News digest

I have been so busy since last week that I didn’t have much time to write for this blog… And, to tell you the truth, I was almost shocked: barely any news on banks capital, regulation, monetary policy, etc, over the past few days. Sure, the ECB cut its rate by 25bp to 0.25%, but I’m not sure I should comment within the scope of this blog: I am still not convinced by such such a diverse monetary union as the Eurozone and find it hard to believe we can actually set a common interest rate for all country members within the union… Anyway, today I only wish to comment on a few articles published over the last few days.

A very interesting article published on SNL (subscription required) called Everybody wants to rule the world, including bank regulators, in which an analyst argued that “Banks are not only facing over-regulation. They are also emerging as a convenient channel through which regulators can extend their reach far beyond their legal writ.” You probably understand as well as I do how dangerous this is.

I found out yesterday that Bear Stearns liquidators filed a lawsuit against the three credit rating agencies for alleged manipulation of structured products’ ratings. They are basically arguing that, if ratings had been right, Bears Stearns’ hedge funds would not have collapsed. Blaming the rating agencies because…..hedge funds collapsed? We are not talking about simple retail investors here. We are talking about sophisticated investors. Aren’t hedge funds supposed to undertake their own analysis? Are they just blindly investing in various assets? If hedge funds managers and analysts did not believe in rating agencies’ ratings, why did they invest in those assets the first place? Or perhaps they indeed did not believe in those ratings and took on the risk on purpose. In both cases, we cannot blame the agencies for the lack of competence of those highly-remunerated hedge funds employees.

Yesterday, the FT reported that shadow banks had been among the biggest beneficiaries of the Fed’s monetary policies. I’ve already argued that it might well be a sign that real interest rates are too low (i.e. lower than the equilibrium natural rate of interest). As a result, regulators wish to regulate (of course) this segment of the financial system. My guess is that surplus liquidity would then shift to another less-regulated sector or asset class, as it always does.

A few days ago, I read in horror that Germany may start backing the financial transaction tax. A tax of 0.1% of the value of the transaction (as is proposed on cash instruments) would be a massive drain of wealth: just imagine what would happen to a newly set-up EUR100bn mutual fund (ok, no new fund would ever be of that size, but follow me just for the intellectual exercise). The fund has evidently to invest those 100bn on behalf of its clients, meaning they have to buy EUR100bn of assets. Taxing 0.1% off the total value of the transactions would mean…EUR100m to pay in taxes. This is EUR100m that EU states would withdraw from people’s savings and pensions. Bad idea.

In the Wall Street Journal, a Fed insider described how disillusioned he was from the Fed and QE: he ‘apologises’ to Americans (Scott Sumner comments on this) for QE’s bad or lack of effects. While I do not necessarily share everything he said, I also dislike the Fed’s large scale market manipulation.

On Free Banking, George Selgin criticised this Business Insider piece about airlines debasing their reward points. Reminds me of my own response to Matt Klein on the exact same topic a few weeks ago. No guys: those cases do not reflect free banking and private currencies.

Well, that’s all for the catch up.

Banks’ RWAs as a source of malinvestments – Update

Following a couple of comments I received on my RWA-based Austrian business cycle theory (ABCT) post, I’d like to clarify a few points:

- In the original ABCT, one cannot figure out where malinvestments will appear following an increase in the money supply not matched by an increase in the demand for money, apart from the fact that they are likely to be in producer goods industries rather than in consumer goods industries, due to the artificial lengthening of the structure of production. The mechanism involved is the Cantillon effect: the first firms to receive the new money will see their purchasing/investing power increase at the expense of the rest. We cannot really foresee where the new spending/investments will be directed though but what is certain is that the original structure of relative prices between goods in the economy will be modified as a result.

- In the RWA-based theory the Cantillon effect is ‘limited’: new funds are effectively channelled towards a few specific sectors that benefit from regulatory advantages (lower capital requirements for banks). It is thus possible to foresee which sectors could boom first and where some of the malinvestments could emerge. This does not mean that all malinvestments will show up in those sectors. Other related sectors could also boom as a result. And the increasing wealth effects of the people concerned could also reflect on unrelated sectors…

- Securitisation also makes it a lot more difficult to follow the channelling effect: asset-backed securities were lowly weighted under Basel 2 (under both Standardised and IRB methods) if they obtained a good credit rating. As a result, some corporate lending got a boost from the measure and this would typically replicate the exact process of the original ABCT. Risk-weights were tightened under latest Basel rules though.

- In the RWA-based ABCT, there is no increase in the money supply as assumption. Interest rates are lowered for some sectors (increasing related prices) and raised for others (depressing related prices) as a result of funding rebalancing through banks’ optimisation of capital. Consequences could be less catastrophic than an actual increase in money supply though (although I have no evidence of that). But there is always increase in the money supply at the same time anyway! 🙂

Today in an SNL article (membership required), I found out that the UK government is becoming increasingly frustrated about the lack of SME lending in the country. Hold your breath:

After years of frustration in its attempts to induce banks to extend more credit to small and medium-sized enterprises, the U.K. government has reached the perhaps surprising conclusion that bankers may simply lack the skills they need to lend.

RWAs? Capital requirements guys? No? It must be the skills! To be so clueless is both sad and hilarious.

RWA-based ABCT Series:

- Banks’ risk-weighted assets as a source of malinvestments, booms and busts

- Banks’ RWAs as a source of malinvestments – Update

- Banks’ RWAs as a source of malinvestments – A graphical experiment

- Banks’ RWAs as a source of malinvestments – Some recent empirical evidence

- A new regulatory-driven housing bubble?

A few complementary notes on regime uncertainty

Not much about finance or banking today. I just wanted to come back to a few concepts I mentioned in earlier posts (like here, here and here), such as regulatory regime uncertainty.

We keep hearing economists, journalists and politicians complaining about companies not investing ‘enough’ at the moment. Keynesians like Krugman, de Long and co, and some other non-Keynesian mainstream economists think that the main underlying reason to this phenomenon is lack of demand. I argued several times that, while demand fell probably too low in 2009, one of the other main culprits since then had been regime uncertainty: regulations keep changing and red tape expanding, leading most firms to postpone their various investments and projects until they have a clearer view of the rules going forward.

The Economist’s Buttonwood’s blog had a post about business regulation two days ago, which led me to look for some evidence that increasing (and uncertain) regulation was negatively impacting investments. I found this US Chamber of Commerce Small Business Study, which is enlightening. What it reveals:

- 44% of SME owners ranked economic uncertainty as their number 1 worry (with over-regulation at number 3, or 39%, and high taxes number 4, or 37%). To be fair, economic uncertainty also comprises demand uncertainty. But read the rest first.

- Only 24% indicated that they thought that business climate for SME had improved over the last couple of years.

- 42% of SME owners ranked the US growing deficit and debt as number 2 worry.

- “Seventy-eight percent of small business owners said that the U.S. deficit and debt pose a threat to the success of their businesses. The current federal debt and deficit (40%) and the regulations coming out of Washington (35%) are the top two current issues coming out of Washington that cause concern about the future of their businesses. In addition, sentiment is strong that the climate for small businesses is worse than under the previous administration (80%).”

- “The majority of small business owners, when asked what they need most from Washington right now, would like Washington to get out of the way (84%) as opposed to lending a helping hand (11%). When asked about specific actions they needed from Washington, overwhelmingly small business owners wanted more certainty (87%).”

- “Government regulations on small businesses continue to be seen as unreasonable (73%) by small business owners with a two thirds majority (66%) saying that what Washington will do next to small businesses scares them most.”

Right. It’s kind of a proof, isn’t it? This is also applicable to banks: giving God-like powers to regulators (or anyone) is usually not a good idea. Uncertainty is everywhere in the banking world. Just look at the latest Swiss news: a top official announced that, perhaps, Swiss banks will be subject to a very high 10% leverage ratio. Or perhaps just 6%. Or in between. Or possibly not at all. Or…well, they’re gonna discuss and let you know later. How can any bank plan for the future and lend in such conditions?

On a side not, I am wondering whether or not increasing red tape is linked to The Decline of Creative Destruction, as this Bryan Caplan piece was named today. Surely it is. Very interesting chart anyway (see below). Job destructions during the crisis were actually at the same level as they were throughout the 1990’s… It would be interesting to compare this chart to the evolution of business red tape. Unfortunately, this isn’t my area, so I’ll let you do it!

Banks’ risk-weighted assets as a source of malinvestments, booms and busts

Here I’m going to argue that Basel-defined risk-weighted assets, a key component of banking regulation, may be partly responsible for recent business cycles.

Readers might have already noticed my aversion to risk-weighted assets (RWAs), which I view as abominations for various reasons. They are defined by Basel accords and used in regulatory capital ratios. Basel I (published in 1988 and enforced from 1992) had fixed weights by asset class. For example, corporate loans and mortgages would be weighted respectively 100% and 50%, whereas OECD sovereign debt would be weighted 0%. If a bank had USD100bn of total assets, applying risk-weights could, depending on the lending mix of the bank, lead to total RWAs of anything between USD20bn to USD90bn. Regulators would then take the capital of the bank as defined by Basel (‘Tier 1’ capital, total capital…) and calculate the regulatory capital ratio of the bank: Tier 1 capital/RWAs. Basel regulation required this ratio to be above 4%.

Basel II (published in 2004 and progressively implemented afterwards) introduced some flexibility: the ‘Standardised method’ was similar to Basel I’s fixed weights with more granularity (due to the reliance on external credit ratings), while the various ‘Internal Ratings Based’ methods allowed banks to calculate their own risk-weight based on their internal risk management models (‘certified’ by regulators…).

This system is perverse. Banks are profit-maximising institutions that answer to their shareholders. Shareholders on the other hand have a minimal threshold under which they would not invest in a company: the cost of capital, or required return on capital. As a result, return on equity (ROE) has to at least cover the cost of capital. If it doesn’t, economic losses ensue and investors would have been better off investing in lower yielding but lower risk assets in the first place. But Basel accords basically dictate banks how much capital they need to hold. Therefore banks have an incentive in trying to ‘manage’ capital in order to boost ROE. Under Basel, this means pilling in some particular asset classes.

Let’s make very rough calculations to illustrate the point under a Basel II Standardised approach: a pure commercial bank (i.e. no trading activity) has a choice between lending to SMEs (option 1) or to individuals purchasing homes (option 2). The bank has EUR1bn in Tier 1 capital available and wishes to maximise returns while keeping to the minimum of 4% Tier 1 ratio. We also assume that external funding (deposits, wholesale…) is available and that the marginal increase in interest expense is always lower than the marginal increase in interest income.

- Option 1: Given the 100% risk-weight on SME lending, the bank could lend EUR25bn (25bn x 100% x 4% = 1bn), at an interest rate of 7% (say), equalling EUR1.75bn in interest income.

- Option 2: Mortgage lending, at a 35% risk-weight, allows the same bank to lend a total of EUR71.4bn (71.4bn x 35% x 4% = 1bn) for EUR1bn in capital, at an interest rate of 3% (say), equalling EUR2.14bn in interest income.

The bank is clearly incentivised to invest its funding base in mortgages to maximise returns. In practice, large banks that are under the IRB method can push mortgage risk-weights to as low as barely above 10%, and corporate risk-weights to below 50%. As a result, banks are involuntarily pushed by regulators to game RWAs. The lower RWAs, the lower capital the bank needs, the higher its ROE and the happier the regulators. Banks call this ‘capital optimisation’.

Consequently, does it come as a surprise that low-risk weighted asset classes were exactly the ones experiencing bubbles in pre-crisis years? Oh sorry, you don’t know which asset classes were lowly rated… Here they are: real estate, securitisation, OECD sovereign debt. Yep, that’s right. Regulatory incentives that create crises. And the new Basel III regime does pretty much nothing to change the incentivised economic distortions introduced by its predecessors.

Yesterday, Fitch, the rating agency, published a study of lending and RWAs among Europe’s largest banks (press release is available here, full report here but requires free subscription). And, what a surprise, corporate lending is going…down, while mortgage lending and credit exposures to sovereigns are going…up (see charts below). The trend is even exacerbated as banks are under pressure from regulators to boost regulatory capitalisation and from shareholders to improve ROE. And this study only covers IRB banks. My guess is that the situation is even more extreme for Standardised method banks that cannot lower their RWAs.

The ‘funny’ thing is: not a single regulator or central banker seems to get it. As a result, we keep seeing ill-founded central banks schemes aiming at giving SME lending a boost, like the Funding for Lending Scheme launched by the Bank of England in 2012, which provided banks with cheap funding. Yes, you guessed it: SME lending continued its downward trend and the scheme provided mortgage lending a boost.

Should the situation ‘only’ prevent corporates to borrow funds, bad economic consequences would follow but remain limited. Economic growth would suffer but no particular crisis would ensue. The problem is: Basel and RWAs force a massive misallocation of capital towards a few asset classes, resulting in bubbles and large economic crises when the crash occurs.

The Mises and Hayek Austrian business cycle theory emphasises the distortion in the structure of relative prices that emanates from central banks lowering the nominal interest rate below the natural rate of interest as represented by economic agents’ intertemporal preferences, resulting in monetary disequilibrium (excess supply of money). The consequent increase in money supply flows in the economy through one (or a few) entry points, increasing the demand in those sectors, pushing up their prices and artificially (and unsustainably) increasing their return on investment.

I argue here that due to Basel’s RWAs distortions, central banks could even be excluded from the picture altogether: banks are naturally incentivised to channel funds towards particular sectors at the expense of others. Correspondingly, the supply of loanable funds increases above equilibrium in the favoured sectors (hence lowering the nominal interest rate and bringing about an unsustainable boom) but reduces in the disfavoured ones. There can be no aggregate overinvestment during the process, but bad investments (i.e. malinvestments) are undertaken: the investment mix changes as a result of an incentivised flow of lending, rather than as a result of economic agents’ present and future demand. Eventually, the mismatch between expected demand and actual demand appears, malinvestments are revealed, losses materialise and the economy crashes. Central banks inflation worsen the process through the mechanism described by the Austrians.

I am not sure that regulators had in mind a process to facilitate boom and bust cycles when they designed Basel rules. The result is quite ‘ironic’ though: regulations developed to enhance the stability of the financial sector end up being one of the very sources of its instability.

RWA-based ABCT Series:

- Banks’ risk-weighted assets as a source of malinvestments, booms and busts

- Banks’ RWAs as a source of malinvestments – Update

- Banks’ RWAs as a source of malinvestments – A graphical experiment

- Banks’ RWAs as a source of malinvestments – Some recent empirical evidence

- A new regulatory-driven housing bubble?

The EBA banks’ balance sheets assessment and the standardisation problem

About two weeks ago, the European Banking Authority announced their standard definitions of impaired loans (i.e. non-performing loans) and other asset quality standards, which aim at harmonising the various definitions in place throughout Europe for their upcoming asset quality review. Today, I won’t even be mentioning the odd fact to see a regulator getting in a bank for a few days and basically telling the bank that it knows its loan book better than the bankers themselves. No, today I will only speak about the harmonisation issue.

![]()

Banks have different ways of classifying past-due loans, impaired loans, loans in forbearance and so on, not only in between countries but also within countries. For instance, in the UK, I know some banks that will classify all loans in forbearance as impaired, artificially pushing up their headline bad loans ratio, while others do not, looking better as a result to the untrained eye. Most British banks will automatically classify loans 90 days and more in arrears as impaired, whereas most French banks will only apply the impaired definition when loans are 180 days and more in arrears.

So a standardisation seems to be a good thing as data becomes comparable. Well, it is, and it isn’t. To be fair, standardisation within a country is probably a good thing, although shareholders, investors and auditors – rather than regulators – should force management to report financial data the way they deem necessary. However, it makes a lot less sense on an international basis. Why? Countries have different cultural backgrounds and legal frameworks, meaning that certain financial ratios should not be interpreted the same way from one country to another.

Let’s take a few examples. In the US, people are much more likely than Europeans on average to walk away from their home if they can’t pay off their mortgage. Most Europeans, on the other hand, will consider mortgage repayment as priority number 1. As a result, impaired mortgage ratios could well end-up higher in the US. But US banks know that and adapt their loan loss reserves in consequence. Within Europe, legal frameworks and judiciary efficiency are also key: UK banks often set aside fewer funds against mortgage losses as the legal system allows them to foreclose and sell homes relatively quickly and with minimal losses. In France on the other hand, the process is much longer with many regulatory and legal hurdles. Consequently, UK-based mortgage banks seem to have lower loan loss reserves compared with some of their continental Europe peers. Does it mean they are riskier? Not really.

Another (abstract) example: in country A, the local culture pushes people to pay off their debt at all costs, whereas in country B, most people, once they stop paying back when they run into short-term trouble, never resume payment. In country A, banks consider it safe to classify a loan as impaired only after 180 days without payment. In country B though, banks know that the loan will never be paid off as soon as it is 30 days past due. Standardisation would make both countries use the same classification. Why not, but it doesn’t bring much: analysts will still have to take into account local variations (just in a different way). However, it might spark an unnecessary panic in country A when figures suddenly look much worse to the untrained public.

This is the issue with harmonising. Some standardisation may be welcome, but most analysts and investors already know the differences in reporting between countries and don’t take headline figures at par value, making the EBA exercise relatively pointless. For the less-well informed individuals, the EBA harmonisation could also bring a false sense of safety: figures look comparable, but in reality, they’re not entirely. In the end, harmonised reporting or not, adjustments always have to be made…

The same apply to most internationally-applied regulations. Basel rules, for example, effectively apply standardised capital and liquidity requirements throughout the world (with some local implementation differences). Banks in higher-risk countries have to comply with the same capital ratios as banks in lower-risk countries, the adjustment being made through risk-weighted assets…which are easily gamed. But analysts know well enough that a 17% regulatory Tier 1 ratio (a key bank capital safety ratio) is actually poor for an African bank, despite looking high by Western standards and way above official requirements.

In the end, standardisation makes particular sense in geographical areas where both culture and legal frameworks present only minor differences, such as the US. Europe is still a pretty fragmented continent, and it doesn’t look like things are going to change overnight. The EBA hasn’t been very clear about the exact implementation of its criteria. Let’s just hope they keep the issues discussed in this post in mind.

What Walter Bagehot really said in Lombard Street (and it’s not nice for central bankers and regulators)

(Warning: this is quite a long post as I reproduce some parts of Bagehot’s writings)

As I promised in a post a few days ago, I am today getting back to the common ancestor of all of today’s central bankers, Walter Bagehot.

Bagehot is probably one of the most misquoted economist/businessmen of all times. Most people seem to think they can just cherry pick some of his claims to justify their own beliefs or policies, and leave aside the other ones. Sorry guys, it doesn’t work like that. Bagehot’s recommendations work as a whole. Here I am going to summarise what Bagehot really said about banking and regulation in his famous book Lombard Street: A description of the Money Market.

Let’s start with central banking. As I’ve already highlighted a few days ago, Bagehot said that the institution that holds bank reserves (i.e. a central bank) should:

- Lend freely to solvent banks and companies

- Lend at a punitive rate of interest

- Lend only against good quality collateral

I can’t recall how many times I’ve heard central bankers, regulators and journalists repeating again and again that “according to Bagehot” central banks had to lend freely. Period. Nothing else? Nop, nothing else. Sometimes, a better informed person will add that Bagehot said that central banks had to lend to solvent banks only or against good collateral. Very high interest rates? No way. Take a look at what Mark Carney said in his speech last week: “140 years ago in Lombard Street, Walter Bagehot expounded the duty of the Bank of England to lend freely to stem a panic and to make loans on “everything which in common times is good ‘banking security’.”” Typical.

Now hold your breath. What Bagehot said did not only involve central banking in itself but also the banking system in general, as well as its regulation. Bagehot attacked…regulatory ratios. Check this out (chapter 8, emphasis mine):

But possibly it may be suggested that I ought to explain why the American system, or some modification, would not or might not be suitable to us. The American law says that each national bank shall have a fixed proportion of cash to its liabilities (there are two classes of banks, and two different proportions; but that is not to the present purpose), and it ascertains by inspectors, who inspect at their own times, whether the required amount of cash is in the bank or not. It may be asked, could nothing like this be attempted in England? could not it, or some modification, help us out of our difficulties? As far as the American banking system is one of many reserves, I have said why I think it is of no use considering whether we should adopt it or not. We cannot adopt it if we would. The one-reserve system is fixed upon us.

Here Bagehot refers to reserve requirements, and pointed out that banks in the US had to keep a minimum amount of reserves (i.e. today’s equivalent would be base fiat currency) as a percentage of their liabilities (= customer deposits) but that it did not apply to Britain as all reserves were located at the Bank of England and not at individual banks (the US didn’t have a central bank at that time). He then follows:

The only practical imitation of the American system would be to enact that the Banking department of the Bank of England should always keep a fixed proportion—say one-third of its liabilities—in reserve. But, as we have seen before, a fixed proportion of the liabilities, even when that proportion is voluntarily chosen by the directors, and not imposed by law, is not the proper standard for a bank reserve. Liabilities may be imminent or distant, and a fixed rule which imposes the same reserve for both will sometimes err by excess, and sometimes by defect. It will waste profits by over-provision against ordinary danger, and yet it may not always save the bank; for this provision is often likely enough to be insufficient against rare and unusual dangers.

Bagehot thought that ‘fixed’ reserve ratios would not be flexible enough to cope with the needs of day-to-day banking activities and economic cycles: in good times, profits would be wasted; in bad times, the ratio is likely not to be sufficient. Then it gets particularly interesting:

But bad as is this system when voluntarily chosen, it becomes far worse when legally and compulsorily imposed. In a sensitive state of the English money market the near approach to the legal limit of reserve would be a sure incentive to panic; if one-third were fixed by law, the moment the banks were close to one-third, alarm would begin, and would run like magic. And the fear would be worse because it would not be unfounded—at least, not wholly. If you say that the Bank shall always hold one-third of its liabilities as a reserve, you say in fact that this one-third shall always be useless, for out of it the Bank cannot make advances, cannot give extra help, cannot do what we have seen the holders of the ultimate reserve ought to do and must do. There is no help for us in the American system; its very essence and principle are faulty.

To Bagehot, requirements defined by regulatory authorities were evidently even worse, whether for individual banks or applied to a central bank. I bet he would say the exact same thing of today’s regulatory liquidity and capital ratios, which are essentially the same: they can potentially become a threshold around which panic may occur. As soon as a bank reaches the regulatory limit (for whatever reason), alarm would ring and creditors and depositors would start reducing their lending and withdrawing their money, draining the bank’s reserves and either creating a panic, or worsening it. This reasoning could also be applied to all stress tests and public shaming of banks by regulators over the past few years: they can only make things worse.

Even more surprising: the spiritual leader of all of today’s central bankers was actually…against central banking. That’s right. Time and time again in Lombard Street he claimed that Britain’s central banking system was ‘unnatural’ and only due to special privileges granted by the state. In chapter 2, he said:

I shall have failed in my purpose if I have not proved that the system of entrusting all our reserve to a single board, like that of the Bank directors, is very anomalous; that it is very dangerous; that its bad consequences, though much felt, have not been fully seen; that they have been obscured by traditional arguments and hidden in the dust of ancient controversies.

But it will be said—What would be better? What other system could there be? We are so accustomed to a system of banking, dependent for its cardinal function on a single bank, that we can hardly conceive of any other. But the natural system—that which would have sprung up if Government had let banking alone—is that of many banks of equal or not altogether unequal size. In all other trades competition brings the traders to a rough approximate equality. In cotton spinning, no single firm far and permanently outstrips the others. There is no tendency to a monarchy in the cotton world; nor, where banking has been left free, is there any tendency to a monarchy in banking either. In Manchester, in Liverpool, and all through England, we have a great number of banks, each with a business more or less good, but we have no single bank with any sort of predominance; nor is there any such bank in Scotland. In the new world of Joint Stock Banks outside the Bank of England, we see much the same phenomenon. One or more get for a time a better business than the others, but no single bank permanently obtains an unquestioned predominance. None of them gets so much before the others that the others voluntarily place their reserves in its keeping. A republic with many competitors of a size or sizes suitable to the business, is the constitution of every trade if left to itself, and of banking as much as any other. A monarchy in any trade is a sign of some anomalous advantage, and of some intervention from without.

As reflected in those writings, Bagehot judged that the banking system had not evolved the right way due to government intervention (I can’t paste the whole quote here as it would double the size of my post…), and that other systems would have been more efficient. This reminded me of Mervyn King’s famous quote: “Of all the many ways of organising banking, the worst is the one we have today.” Another very interesting passage will surely remind my readers of a few recent events (chapter 4):

And this system has plain and grave evils.

1st. Because being created by state aid, it is more likely than a natural system to require state help.

[…]

3rdly. Because, our one reserve is, by the necessity of its nature, given over to one board of directors, and we are therefore dependent on the wisdom of that one only, and cannot, as in most trades, strike an average of the wisdom and the folly, the discretion and the indiscretion, of many competitors.

Granted, the first point referred to the Bank of England. But we can easily apply it to our current banking system, whose growth since Bagehot’s time was partly based on political connections and state protection. Our financial system has been so distorted by regulations over time than it has arguably been built by the state. As a result, when crisis strikes, it requires state help, exactly as Bagehot predicted. The second point is also interesting given that central bankers are accused all around the world of continuously controlling and distorting financial markets through various (misguided or not) monetary policies.

For all the system ills, however, he argued against proposing a fundamental reform of the system:

I shall be at once asked—Do you propose a revolution? Do you propose to abandon the one-reserve system, and create anew a many-reserve system? My plain answer is that I do not propose it. I know it would be childish. Credit in business is like loyalty in Government. You must take what you can find of it, and work with it if possible.

Bagehot admitted that it was not reasonable to try to shake the system, that it was (unfortunately) there to stay. The only pragmatic thing to do was to try to make it more efficient given the circumstances.

But what did he think was a good system then? (chapter 4):

Under a good system of banking, a great collapse, except from rebellion or invasion, would probably not happen. A large number of banks, each feeling that their credit was at stake in keeping a good reserve, probably would keep one; if any one did not, it would be criticised constantly, and would soon lose its standing, and in the end disappear. And such banks would meet an incipient panic freely, and generously; they would advance out of their reserve boldly and largely, for each individual bank would fear suspicion, and know that at such periods it must ‘show strength,’ if at such times it wishes to be thought to have strength. Such a system reduces to a minimum the risk that is caused by the deposit. If the national money can safely be deposited in banks in any way, this is the way to make it safe.

What Bagehot described is a ‘free banking’ system. This is a laissez faire-type banking system that involves no more regulatory constraints than those applicable to other industries, no central bank centralising reserves or dictating monetary policy, no government control and competitive currency issuance. No regulation? No central bank to adequately control the currency and the money supply and act as a lender of last resort? No government control? Surely this is a recipe for disaster! Well…no. There have been a few free banking systems in history, in particular in Scotland and Sweden in the 19th century, to a slightly lesser extent in Canada in the 19th and early 20th, and in some other locations around the world as well. Curiously (or not), all those banking systems were very stable and much less prone to crises than the central banking ones we currently live in. Selgin and White are experts in the field if you want to learn more. If free banking was so effective, why did it disappear? There are very good reasons for that, which I’ll cover in a subsequent post on the history of central banking.

I am not claiming that Bagehot held those views for his entire life though. A younger Bagehot actually favoured monopolised-currency issuance and the one-reserve system he decried in his later life. I am not even claiming that everything he said was necessarily right. But Bagehot as a defender of free banking and against regulatory requirements of all sort is a far cry from what most academics and regulators would like us to believe today. Personally, I find that, well, very ironic.

Financial innovation is back with a vengeance

What didn’t we hear about financial innovation throughout the crisis? Whereas innovation in general is good, financial innovation on the other hand was the worst possible thing coming out of a human mind. Paul Volcker, former Chairman of the Fed, famously declared that the ATM was the only useful financial innovation since the 1980s. Harsh.

True, some financial innovations are better than others. In particular, those used to bypass regulatory restrictions are more dangerous, not because they are intrinsically evil or anything, but simply because their often complex legal structure makes them opaque and difficult for external analysts and investors to analyse. This famous 2010 Fed paper attempted to map the shadow banking system (see picture), and usefully stated that not all shadow banking (and financial innovations) activities were dangerous (but those specifically designed to avoid regulations were). Ironically (and typically…) one of the first innovations to ever appear within the shadow banking system was money market funds. What was the rationale behind their creation? In the 1960s and 1970s in the US, interest payment on bank demand deposits was prohibited and capped on other types of deposits. The resulting financial repression through high inflation pushed financial innovators to come up with a way of bypassing the rule: money market funds became a deposit-equivalent that paid higher interests. Today we blame money market funds for being responsible for a quiet run on banks during the crisis, precipitating their fall. It would just be good to remember that without such stupid regulation in the first place, money market funds might have never existed…

The last decade has seen the growth of two particularly interesting innovations within the shadow banking system: one was relatively hidden (securitisation) while the other one grew in the spotlight (crowdfunding/peer-to-peer lending). One was deemed dangerous. The other one was more than welcome (ok, not in France). What had to happen happened: they are now combining their strength.

Various types of crowdfunding exist: equity crowdfunding, P2P lending, project financing… Today I’m going to focus on P2P lending only. What started as platforms enabling individuals to lend to other individuals are now turning into massive gates for complex institutional investors to lend to individuals and SMEs. Given the retreat of banks from the SME market (thank you Basel), various institutional investors (mutual and hedge funds, insurance firms) thought about diversifying their investments (and maximising their returns) by starting to offer loans to individuals and companies they normally can’t reach.

Basically, those funds had a few options: developing the capabilities to directly lend to those customers, investing in securitised portfolios of bank loans, or investing in securitised portfolios of P2P loans. The first option was very complex to implement and the required infrastructure would take a long time to develop. The second option had already existed for a little while, but was dependent on banks lending to customers, which current regulations limit due to higher capital requirements on such loans. The third option, on the other hand, allowed funds to maximise returns and attract more potential borrowers thanks to the reduction of the cost of borrowing by disintermediating banks. And funds could also strike deals with those still tiny online platforms that would have never happened with massive banks.

While securitisation sounds scary, it is actually only a simpler way of investing in loans of small sizes (the alternative being to invest in every single loan, some of them amounting to only USD500… Not only many funds don’t have the capability of doing such things, but many have also restrictions about the types of asset class and amounts they can invest in). Securitisation also bypasses Wall Street investment banks: funds directly invest in P2P loans, package them and sell them on to other investors while retaining a ‘tranche’ in the deal, which absorbs losses first. Now some entrepreneurs are even talking of setting up secondary markets to trade investments in loans, pretty much like a smaller version of the bond market.

Is this a welcome evolution for the P2P industry? I would say that it is a necessary evolution. It is once again a spontaneous development that merely reflects the need for funding of the P2P industry, which small retail investors cannot fulfil (unless all investment funds’ customers start withdrawing their money to directly invest in P2P, which is highly unlikely). Many start to think that large institutional investors will end up crowding out small retail investors. Possibly, but as long as regulation remains light, keeping barriers to entry low, new platforms only accepting retail investors could well appear if the demand is present.

All this is fascinating. Not only because technology and the internet enables new ways of channelling funds from savers to borrowers, but also because this is the growth of a parallel 100%-reserve banking system. The shadow banking system is effectively some version of a 100%-reserve banking. And it keeps growing through those various innovations. As I argued in a previous post, this may well have implications for monetary policy that current central banks and economists don’t take into account. A 100%-reserve banking system does not have a deposit multiplier and consequently does not have an elastic currency to respond to a sudden increase or decrease in the demand for money. However, such a system perfectly matches savers’ and borrowers’ intertemporal preferences, limiting malinvestments. Nonetheless, we for now remain in a mix system of 100% reserve (most of shadow banking) and fractional reserves (traditional banking). It would still be interesting to study the possible policy implications of a growth in the 100%-reserve part of the economy.

The Economist struggles with Wicksell

Looks like Wicksell is back in fashion. After years (decades?) with barely any mention of this distinguished Swedish economist outside of work from some heterodox economic schools academics (like the Austrians), he is now everywhere and has unleashed a great debate among academics and financial practitioners. This is the outcome of both the financial crisis (preceded by interest rates that were below their ‘natural’ level according to Wicksellian-based theories) and the current unconventional policies undertaken by central banks all over the world (that risk repeating the same mistakes according to those same theories).

This week’s Economist’s column Free Exchange tries to identify whether or not current interest rates are too low based on a Wicksellian framework (A natural long-term rate). The article is complemented by a Free Exchange blog post on the newspaper’s website.

I won’t get back to the definitions of Wicksell’s money and natural rates of interest as I’ve done it in two recent posts (here and here). I only wish today to comment on The Economist’s interpretation (and misconceptions) of the Wicksellian rate.

A few of things shocked me in this week’s column. First, the assertions that “the natural rate prevails when the economy is at full employment” and that “the natural interest rate is often assumed to be constant.” I’m sorry…what? Putting aside the fact that ‘full employment’ is hard to define, there can be full employment with interest rates below or above their natural level, and interest rates can be at their natural level with the economy not at full employment. Many other ‘real’ factors have effects on ‘full employment’. Using full employment as a basis for spotting the equilibrium rate is dangerous.

Second, where did they get that the natural interest rate was constant? This doesn’t make sense. The natural interest rate rises and decreases following a few variables (various economic schools of thought will have differing opinions) such as time preference (i.e. whether or not people prefer to use income for immediate or future consumption), marginal product of capital (demand for loanable funds by entrepreneurs would increase as long as they can make a profit on the marginal increase in capital stock, driving up the interest rate in the process), liquidity preference (i.e. whether or not people desire to hold money as cash rather than some other less liquid form of wealth – pretty much the only important factor driving the interest rate for Keynesians –)… As you can imagine, all those factors vary constantly, impacting the demand for money and the demand for credit and in turn the rate of interest. It clearly does not remain constant…

The Economist also dismisses the possibility that real interest rates are too low by the fact that sovereign bonds’ yields are low, not only in the US (where the Fed is engaged in massive bonds purchases), but also in other economies whose central banks are less active in purchasing sovereign debt. But it overlooks the fact that natural rates aren’t uniform and may well be lower in other countries (for example, the natural rate was probably lower in Germany than in Spain and Ireland before the crisis, despite having a common central bank). It also overlooks that ‘risk-free’ rates used as a basis of most financial calculations internationally are US Treasuries, not sovereign bonds of other countries.

Finally, in support of its point, the column argues that expected future low rates could also reflect investors’ expectations of sluggish future growth and that “despite profit margins near record levels and rock-bottom interest rates, business investment has been sluggish, recently peaking at just above 12% of GDP; it topped 14% in the late 1990s.” Once again, this is misinterpreting the natural rate: the level of the natural rate of interest does not necessarily depend on expected future economic growth as I described above. Sluggish business investments also are more likely to reflect current regulatory ‘regime uncertainty’ than entrepreneurs’ doubts about the future state of the economy. On top of that, using the dotcom bubble as a reference for business investment is intellectually dishonest. Moreover, the article contradicts itself starting with “central banks ignore this century-old observation at their peril” only to conclude that “all this suggests that policy rates, low as they seem, are not out of line with their natural level.” Hhhmmm, ok.

The Free Exchange blog post by Greg Ip is a little better but still overall quite confused and confusing. Interestingly, it cites a paper by Bill White (http://dallasfed.org/assets/documents/institute/wpapers/2012/0126.pdf) who argues that the sort of yield-chasing that we can witness in financial markets today is a symptom of nominal rates being lower than natural rates. Doesn’t this remind you of anything? That’s right; it was exactly my point in this post. But it then cites Brad de Long, who can be added to the list of people who don’t understand what regulatory uncertainty is, and who tries as a result to convince us that the natural rate is below zero. Theoretically, a below zero natural rate if possible in period of deflation. But it does not make much sense to have a natural rate below zero when inflation is above zero.

It is definitely a hard task to identify the natural rate of interest. Nonetheless, a few rules of thumb are sometimes better than overly-complex reasoning. Investors would be perfectly happy with negative nominal yields if cost of life was declining even faster. This is obviously not the case at the moment.

BoE’s Mark Carney is burying Walter Bagehot a second time

Banks were partying on Thursday. Mark Carney, the new governor of the Bank of England, decided to ‘relax’ rules that had been put in place by its predecessor, Mervyn King. From now on, the BoE will lend to banks (as well as non-bank financial institutions) for longer maturities, accept less quality collateral in exchange, and lower the interest rate on/cost off those facilities. Mervin King was worried about ‘moral hazard’. Mark Carney has no idea what that means.

According to the FT, Barclays quickly figured out what this move implied: “it reduces the need for, and the cost of, holding large liquidity buffers.” Just wow. So, while we’ve just experienced a crisis during which some banks collapsed because they didn’t hold enough liquid assets on their balance sheet as they expected central banks and governments to step in if required, Carney’s move is expected to make the banks hold……even less liquidity.

It’s obviously nothing to say that this goes against every possible piece of regulation devised over the last few years. While the regulators were right in thinking that banks needed to hold more liquid assets, they took on the wrong problem: it was government and central bank support that brought about low liquidity holdings, and not free-markets recklessness. Anyway, Carney’s move kind of undermines that effort and risks rewarding mismanaged banks at the expense of safer ones.

Carney’s decision also goes against all the principles devised by the ‘father’ of central banking: Walter Bagehot. I guess it is time to decipher Bagehot, as he has been constantly misquoted since the start of the crisis by people who have apparently never read him. As a result he was used to justify what were actually anti-Bagehot policies. Bagehot’s principles are underlined in his famous book Lombard Street, written in 1873. What should a central bank do during a banking crisis? According to Bagehot (as described in chapters 2, 4 and 7), it should:

- Lend freely to solvent banks and companies

- Lend at a punitive rate of interest

- Only accept good quality collateral in exchange

For instance, in chapter 2:

The holders of the cash reserve must be ready not only to keep it for their own liabilities, but to advance it most freely for the liabilities of others. They must lend to merchants, to minor bankers, to ‘this man and that man,’ whenever the security is good.

In chapter 7:

First. That these loans should only be made at a very high rate of interest. This will operate as a heavy fine on unreasonable timidity, and will prevent the greatest number of applications by persons who do not require it. The rate should be raised early in the panic, so that the fine may be paid early; that no one may borrow out of idle precaution without paying well for it; that the Banking reserve may be protected as far as possible.

Secondly. That at this rate these advances should be made on all good banking securities, and as largely as the public ask for them. The reason is plain. The object is to stay alarm, and nothing therefore should be done to cause alarm. But the way to cause alarm is to refuse some one who has good security to offer… No advances indeed need be made by which the Bank will ultimately lose.

No central bank applied Bagehot’s recommendations during the financial crisis. Granted, given the organisation of today’s financial system, it is difficult for central bank to lend to non-financial firms. Nonetheless, it took them a little while to start lending freely and lent to insolvent banks as well. They also started to accept worse quality collateral than what they used to (think about the Fed now purchasing mortgage/asset-backed securities for example). Finally, central banks have never charged a punitive rate on their various facilities. Quite the contrary: interest rates were pushed down as much as humanly possible on all normal and exceptional refinancing facilities.

While the ECB and the Fed have made clear that some of those were temporary measures, Carney now seems to imply that, not only are they here to stay, but they also will be extended in non-crisis times. He calls that being “open for business”. Poor Bagehot must be turning in his grave right now.

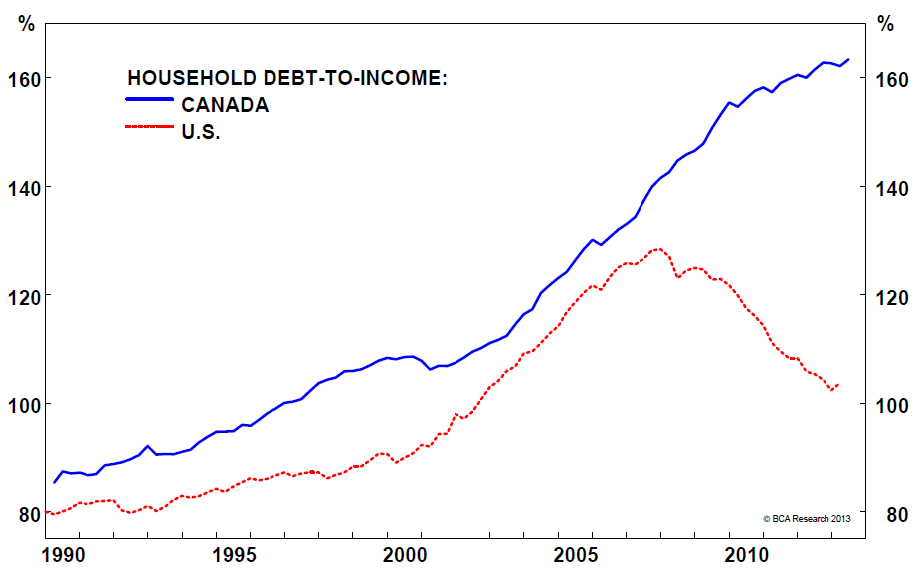

According to Carney, those measures will reinforce financial stability. Really? So no moral hazard involved? no bank taking unnecessary risks because it knows that the BoE has its back? If Mervyn King didn’t do everything perfectly while in charge, at least he had a point. Carney, after overseeing a large credit bubble in Canada over the past few years (he first joined the Bank of Canada in 2003, then rejoined it as Governor in 2008), is now applying his brilliant recipe to the UK.

I think that Carney’s decisions introduce considerable incentive distortions in the banking system. This is clearly not what a free-market should look like. In any case, if a new crisis strikes as a result, I am pretty sure that laissez-faire will be blamed again. It is ironic to see that some of those central bankers destroy faith in free-markets while trying to protect them.

Bagehot also said other things that go against the principles driving our current banking and regulatory system. More details in another post!

Photograph: Reuters/Bloomberg

Chart: The Big Picture

Co-operative Bank’s new ownership ‘tragedy’ is rather a good thing

For those of you who don’t live in the UK, the Co-operative Bank has been struggling with a large GBP1.5bn capital shortfall (vs. a capital base of GBP1.6bn) since early summer due to losses on its loan book (most of them emanating from the takeover of Britannia Building Society in 2009, a struggling mutual mortgage bank). Moody’s, the rating agency, even downgraded it by six notches all of a sudden. The Co-operative Bank was a subsidiary of the Co-operative Group, a mutual company that owns multiple businesses.

I said ‘was’ because…it won’t be anymore. And it’s apparently causing some headaches.

Mutual companies are owned by their members (who are some of their customers), and not by external shareholders. This was the case of both Britannia’s and Co-op’s equity capital (indirectly through the Co-op Group). However, due to their very nature, mutuals’ ability to raise capital is limited. Consequently, they raise complementary capital from external investors in order to grow. In the case of Co-op, its equity capital was complemented by some sort of hybrid capital: GBP60m of preference shares owned by retail investors and around GBP1.1bn of subordinated debt, which happened to be partly held by…hedge funds. Both counted towards the total regulatory capital ratio of the bank, as defined by Basel accords. Ranking of the capital structure in case of bankruptcy of the bank was as follows: after depositors and other senior creditors, subordinated creditors had the second claims on the liquidated assets of the bank, followed by preference shares-holders and members.

Following several months of negotiations that saw creditors threatening to block a deal under which they would take a loss on their investments, a deal was finally reached a few days ago: a conversion of their bonds into new equity. As a result, 70% of the capital of the bank will be owned by institutional investors, among which several hedge funds (representing around 30/40%). The Co-op Group (and hence members) will retain a 30% stake in the bank. It obviously sounds quite ironic to see a mutual company owned by vulture capitalists… It also looks quite ironic to see the failure of the now all-powerful UK regulators: they never spotted the problems at Co-op Bank, all their proposed solutions collapsed once after the other, and the agreed deal was reached in a perfect free-market type agreement without their intervention…

Many people around me and in the media have raised concerns that the new hedge funds ownership was a bad thing due to the short-term view of their investment strategy. Those fears are misplaced. Hedge funds and private equity firms indeed invest for the short-term. As far as I’m aware, there aren’t many studies analysing the impacts of hedge funds on the performance of the firms in which they own a stake. This recent one found that activist hedge funds actually improved future performances! There are many more studies on the long-term effects of short-term private equity investments. It was actually the topic of my Masters’ research dissertation. The academic research was clear: private equity-owned firms suffered over the short-term through tough restructuring processes (involving job losses and pressure on salaries), but over the longer-term performed better than their peers and actually even hired more people…

Is this surprising? No. We really need to keep emotions aside and think about the underlying reasons for all this. What is the hedge fund’s goal? To maximise profits. What is the time frame? Usually quite short-term (= a few years). How can the fund exit the investment? By selling the company to external investors. Here we go. This is key. Do you think that funds would be able to maximise the selling price if external investors viewed the company as unlikely to perform well over time? Of course not. Prices are derived from future discounted cash flows. The more likely the company is to perform well after the sale, the higher the price the hedge (or private equity) fund can extract from it. As a result, it is not in the interest of the fund to seek “short-term gains at the expense of the future”.

Of course, this does not mean that no failure ever happens. Some funds also acquire companies to dismantle them. Which does not necessarily imply that they are evil. Some companies actually represent net economic losses to society with no prospect of improvements. Those companies should disappear and capital reallocated to more efficient ones. Funds that dismantle companies usually do it as there is no other way to realise profits. Some funds also fail in restructuring firms, or overload them with debt. But when the companies fail, funds also make massive losses that threaten their own existence. It is in the interest of both to succeed.

Co-op Bank’s former CEO declared that the restructuring process was a ‘tragedy’, that hedge funds were ‘maximising profits’ and were ‘unethical’. I would like to ask: what is actually a tragedy? Is mismanaging an institution leading to bankruptcy and potential losses for ordinary individuals that ethical? What about mis-selling financial products to naïve customers on top of that? Wouldn’t it be better to have a well-performing bank that generates economic profits? Are low profits, losses and waste of capital a way of proving that a company is behaving well? Or is a company more useful for human and social advancement if it actually delivers economic benefit and creates additional capital? Some people have serious rethinking to do.

There is no real need to worry about hedge funds owning a large stake in Co-operative Bank. Co-op may well at last become an asset to society instead of a liability. Its new hedge fund owners also seem to understand that to maximise the value of the brand, ethics must remain a focus, whatever that means. But if eventually Co-op does not survive, it may also well be because it couldn’t be saved in the first place.

Update: I don’t know how I originally missed the senior creditors but I did… Depositors aren’t the only senior creditors and this is now corrected

Recent Comments