending a boost.

Should the situation ‘only’ prevent corporates to borrow funds, bad economic consequences would follow but remain limited. Economic growth would suffer but no particular crisis would ensue. The problem is: Basel and RWAs force a massive misallocation of capital towards a few asset classes, resulting in bubbles and large economic crises when the crash occurs.

The Mises and Hayek Austrian business cycle theory emphasises the distortion in the structure of relative prices that emanates from central banks lowering the nominal interest rate below the natural rate of interest as represented by economic agents’ intertemporal preferences, resulting in monetary disequilibrium (excess supply of money). The consequent increase in money supply flows in the economy through one (or a few) entry points, increasing the demand in those sectors, pushing up their prices and artificially (and unsustainably) increasing their return on investment.

I argue here that due to Basel’s RWAs distortions, central banks could even be excluded from the picture altogether: banks are naturally incentivised to channel funds towards particular sectors at the expense of others. Correspondingly, the supply of loanable funds increases above equilibrium in the favoured sectors (hence lowering the nominal interest rate and bringing about an unsustainable boom) but reduces in the disfavoured ones. There can be no aggregate overinvestment during the process, but bad investments (i.e. malinvestments) are undertaken: the investment mix changes as a result of an incentivised flow of lending, rather than as a result of economic agents’ present and future demand. Eventually, the mismatch between expected demand and actual demand appears, malinvestments are revealed, losses materialise and the economy crashes. Central banks inflation worsen the process through the mechanism described by the Austrians.

I am not sure that regulators had in mind a process to facilitate boom and bust cycles when they designed Basel rules. The result is quite ‘ironic’ though: regulations developed to enhance the stability of the financial sector end up being one of the very sources of its instability.

RWA-based ABCT Series:

- Banks’ risk-weighted assets as a source of malinvestments, booms and busts

- Banks’ RWAs as a source of malinvestments – Update

- Banks’ RWAs as a source of malinvestments – A graphical experiment

- Banks’ RWAs as a source of malinvestments – Some recent empirical evidence

- A new regulatory-driven housing bubble?

The investors’ great search for yield (and the likely collapse?)

Quite a long post… Here I’m going to have to get to the heart of my theoretical economic beliefs. I’ll try to keep it simple and as short as I can though. I will argue that there are many risks to investors going forward due to distortions in interest rates.

I wasn’t surprised yesterday when I read the two following FT articles. The first one tells how leveraged buyouts (LBOs) in the US have boomed recently, with leverage reaching the height of the pre-crisis boom of 5.3 times EBITDA, some even reaching 7.5 times EBITDA. This means that the private equity funds that acquired those firms used debt equivalent to 5 times earnings before depreciation, interest and taxes of the targets to fund the acquisitions. It is a lot. What is usually considered a highly leveraged LBO is around 4 times EBITDA and higher.

The second FT article talks about the fact that hedge funds are struggling to achieve high returns due to the size of the industry. Institutional investors have piled in hedge funds expecting higher returns than what traditional investments yield at the moment.

Earlier this year, we have seen many investors also piling in junk bonds, offering some of the lowest non-investment grade yields on record (despite the economy still not being in great shape and spreads over US treasuries not being at their lowest level ever). What’s going on?

Many people won’t agree with that, but to me, it looks like central banks’ monetary policies (low interest rates, quantitative easing, LTRO, OMT…) are lowering interest rates below their so-called ‘natural rates’. What is the natural rate of interest? It was the Swedish economist Knut Wicksell who came up with this term, highlighting to him the equivalent of the equilibrium free-market rate of interest in a barter world. Wicksell defined the natural rate in those terms in his 1898 book Interest and Prices, chapter 8:

“There is a certain rate of interest on loans which is neutral in respect to commodity prices, and tends neither to raise nor to lower them. This is necessarily the same as the rate of interest which would be determined by supply and demand if no use were made of money and all lending were effected in the form of real capital goods. It comes to much the same thing to describe it as the current value of the natural rate of interest on capital.” (emphasis his)

We can interpret it as the equilibrium interest rate that would exist under free market conditions, with no external interferences such as central banks’ monetary policies and governments’ interest-lowering schemes. In such conditions, intertemporal preferences between savers and borrowers are matched. This natural rate is in opposition to the ‘money rate of interest’, or the actual interest rate prevalent in a money and credit economy. The system is near equilibrium when the natural and the money rates coincide.

At the moment, some people such as Scott Sumner would argue that the natural rate of interest is below zero, justifying massive cash injection in the economy in order to lower the money rate of interest (= nominal interest rate). For him, the evidence is that nominal GDP has been allowed to fall below trend during the crisis and hasn’t recovered since then. While I agree that there was a case for an increase in the quantity of money to counteract a higher demand for money in the earlier stages of the crisis, I don’t believe this is now necessary. (I also believe that ‘trend’ is a very imperfect indicator on which to base policies. NGDP growth trend changed several times since World War 2 and can also be impacted over fairly long periods by unsustainable booms).

But it does continue. There have now been several rounds of QE in the US and monetary easing in Europe, Japan and China, to name a few. So the current situation looks like a sign that the money rate of interest has been pushed below the natural rate for quite some time. While nominal interest rates have been low for a while, real interest rates are now even lower (or even negative). And real interest rates are what investors care about, as it represents the actual gain over cost of life inflation. This has the consequence of pushing investors toward higher-yielding asset classes (hedge funds, private equity, junk bonds, emerging market equities…), in order to generate the returns they normally get on lower-risk assets.

But there is no inflation, you’re going to tell me. True, inflation as measured by CPI has also been relatively low for a while. Is CPI the right measure though? Asset prices (from real estate to equities and bonds) are not reflected in it despite arguably representing a form of inflation. Remember what Wicksell said: “There is a certain rate of interest on loans which is neutral in respect to commodity prices, and tends neither to raise nor to lower them.” Well… It’s clearly not what’s happening now. Even excluding asset classes, CPI may even not accurately reflect goods’ prices inflation. Would investors really need to search for yield if the cost of life actually declined or remained stable?

Does it mean that asset prices should always remain stable at the natural rate? Not at all, and there can be good reasons why asset prices move (real supply shocks for example). But what we can now witness in financial markets look more like malinvestments than anything else. Malinvestments represent bad allocation of capital to investments that would not be profitable under natural rate of interest conditions. As the discount rate on those investments decline in line with the nominal interest rate, they suddenly look attractive from a risk-reward point of view. But what if the discount rate is wrong in the first place? And what if future cash flows are also artificially boosted by low rates? This is a variation of the original Austrian business cycle theory, first developed by Ludwig von Mises and F.A. Hayek early 20th century, and which originally focused on the effects of a distorted interest rate on the structure of production.

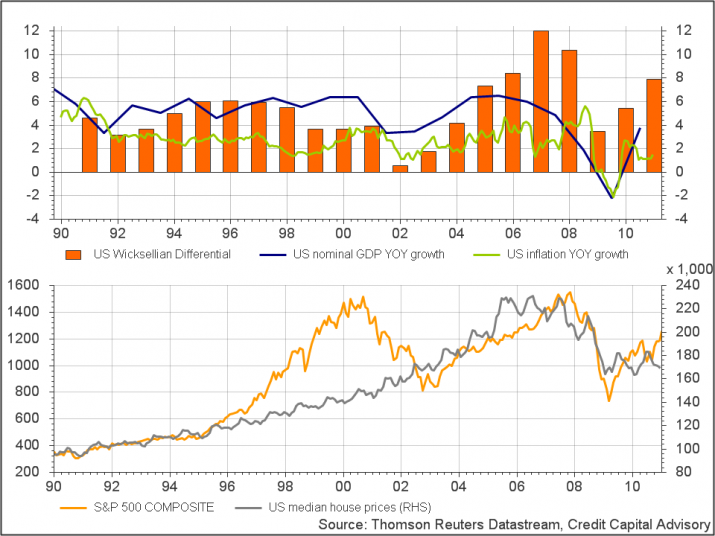

Another indication – more scientific than my previous observation – that the money rate may well be below the natural rate, has been devised by a former colleague of mine. Thomas Aubrey published a very interesting book in 2012, Profiting from Monetary Policy, in which he underlines his own calculation of what he calls the ‘Wicksellian differential’ (the difference between the natural and the money rates of interest). He uses estimates of the return on capital and the cost of capital in order to calculate the differential (according to neoclassical economic theory, the real interest rate should equal the marginal product of capital in equilibrium conditions – not everybody agrees though). Using those assumptions, it does look like we have been in a new credit boom since 2010 as you can see from the charts here:

Where does this lead us? Every unsustainable boom has to end at some point. It is likely that as soon as nominal interest rates start rising above a certain level, mark to market losses and worse, outright defaults, will force investors to mark down their holdings of malinvestments. We’ve already recently seen the impact on emerging markets of a mere talk of reducing the pace of quantitative easing.

What could be the consequences? Banks don’t place their liquidity in such risky assets, but might well be exposed to clients that do (many banks provide so-called leveraged loans for instance). Such impact on banks should be relatively limited though, given current regulatory constraints and deleveraging. In turn, this should limit the damage to credit creation and reduce the risk of another monetary contraction through the money multiplier. However, and it is a big question mark, banks might be exposed to companies (and households) under life support from low interest rates. This is more likely to be the case in some countries than others (I’ll let you guess which ones). When rates rise, loan impairment charges may rise quite a lot in those countries.

Private losses (through various types of investment funds and not subject to the money multiplier) may well be large though, negatively affecting private investments for some time afterwards. If you were thinking that the economy was naturally recovering at the moment, you might give it a second thought… Investors, beware, timing will be crucial.

First chart: Wall Street Journal; Second chart: Credit Capital Advisory

Ludwig von Mises’ death

Today is the 40th anniversary of Austrian economist Ludwig von Mises’ death.

I can’t emphasize enough how much Mises has been influential on my way of looking at both economic and social interactions. When I compared his writings to my day to day life as a banks analyst, everything made so much sense… I’ve read several of his books, of which Human Action is one of my favourite. I found myself in agreement with 99% of what I read in it. Believe me, this usually never happens.

He was a true believer in freedom, and was mocked during several decades for predicting the fall of the Soviet Union. A great economist.

Thank you Ludwig.

PS: You can read more about Mises on Free Banking and on the Mises Institute website (also here).

{kind=link}

Recent Comments