A UK housing bubble? Sam Bowman doubts it

On the Adam Smith Institute’s blog, Sam Bowman had a couple of posts (here and a follow-up here, and mentioned by Lars Christensen here) attempting to explain that there might not have been any house price bubble in the UK. He essentially says that there was no oversupply of housing in the 1990s and 2000s. Here’s Sam:

These charts show that housing construction was actually well below historical levels in the 1990s and 2000s, both in absolute terms and relative to population. It is difficult to see how someone could claim that the 2008 bust was caused by too many resources flowing toward housing and subsequently needing time to reallocate if there was no bubble in housing to begin with.

What this suggests is that the Austrian story about the crisis may be wrong in the UK (and, if Nunes’s graphs are right, the US as well). The Hayek-Mises story of boom and bust is not just about rises in the price of housing: it is about malinvestments, or distortions to the structure of production, that come about when relative prices are distorted by credit expansion.

Well, I think this is not that simple. Let me explain.

First, the Hayek/Mises theory does not apply directly to housing. In the UK, there are tons of reasons, both physical and legal, why housing supply is restricted. As a result, increased demand does not automatically translate into increased supply, unlike in Spain, which seems to have lower restrictions as shown by the housing start chart below:

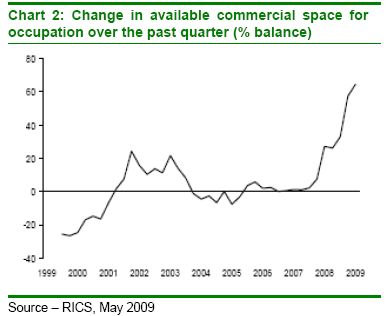

Second, Sam overlooks what happened to commercial real estate. There was indeed a CRE boom in the UK and CRE was the main cause of losses for many banks during the crisis (unlike residential property, whose losses remained relatively limited).

Third, the UK is also characterised by a lot of foreign buyers, who do not live in the UK and hence not included in the population figures. Low rates on mortgages help them purchase properties, pushing up prices, triggering a reinforcing trend while supply in the demanded areas often cannot catch up.

Fourth, the impact of Basel regulations seems to be slightly downplayed. Coincidence or not, the first ‘bubble’ (in the 1980s) appeared right when Basel’s Risk Weighted Assets were introduced. And it is ‘curious’, to say the least, that many countries experienced the same trend at around the same time. Would house lending and house prices have increased that much if those rules had never been implemented? I guess not, as I have explained many times. I have yet to write posts on what happened in several countries. I’ll do it as soon as I find some time.

I recommend you to take a look at my RWA-based Austrian Business Cycle Theory, which seems to show that, while there should indeed be long-term real estate projects started (depending on local constraints of course), there is also an indirect distortion of the capital structure of the non-real estate sector.

While there may well be ‘real’ factors pushing up real estate prices in the UK, there also seems to be regulatory and monetary policy factors exacerbating the rise.

- Chart 1: Spanish Property Insight

- Chart 2: FT Alphaville

- Chart 3: Guardian

Blame the rich for the next asset bubble. Or not.

First of all, happy new year to all of you! Fingers crossed we don’t witness another market crash this year! 🙂

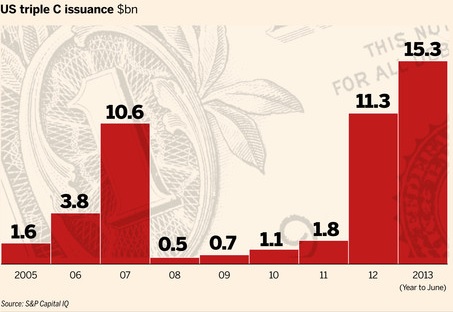

Indeed, credit markets are hot. Equity markets are also hot. The FT published an article yesterday with some striking facts about the ‘improvements’ in credit markets over the past couple of years. Some would say that it’s encouraging. I am not convinced…

Most credit indicators are close to or above their pre-credit crisis high. Sales of leveraged loans and high-yield bonds are above their pre-crisis peak. The average leverage level of US LBOs is back to 2006 level. Issuance of collateralised loan obligations is close to its pre-crisis peak. Even CCC-rated junk bonds are way above their previous peak. I’ve already mentioned some of those facts a few months ago.

In a relatively recent presentation, Citi’s strategist Hans Lorenzen confirmed the trend: central banks are indirectly suppressing most risky investments’ risk premia. Most investors expect junk bonds’ spreads to tighten further or at least to stabilise at those narrow levels and emerging markets bonds and equities, as well as junk bonds are now among investors’ top asset classes .

My ‘theory’ at the time was that (see also here), if investors were piling in increasingly riskier asset classes, bringing their yield down to record low levels in the process, and nonetheless accepting this level of risk for such low returns, it was because current central bank-defined nominal interest rates were below the Wicksellian natural rate of interest. Inflation, as felt by investors rather than the one reported by national statistics agencies, was higher than most real rates of return on relatively safe assets. In order to see their capital growing (or at least to prevent it from declining), they were forced to pick riskier assets, such as high-yield bonds, which were not really high-yield anymore as a result but remained junk nonetheless. This would result in capital misallocation as, under ‘natural’ interest rate conditions, those investments would have never taken place. Thomas Aubrey’s Wicksellian differential, an indicator of the likely gap between the nominal and the natural rates of interest, was, in line with credit markets, reaching its pre-crisis high and seemed to confirm that ‘theory’.

Well, I now think that not all investors are responsible for what we are witnessing today. The (very) rich are.

This came to my mind some time ago while reading that FT piece by John Authers. This was revealing.

“Their wealth gives them scope to try imaginative investments, but they are terrified of inflation, even as deflation is emerging as a greater risk. That is in part because inflation for the goods and services bought by the very rich is running about 2 percentage points faster than retail inflation as a whole in the UK.” (my emphasis)

In the UK, real gilts’ yields were already in negative territory: adjusted by the (potentially underestimated) consumer price index, gilts were yielding around -1% early 2013. Savers were effectively losing money by investing in those bonds. Now think about the rich: by investing in such bonds, they would get a real return of around -3% instead.

Moreover, “71 per cent of respondents said they were more worried now about a steep rise in inflation than they were five years ago.”

Does it start to make sense? The cost of living I was mentioning earlier is increasing particularly quickly for the rich. And… they are the ones who own most financial assets. In order to offset those rising living costs, they naturally look for higher-yielding investments. And it is exactly what the FT reports:

“Their favourite asset classes for the next three decades are emerging markets equities, developed equities and agricultural land, in that order. Private equity comes close after farmland, while art and collectables were also a more popular asset class than any kind of bonds. […]

Hedge funds, as a group, have not fared well since the crisis. But wealthy investors preoccupied by inflation, and robbed of the easy option of bonds, are evidently disposed to give them a try, with an average projected allocation for the next three decades of 25 per cent. Meanwhile, the chance of a bubble in agricultural land prices, or in art, looks very real.”

Are the rich responsible for our current frothy markets then? Obviously not. They are acting rationally in response to central banks’ policies. Nonetheless, this raises an interesting question. Mainstream economics only considers a high aggregate inflation rate as dangerous. What about ‘class warfare’-type inflation? It does look like inflation experienced by one socioeconomic class could inadvertently lead to asset bubbles and bursts, despite aggregate inflation remaining subdued. This may be another destabilising effect of monetary injections on relative prices.

Granted, central banks possibly are on a Keynesian’s ‘euthanasia of the rentier’-type scheme in order to try to alleviate the pain of over-indebted borrowers (and/or to encourage further lending). But financial repression avoidance might well end-up coming back with a vengeance if savers’ reactions, and in particular, rich savers’, make financial markets bubble and crash.

Charts: FT (link above), Citi and Societé Générale

The problems with the MMT-derived banking theory

(Update: Following Scott Fullwiler’s comment, I published an update here, in which I provide extra clarifications and introduce what I see as the fallacy of composition of the endogenous money theory (I moved this update to the top of my post following a few questions I received).)

Today will be a little long and technical… Many people have heard of the classic textbook story of the banking money multiplier, a characteristic of fractional reserve banking systems. Banks obtain reserves (i.e. central bank-issued high-powered money – HPM, which forms the monetary base) as customers deposit their money in, then lend out a fraction of those deposits that gets redeposited at another bank, effectively creating money in the process, and so on. In fine, reserve requirements at central banks prevent banks from expanding lending (and hence money supply) beyond a certain point. This led to the view that banks’ expansion is reserve-constrained.

But proponents of Modern Monetary Theory (MMT), and others who have no idea what MMT is, but who have been convinced by the argument, have been shouting out for a while now that this view is wrong. Banks do not lend out reserves they assert. Banks aren’t reserve-constrained but capital-constrained. Therefore, lending is endogenous, the supply of bank loans is almost perfectly elastic and the quantity supplied only driven by demand. Scott Fullwiler described the process on Warren Mosler’s (aka current MMT Guru) website. Cullen Roche has also been a strong proponent of this view (see here and here for example).

I managed to find a relatively good detailed summary of this view here:

[…] we had discussed the orthodox belief that the government controls the money supply through control over bank reserves. This position is rejected by Post Keynesians, who argue that banks expand the money supply endogenously. How is this possible in nations with a legally required reserve ratio? Banks, like other firms, take positions in assets by issuing liabilities on the expectation of making profits. Much bank activity can be analyzed as a “leveraging” of HPM–because banks issue liabilities that can be exchanged on demand for HPM on the expectation that they can obtain HPM as necessary to meet withdrawals–but many other firms engage in similar activity. For our purposes, however, the main difference between banks and other types of firms involves the nature of the liabilities. Banks “make loans” by purchasing IOUs of “borrowers”; this results in a bank liability–usually a demand deposit, at least initially–that shows up as an asset (“money”) of the borrower. Thus, the “creditors” of a bank are created simultaneously with the “debtors” to the bank. The creditors will almost immediately exercise their right to use the created demand deposit as a medium of exchange.

Indeed, bank liabilities are the primary “money” used by non-banks. The government accepts some bank liabilities in payment of taxes, and it guarantees that many bank liabilities are redeemable at par against HPM. In turn, reserves are the “money” used as means of payment (or inter-bank settlement) among banks and for payments made to the central bank; as bank “creditors” draw down demand deposits, this causes a clearing drain for the individual bank. The bank may then operate either on its asset side (selling an asset) or on its liability side (borrowing reserves) to cover the loss of reserves. In the aggregate, however, such activities only shift reserves from bank-to-bank. Aggregate excesses or deficiencies of reserves have to be rectified by the central bank. Ultimately, then, reserves are not discretionary in the short run; the central bank can determine the price of reserves–admittedly, within some constraints–but then must provide reserves more-or-less on demand to hit its “price” target (the fed funds rate in the US, or the bank rate in the UK). This is because excess or deficient reserves would cause the fed funds rate (or bank rate) to move away from the target immediately.

This means that central banks cannot control the money supply.

I am going to argue here that this view is at best inexact. And that, if the textbook description is outdated, it is still mostly right.

Scott Sumner argued on his blog that lending was effectively endogenous in the short-run but not in the long-run. I only partially agree, as even in the short-run in-built markets limits are in place.

Banks raise funding to obtain reserves

My arguments come both from my theoretical knowledge and from my practical experience of analysing banks all day long and meeting banks’ management, including treasurers/ALM managers. On a side note, the MMT story is wrong in a commodity-backed currency environment. But its proponents reply that it is only valid in our modern fiat money-based banking systems. Fair enough.

The reality is… banks do obtain funding (hence reserves) before lending in most cases. The opposite would be suicidal. Equity funding is obvious: a bank issues equity liabilities in exchange for cash that it then invests/lends. Non-equity funding, by far the largest component of banks’ funding structure (around 95% of funding), mainly comes from two sources: customer deposits and wholesale funding. Banks primarily rely on deposits to fund their lending activities. They try to attract depositors as they provide banks with more funds to lend. Of course they don’t lend out the deposits but the increase in reserves that comes along an increase in deposits allows the bank to lend more without risking a depletion of its reserve base.

Banks at the same time try to minimise the interest rate they pay on deposits in order to minimise their funding costs and maximise their net interest margin (basically the margin between the rate at which banks lend and the rate at which they borrow from depositors and other creditors). They also try to attract sticky saving and term deposits, rather than more volatile (but cheaper) demand deposits.

When banks want to lend more than what their deposit base allows them to lend, they need to turn to wholesale funding. Wholesale funding roughly comprises senior and subordinated liabilities (bonds) issued on the markets as well as interbank borrowings and repurchase agreements. Bond issues are quite simple: the bank issues its liabilities on the financial markets in exchange for cash. Cash that will then complement its existing cash reserves, and that the bank consequently lends out at a margin (unless of course the purpose of the issue was to refinance existing bonds). Interbank borrowings and repos are usually minimally used by banks as a source of funding, as they are very often short-term and unstable (i.e. can be withdrawn by other banks or not rolled over). Interbank funding (and borrowing from central banks) is the cheapest source of funds (although continuously rolling over this type of funding makes it expensive in the end). Deposits and other wholesale issues are more expensive.

What do banks do with the cash/reserves/HPM that they acquire through their various funding sources? Well, as you guessed, they lend. But not only. Banks invest. In order to maintain an adequately liquid balance sheet at all times to face withdrawals and settlements, banks mostly 1. keep some cash in hands and at the central bank, which represents their official reserves (as specified by reserve requirements), 2. invest the remaining of their cash in liquid securities, often sovereign bonds or highly-rated firms’ debt securities, which represent their ‘secondary reserves’, and 3. place some cash at other banks (interbank lending mainly).

In the end, all banks hold a liquidity buffer that represents between around 10% and 25% of their assets (and between 10 and 40% of their deposit base), under the form of both primary and secondary reserves. Why not keeping all as cash? Because of the opportunity cost of holding cash. To maximise their margins, banks prefer to invest that cash in liquid, easily marketable, interest-bearing securities. Why even keeping reserves in the first place? To minimise the probability of a liquidity crisis (i.e. not being able to face deposit withdrawals, interbank settlements or other liability maturity). If liquidity were not a constraint and banks’ only goal was to maximise profits independently of liquidity risk, they would simply avoid investing in low-yielding securities and lend at a higher margin instead. In order to maintain their net interest margin, it also happens that banks try to slow the pace of deposit inflows by lowering their rates on saving accounts, if they don’t have enough lending opportunities.

Are you starting to see the differences with the MMT/endogenous lending story?

Let’s take a real life example (figures at end-2012): Wells Fargo (a large bank that does not have oversized investment banking activities that distort its balance sheet, which makes it similar to smaller-sized banks as a result). What does its funding structure (liability side of the balance sheet) look like? Unsurprisingly, 83% of its non-equity funding comes from customer deposits. Long-term senior and wholesale funding represents 9% of its funding structure. What about short-term wholesale and interbank funding? 6% only of its total funding. Clearly, Wells Fargo does not fund its lending by borrowing from other banks. Its loans/deposits ratio is 84%. It gets its reserves from other sources.

Let’s pick another similar bank that has a 126% loans/deposits ratio, UK-based Lloyds Banking Group. In this case, deposits could obviously not fund all lending. Did the bank fund its additional lending through interbank borrowing? No. Interbank borrowing only represents 2% of its funding structure. Adding other short-term wholesale funding makes it 10%.

A few points directly stand out:

- Why would banks try to attract depositors, or even bother issuing expensive debt on the bond markets, if all they have to do to fund their lending is an accounting entry followed by some interbank or central bank borrowing?

- Why would banks bother attracting expensive stable funding sources if all they have to do is to continuously increase (or roll over) short-term interbank or central bank borrowings?

- Why are banks even keeping such amounts of primary and secondary reserves if, once again, reserves are not a constraint and all they have to do is to go ask fellow banks or central banks for reserves, which they have to provide to stick to their monetary policy?

From all those points, MMTers could reach the conclusion that bankers don’t seem to know what they’re doing.

There is a relatively straightforward answer to those questions: reserves still matter. Reserves are not directly lent out. They are indirectly lent out. When a bank credits the account of a customer out of thin air following a loan agreement, it exposes itself to a flight of reserves whose amount is equal to the loan, as correctly described by MMTers. Therefore, banks need to maintain an adequate level of reserves, as represented by their primary and secondary reserve buffers. If their primary reserves are low, banks can sell some of their secondary reserves to get hold of new cash for settlements. No need to borrow from the interbank market. However, there is a limit to this process: at some point, secondary reserves will also be exhausted. This is extremely unlikely though. Such a fall in balance sheet liquidity would be punished by financial markets (see below), incentivising banks to retain enough liquidity.

Moreover, banks usually try to avoid borrowing more than a limited amount on the interbank/money market. Why?

- Because this is a suicidal way of funding banking activities. A bank that would only rely on short-term and volatile interbank borrowing to fund its lending would expose itself to market actors’ furore: banks would start reducing their exposures to it, rating agencies would downgrade it, its share price would fall, and its cost of borrowing on the interbank market (or anywhere else) would rise.

- Because borrowing at very short-notice on wholesale markets would expose the bank to penalty interest rates. Most central banks also apply penalty rates to banks short of reserves.

But, the central bank has a target rate and needs to stick to it, MMTers are going to reply, thereby providing all the required reserves to this bank. What are the implications of such a claim?

Implications for a single bank

A bank that would have single-handedly increased its lending, and hence its liabilities, without securing reserves in the first place, is at risk of experiencing adverse interbank clearing and losing some of its reserves. At some point, its reserves could fall below the required amount. However, as we have seen above, the bank holds secondary reserves that it can deplete before running out of primary reserves. What the MMT story overlooks is market reactions to a bank losing its liquidity. I know no investor or no banker that would provide funds to a bank running out of liquid reserves, unless at increasingly high interest rates, even if they know that the bank could obtain reserves from the central bank. As a result, a bank single-handedly expanding beyond what its reserve would normally allow it to is going to experience a quickly rising marginal cost of funding as a response to the loss of its liquid holdings, pressurising its net interest margin and stopping its expansion.

If the bank reaches the point at which it has to borrow directly from the central bank as it has no other choice, it is already too late: markets are aware of its lack of primary or secondary reserves and won’t deal with it anymore. As a result, central banks’ overnight lending in such conditions is self-defeating. Banks, which is an industry based on trust and reputation, will do everything they can to prevent this situation from occurring in order to avoid the stigma associated with it, as we’ve seen many times during the crisis (see also a Fed study here, as well as this one). However, a bank in good financial health could well borrow from the central bank’s discount window from time to time to optimise its liability structure and cost of funding. In the end, a single bank might not technically be reserve-constrained, but it becomes reserve-constrained through market discipline! Of course, in good times, market participants can become more tolerant towards less-liquid balance sheet structures, but the principle still applies.

We could apply the same line of reasoning to asset quality. As a bank expands, the marginal return on lending diminishes and it has to lend to increasingly less creditworthy borrowers. The resulting pressure on its asset quality starts worrying market actors, impacting its cost of funding and slowing its expansion.

Moreover, the interbank lending rate need not rise if a single bank is having difficulties to fund itself. Other banks could actually see their borrowing cost fall as they see massive money market deposit inflows, keeping the aggregate rate stable. Second, central banks clearly cannot completely control the rate: it jumps way above target from time to time.

Implications for the system as a whole

There seems to be an inherent implication to the MMT/endogenous lending story: all banks have a natural incentive to expand as they can freely borrow reserves from the central bank. By literally following their description, it seems that most, if not all banks are fully loaned up as there is no risk of becoming illiquid. Although in such a case, there is no way they can borrow and lend from the interbank market: none of them has excess reserves. The only thing they can do is borrow from the central bank, which cannot refuse if it wants its target interest rate to remain on target. Consequently, the central bank cannot control the money supply as demand for commercial loans is out of its control.

There are a couple of contradictions here. If all banks are short of reserves, there is no interbank market anymore. Nonetheless, it is true that money markets can still exist with money market funds and other non-bank financial institutions and businesses supplying short-term cash to banks. However, this situation is unlikely to happen: as described above, increasing marginal cost of funding for all the banks trying to expand beyond reasonable will slow and eventually stop the process. Only a simultaneous increase in lending by all banks could lead to all banks expanding beyond the limit. In such a case, interbank settlements would cancel out, leaving the reserve positions of each bank unaffected, with no need to borrow for settlements. In practice, banks never expand at the exact same time: some banks are aggressive, some banks are conservative.

What about empirical evidence?

The evident conclusion that MMTers reach is that reserve requirements are ineffective in reducing loan growth. Is there any empirical evidence to confirm this claim? There is. But it doesn’t exactly reach the same conclusion. A few central banks actively use reserve requirements as a monetary policy tool, such as China’s, Russia’s, Brazil’s and Turkey’s. Take a look at the charts from this recent Gavyn Davies article in the FT on China:

From those charts, we can see that every time reserve requirements are cut (mid-2008, early 2012), loan growth surges temporarily while the newly-available reserves are released. When reserve requirements are increased (early 2010, early 2011), loan growth slightly falls relative to trend. Granted, those charts do not show us the whole picture: other factors may well impact loan growth.

Another FT blog post summarised the trend, although the chart stops in 2010:

A BIS study on Chinese reserve requirements also found a link:

I don’t have data for Turkey and Russia, but this study found that increases in reserve requirements led to a contraction in domestic credit in Brazil.

What about interbank lending rate? It is pretty well reported that banks in worse financial health have to pay more for reserves on the interbank market (or on any other market). This should not be a surprise to financial markets actors: everyone knows that illiquid and/or insolvent banks have wider credit spreads. Does it necessarily mean that, as soon as a bank has to pay more than the target rate, it should instead borrow from the central bank? Obviously not. And we have already mentioned the stigma associated to this.

Finally, what about the moral hazard associated with unrestricted supply of reserves? If this were true, surely this is a very bad way of designing and managing a banking system?

This leaves us with the good’ol money multiplier textbook explanation. As I said at the beginning of this (long) post, it is quite outdated, but it remains essentially right, albeit in an indirect way. Nowadays, banks engage in what they call ALM (asset/liability management) through specific departments that identify and manage mismatches between the maturities of assets and liabilities and their respective cash inflows and outflows. As a result of this dynamic and active management, banks try to economise on reserves and take slightly more funding and liquidity risks than 19th century “collect and lend”-type banks. Nonetheless, reserves still matter and ALM bankers and treasurers also set up contingency liquidity plans, which would not make sense if they could freely access interbank or central bank funding without repercussions.

There are probably other things I could say about the MMT/endogenous money story. I may follow-up later, but for now this post is long enough… I just thought that some reality had to be reintroduced into the story, which sounds theoretically as pleasant as a fairy tale but doesn’t seem to stand its ground when you dig a little deeper.

Update: I initially quoted Frances Coppola in this post as her view seemed to be pretty similar to the quoted MMT story. She told me it wasn’t the case, and I updated the post as a result. There are still several things she said that I don’t agree with though.

Cato Institute’s 31st Monetary Conference – Was the Fed a good idea?

About two weeks ago, the US-based think tank Cato organised its annual monetary conference. Great panels and very interesting speeches.

Three panels were of particular interest to me: panel 1 (“100 Years of the Fed: What Have We Learned?”), panel 2 (“Alternatives to Discretionary Government Fiat Money”), panel 3 (“The Fed vs. the Market as Bank Regulator”).

In panel 1, George Selgin destroys the Federal Reserve’s distorted monetary history. Nothing much new in what he says for those who know him but it just never gets boring anyway. He covers: some of the lies that the Federal Reserve tells the general public to justify its existence, pre-WW2 Canada and its better performing monetary system despite not having a central bank, the lack of real Fed independence from political influence and……the Fed not respecting Bagehot’s principles despite claiming to do so. In this panel, the speech of Jerry Jordan, former President of the Federal Reserve Bank of Cleveland, is also very interesting.

In panel 2, Larry White speaks about alternatives to government fiat money, counterfeiting laws and state laws making it illegal to issue private money. Scott Sumner describes NGDP level targeting. Here again, nothing really new for those who follow his blog, but interesting nonetheless (even though I don’t agree with everything) and a must see for those who don’t.

In panel 3, John Allison provides an insider view of regulators’ intervention in banking (he used to be CEO of BB&T, an American bank). He argues that mathematical risk management models provide unhelpful information to bankers. He would completely deregulate banking but increase capital requirements, which is an original position to say the least. Kevin Dowd’s speech is also interesting: he covers regulatory and accounting arbitrage (SPEs, rehypothecation…) and various banking regulations including Basel’s.

Overall, great stuff and you should watch the whole of it (I know, it’s long… you can probably skip most Q&As).

PS: Scott Sumner also commented on the Pope’s speech on “evil incarnate”. Reminds me of the vocabulary I used…

What Walter Bagehot really said in Lombard Street (and it’s not nice for central bankers and regulators)

(Warning: this is quite a long post as I reproduce some parts of Bagehot’s writings)

As I promised in a post a few days ago, I am today getting back to the common ancestor of all of today’s central bankers, Walter Bagehot.

Bagehot is probably one of the most misquoted economist/businessmen of all times. Most people seem to think they can just cherry pick some of his claims to justify their own beliefs or policies, and leave aside the other ones. Sorry guys, it doesn’t work like that. Bagehot’s recommendations work as a whole. Here I am going to summarise what Bagehot really said about banking and regulation in his famous book Lombard Street: A description of the Money Market.

Let’s start with central banking. As I’ve already highlighted a few days ago, Bagehot said that the institution that holds bank reserves (i.e. a central bank) should:

- Lend freely to solvent banks and companies

- Lend at a punitive rate of interest

- Lend only against good quality collateral

I can’t recall how many times I’ve heard central bankers, regulators and journalists repeating again and again that “according to Bagehot” central banks had to lend freely. Period. Nothing else? Nop, nothing else. Sometimes, a better informed person will add that Bagehot said that central banks had to lend to solvent banks only or against good collateral. Very high interest rates? No way. Take a look at what Mark Carney said in his speech last week: “140 years ago in Lombard Street, Walter Bagehot expounded the duty of the Bank of England to lend freely to stem a panic and to make loans on “everything which in common times is good ‘banking security’.”” Typical.

Now hold your breath. What Bagehot said did not only involve central banking in itself but also the banking system in general, as well as its regulation. Bagehot attacked…regulatory ratios. Check this out (chapter 8, emphasis mine):

But possibly it may be suggested that I ought to explain why the American system, or some modification, would not or might not be suitable to us. The American law says that each national bank shall have a fixed proportion of cash to its liabilities (there are two classes of banks, and two different proportions; but that is not to the present purpose), and it ascertains by inspectors, who inspect at their own times, whether the required amount of cash is in the bank or not. It may be asked, could nothing like this be attempted in England? could not it, or some modification, help us out of our difficulties? As far as the American banking system is one of many reserves, I have said why I think it is of no use considering whether we should adopt it or not. We cannot adopt it if we would. The one-reserve system is fixed upon us.

Here Bagehot refers to reserve requirements, and pointed out that banks in the US had to keep a minimum amount of reserves (i.e. today’s equivalent would be base fiat currency) as a percentage of their liabilities (= customer deposits) but that it did not apply to Britain as all reserves were located at the Bank of England and not at individual banks (the US didn’t have a central bank at that time). He then follows:

The only practical imitation of the American system would be to enact that the Banking department of the Bank of England should always keep a fixed proportion—say one-third of its liabilities—in reserve. But, as we have seen before, a fixed proportion of the liabilities, even when that proportion is voluntarily chosen by the directors, and not imposed by law, is not the proper standard for a bank reserve. Liabilities may be imminent or distant, and a fixed rule which imposes the same reserve for both will sometimes err by excess, and sometimes by defect. It will waste profits by over-provision against ordinary danger, and yet it may not always save the bank; for this provision is often likely enough to be insufficient against rare and unusual dangers.

Bagehot thought that ‘fixed’ reserve ratios would not be flexible enough to cope with the needs of day-to-day banking activities and economic cycles: in good times, profits would be wasted; in bad times, the ratio is likely not to be sufficient. Then it gets particularly interesting:

But bad as is this system when voluntarily chosen, it becomes far worse when legally and compulsorily imposed. In a sensitive state of the English money market the near approach to the legal limit of reserve would be a sure incentive to panic; if one-third were fixed by law, the moment the banks were close to one-third, alarm would begin, and would run like magic. And the fear would be worse because it would not be unfounded—at least, not wholly. If you say that the Bank shall always hold one-third of its liabilities as a reserve, you say in fact that this one-third shall always be useless, for out of it the Bank cannot make advances, cannot give extra help, cannot do what we have seen the holders of the ultimate reserve ought to do and must do. There is no help for us in the American system; its very essence and principle are faulty.

To Bagehot, requirements defined by regulatory authorities were evidently even worse, whether for individual banks or applied to a central bank. I bet he would say the exact same thing of today’s regulatory liquidity and capital ratios, which are essentially the same: they can potentially become a threshold around which panic may occur. As soon as a bank reaches the regulatory limit (for whatever reason), alarm would ring and creditors and depositors would start reducing their lending and withdrawing their money, draining the bank’s reserves and either creating a panic, or worsening it. This reasoning could also be applied to all stress tests and public shaming of banks by regulators over the past few years: they can only make things worse.

Even more surprising: the spiritual leader of all of today’s central bankers was actually…against central banking. That’s right. Time and time again in Lombard Street he claimed that Britain’s central banking system was ‘unnatural’ and only due to special privileges granted by the state. In chapter 2, he said:

I shall have failed in my purpose if I have not proved that the system of entrusting all our reserve to a single board, like that of the Bank directors, is very anomalous; that it is very dangerous; that its bad consequences, though much felt, have not been fully seen; that they have been obscured by traditional arguments and hidden in the dust of ancient controversies.

But it will be said—What would be better? What other system could there be? We are so accustomed to a system of banking, dependent for its cardinal function on a single bank, that we can hardly conceive of any other. But the natural system—that which would have sprung up if Government had let banking alone—is that of many banks of equal or not altogether unequal size. In all other trades competition brings the traders to a rough approximate equality. In cotton spinning, no single firm far and permanently outstrips the others. There is no tendency to a monarchy in the cotton world; nor, where banking has been left free, is there any tendency to a monarchy in banking either. In Manchester, in Liverpool, and all through England, we have a great number of banks, each with a business more or less good, but we have no single bank with any sort of predominance; nor is there any such bank in Scotland. In the new world of Joint Stock Banks outside the Bank of England, we see much the same phenomenon. One or more get for a time a better business than the others, but no single bank permanently obtains an unquestioned predominance. None of them gets so much before the others that the others voluntarily place their reserves in its keeping. A republic with many competitors of a size or sizes suitable to the business, is the constitution of every trade if left to itself, and of banking as much as any other. A monarchy in any trade is a sign of some anomalous advantage, and of some intervention from without.

As reflected in those writings, Bagehot judged that the banking system had not evolved the right way due to government intervention (I can’t paste the whole quote here as it would double the size of my post…), and that other systems would have been more efficient. This reminded me of Mervyn King’s famous quote: “Of all the many ways of organising banking, the worst is the one we have today.” Another very interesting passage will surely remind my readers of a few recent events (chapter 4):

And this system has plain and grave evils.

1st. Because being created by state aid, it is more likely than a natural system to require state help.

[…]

3rdly. Because, our one reserve is, by the necessity of its nature, given over to one board of directors, and we are therefore dependent on the wisdom of that one only, and cannot, as in most trades, strike an average of the wisdom and the folly, the discretion and the indiscretion, of many competitors.

Granted, the first point referred to the Bank of England. But we can easily apply it to our current banking system, whose growth since Bagehot’s time was partly based on political connections and state protection. Our financial system has been so distorted by regulations over time than it has arguably been built by the state. As a result, when crisis strikes, it requires state help, exactly as Bagehot predicted. The second point is also interesting given that central bankers are accused all around the world of continuously controlling and distorting financial markets through various (misguided or not) monetary policies.

For all the system ills, however, he argued against proposing a fundamental reform of the system:

I shall be at once asked—Do you propose a revolution? Do you propose to abandon the one-reserve system, and create anew a many-reserve system? My plain answer is that I do not propose it. I know it would be childish. Credit in business is like loyalty in Government. You must take what you can find of it, and work with it if possible.

Bagehot admitted that it was not reasonable to try to shake the system, that it was (unfortunately) there to stay. The only pragmatic thing to do was to try to make it more efficient given the circumstances.

But what did he think was a good system then? (chapter 4):

Under a good system of banking, a great collapse, except from rebellion or invasion, would probably not happen. A large number of banks, each feeling that their credit was at stake in keeping a good reserve, probably would keep one; if any one did not, it would be criticised constantly, and would soon lose its standing, and in the end disappear. And such banks would meet an incipient panic freely, and generously; they would advance out of their reserve boldly and largely, for each individual bank would fear suspicion, and know that at such periods it must ‘show strength,’ if at such times it wishes to be thought to have strength. Such a system reduces to a minimum the risk that is caused by the deposit. If the national money can safely be deposited in banks in any way, this is the way to make it safe.

What Bagehot described is a ‘free banking’ system. This is a laissez faire-type banking system that involves no more regulatory constraints than those applicable to other industries, no central bank centralising reserves or dictating monetary policy, no government control and competitive currency issuance. No regulation? No central bank to adequately control the currency and the money supply and act as a lender of last resort? No government control? Surely this is a recipe for disaster! Well…no. There have been a few free banking systems in history, in particular in Scotland and Sweden in the 19th century, to a slightly lesser extent in Canada in the 19th and early 20th, and in some other locations around the world as well. Curiously (or not), all those banking systems were very stable and much less prone to crises than the central banking ones we currently live in. Selgin and White are experts in the field if you want to learn more. If free banking was so effective, why did it disappear? There are very good reasons for that, which I’ll cover in a subsequent post on the history of central banking.

I am not claiming that Bagehot held those views for his entire life though. A younger Bagehot actually favoured monopolised-currency issuance and the one-reserve system he decried in his later life. I am not even claiming that everything he said was necessarily right. But Bagehot as a defender of free banking and against regulatory requirements of all sort is a far cry from what most academics and regulators would like us to believe today. Personally, I find that, well, very ironic.

Financial innovation is back with a vengeance

What didn’t we hear about financial innovation throughout the crisis? Whereas innovation in general is good, financial innovation on the other hand was the worst possible thing coming out of a human mind. Paul Volcker, former Chairman of the Fed, famously declared that the ATM was the only useful financial innovation since the 1980s. Harsh.

True, some financial innovations are better than others. In particular, those used to bypass regulatory restrictions are more dangerous, not because they are intrinsically evil or anything, but simply because their often complex legal structure makes them opaque and difficult for external analysts and investors to analyse. This famous 2010 Fed paper attempted to map the shadow banking system (see picture), and usefully stated that not all shadow banking (and financial innovations) activities were dangerous (but those specifically designed to avoid regulations were). Ironically (and typically…) one of the first innovations to ever appear within the shadow banking system was money market funds. What was the rationale behind their creation? In the 1960s and 1970s in the US, interest payment on bank demand deposits was prohibited and capped on other types of deposits. The resulting financial repression through high inflation pushed financial innovators to come up with a way of bypassing the rule: money market funds became a deposit-equivalent that paid higher interests. Today we blame money market funds for being responsible for a quiet run on banks during the crisis, precipitating their fall. It would just be good to remember that without such stupid regulation in the first place, money market funds might have never existed…

The last decade has seen the growth of two particularly interesting innovations within the shadow banking system: one was relatively hidden (securitisation) while the other one grew in the spotlight (crowdfunding/peer-to-peer lending). One was deemed dangerous. The other one was more than welcome (ok, not in France). What had to happen happened: they are now combining their strength.

Various types of crowdfunding exist: equity crowdfunding, P2P lending, project financing… Today I’m going to focus on P2P lending only. What started as platforms enabling individuals to lend to other individuals are now turning into massive gates for complex institutional investors to lend to individuals and SMEs. Given the retreat of banks from the SME market (thank you Basel), various institutional investors (mutual and hedge funds, insurance firms) thought about diversifying their investments (and maximising their returns) by starting to offer loans to individuals and companies they normally can’t reach.

Basically, those funds had a few options: developing the capabilities to directly lend to those customers, investing in securitised portfolios of bank loans, or investing in securitised portfolios of P2P loans. The first option was very complex to implement and the required infrastructure would take a long time to develop. The second option had already existed for a little while, but was dependent on banks lending to customers, which current regulations limit due to higher capital requirements on such loans. The third option, on the other hand, allowed funds to maximise returns and attract more potential borrowers thanks to the reduction of the cost of borrowing by disintermediating banks. And funds could also strike deals with those still tiny online platforms that would have never happened with massive banks.

While securitisation sounds scary, it is actually only a simpler way of investing in loans of small sizes (the alternative being to invest in every single loan, some of them amounting to only USD500… Not only many funds don’t have the capability of doing such things, but many have also restrictions about the types of asset class and amounts they can invest in). Securitisation also bypasses Wall Street investment banks: funds directly invest in P2P loans, package them and sell them on to other investors while retaining a ‘tranche’ in the deal, which absorbs losses first. Now some entrepreneurs are even talking of setting up secondary markets to trade investments in loans, pretty much like a smaller version of the bond market.

Is this a welcome evolution for the P2P industry? I would say that it is a necessary evolution. It is once again a spontaneous development that merely reflects the need for funding of the P2P industry, which small retail investors cannot fulfil (unless all investment funds’ customers start withdrawing their money to directly invest in P2P, which is highly unlikely). Many start to think that large institutional investors will end up crowding out small retail investors. Possibly, but as long as regulation remains light, keeping barriers to entry low, new platforms only accepting retail investors could well appear if the demand is present.

All this is fascinating. Not only because technology and the internet enables new ways of channelling funds from savers to borrowers, but also because this is the growth of a parallel 100%-reserve banking system. The shadow banking system is effectively some version of a 100%-reserve banking. And it keeps growing through those various innovations. As I argued in a previous post, this may well have implications for monetary policy that current central banks and economists don’t take into account. A 100%-reserve banking system does not have a deposit multiplier and consequently does not have an elastic currency to respond to a sudden increase or decrease in the demand for money. However, such a system perfectly matches savers’ and borrowers’ intertemporal preferences, limiting malinvestments. Nonetheless, we for now remain in a mix system of 100% reserve (most of shadow banking) and fractional reserves (traditional banking). It would still be interesting to study the possible policy implications of a growth in the 100%-reserve part of the economy.

The Economist struggles with Wicksell

Looks like Wicksell is back in fashion. After years (decades?) with barely any mention of this distinguished Swedish economist outside of work from some heterodox economic schools academics (like the Austrians), he is now everywhere and has unleashed a great debate among academics and financial practitioners. This is the outcome of both the financial crisis (preceded by interest rates that were below their ‘natural’ level according to Wicksellian-based theories) and the current unconventional policies undertaken by central banks all over the world (that risk repeating the same mistakes according to those same theories).

This week’s Economist’s column Free Exchange tries to identify whether or not current interest rates are too low based on a Wicksellian framework (A natural long-term rate). The article is complemented by a Free Exchange blog post on the newspaper’s website.

I won’t get back to the definitions of Wicksell’s money and natural rates of interest as I’ve done it in two recent posts (here and here). I only wish today to comment on The Economist’s interpretation (and misconceptions) of the Wicksellian rate.

A few of things shocked me in this week’s column. First, the assertions that “the natural rate prevails when the economy is at full employment” and that “the natural interest rate is often assumed to be constant.” I’m sorry…what? Putting aside the fact that ‘full employment’ is hard to define, there can be full employment with interest rates below or above their natural level, and interest rates can be at their natural level with the economy not at full employment. Many other ‘real’ factors have effects on ‘full employment’. Using full employment as a basis for spotting the equilibrium rate is dangerous.

Second, where did they get that the natural interest rate was constant? This doesn’t make sense. The natural interest rate rises and decreases following a few variables (various economic schools of thought will have differing opinions) such as time preference (i.e. whether or not people prefer to use income for immediate or future consumption), marginal product of capital (demand for loanable funds by entrepreneurs would increase as long as they can make a profit on the marginal increase in capital stock, driving up the interest rate in the process), liquidity preference (i.e. whether or not people desire to hold money as cash rather than some other less liquid form of wealth – pretty much the only important factor driving the interest rate for Keynesians –)… As you can imagine, all those factors vary constantly, impacting the demand for money and the demand for credit and in turn the rate of interest. It clearly does not remain constant…

The Economist also dismisses the possibility that real interest rates are too low by the fact that sovereign bonds’ yields are low, not only in the US (where the Fed is engaged in massive bonds purchases), but also in other economies whose central banks are less active in purchasing sovereign debt. But it overlooks the fact that natural rates aren’t uniform and may well be lower in other countries (for example, the natural rate was probably lower in Germany than in Spain and Ireland before the crisis, despite having a common central bank). It also overlooks that ‘risk-free’ rates used as a basis of most financial calculations internationally are US Treasuries, not sovereign bonds of other countries.

Finally, in support of its point, the column argues that expected future low rates could also reflect investors’ expectations of sluggish future growth and that “despite profit margins near record levels and rock-bottom interest rates, business investment has been sluggish, recently peaking at just above 12% of GDP; it topped 14% in the late 1990s.” Once again, this is misinterpreting the natural rate: the level of the natural rate of interest does not necessarily depend on expected future economic growth as I described above. Sluggish business investments also are more likely to reflect current regulatory ‘regime uncertainty’ than entrepreneurs’ doubts about the future state of the economy. On top of that, using the dotcom bubble as a reference for business investment is intellectually dishonest. Moreover, the article contradicts itself starting with “central banks ignore this century-old observation at their peril” only to conclude that “all this suggests that policy rates, low as they seem, are not out of line with their natural level.” Hhhmmm, ok.

The Free Exchange blog post by Greg Ip is a little better but still overall quite confused and confusing. Interestingly, it cites a paper by Bill White (http://dallasfed.org/assets/documents/institute/wpapers/2012/0126.pdf) who argues that the sort of yield-chasing that we can witness in financial markets today is a symptom of nominal rates being lower than natural rates. Doesn’t this remind you of anything? That’s right; it was exactly my point in this post. But it then cites Brad de Long, who can be added to the list of people who don’t understand what regulatory uncertainty is, and who tries as a result to convince us that the natural rate is below zero. Theoretically, a below zero natural rate if possible in period of deflation. But it does not make much sense to have a natural rate below zero when inflation is above zero.

It is definitely a hard task to identify the natural rate of interest. Nonetheless, a few rules of thumb are sometimes better than overly-complex reasoning. Investors would be perfectly happy with negative nominal yields if cost of life was declining even faster. This is obviously not the case at the moment.

Should the Bank of England have tools to prick property bubbles?

The answer is no. (but not according to this FT article)

Wait… Actually, it already has tools: it’s called monetary policy. Place the interest rate at the right level and stop massively injecting cash in the economy and, perhaps, you won’t witness real estate bubbles?

There are other hugely distorting UK government policies at the moment: the Funding-for-Lending scheme and the more recent Help-to-Buy, which both push demand for property up through artificially low interest rates. I’ll explain that in details in another post.

So the question becomes: why adding other distorting tools (whether ‘macroprudential‘ or ‘microprudential‘) and policies, such as maximum loan-to-value or loan-to-income ratios, on top of already deficient tools and policies? I have another suggestion: why not trying to correct the failings of the first layer of policies? Just saying.

PS: Lord Turner is obviously mentioned in this FT article.

Recent Comments