Some ‘good’ principles of financial regulation

Readers of this blog know the extent of my love for banking regulation. I love regulation. I really do. Otherwise I wouldn’t have much to write about.

Irony aside, I recently read a very good paper by Calomiris (Financial Innovation, Regulation, and Reform, 2009, which you can find here) that made me give regulation a rethink (to be frank, I was disappointed that there’s not much about financial innovation in this paper, but the rest is pretty good).

Calomiris is a free-market guy. He makes it clear is most of his papers, this one included:

The risk-taking mistakes of financial managers were not the result of random mass insanity; rather they reflected a policy environment that strongly encouraged financial managers to underestimate risk in the subprime mortgage market. Risk-taking was driven by government policies; government’s actions were the root problem, not government inaction.

He is right. But he also seems to be a ‘realist’ (if ever this really means anything). He considers that, given our current distortive institutional framework, the best thing we can do is to mitigate its effect through proper regulation. He writes:

If there were no governmental safety nets, no government manipulation of credit markets, no leverage subsidies, and no limitations on the market for corporate control, one could reasonably argue against the need for prudential regulation. Indeed, the history of financial crises shows that in times and places where government interventions were absent, financial crises were relatively rare and not very severe.

[…But] it is not very helpful to suggest only regulatory changes that are very far beyond the feasible bounds of the current political environment. […] Absent the elimination of [all the policies described above], government prudential regulation is a must.

In a way, he has a point. Whereas I’d like to see the implementation of a free banking system, I also have to admit that this possibility is pretty unlikely to ever reoccur (unless a once in a thousand years financial collapse suddenly strikes). Which led me to think about a ‘second best’. This ‘second best’ solution should follow the principles I described here (where I argued in favour of a stable rule set and regulatory framework) and here (where I agreed with Lars Christensen and John Cochrane and argued against macro-prudential regulations). This is what I wrote:

Stable rules are a fundamental feature of intertemporal coordination between savers and borrowers, between investors and entrepreneurs. In order for economic agents to (more or less) accurately plan for the future, for entrepreneurs to develop their business ideas and anticipate future demand, for savers to invest their money and know that their property rights are not going to disappear overnight and accordingly plan their own delayed consumption and provide entrepreneurs with directly available funds, the economic system needs a stable and predictable rule framework. Production and investments take time and as a result involve uncertainty, which should not be exacerbated by an instable rule set. The rule of law is part of this framework. Monetary policy, financial regulation and government policies should follow the same pattern, instead of being discretionary.

What I am about to describe is a non-exhaustive list of ‘good’ principles of regulation that fit (to an extent) a free-market framework. I may update the list over time. Following the principles above, and even though not perfect, a ‘second best’ solution would have to be:

- As least distortive as possible (i.e. introducing as few loopholes and incentives to game the rules as possible)

- As stable as possible (i.e. no discretionary powers), and

- As simple, transparent and clear as possible (i.e. a few clear and straightforward rules are better than a multitude of obscure and complex ones)

On the monetary policy side, despite its flaws, NGDP targeting seems to be the only ‘easily implementable’ policy that meets the three criteria. I won’t discuss it here (see The Money Illusion, The Market Monetarist, Worthwhile Canadian Initiative, and many other blogs for more information). On the slightly ‘less easily implementable’ side, the ‘productivity norm’ would nonetheless be an even better alternative (see George Selgin’s implementation here, from page 64 onwards).

What about financial and banking regulation? In order to respect the three fundamental rules described above, regulators should:

- Define few transparent, straightforward limits and ratios based on objective and easily measurable criteria that are neither pro- nor counter-cyclical

- Not impose their own perception of risk to the market

- Not vary regulatory limits and requirements over time

- Not publicly shame financial institutions that respect regulatory requirements even if borderline-compliant: the regulators’ role is to make sure that institutions respect the requirements, period

- Publicly make clear that regulations only represent minimums, that regulators are only here to make those minimums respected, and that it is the role of market actors to identify stronger from weaker institutions within those regulatory-defined limits

- Not interfere with financial institutions’ strategy and internal organisational structures: harmonising business models takes the risk of weakening the whole system

- Refrain from making any comment unrelated to the (non)compliance of institutions to regulatory requirements

- Allow the market process to run its course and not institutionalise moral hazard by implementing bailout and other backstop mechanisms

Banking regulation is divided into micro-prudential and macro-prudential regulation. The former provides individual banks with rules they have to respect at all times, independently of the performance of the whole economy. The latter provides all banks with rules that vary according to the state of the economy, independently of the performance of each bank. Following the principles above, fixed and straightforward sets of micro-prudential regulations may be acceptable. On the other hand, most macro-prudential regulations would be eliminated given their discretionary component and their variability over time. It is indeed very hard for regulators to identify bubbles and other excesses (see White, 2011, here). They have a poor track record at it. Discretion could well prevent a bubble from growing too much but it could also prevent a genuinely growing market to reach its full potential. Regulators suffer from the central planner’s problem. As Hayek said in his essay The Use of Knowledge in Society:

The peculiar character of the problem of a rational economic order is determined precisely by the fact that the knowledge of the circumstances of which we must make use never exists in concentrated or integrated form, but solely as the dispersed bits of incomplete and frequently contradictory knowledge which all the separate individuals possess.

I can already hear the rebuttals: “but counter-cyclical macro-prudential policies would help mitigate the bust after the boom!” To which I would respond: “how do you identify a ‘boom’?” For a bust to occur, a boom must be unsustainable. Solid and sustainable growth may well happen and should not be interfered with by counter-cyclical regulations that would in fact not be counter-cyclical at all in this case. Nominal stability is primarily the role of monetary policy, which should promote a stable framework to the real economy. An unsustainable boom is likely to emanate from nominal instability. The goal of regulation is not to mitigate the effects of destabilising monetary policies.

Of course, this does not mean that one should not strive to reduce political and regulatory distortions. ‘Idealists’ (if ever this also means anything) are a necessary part of a healthy democratic process. Moreover, too much compromise can be dangerous: where to fix the limit? Because the very distortive sources are still present, crises can still occur and provide extra arguments to further expand the regulatory burden.

PS: I’ll provide examples of regulations that comply or not with those principles in a subsequent post. This post would have been too long otherwise!

A clarification on mortgage rates for ASI’s Ben Southwood

Ben Southwood from the Adam Smith Institute replied to my previous post here. I am still confused about Ben’s claim that the spread varied “widely”. As the following chart demonstrates, the margins of SVR, tracker and total floating lending over the BoE base rate remained remarkably stable between 1998 and 2008, despite the BoE rate varying from a high 7.5% in 1998 to a low of 3.5% in 2003:

Everything changed in 2009 when the BoE rate collapsed to the zero lower bound. Following his comments, I think I need to address a couple of things. Two particular points attracted my attention. Ben said:

If other Bank schemes, like Funding for Lending or quantitative easing were overwhelming the market then we’d expect the spread to be lower than usual, not much higher.

His second big point, that the spread between the Bank Rate and the rates banks charged on markets couldn’t narrow any further 2009 onwards perplexes me. On the one hand, it is effectively an illustration of my general principle that markets set rates—rates are being determined by banks’ considerations about their bottom line, not Bank Rate moves. On the other hand, it seems internally inconsistent. If banks make money (i.e. the money they need to cover the fixed costs Julien mentions) on the spread between Bank Rate and mortgage rates (i.e. if Bank Rate is important in determining rates, rather than market moves) then the absolute levels of the numbers is irrelevant. It’s the spread that counts.

It looks to me that we are both misunderstanding each other here. It is indeed the spread that counts. But the spread over funding (deposit) cost, not BoE rate! (Which seems to me to be consistent with my posts on MMT/endogenous money.) Let me clarify my argument with a simple model.

Assumptions:

- A medium-size bank’s only assets are floating rate mortgages (loan book of GBP1bn). Its only source of revenues is interest income. The bank maintains a fixed margin of 1% above the BoE rate but keeps the right to change it if need be.

- The bank’s funding structure is composed only of demand deposits, for which the bank does not pay any interest. As a result, the bank has no interest expense.

- The bank has a 100% loan/deposit ratio (i.e. the bank has ‘lent out’ the whole of its deposit base and therefore does not hold any liquid reserve).

- The bank has an operational cost base of GBP20m that is inflexible in the short-term (not in the long-term though there are upwards and downwards limits) and no loan impairment charge.

Of course this situation is unrealistic. A 100% loan/deposit bank would necessarily have some sort of wholesale funding as it needs to maintain some liquidity. It would also very likely have a more expensive saving deposit base and some loan impairment charges. But the mechanism remains the same therefore those details don’t matter.

In order to remain profitable, the bank’s interest income has to be superior to its cost base. Moreover, the bank’s interest income is a direct, linear function, of the BoE rate. The higher the rate, the higher the income and the higher the profitability. As a result, the bank’s profitability obeys the following equation:

Net Profit = Interest Income – Costs = f(BoE rate) – Costs,

with f(BoE rate) = BoE rate + margin = BoE rate + 1%.

Consequently, in order for Net Profit > 0, we need f(BoE rate) > Costs.

Now, we know that the bank’s cost base is GBP20m. The bank must hence earn more than GBP20m on its loan book to remain profitable (which does not mean that it is enough to cover its cost of capital).

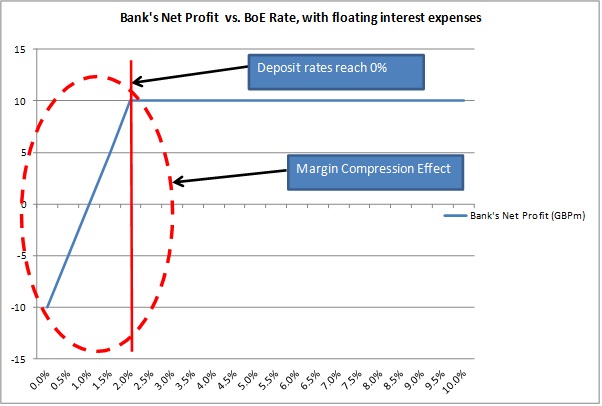

The BoE rate is 2%, making the rate on the mortgage book of the bank 3%, leading to a GBP30m income and a GBP10m net profit. Almost overnight, the BoE lowers its rate to 0.5%. The bank’s loan book’s average rate is now 1.5%, and generates GBP15m of income. The bank is now making a GBP5m loss. Having inflexible short-term costs, it’s only way of getting back to profitability is to increase its margin by at least 0.5%. The bank’s net profit profile is summarised by the following chart:

However, a more realistic bank would pay interest on its deposit base (its funding). Let’s now modify our assumptions and make that same bank entirely demand deposit-funded, remunerated at a variable rate. The bank pays BoE rate minus a fixed 2% margin on its deposit base. As a result, what needs to cover the banks operational costs isn’t interest income but net interest income. The bank’s net profit equation is now altered in the following way:

Net Profit = Net Interest Income – Costs

Net Profit = Interest Income – Interest Expense – Costs

Net Profit = f1(BoE rate) – f2(BoE rate) – Costs

with f1(BoE rate) = BoE rate + margin = BoE rate + 1%,

and f2(BoE rate) = BoE rate – margin = BoE rate – 2%.

The equation can be reduced to: Net Profit = 3% (of its loan book) – Costs, as long as BoE rate >= 2% (see below).

Let’s illustrate the net profit profile of the bank with the below chart:

What happens is clear. Independently of its effects on the demand for credit and loan defaults, the BoE rate level has no effect on the bank’s profitability. Everything changes when deposit rates reach the zero lower bound (i.e. there is no negative nominal rate on deposits), which occurs before the BoE rate reaches it. From this point on, the bank’s interest income decreases despite its funding cost unable to go any lower. This is the margin compression effect that I described in my first post. In reality, things obviously aren’t that linear but follow the same pattern nevertheless.

Realistic banks are also funded with saving deposits and senior and subordinated debt, on which interest expenses are higher. This is when schemes such as the Funding for Lending Scheme kicks in, by providing cheaper-than-market funding for banks, in order to reduce the margin compression effect. The other way to do it is to reflect a rate rise in borrowers’ cost, while not increasing deposit rates. This is highly likely to happen, although I guess that banks would only partially transfer a rate hike in order not to scare off customers.

Overall, we could say that markets determine mortgage rates to an extent. But this is only due to the fact that banks have natural (short-term) limits under which they cannot go. It would make no sense for banks not to earn a single penny on their loan book (and they would go bust anyway). Beyond those limits, the BoE still determines mortgage rates.

Although I am going to qualify this assertion: the BoE roughly determines the rate and markets determine the margin. At a disaggregated level, banks still compete for funding and lending. They determine the margins above and below the BoE rate in order to maximise profitability. They, for instance, also have to take into account the fact that an increase in the BoE rate might reduce the demand for credit, thereby not reflecting the whole increase/decrease to customers as long as it still boosts their profitability. Those are some of the non-linear factors I mentioned above. But they remain relatively marginal and the aggregate, competitively-determined, near-equilibrium margin remains pretty stable over time as demonstrated with the first chart above.

With this post I hope to have clarified the mechanism I relied on in my previous post, but feel free to send me any question you may have!

Mortgage rates are still determined by the BoE

Ben Southwood from the Adam Smith Institute wrote an interesting piece this week. I have an objection to his title and the conclusion he reached. Ben wrote:

However, it was recently pointed out to me that since a high fraction of UK mortgages track the Bank of England’s base rate, a jump in rates, something we’d expect as soon as UK economic growth is back on track, could make mortgages much less affordable, clamping down on the demand for housing.

This didn’t chime with my instincts—it would be extremely costly for lenders to vary mortgage rates with Bank Rate so exactly while giving few benefits to consumers—so I set out to check the Bank of England’s data to see if it was in fact the case. What I found was illuminating: despite the prevalence of tracker mortgages the spread between the average rate on both new and existing mortgage loans and Bank Rate varies drastically.

Wait. I really don’t reach the same conclusion from the same dataset. This is what I extracted from the BoE website (using the BoE’s old reporting format, as the new one only started in 2011):

Banks and building societies offer two main types of floating rate mortgages: standard variable rate (SVR) and trackers. Trackers usually follow the BoE rate closely. SVR are slightly different: margins above the BoE rate are more flexible. Banks vary them to manage their revenues but usually fix them for an extended period of time before reviewing them again. During the crisis, some banks that had vowed to maintain their SVR at a certain spread angered their customers when this situation became unsustainable due to low base rates. Some banks and building societies made losses on their SVR portfolio as a result and had to break their promise and increase their SVR.

What we can notice from the chart above is clear: since the mid-1990s, it is the BoE that determine both mortgage and deposit rates. Not the market. All rates moved in tandem with the BoE base rate. Still, the linkage was broken when the BoE rate collapsed to the zero lower bound in 2009. And this is probably why Ben declared that

but what is clear is that tracker mortgages be damned, interest rates are set in the marketplace.

I think this is widely exaggerated. Ben missed something crucial here: banks have fixed operational costs. Banks generate income by earning a margin between their interest income (from loans) and interest expense (from deposits and other sources of funding). They usually pay demand deposits below the BoE rate and saving/time deposits at around the BoE rate, and make money by lending at higher rates. From this net interest income, banks have to deduce their fixed costs (salaries and other administrative expenses) and bad debt provisions.

There is a problem though. Setting the BoE rate near zero involves margin compression. Banks’ back books (lending made over the previous years) on variable rates see their interest income collapse. Banks’ deposit base is stickier: many saving accounts are not on variable rates. Therefore, there is a time lag before the deposit base reprice (we can see this on the chart above: whereas lending reprices instantaneously when the BoE rate moves, deposits show a lag). Moreover, near the zero bound, the spread between demand deposit rates and the BoE rates all but disappears. The two following charts clearly illustrate this margin compression phenomenon:

It is clear that banks started to make losses when the BoE rate fell, as the margin on the floating rate back book (stock) became negative. Using the new BoE reporting would make those margins look even worse*. To offset those losses, banks started to increase the spread on new lending, leading to a spike on the interest margin of the front book (green line above). Banks can potentially reprice their whole loan book at a higher margin, but this takes time, especially with 15 to 30-year mortgages. Consequently, banks not only increased the spread on new lending, but also decided to break their SVR promises and increase their back book SVR rates (see black line in charts). This usually did not go down well with their customers, but some banks had no choice, having entered the crisis with too low SVRs.

What happens to a bank whose net interest income is negative (assuming it has no other income source)? It reports net accounting losses as it still has fixed operational expenses… Continuously depressed margins explain why banks’ RoE remains low. For banks to report net profits, their net interest income must cover (at least) both operational expenses and loan impairment charges. What Ben identified as ‘market-defined interest rates’ or the ‘spread over BoE’s rate’ from 2009 onwards is simply the floor representing banks’ operational costs, under which banks cannot go… The only other (and faster) way to rebuild banks’ bottom line would be to increase the BoE rate.

A mystery though: why didn’t banks decrease their time deposit rates further? I am unsure to have an answer to that question. A possibility is that the spread between demand and time deposits remained the same. Another possibility is that banks’ time deposit rates remained historically roughly in line with UK gilts rates. Decreasing time deposit rates much below those of gilts would provide savers with incentives to invest their money in gilts rather than in banks’ saving accounts.

What would a rate hike mean? Ben thinks it would have little impact, probably because the spread over BoE seems to show quite a lot of breathing space before the base rate impacts lending rates. I don’t think this is the case. A rate increase would likely push lending rates upwards on bank’s back book (i.e. banks are not going to reduce the spread in order to maintain stable mortgage rates). Why? Banks’ net interest margin and return on equity are still very depressed. Moreover, new Basel III regulations are forcing banks to hold more equity, further reducing RoE. Consequently, banks will seek to rebuild their margin and profitability, making customers pay higher rates to compensate for years of low rates and newly-introduced regulatory measures.

* I am unsure why the BoE changed its reporting and what the differences are, but reported lending rates are much lower than with the old reporting standards. Tracker mortgage rates even seem to be lower than time deposit rates. See below and compare with my first chart. If anybody has an explanation, please enlighten me:

Update: I replaced ‘ceiling’ with ‘floor’ in the post as it makes a lot more sense!

Update 2: Ben Southwood replies here…

Update 3: …and I replied there!

Bundesbank’s Dombret has strange free market principles

Andreas Dombret, member of the executive board of the Bundesbank, made two very similar speeches last week (The State as a Banker? and Striving to achieve stability – regulations and markets in the light of the crisis). When I started to read them, I was delighted. Take a look:

If one were to ask the question whether or not the market economy merits our trust, another question has to be added immediately: “Does the state merit our trust?”

[…]

Sometimes it seems as if we are witnessing a transformation of values and a redefinition of fundamental concepts. The close connection between risk-taking and liability, which is an important element of a market economy, has weakened.

Conservative and risk-averse business models have become somewhat old-fashioned. If the state is bearing a significant part of the losses in the case of a default of a bank, banks are encouraged to take on more risks.

[…]

[High bonuses and short-termism] are the result of violated market principles and blurred lines between the state and the banks. They are not the result of a well-designed market economy but rather indicative of deformed economies. However, the market economy stands accused of these faults.

Brilliant. I was just about to become a Dombret fan when…I read the rest:

In my view, the solution is to be found in returning the state to its role of providing a framework in which the private sector can operate. This means a return to the role the founding fathers of the social market economy had in mind.

They knew that good banking regulation is a key element of a well-designed framework for a well-functioning banking industry and a proper market economy in general.

[…]

This is where good bank capitalisation comes into play. It is the other side of the coin. Good regulation should directly address the key problem. If the system is too fragile, an important and direct measure to reduce fragility is to have enough capital.

[…]

Good capitalisation will have the positive side effect of reducing many of the wrong incentives and distortions created by taxpayers’ implicit guarantees and therefore making the bail-in threat more credible ex ante.

And from the second article:

In view of all this, I believe that two elements will be especially important in making banks more stable: capital and liquidity. Deficits in both of these things were factors which contributed significantly to the financial crisis. The state can bring in regulation to address these deficits, and has done so very successfully.

And on shadow banking:

In terms of financial stability, the crux of the matter is that these entities can cause similar risks to banks but are not subject to bank regulation.And the shadow banking system can certainly generate systemic risks which pose a threat to the entire financial system.

Much the same applies to insurance companies. Although they aren’t a direct component of the shadow banking system, they can also be a source of systemic risk. All of this makes it appropriate to extend the reach of regulation.

Sorry but I will postpone joining the fan club…

Mr. Dombret correctly identifies the issue with the financial system: too much state involvement. What is his solution? More state involvement. It is hard to believe that one person could come up with the exact same solution that had not worked in the past. Were the banks not already subject to capital requirements before the crisis? Even if not ‘high’ enough they were still higher than no capital requirement at all. So in theory they should have at least mitigated the crisis. But the crisis was the worst one since 1929, and much worse than previous ones during which there were no capital requirements. Efficient regulation indeed…

Like 95% of regulators, he makes such mistakes because of his (voluntary?) ignorance of banking history. A quick look at a few books or papers such as this one, comparing US and Canadian banking systems historically, would have shown him that Canadian banks were more leveraged than US banks on average since the early 19th century, yet experienced a lot fewer bank failures. There is clearly so much more at play than capital buffers in banking crises…

Moreover, he views formerly ‘low’ capital requirements as a justification for bankers to take on more risks to generate high return on equity. This doesn’t make sense. For one thing, the higher the capital requirements the higher the risks that need to be taken on to generate the same RoE. It also encourages gaming the rules. This is what is currently happening, as banks are magically managing to reduce their risk-weighted assets so that their regulatory-defined capital ratios look healthier without having to increase their capital.

Mr. Dombret starts by seriously questioning the state’s ability to manage the system and highlights the very harmful and distortive effects of state regulation to eventually… back further and deeper state regulation.

A question Mr. Dombret: what are we going to do following the next crisis? Continue down the same road?

Can please someone remind Mr. Dombret of what a free market economy, which he seems to cherish, means?

Picture: Marius Becker

Banks’ branches/IT problems, and bank regulation vs. freedom

Barclays this week unsurprisingly announced the closure of a quarter of its 1600 branches. A ‘person familiar with the plans of Barclays’ said:

This is a fundamental 100-year transformation of the banking industry, that’s what I think we are seeing.

He/she is right. Though this has been obvious to banking innovators for a while already. SNL expands on that here and mentions high cost/income in retail banking. An analyst:

No bank in Europe can avoid the online banking issue. It is the future of the bank business.

As I have already said, it questions the plans of some of British politicians to cap the market share of large banks. How could their plan work when banks are already slashing branches by the thousands and when new and growing banks are increasingly established online or within other types of stores (see Tesco Bank, which has no actual branch but ‘in-store branches’ within its Tesco supermarkets). Politicians are able to foresee trends and innovation you said? How can one trust people who can only offer yesterday’s solutions to tomorrow’s problems? Same question about general banking regulation…

Anyway, banks also have some serious work to do. Many of them have antiquated IT systems, which makes us think that a transition to an IT-heavy (or perhaps IT-only…) banking business model won’t be smooth… UK banks have experienced a number of IT problems over the past few months (payment systems down mainly) as a result of their underinvestment in basic IT and the accumulation of various systems on top of one another following acquisitions, without never having really tried to integrate them all.

I personally check my accounts a lot more often now that I have access to smartphone apps, and I am certainly not the only one to do so. With the growth of mobile and contactless payments and the reduction in the number of hard cash transactions, the pressure on banks’ IT systems will become enormous. Increased mobile transaction volumes will also impact mobile telecom networks, though they often more rapidly update their systems than banks. What’s going to be interesting is that banks will increasingly rely on the infrastructure of private mobile and internet telcos. This emergent symbiosis may well accelerate the development of mobile networks, in terms of speed, security and coverage.

And banks better be in a hurry. As they now have payment systems competitors such as Paypal or Bitcoin, which ironically would also benefit from the same technological developments. Telcos could potentially also enter the payment space, as Kenya’s Safaricom did with M-Pesa.

Unrelated, a good piece by Sean Ryan on SNL (gated link) called “Bank regulation versus Americans’ freedom”, and reminiscent of one of my previous posts. This is Sean:

The power to regulate banks is impeding the ability of law-abiding citizens to exercise their rights. Washington is full of people with very strong ideas about how the rest of us should live, and I fear that increasingly intrusive bank regulation has given them an opening to do something about it.

[…]

Given the rapid proliferation of nominally legal activities being exiled from the economic mainstream by bank regulators, it seems only a modest exaggeration, and less modest by the week, to suggest that we are incubating a fourth branch of government. And this one isn’t so hamstrung by those pesky checks and balances.

I couldn’t have said it better myself.

Banks don’t lend out reserves. Or do they?

Over the last weeks/months there has been a lot of agitation in some circles of the financial blogosphere: are banks lending out their reserves? The matter might sound trivial, but it theoretically impacts various monetary policies, such as quantitative easing. I won’t speak about that here. For those of you who don’t know what reserves are, here is a quick reminder:

The money supply comprises several elements. To make things simple the monetary base is the ‘real’ money (remnants of the gold standard and since then, created by the central bank) and the rest of the money supply is some sort of credit money created by the banking system. The ‘real’ money (monetary base) is also what we call high-powered money, and comprises both physical cash and… reserves held by banks at their respective central banks. Credit money created by banks is actually a claim on high-powered money, or high-powered money substitute. Reserves are convertible into physical cash and vice versa. In the UK, the monetary base represents about 17% of M4 (a measure of the money supply that does not include reserves). Reserves represent 82% of the monetary base.

Frances Coppola keeps reiterating again, and again, and again, and sometimes again, that banks don’t lend out reserves. She wrote her latest piece on the topic last week on the Forbes website. The title couldn’t be clearer: “Banks Don’t Lend Out Reserves”

A simple question that could come to anyone’s mind is: what do banks lend out then?

To be honest, I think that a large part of the misunderstanding comes from semantics. I actually agree with Frances on a number of points she makes. I have some objections to her ‘extreme’ view, or at least ‘extreme semantics’. Things aren’t that clear-cut.

While the endogenous money view suffers in my opinion from fallacy of composition, it looked to me at first that the view that banks don’t lend out their reserves suffered from the converse fallacy, the fallacy of division. But it doesn’t look like Frances falls in that trap, given what she made clear in the comment section of her article.

To be clear, banks do need reserves. If a (single) bank makes a loan to a customer, the bank is going to increase both its assets and its deposits (liabilities) by the amount of the loan. So far it does seem that the bank has created money out of thin air. But what happens if the customer withdraws the money from the bank? Deposits will get back to their previous amount, creating a discrepancy with the total loan figure. At the same time, there will be a drain on the bank’s reserves equal to the amount of the loan, as reserves will have been converted into physical cash (while total high-powered money remained the same). Seen this way, we could probably say that banks do lend out reserves.

What happens if the customer doesn’t withdraw the money but pays with it for a good by bank transfer? The drain on reserves still occurs as the beneficiary bank knocks on the door of the borrower’s bank to get hold of the money. In this case again, we could probably say that banks do lend out reserves.

The borrower’s bank also sees its deposits decrease while, on the other hand, the beneficiary bank experiences a deposit and reserves inflow. As a result, its deposit base grows without lending beforehand. Its now increased reserves will allow it to invest or lend more. This clearly nuances Frances’ claim that

when a bank creates a new loan, it also creates a new balancing deposit. It creates this “from thin air”, not from existing money: banks do not “lend out” existing deposits, as is commonly thought.

As we can see, reserves are used for two things: cash withdrawals and interbank settlements.

Let’s now consider the banking system as a whole in a closed economy. If lending leads to cash withdrawals, we could say again that banks lend out their reserves. However, let’s consider the following case: nobody ever withdraws cash. In this situation, all payments are made by electronic bank transfer. While individual banks experience fluctuations in their reserves, the total amount of reserves in the system never changes. Here, we could say that, indeed, banks don’t lend out reserves.

Here is what I meant by fallacy of division: what is true of the system as a whole isn’t for individual banks.

But so far, apart from semantic issues, I think that Frances and I agree although I wish she were more precise in differentiating single banks from the banking system as a whole. However, what I (kind of) disagree with is about her treatment of reserves as a source (or not) of lending and deposit creation. Frances says:

The volume of excess reserves in the system is what it is, and banks cannot reduce it by lending. […]

The volume of excess reserves in the system is what it is, and banks cannot reduce it by lending. They could reduce excess reserves by converting them to physical cash, but that would simply exchange one safe asset (reserves) for another (cash). It would make no difference whatsoever to their ability to lend. Only the Fed can reduce the amount of base money (cash + reserves) in circulation. While it continues to buy assets from private sector investors, excess reserves will continue to increase and the gap between loans and deposits will continue to widen.

This is something I cannot agree with. She is right to say that reserves will permanently be higher than before they were created (at least until the central bank tries to destroy them one way or another). But she overlooks the multiplier effect on lending and deposit expansion.

Assuming no reserve requirements, a fractional reserve bank will estimate how much high-powered money it needs to retain in order to face withdrawals and settlements. It is well-documented that banks in free banking systems naturally maintained reserves. Let’s assume that a whole banking system estimated that it needed to maintain 10% of the amount of its deposits as reserves to face settlements and withdrawals without endangering its existence. This would de facto become an internally-defined reserve requirement. The system can now create a maximum amount of demand deposits (claims on high-powered money) equal to 1/RR = 1/0.10 = 10 times the amount of reserves in its vaults*.

Now let’s get back to the situation described in Frances’ article. Reserves have been created, but have not been ‘lent out’ apparently. Of course, as Frances said, those reserves will not leave the system, unless they are withdrawn. But, they theoretically do provide banks with the ability to create extra deposits ‘out of thin air’ (the pyramiding process), allowing them to maintain their pre-crisis reserves to deposits ratio. And, as deposits expand, the reserves would not disappear but would simply not be considered ‘in excess’ anymore…

The question becomes: why didn’t banks expand their loans and deposit base in line with the increase in reserves? According to the chart below, the M2 multiplier (obtained by dividing all demand and saving deposits by the monetary base), declined significantly when the Fed started its quantitative easing policies.

I don’t think anybody has a clear answer to this. Low demand for loans, the Fed now paying interests on excess reserves, maintenance of precautionary excess reserves to face a possible future liquidity squeeze as long as the crisis isn’t completely over, are some of the possible underlying reasons. From my experience, the third reason is highly likely. I’ve heard many banking executives over the past few years who made clear that they were temporarily hoarding extra cash and reserves not to lend but… “just in case”.

* This multiplier is obviously a very simple one. Chester A. Phillips, in its famous 1921 book Bank Credit, identified the maximum amount x that can be lent out as:

, with c being the amount of reserves deposited, r the reserve/deposit ratio and k the derivative deposit/loan ratio (derivative deposits being the amount of newly-created deposits by lending that are not withdrawn or transferred by the depositors).

, with c being the amount of reserves deposited, r the reserve/deposit ratio and k the derivative deposit/loan ratio (derivative deposits being the amount of newly-created deposits by lending that are not withdrawn or transferred by the depositors).

In 1984, Alex Mcleod also wrote a brilliant, but barely readable, book called Principles of Financial Intermediation. He covers pretty much all possible and theoretical cases involving credit expansion based on the public’s acceptance ratio for claims (notes and deposits) on ‘money proper’, reserve to deposit ratio of financial intermediaries, external drain in case of an open economy, simple, cross and compound pyramiding (when the claims on money of one or several institutions can be used as reserves by other institutions)… There is no way I can reproduce his massive equations here…

Moreover, things get even more complex when you add in secondary reserves (very liquid low-yielding financial instruments almost instantly convertible into cash), as well as technology and financial innovations that allow banks to economise on reserves.

We are now in a micromanaged economy

Interesting piece from Matt Levine on Bloomberg on Wednesday. It highlights how far regulators are now going to micromanage the financial system. They now prevent banks from lending to private equity firms (so-called ‘leveraged loans’), distorting lending mechanisms, market pricing and economic agents’ learning process. The whole scheme is subject to potential arbitrage and could possibly lead to even more devastating opaque financial engineering.

Some of my friends (senior bankers working in financial institutions mergers and acquisitions at other banks) recently told me that regulators prevent their clients (banks) from trying to acquire any other banks. Nonetheless, during the crisis, regulators almost forced, or at the very least engineered, banks mergers…Does anybody still believe we are in a free market?

This is a regulator:

The impact on private equity, a significant driver of what we see as risky practices, is an intended consequence of our actions,” Martin Pfinsgraff, the OCC’s senior deputy comptroller for large-bank supervision, said in an interview. “As regulators, we certainly hope to change bad practices and remove the extraordinary froth that’s experienced at the peak of a credit cycle. If we can mitigate that, it reduces the size of the valley to follow.

A suggestion to this person: why don’t you become a banker? It looks like you know better than bankers how to safely pick counterparties to lend to. Moreover, what he does not realise is that by restraining the flow of credit somewhere, it’s going to reappear somewhere else, shifting systemic risk to another (and possibly darker) corner of the economy.

Forcing banks: to add a bit of capital there and there and some liquidity here, to consider which assets are safe and liquid and which aren’t, to trade some products through specific counterparties, not to acquire competitors, to force the acquisition of competitors, and so on, was not enough. Regulators have now introduced another new tool and earned another power. Moreover, in their quest to make the banking system ‘safer’, regulators are likely to make it more vulnerable: banks will become less differentiated, holding the same types of assets, lending to the same types of clients, having the same types of internal models and engaged in the same types of trading activities. I let you guess what happens when those regulatory-favoured activities collapse.

Exactly 70 years after Hayek’s The Road to Serfdom was published, it looks like we’re back to the same point.

Photo: HR People

A UK housing bubble? Sam Bowman doubts it

On the Adam Smith Institute’s blog, Sam Bowman had a couple of posts (here and a follow-up here, and mentioned by Lars Christensen here) attempting to explain that there might not have been any house price bubble in the UK. He essentially says that there was no oversupply of housing in the 1990s and 2000s. Here’s Sam:

These charts show that housing construction was actually well below historical levels in the 1990s and 2000s, both in absolute terms and relative to population. It is difficult to see how someone could claim that the 2008 bust was caused by too many resources flowing toward housing and subsequently needing time to reallocate if there was no bubble in housing to begin with.

What this suggests is that the Austrian story about the crisis may be wrong in the UK (and, if Nunes’s graphs are right, the US as well). The Hayek-Mises story of boom and bust is not just about rises in the price of housing: it is about malinvestments, or distortions to the structure of production, that come about when relative prices are distorted by credit expansion.

Well, I think this is not that simple. Let me explain.

First, the Hayek/Mises theory does not apply directly to housing. In the UK, there are tons of reasons, both physical and legal, why housing supply is restricted. As a result, increased demand does not automatically translate into increased supply, unlike in Spain, which seems to have lower restrictions as shown by the housing start chart below:

Second, Sam overlooks what happened to commercial real estate. There was indeed a CRE boom in the UK and CRE was the main cause of losses for many banks during the crisis (unlike residential property, whose losses remained relatively limited).

Third, the UK is also characterised by a lot of foreign buyers, who do not live in the UK and hence not included in the population figures. Low rates on mortgages help them purchase properties, pushing up prices, triggering a reinforcing trend while supply in the demanded areas often cannot catch up.

Fourth, the impact of Basel regulations seems to be slightly downplayed. Coincidence or not, the first ‘bubble’ (in the 1980s) appeared right when Basel’s Risk Weighted Assets were introduced. And it is ‘curious’, to say the least, that many countries experienced the same trend at around the same time. Would house lending and house prices have increased that much if those rules had never been implemented? I guess not, as I have explained many times. I have yet to write posts on what happened in several countries. I’ll do it as soon as I find some time.

I recommend you to take a look at my RWA-based Austrian Business Cycle Theory, which seems to show that, while there should indeed be long-term real estate projects started (depending on local constraints of course), there is also an indirect distortion of the capital structure of the non-real estate sector.

While there may well be ‘real’ factors pushing up real estate prices in the UK, there also seems to be regulatory and monetary policy factors exacerbating the rise.

- Chart 1: Spanish Property Insight

- Chart 2: FT Alphaville

- Chart 3: Guardian

Mises’ Theory of Money and Credit, Funding Valuation Adjustment and other stuff

Quick post today. A few interesting Austrian economics links first.

Liberty Fund is hosting an interesting debate on Ludwig von Mises’ Theory of Money and Credit. I read that book in 2012, a 100 years after it was released and for its 101 years, Lawrence White is writing an interesting review of what he thinks was original and/or revolutionary in this work. Liberty Fund also asked a few other economists to comment on White’s article and on Mises’ book: Jörg Guido Hülsmann, Jeffrey Rogers Hummel, and George Selgin. They reply to each other so the debate is constantly evolving, which is cool.

The Bastiat blog of the Mises Institute advertised the Austrians in Finance LinkedIn group. Good opportunity to network with fellow Austrians working in financial services. I actually didn’t know that group before, so I just joined!

Bob Murphy had a funny post a few days ago about… the von Mises yield curve! Sounds financial, which would be logical given Mises’ work, but it is actually about material physics… And the theory’s author wasn’t Ludwig von Mises but Richard von Mises. They were contemporaries and the theory was formulated in 1913, just one year after The Theory of Money and Credit was published!

Finally, nothing to do with Mises or Austrian economics, but here is an interesting link for the (possibly very) few of you who analyse banks and would be interested in finding out more about Funding Value Adjustment (FVA). FVA is the new fashionable accounting tool used by some investments bank to help value their derivatives portfolio. JP Morgan reported a… USD1.5bn loss after implementing FVA last week, making people wonder where all those new acronyms came from and how they could lead to such losses out of nowhere. Deutsche Bank also reported a EUR623m charge related to FVA, as well as DVA and CVA (debt and credit valuation adjustments, now ‘famous’, unlike their ‘new’ little brother).

Diagram: Wikipedia

The bank branch is dying. Some politicians don’t seem to get it

Technology is both a curse and a blessing for banks. It usually starts as a curse and ends up being a blessing (at least for the banks that eventually managed to master technological disruptions). I’ve personally argued several times during BarcampBank debates that the branch was outdated. The rebuttal I usually got (especially from French financial actors and entrepreneurs, probably a cultural thing) is that customers want to ‘feel’ some humanity, and not interact with some faceless system. I don’t disagree, but I would argue that they are massively overestimating the ‘humanity’ factor. What people want is convenience.

‘Humanity’ is just an inefficient way of providing convenient services to customers. When your services and IT systems aren’t convenient and instinctive enough for customers to use easily, they will naturally seek human help and reassurance. Does it mean customers necessarily want ‘access to other humans’ for most of their banking transactions? No. What it does mean it that banks don’t have straightforward enough and easy-to-use systems.

So here I reiterate: branches are outdated. And, once again, it is both a curse and a blessing for banks. For now, it is a curse: the retail banking business of most (large) banks is plagued by an unsustainable cost/income ratio (often around 70%+ when it should be closer to 50). The internet revolution led banks to open websites but not to close branches: branches were still the primary medium through which they could attract depositors (hence funding). Having a branch near potential customers’ home was crucial in order to both obtain funding and revenues. Internet obviously changes everything. But with a lag. Young people quickly get used to utilising internet websites for shopping and banking, but don’t have the financial resources that drive banking revenues. On the other hand, older customers are much slower to keep up with the trend. Some of the very first internet banks, like UK’s Egg, were not as successful as expected as a result.

Now that mainstream internet use has been among us for around 15 years, much more customers use online services, including banking, and former early adopter but resource-poor students are now working professionals. Smartphones have compounded the trend. Brett King has extensively described the possible functions of a branch in the 21st century and documented the various trends in customer preferences in his Bank 2.0 and Bank 3.0 books. Mobile banking is booming and banks are at last starting to react. Over the last year, banks have followed each other in announcing reductions in their branch network, something that would have been unimaginable just a few years ago. In the US, banks are axing branches, the latest in line being Bank of America. In the UK, Barclays referred to branch closures as a ‘necessity’ at the end of last year. RBS and HSBC have also announced branch closures. In the rest of Europe, the trend is the same (see Belgian and French banks for instance). The other part of the curse is that banks do have to heavily invest in IT to catch up with the trend. And I am not even mentioning unions’ rejection of the branch axing plans, which indeed involve jobs cutting.

The blessing part of the story is that, while banks are constrained by increasing compliance costs and fall of revenues due to new regulations, smaller branch networks also means reduced cost bases. Bankers, desperate to improve their single-digit RoE can only welcome the change in the medium-term. More profitable banks also mean more flexible and more robust banks.

But. Some (most?) politicians don’t seem to get it. The UK’s Labour party came up with a brand new ‘brilliant’ idea to end the dominance of the largest retail banks of the country: a cap on the number (market share) of branches. As they are saying:

We are not asking whether existing banks might have to divest themselves of a significant number of branches. We are asking how we make that happen.

Well, you know what guys? It’s already happening. 21st century technological disruption does not require 20th century reasoning. Yet many professional politicians seem to have been blessed with the very skill of thinking using ‘previous century logic’. Politicians, please back away and let technology implement more efficient measures than anything you would have ever been able to plan.

PS: One of my (unrealistic at the moment) proposals was that alternative and independent interbank ‘superbranches’ could appear, gathering services/ATMs from all high-street banks under the same roof. This place would effectively be for banks what UK-based Carphone Warehouse and its competitors are for mobile phone providers. Banks would be a big step closer to being virtual service-providers and customers could potentially switch almost at will, intensifying competition. That would be a revolution.

PPS: Other technological disruptions I didn’t mention in the post were P2P-lending and associated services. This is also a big challenge but requires different responses, although some of the issues are interlinked.

- Chart 1: The Bankwatch, McKinsey

- Chart 2: McKinsey, The Triple Transformation, p. 33

- Chart 3: Mobility Enterprise

Recent Comments