Is the BIS on the Dark Side of macroeconomics?

The BIS has got a hobby: to annoy other economists and central bankers. It’s a good thing. It published its annual report about two weeks ago, and the least we can say is that it didn’t please many.

Gavin Davies wrote a very good piece in the FT last week, summarising current opposite views: “Keynesian Yellen versus Wicksellian BIS”. What’s interesting is that Davies views the BIS as representing the ‘Wicksellian’ view of interest rates: that current interest rates are lower than their natural level (i.e. monetary policy is ‘loose’ or ‘easy’). On the other hand, Scott Sumner and Ryan Avent seem to precisely believe the opposite: that current rates are higher than their natural level and that the BIS is mistaken in believing that low nominal rates mean easy money. This is hard to reconcile both views.

Neither is the BIS particularly explicit. Why does it believe that interest rates are low? Because their headline nominal level is low? Because their real level is low? Or because its own natural rates estimates show that central banks’ rates are low?

It is hard to estimate the Wicksellian ‘natural rate’ of interest. Some people, such as Thomas Aubrey, attempt to estimate the natural rate using the marginal product of capital theory. There are many theories of the rate of interest. Fisher (described by Milton Friedman as America’s best ever economist), Bohm-Bawerk, and Mises would argue that the natural interest rate is defined by time preference (even though they differ on details), and Keynes liquidity preference. Some economists, such as Miles Kimball, currently argue that the natural rate of interest is negative. This view is hard to reconcile with any of the theories listed above. Fisher himself declared in The Rate of Interest that interest rates in money terms cannot be negative (they can in commodity terms).

Unfortunately, and as I have been witnessing for a while now, Wicksell is very often misinterpreted, even by senior economists. The latest example is Paul Krugman, evidently not a BIS fan. Apart from his misinterpretation of Wicksell (see below), he shot himself in the foot by declaring (my emphasis):

Now, what about the BIS? It is arguing that central banks have consistently kept rates too low for the past couple of decades. But this is not a statement about the Wicksellian natural rate. After all, inflation is lower now than it was 20 years ago.

Given that we indeed got two decades of asset bubbles and crashes, it looks to me that the BIS view was vindicated…

Furthermore, in a very good post, Thomas Aubrey corrects some of those misconceptions:

The second issue to note is that when the natural rate is higher than the money rate there is no necessary impact on the general price level. As the Swedish economist Bertie Ohlin pointed in the 1930s, excess liquidity created during a Wicksellian cumulative process can flow into financial assets instead of the real economy. Hence a Wicksellian cumulative process can have almost no discernible impact on the general price level as was seen during the 1920s in the US, the 1980s in Japan and more recently in the credit bubble between 2002-2007.

(Bob Murphy also wrote a very good post here on Krugman vs. Wicksell)

But there are other problematic issues. First, inflation (as defined by CPI/RPI/general increase in the price level) itself is hard to measure, and can be misleading. Second, as I highlighted in an earlier post, wealthy people, who are the ones who own most investible assets, experience higher inflation rates. In order to protect their wealth from declining through negative real returns (what Keynes called the ‘euthanasia of the rentiers’), they have to invest it in higher-yielding (and higher-risk) assets, causing bubbles is some asset classes (while expectations that central bank support to asset prices will remain and allow them to earn a free lunch, effectively suppressing risk-aversion).

If natural rates were negative – or at least very low – and the environment deflationary, it is unlikely that we would witness such hunt for yield: people care about real rates, not nominal ones (though in the short-run, money illusion can indeed prevail). But this is not only an ultra-rich problem: there are plenty of stories of less well-off savers complaining of reduced purchasing power.

Meanwhile, the rest of the population and overleveraged companies, supposedly helped by lower interest rates, seem not to deleverage much: overall debt levels either stagnate or even increase in most economies, as the BIS pointed out.

Banks also suffer from the combination of low rates* and higher regulatory requirements that continue to pressurise their bottom line, and have ceased to pass lower rates on to their customers.

In this context, the BIS seems to have a point: rates may well be too low. Current interest rate levels seem to only prevent the reallocation of capital towards more economically efficient uses, while struggling banks are not able to channel funds to productive companies.

Critics of the BIS point to their call to rise rates to counter inflation back in 2011. Inflation, as conventionally measured, indeed hasn’t stricken in many countries. In the UK and some other European countries though, complaints about quickly rising prices and falling purchasing power have been more than common (and I’m not even referring to house price inflation). This mismatch between aggregate inflation indicators and widespread perception is a big issue, which underlies financial risk-taking.

In the end, Keynes’ euthanasia of the rentiers only seem to prop up dying overleveraged businesses and promote asset bubbles (and financial instability) as those rentiers pile in the same asset classes. I side with the BIS in believing this is not a good and sustainable policy.

I also side with the BIS and with Mohamed El-Erian in believing in the poor forecasting ability of most central bankers, who seem to constantly display a dovish view of the economy, which apparently experiences never-ending ‘slack’, as well as the very uncertain effect of macro-prudential policies, which cannot and will not get in all the cracks. Nevertheless, many mainstream economists and economic publications seem to be overconfident in the effectiveness of macro-prudential policies (see The Economist here, Yellen here, Haldane here, who calls macropru policies “targeted lightning strikes”…).

While central banks’ rates should probably already have risen in several countries (and remain low in others, hence the absurdity of having a single monetary policy for the whole Eurozone), everybody should keep the BIS warnings in mind: after all, they were already warning us before the financial crisis, yet few people listened and many laughed at them.

Unfortunately, politicians and regulators have repeated some of the mistakes made during the Great Depression: they increased regulation of business and banking while the economy was struggling. I have many times referred to the concept of regulatory uncertainty, as well as the over-regulation that most businesses are now subject to (in the US at least, though this is also valid in most European countries). Businesses complaints have been increasing and The Economist reported on that issue last week.

In the meantime, while monetary policy has done (almost) everything it could to boost credit growth and to prevent the money supply from collapsing, harsher banking regulation has been telling banks to do the exact opposite: raise capital, deleverage, and don’t take too much risk.

In the end, monetary policy cannot fix those micro-level issues. It is time to admit that we do not live in the same microeconomic environment as before the crisis. What about cutting red tape to unleash growth rather than risk another financial crisis?

* Yes, for banks, rates are low, whichever way you look at them. Banks can simply not function by earning zero income on their interest-earning assets (loan book and securities portfolio).

PS: Noah Smith, another member of the anti-BIS crowd, has a nonsense ‘let’s keep interest rate low forever’-type article here: raising interest rates would lead to an asset price crash, so we should keep them low to have a crash later. Thanks Noah. The way he describes a speculative bubble is also wrong (my emphasis):

The theory of speculation tells us that bubbles form when people think they can find some greater fool to sell to. But when practically everyone is convinced that asset prices are relatively high, like now, it’s pretty obvious that there aren’t many greater fools out there.

Really? No, speculation involved buying as long as you believe you can get the right timing to exit the position. Even if everyone believed that asset prices were overvalued, as long as investors expect prices to continue to increase, speculation would continue: profits can still be made by exiting on time, even if you join the party late.

PPS: A particularly interesting chart from the BIS report was the one below:

It is interesting to see how coordinated financial cycles have become. Yet the BIS seems not to be able to figure out that its own work (i.e. Basel banking rules) could well be the common denominator of those cycles (which were rarely that synchronised in the past).

It is interesting to see how coordinated financial cycles have become. Yet the BIS seems not to be able to figure out that its own work (i.e. Basel banking rules) could well be the common denominator of those cycles (which were rarely that synchronised in the past).

The era of the neverending bubble?

The IMF got the timing right. It published last week a new ‘Global Housing Watch‘, and warned that house prices were way above trend in a lot of different countries all around the world. The FT also reports here:

The world must act to contain the risk of another devastating housing crash, the International Monetary Fund warned on Wednesday, as it published new data showing house prices are well above their historical average in many countries.

As I said, perfect timing, as this announcement follows my previous post on the influence of Basel’s RWAs on mortgage lending.

As long as international banking authorities don’t get rid of this mechanism, we are likely to experience reoccuring housing bubbles with their devastating economic effects (hint for Piketty: and investors/speculators will have an easy life making capital gains).

PS: I am on holidays until the end of the week, so probably not many updates over the next few days.

The (negative) mechanics of negative ECB deposit rates

The ECB has finally announced last week that it would be lowering its main refinancing rate from 0.25% to 0.15%, and that it would lower the rate it pays on its deposit facility from 0% to -1%. The ECB hopes to incentivise banks to take money out of that facility and lend it to customers*, providing a boost to the broad money supply and counteracting deflation risks.

The interest rate of the ECB deposit facility is supposed to help the central bank define a floor under which the overnight interbank lending rate (EONIA) should not go. The reason is that deposits at the ECB are supposedly risk-free (or at least less risky than placing the money anywhere else). Consequently, banks would never place money (i.e. excess reserves) at another bank/ investment (which involves credit risk) for a lower rate. When the deposit facility rate is high, banks are incentivised to reduce their interbank lending exposures and leave their money at the ECB (and vice versa). On the other hand, the main refinancing rate is supposed to represent an upper boundary to the interbank lending rates: theoretically, banks should not borrow from another bank at a higher rate than what it would pay at the ECB. In practice, this is not exactly true, as banks do their best to avoid the stigma associated with borrowing from the central bank.

Unfortunately, there is a fundamental microeconomic reason why banks cannot diminish their lending rate indefinitely. I have already described how banks are not able to transmit interest rates lower than a certain threshold to their customers due to the margin compression effect (see also here). Indeed, banks’ net interest income must be able to cover banks’ fixed operating costs for the bank to remain profitable from an accounting point of view. When rates drop below a certain level, banks have to reprice their loan book by increasing the spread above the central bank rate on the marginal loans they make, breaking the transmission mechanism of the lending channel of monetary policy. As we have already seen, in the UK, that threshold seems to be around 2%.

But the same thing seems to happen in other European countries. This is Ireland (enlarge the charts)**:

We can notice the margin compression effect on the first chart. The lending rate stops dropping despite the ECB rate falling as banks reprice their lending upward to re-establish profitability (evidenced from the second chart, where interest rates on new lending increase rather than decrease).

This is France:

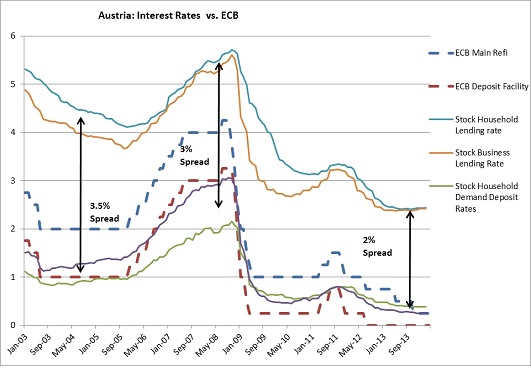

This is Austria:

Clearly, what happens in the UK regarding margin compression also occurs in those countries. When the ECB rate dropped, outstanding floating rate lending rates also dropped (because floating rate lending is indexed on either the ECB base rate or on Euribor), causing pressure on revenues. As long as deposit rates could also fall (this varies a lot by country, as French banks never pay anything on demand deposits), the loss in interest income was offset by reduced interest expense. But once deposit rates reached 0 and couldn’t fall any lower, banks in those countries experienced margin compression and their net interest income started to suffer. Moreover, this happened exactly when loan impairment charges peaked because of increased credit risk.

Banks in emerging countries have constantly high non-performing loans ratios. But they still manage to remain (often highly) profitable by maintaining very high net interest income and margins. In Western Europe, banks saw their net profits all but disappear with rates dropping that low. As a result, it is likely that the new ECB rate cut won’t affect lending rates much…

Nonetheless, the ECB had been trying to revive, or encourage, interbank lending throughout most of the crisis, and had already lowered to its deposit rate to 0%. Nevertheless, banks maintained cash in those accounts. Why would a bank leave its money in an account that pays 0%? Because banks adjust those interest rates for risk. An ECB risk-adjusted 0% can be worth more than a risk-adjusted 4% interbank deposit at a zombie/illiquid/insolvent bank. However, the ECB is clearly not satisfied with the situation: it now wants banks to take their money out of the facility and lend it to the ‘real economy’.

How do the combination of low refi rate and negative ECB deposit rates impact banks? Let’s remember banks’ basic profit equations:

Accounting Profit = II – IE – OC, and Economic Profit = II – IE – OC – Q

where II represents interest expense, IE interest income, OC operating costs (which include impairment charges on bad debt), and Q liquidity cost.

For a bank to remain economically profitable (or even viable in the long-term), the rate of economic profit must be at least equal to the bank’s cost of equity.

To maximise their economic profits, banks look for the most-profitable risk-adjusted lending opportunities. ‘Lending’ to the ECB is one of those opportunities. Placing money at the ECB generates interest income. This interest income is more than welcome to (at least) maintain some level of accounting profitability (though not necessarily economic profitability) when economic conditions are bad and income from lending drops while impairment charges jump***.

With deposit rates at 0, banks’ income became fully constrained by financial markets and the economy. With rates in negative territory, not only banks see their interest income vanish but also their interest expense increase. From the equations above, it is clear that it makes banks less profitable****. On top of that, lending that cash can make banks less liquid, which increases their riskiness and elevates their cost of capital (the ‘Q’ above). The question becomes: adjusted for credit and liquidity risk, is it still worth keeping that cash at the ECB? The answer is probably yes.

(unless banks find worthwhile investments outside of the Eurozone, which wouldn’t be of much help to prop up Euro economies…)

To summarise, ‘II’ is negatively impacted by a low base rate whereas ‘IE’ reaches a floor (= margin compression). ‘IE’ then increases when the central bank deposit rate turns negative. Meanwhile, ‘OC’ increases as loan impairment charges jump due to heightened credit risk. Profitability is depressed, partly due to the central bank’s decisions.

Many European banks aren’t currently lending because they are trying to implement new regulatory requirements (which makes them less profitable) in the middle of an economic crisis (which… also makes them less profitable). As a result, the ECB measures seem counterproductive: in order to lend more, banks need to be economically profitable. Healthy banks lend, dying ones don’t.

The ECB is effectively increasing the pressure on banks’ bottom line, hardly a move that will provide a boost to lending. The only option for banks will be to cut costs even further. And when a bank cut costs, it effectively reduces its ability to expand as it has less staff to monitor lending opportunities, and consequently needs to deleverage. Once profitability is re-established, hiring and lending could start growing again.

A counterintuitive (and controversial) approach to provide a boost to lending would be to subsidise even more the banking sector by increasing interest rates on both the refinancing and deposit facilities.

Defining the appropriate level of interest rates would be subtle work though: struggling over-indebted households and businesses may well start defaulting on their debt. On the other hand banks’ revenues would increase as margin compression disappears, making them able to lend more eventually. The subtle balance would be achieved when interest income improvements more than offset credit losses increases. Not easy to achieve, but pushing rates ever lower is likely to cripple the banking system ever more and reduce lending in proportion (while allowing zombie firms to survive).

Furthermore, banks are repricing their loan book upward anyway, making the ECB rate cuts pointless. The process takes time though and it would be better for banks to rebuild their revenue stream sooner than later. The ECB could still use other monetary tools to influence a range of interest rates and prices through OMO and QE measures, which would be less disruptive to banks’ margins.

Finally, the ECB has launched its own-FLS style ‘TLTRO’, a scheme that provides cheap funding to banks if they channel the funds to businesses. Similarly to the BoE’s FLS, I believe such scheme suffers from delusion. Banks are currently deleveraging to lower their RWAs in order to comply with the harsher capital requirements of Basel 3. If there is one thing banks want to avoid, it is to lend to RWA-dense customers such as SMEs… (and instead focus on better RWA/risk-adjusted profitable lending such as… mortgages). Banks can also already extract relatively low wholesale funding rates by issuing secured funding instruments such as covered bonds. (UPDATE: see this follow-up post on that topic)

* This does not mean that banks would ‘lend out’ money to customers, unless they withdraw it as cash. But by increasing lending, absolute reserve requirements increase and banks have to transfer money from the deposit facility to the reserve facility.

** Data comes from respective central banks. They are not fully comparable. I gathered data from many different Eurozone countries, but unfortunately, some central banks don’t provide the data I need (or the statistics database doesn’t work, as in Italy…). Spreads are approximate ones calculated between the middle point of deposit rates and the middle point of lending rates. Analysis is very superficial, and for a more comprehensive methodology please refer to my equivalent posts on the UK/BoE.

*** Don’t get me wrong though. Fundamentally speaking, I am not in favour of such central bank mechanisms as I believe this is akin to a subsidy that distorts banks’ risk-taking behaviour. In a central banking environment, like Milton Friedman I’d rather see the central bank manipulate interest rates solely through OMO-type operations.

**** Of course this remains marginal. But in crisis times, ‘marginal’ can save a bank. Let’s also not forget booming litigation charges, currently estimated at USD104Bn… Evidently making it a lot easier for banks to lend as you can imagine…

News digest: P2P lending and HFT, CoCo bonds, Co-op Bank…

Ron Suber, President at Prosper, the US-based P2P lending company, sent me a very interesting NY Times article a few days ago. The article is titled “Loans That Avoid Banks? Maybe Not.” This is not really accurate: the article indeed mentions institutional investors such as mutual and hedge funds increasingly investing in bundles of P2P loans through P2P platforms, but never refers to banks. Unlike what the article says, I don’t think platforms were especially set up to bypass institutional investors… They were set up to bypass banks and their costly infrastructure and maturity transformation.

Some now fear that the industry won’t be ‘P2P’ for very long as institutional investors increasingly take over a share of the market. I think those beliefs are misplaced. Last year, I predicted that this would create opportunities for niche players to enter the market, focusing on real ‘P2P’.

A curious evolution is the application of high-frequency trading strategies to P2P. I haven’t got a lot of information about their exact mechanisms, but I doubt they would resemble the ones applied in the stock market given that P2P is a naturally illiquid and borrower-driven market.

The main challenge of the industry at the moment seems to be the lack of potential customer awareness. Despite offering better deals (i.e. cheaper borrowing rates) than banks, demand for loans remains subdued and the industry tiny next to the banking sector.

In this FT article, Alberto Gallo, head of macro-credit research at RBS, argues that regulators should intervene on banks’ contingent convertible bonds’ risks. I think this is strongly misguided. Investors’ learning process is crucial and relying on regulators to point out the potential risks is very dangerous in the long-term. Not only such paternalism disincentives investors to make their own assessment, but also regulators have a very bad track record at spotting risks, bubbles and failures (see Co-op bank below).

This piece here represents everything that’s wrong with today’s banking theory:

We know that a combination of transparency, high capital and liquidity requirements, deposit insurance and a central bank lender of last resort can make a financial system more resilient. We doubt that narrow banking would.

Not really… They also argue that 100% reserve banking would not prevent runs on banks:

The mutual funds of the narrow banking world would be subject to the same runs. Indeed, recent research highlights that – in the presence of small investors – relatively illiquid mutual funds are more likely to face exit in the event of past bad performance. […] Since the mutual funds would be holding illiquid loans – remember, they are taking over functions of banks – collective attempts at liquidation to meet withdrawal requests would lead to ruinous fire sales.

They misunderstand the purpose of such a banking system. Those ‘mutual funds’ would not be similar to the ones we currently have, which invests in relatively liquid securities on the stock market, and can as a result exit their positions relatively quickly and easily. Those 100% reserve funds would invest in illiquid loans and investors in those funds would have their money contractually locked in for a certain time. With no legal power to withdraw, no risk of bank run.

The FT reported a few days ago the results of the investigation on the Co-operative bank catastrophe. Despite regulators not noticing any of the problems of the bank, from corporate governance to bad loans and capital shortfall, as well as approving unsuitable CEOs and mergers, the report recommends to… “heed regulatory warnings.” I see…

The impossible sometimes happens: I actually agree with Paul Krugman’s last week piece on endogenous money. No guys, the BoE paper didn’t reveal any mystery of banking or anything…

Finally, Chris Giles wrote a very good article in the FT today, very clearly highlighting the contradictions in the Bank of England policies and speeches, and their tendency to be too dovish whatever the circumstances:

Mark Carney, the governor, certainly displays dovish leanings. Before he took the top job, he said monetary policy could be tightened once growth reached “escape velocity”. But now that growth has shot above 3 per cent, he advocates waiting until the economy has “sustained momentum” – without acknowledging that his position has changed. His attitude to prices also betrays a knee-jerk dovishness. When inflation was above target, he stressed the need to look at forecasts showing a more benign period ahead. Now that inflation is lower it is apparently the short-term data that matters – and it justifies stimulus.

So much for forward guidance… Time to move to a rule-based monetary policy?

Greenspan put, Draghi call? (guest post by Vaidas Urba)

(This is a monetary economics guest post by Vaidas Urba, a market monetarist from Lithuania. He has previously appeared at The Insecurity Analyst blog and TheMoneyIllusion. You can follow him on Twitter here)

Greenspan put, Bernanke put – everybody uses these expressions half-jokingly to describe monetary policy and asset prices. Ricardo Caballero and Emmanuel Farhi have proposed a very serious classification of policy tools, distinguishing between monetary puts and calls. According to Caballero and Farhi, policy puts support the economy in bad states of the world, while policy calls support the economy in good states of world. There is much to disagree with in their “Safety Traps and Economic Policy” paper, but their definition of policy puts and calls is very useful.

QE1 and ARRA stimulus in 2009 are examples of policy puts. On the other hand, QE3 and Evans rule are primarily policy calls. Evans rule supported expectations of low interest rates in good states of the world, while QE3 compressed the term premium by reducing the risk of bond market volatility during the recovery. Policy calls are riskier than policy puts. Evan’s rule increased the risk of suboptimally low interest rates during late stages of recovery, while QE3 increased the risk of losses in Fed’s portfolio. Indeed, on March 1, 2013 Bernanke indicated that the estimated treasury term premium is negative. The Fed has walked back from policy calls. Tapering has restored the bond term premium to more normal levels, and the Fed has replaced the Evans rule with a more vague guidance. Bernanke call was replaced by Yellen put.

The Fed has used both monetary puts and calls, but the ECB has never used policy calls, and is not planning to use them. The policy of the ECB was a succession of impressive policy puts. Temporary liquidity injection in August 2007 has addressed the liquidity panic. Full allotment in October 2008 has placed a floor on the functioning of euro and dollar money markets. Three year LTROs in 2011 have prevented Greece’s default from becoming Lehman II. OMTs are out-of the money policy puts – they were never activated. Forward guidance is a policy put too, the ECB describes it as being all about “subdued outlook for inflation and broad-based weakness of the economy”, and low rates are signalled in bad states of the world without affecting interest rate expectations in good states of the world.

On further weakness the ECB is likely to start QE. Executive Board member Benoit Coeure has recently given us a glimpse of likely modalities of QE in his “Asset purchases as an instrument of monetary policy” speech. Coeure has stressed the continuity of ECB’s approach, he also said that “asset purchases in the euro area would not be about quantity, but about price”, and the ECB will use the yardstick of “the observable effect of our operations on term premia”. Presumably, the intent of QE will be to reduce term premia that are unduly high (policy put), and not to recreate boom conditions in financial markets by driving term premia to excessively low levels (policy call).

The Eurozone economy is very far away from any sensible macro equilibrium, and monetary call would be a very sensible step to take. Unfortunately, a blocking minority exists for any explicit decision. However, Draghi could communicate an implicit policy call by signalling the existence of majority coalition which would block a premature interest rate increase. The rate hike of 2011 was unanimous, so the bar is high for any such communication. Draghi’s talk of “plenty of slack” is a step to the right direction, but stronger and clearer words are needed to persuade the markets that ECB’s reaction function has changed unrecognizably since 2011.

A central banker contradiction?

Last week, Mark Carney, the governor of the Bank of England, was at Cass Business School in London for the annual ‘Mais Lecture’. Coincidentally, I am an alumnus of this school. And I forgot to attend… Yes, I regret it.

Carney’s speech was focused on past, current, and future roles of the BoE. In particular, Carney mentioned the now famous monetary and macroprudential policies combination. It’s a classic for central bankers nowadays. They all have to talk about that.

In January, Andrew Haldane, a very wise guy and one my ‘favourite’ regulators, also from the BoE, made a whole speech about the topic. As Jens Weidmann, president of the Bundesbank, did in February.

I am not going to come back to the all the various possible problems caused and faced by macroprudential policies (see here and here). However, there seems to be a recurrent contradiction in their reasoning.

This is Carney:

The transmission channels of monetary and prudential policy overlap, particularly in their impact on banks’ balance sheets and credit supply and demand – and hence the wider economy. Monetary policy affects the resilience of the financial system, and macroprudential policy tools that affect leverage influence credit growth and the wider economy. […]

The use of macroprudential tools can decrease the need for monetary policy to be diverted from managing the business cycle towards managing the credit cycle. […]

That co-ordination, the shared monitoring of risks, and clarity over the FPC’s tools allows monetary policy to keep Bank Rate as low as necessary for as long as appropriate in order to support the recovery and maintain price stability. For example expectations of the future path of interest rates – and hence longer-term borrowing costs – have not risen as the housing market has begun to recover quickly.

First, it is very unclear from Carney’s speech what the respective roles of monetary policy and macroprudential policies are. He starts by saying (above) that “monetary policy affects the resilience of the financial system”, then later declares “macroprudential policy seeks to reduce systemic risks”, which is effectively the same thing. At least, he is right: both policy frameworks overlap. And this is the problem.

This is Haldane:

In the UK, the Bank of England’s Monetary Policy Committee (MPC) has been pursuing a policy of extra-ordinary monetary accommodation. Recently, there have been signs of renewed risk-taking in some asset markets, including the housing market. The MPC’s macro-prudential sister committee, the Financial Policy Committee (FPC), has been tasked with countering these risks. Through this dual committee structure, the joint needs of the economy and financial system are hopefully being satisfied.

Some have suggested that having monetary and macro-prudential policy act in opposite directions – one loose, the other tight – somehow puts the two in conflict [De Paoli and Paustian, 2013]. That is odd. The right mix of monetary and macro-prudential measures depends on the state of the economy and the financial system. In the current environment in many advanced economies – sluggish growth but advancing risk-taking – it seems like precisely the right mix. And, of course, it is a mix that is only possible if policy is ambidextrous.

Contrary to Haldane, this does absolutely not look odd to me…

Let’s imagine that the central bank wishes to maintain interest rates at a low level in order to boost economic activity after a crisis. After a little while, some asset markets start looking ‘frothy’ or, as Haldane says, there are “renewed signs of risk-taking.” Discretionary macroprudential policy (such as increased capital requirements) is therefore utilised to counteract the lending growth that drives those asset markets. But there is an inherent contradiction here: one of the goals that low interest rates try to achieve is to boost lending growth to stimulate the economy…whereas macroprudential policy aims at…reducing it. Another contradiction: while low interest rates tries to prevent deflation from occurring by promoting lending and thus money supply growth, macroprudential policy attempts to reduce lending, with evident adverse effects on money supply and inflation…

Central bankers remain very evasive about how to reconcile such goals without entirely micromanaging the banking system.

I guess that the growing power of central bankers and regulators means that, at some point, each bank will have an in-house central bank representative that tells the bank who to lend to. For social benefits of course. All very reminiscent of some regions of the world during the 20th century…

Weidman is slightly more realistic:

We have to acknowledge that in the world we live in, macroprudential policy can never be perfectly effective – for instance because safeguarding financial stability is complicated by having to achieve multiple targets all at the same time.

Indeed.

Photograph: Intermonk

Could P2P Lending help monetary policy break through the ‘2%-lower bound’?

The ‘cut the middle man’ effect of P2P lending is already celebrated for offering better rates to both lenders and borrowers. But what many people miss is that this effect could also ease the transmission mechanism of central banks’ monetary policy.

I recently explained that the banking channel of monetary policy was limited in its effects by banks’ fixed operational costs. I came up with the following simplified net profit equation for a bank that only relies on interest income on floating rate lending as a source of revenues:

Net Profit = f1(central bank rate) – f2(central bank rate) – Costs, with

f1(central bank rate) = interest income from lending

= central bank rate + margin and,

f2(central bank rate) = interest expense on deposits

= central bank rate – margin

(I strongly advise you to take a look at the details here, which was a follow-up to my response to Ben Southwood’s own response on the Adam Smith Institute blog to my original post…which was also a response to his own original post…)

Consequently, banks can only remain profitable (from an accounting point of view) if the differential between interest income and interest expense (i.e. the net interest income) is greater than their operational costs:

Net interest income >= Costs

When the central bank base rate falls below a certain threshold, f2 reaches zero and cannot fall any lower, while f1 continues to decrease. This is the margin compression effect.

Above the threshold, the central bank base rate doesn’t matter much. Below, banks have to increase the margin on variable rate lending in order to cover their costs. This was evidenced by the following charts:

As the UK experience seems to show, banks stopped passing BoE rate cuts on to customers around a 2% BoE rate threshold. I called this phenomenon the ‘2%-lower bound’. I have yet to take a look at other countries.

Enter P2P lending.

By directly matching savers and borrowers and/or slicing and repackaging parts of loans, P2P platforms cut much of banks’ vital cost base. P2P platforms’ online infrastructure is much less cost-intensive than banks’ burdensome branch networks. As a result, it is well-known that both P2P savers and borrowers get better rates than at banks, by ‘cutting the middle man’. This is easy to explain using the equations described above, as costs approach zero in the P2P model. This is what Simon Cunningham called “the efficiency of Peer to Peer Lending”. As Simon describes:

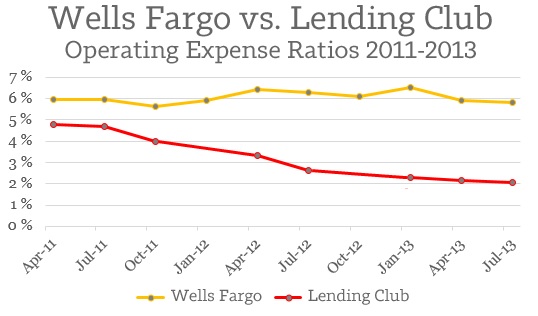

Looking purely at the numbers, Lending Club does business around 270% more efficiently than the comparable branch of a major American bank

Simon calculated the ‘efficiency’ of each type of lender by dividing the outstanding loans of Wells Fargo and Lending Club by their respective operational expenses (see chart below). I believe Lending Club’s efficiency is still way understated, though this would only become apparent as the platform grows. The marginal increase in lending made through P2P platforms necessitates almost no marginal increase in costs.

Perhaps P2P platforms’ disintermediation model could lubricate the banking channel of monetary policy the closer central banks’ base rate gets to the zero bound?

Possibly. From the charts above, we notice that the spread between savings rates and lending rates that banks require in order to cover their costs range from 2 to 3.5%. This is the cost of intermediation and maturity transformation. Banks hire experts to monitor borrowers and lending opportunities in-house and operate costly infrastructures as some of their liabilities (i.e. demand deposits) are part of the money supply and used by the payment system.

However, disintermediated demand and supply for loanable funds are (almost) unhampered by costs. As a result, the differential between borrowers and savers’ rate can theoretically be minimal, close to zero. That is, when the central bank lowers its target rate to 0%, banks’ deposit rates and short-term government debt yield should quickly follow. Time deposits and longer-dated government debt will remain slightly above that level. Savers would be incentivised to invest in P2P if the proposed rate at least matches them, adjusting for credit risk.

Let’s take an example: from the business lending chart above, we notice that business time deposit rates are currently quoted at around 1%. However, business lending is currently quoted at an average rate of about 3%. Banks generate income from this spread to pay salaries and other fixed costs, and to cover possible loan losses. Let’s now imagine that companies deposit their money in a time deposit-equivalent P2P product, yielding 1.5%. Theoretically, business lending could be cut to only slightly above 1.5%. This represents a much cheaper borrowing rate for borrowers.

P2P platforms would thus more closely follow the market process: the law of supply and demand. If most investments start yielding nothing, P2P would start attracting more investors through arbitrage, increasing the supply of loanable funds, and in turn lowering rates to the extent that they only cover credit risk.

The only limitation to this process stems from the nature of products offered by platforms. Floating rate products tend to be the most flexible and quickly follow changes in central banks’ rates. Fixed rate products, on the other hand, take some time to reprice, introducing a time lag in the implementation of monetary policy. I believe that most P2P products originated so far were fixed rate, though I could not seem to find any source to confirm that.

In the end, P2P lending is similar to market-based financing. The bond market already ‘cuts the middle man’, though there remains fees to underwriting banks, and only large firms can hope to issue bonds on the financial markets. In bond markets, investors exactly earn the coupon paid by borrowers. There is no differential as there is no middle man, unlike in banking. P2P platforms are, in a way, mini fixed-income markets that are accessible to a much broader range of borrowers and investors.

However, I view both bond markets and P2P lending as some version of 100%-reserve banking. While they could provide an increasingly large share of the credit supply, banks still have a role to play: their maturity transformation mechanism provides customers with a means of storing their money and accessing it whenever necessary. Would P2P platform start offering demand deposit accounts, their cost base would rise closer to that of banks, potentially raising the margin between savers and borrowers as described above.

It seems that, by partly shifting from the banking channel to the P2P channel over time, monetary policy could become more effective. I am sure that Yellen, Carney and Draghi will appreciate.

Is the zero lower bound actually a ‘2%-lower bound’?

Following my recent reply to Ben Southwood on the relationship between mortgage rates, BoE base rate and banks’ margins and profitability (see here and here), a question came to my mind: if the BoE rate can fall to the zero lower bound but lending rates don’t, should we still speak of a ‘zero lower bound’? It looks to me that, strictly in terms of lending and deposit rates, setting the base rate at 0% or at 2% would have changed almost nothing at all, at least in the UK.

The culprit? Banks’ operational expenses. Indeed, it looks like the only way to break through the ‘2%-lower bound’ would be for banks to slash their costs…

Let’s take a look at the following mortgage rates chart from one of my previous posts:

From this chart, it is clear that lowering the BoE rate below around 2.5% had no further effect on lowering mortgage rates. As described in my other posts, this is because banks’ net interest income necessarily has to be higher than expenses for them to remain profitable. When the BoE rate falls below a certain threshold that represents operational expenses, banks have to widen the margins on loans as a result.

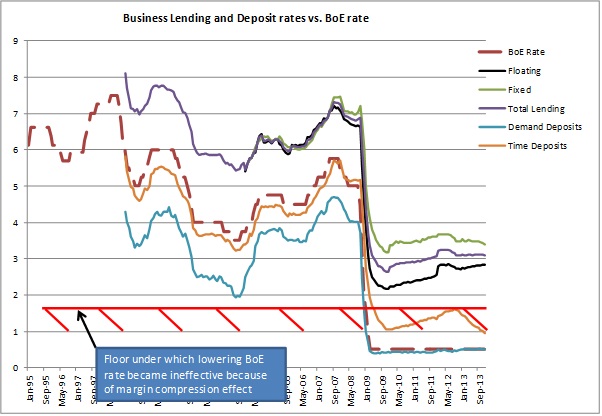

What about business lending rates? Since business lending is funded by both retail and corporate deposits (and excluding wholesale funding for the purpose of the exercise), the analysis must take a different approach. Banks don’t often disclose the share of corporate deposits within their funding base, but I managed to find a retail/corporate deposit split of 75%/25% at a large European peer, which I am going to use as a rough approximation to estimate banks’ business lending margins. Here are the results of my calculations (first chart: margin over time deposits, second chart: margin over demand deposits):

No surprise here, the same margin compression effect appears as a result of the BoE rate collapsing (as well as Libor, as floating corporate lending is often calculated on a Libor + margin basis, unlike mortgages, which are on a BoE + margin basis). Before that period, changes in the BoE and Libor rates had pretty much no effect on margins. After the fall, banks tried to rebuild their margins by progressively repricing their business loan books upward (i.e. increasing the margins over Libor).

No surprise here, the same margin compression effect appears as a result of the BoE rate collapsing (as well as Libor, as floating corporate lending is often calculated on a Libor + margin basis, unlike mortgages, which are on a BoE + margin basis). Before that period, changes in the BoE and Libor rates had pretty much no effect on margins. After the fall, banks tried to rebuild their margins by progressively repricing their business loan books upward (i.e. increasing the margins over Libor).

Here again we can identify a 1.5% BoE rate floor, under which lowering the base rate does not translate into cheaper borrowing for businesses:

This has repercussions on monetary policy. The banking/credit channel of monetary policy aims at: 1. easing the debt burden on indebted household and businesses and, 2. stimulating investments and consumption by making it cheaper to borrow. However, it seems like this channel is restricted in its effectiveness by banks’ ability in passing the lower rate on to customers. Banks’ short-term fixed cost base effectively raises the so-called zero lower bound to around 2%. The only way to make the transmission mechanism more efficient would be for banks to drastically improve their cost efficiency and have assets of good-enough quality not to generate impairment charges, which is tough in crisis times. Unfortunately, there are limits to this process, and a bank without employee and infrastructure is unlikely to lend in the first place…

Don’t get me wrong though, I am not saying that lowering the BoE rate (and unconventional monetary policies such as QE) is totally ineffective. Lowering rates also positively impact asset prices and market yields, ceteris paribus. This channel could well be more effective than the banking one but it isn’t the purpose of this post to discuss that topic. Nevertheless, from a pure banking channel perspective, one could question whether or not it is worth penalising savers in order to help borrowers that cannot feel the loosening.

PS: I am not aware of any academic paper describing this issue, so if you do, please send me the link!

A clarification on mortgage rates for ASI’s Ben Southwood

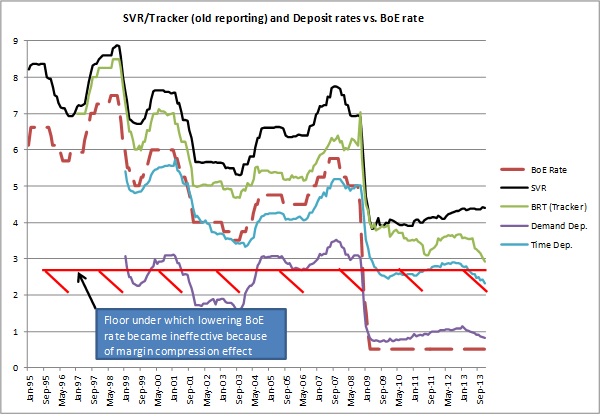

Ben Southwood from the Adam Smith Institute replied to my previous post here. I am still confused about Ben’s claim that the spread varied “widely”. As the following chart demonstrates, the margins of SVR, tracker and total floating lending over the BoE base rate remained remarkably stable between 1998 and 2008, despite the BoE rate varying from a high 7.5% in 1998 to a low of 3.5% in 2003:

Everything changed in 2009 when the BoE rate collapsed to the zero lower bound. Following his comments, I think I need to address a couple of things. Two particular points attracted my attention. Ben said:

If other Bank schemes, like Funding for Lending or quantitative easing were overwhelming the market then we’d expect the spread to be lower than usual, not much higher.

His second big point, that the spread between the Bank Rate and the rates banks charged on markets couldn’t narrow any further 2009 onwards perplexes me. On the one hand, it is effectively an illustration of my general principle that markets set rates—rates are being determined by banks’ considerations about their bottom line, not Bank Rate moves. On the other hand, it seems internally inconsistent. If banks make money (i.e. the money they need to cover the fixed costs Julien mentions) on the spread between Bank Rate and mortgage rates (i.e. if Bank Rate is important in determining rates, rather than market moves) then the absolute levels of the numbers is irrelevant. It’s the spread that counts.

It looks to me that we are both misunderstanding each other here. It is indeed the spread that counts. But the spread over funding (deposit) cost, not BoE rate! (Which seems to me to be consistent with my posts on MMT/endogenous money.) Let me clarify my argument with a simple model.

Assumptions:

- A medium-size bank’s only assets are floating rate mortgages (loan book of GBP1bn). Its only source of revenues is interest income. The bank maintains a fixed margin of 1% above the BoE rate but keeps the right to change it if need be.

- The bank’s funding structure is composed only of demand deposits, for which the bank does not pay any interest. As a result, the bank has no interest expense.

- The bank has a 100% loan/deposit ratio (i.e. the bank has ‘lent out’ the whole of its deposit base and therefore does not hold any liquid reserve).

- The bank has an operational cost base of GBP20m that is inflexible in the short-term (not in the long-term though there are upwards and downwards limits) and no loan impairment charge.

Of course this situation is unrealistic. A 100% loan/deposit bank would necessarily have some sort of wholesale funding as it needs to maintain some liquidity. It would also very likely have a more expensive saving deposit base and some loan impairment charges. But the mechanism remains the same therefore those details don’t matter.

In order to remain profitable, the bank’s interest income has to be superior to its cost base. Moreover, the bank’s interest income is a direct, linear function, of the BoE rate. The higher the rate, the higher the income and the higher the profitability. As a result, the bank’s profitability obeys the following equation:

Net Profit = Interest Income – Costs = f(BoE rate) – Costs,

with f(BoE rate) = BoE rate + margin = BoE rate + 1%.

Consequently, in order for Net Profit > 0, we need f(BoE rate) > Costs.

Now, we know that the bank’s cost base is GBP20m. The bank must hence earn more than GBP20m on its loan book to remain profitable (which does not mean that it is enough to cover its cost of capital).

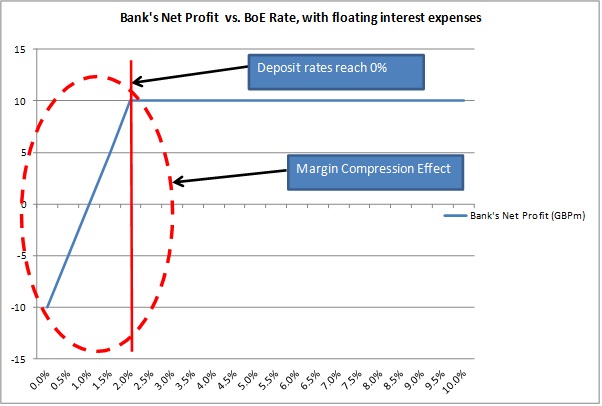

The BoE rate is 2%, making the rate on the mortgage book of the bank 3%, leading to a GBP30m income and a GBP10m net profit. Almost overnight, the BoE lowers its rate to 0.5%. The bank’s loan book’s average rate is now 1.5%, and generates GBP15m of income. The bank is now making a GBP5m loss. Having inflexible short-term costs, it’s only way of getting back to profitability is to increase its margin by at least 0.5%. The bank’s net profit profile is summarised by the following chart:

However, a more realistic bank would pay interest on its deposit base (its funding). Let’s now modify our assumptions and make that same bank entirely demand deposit-funded, remunerated at a variable rate. The bank pays BoE rate minus a fixed 2% margin on its deposit base. As a result, what needs to cover the banks operational costs isn’t interest income but net interest income. The bank’s net profit equation is now altered in the following way:

Net Profit = Net Interest Income – Costs

Net Profit = Interest Income – Interest Expense – Costs

Net Profit = f1(BoE rate) – f2(BoE rate) – Costs

with f1(BoE rate) = BoE rate + margin = BoE rate + 1%,

and f2(BoE rate) = BoE rate – margin = BoE rate – 2%.

The equation can be reduced to: Net Profit = 3% (of its loan book) – Costs, as long as BoE rate >= 2% (see below).

Let’s illustrate the net profit profile of the bank with the below chart:

What happens is clear. Independently of its effects on the demand for credit and loan defaults, the BoE rate level has no effect on the bank’s profitability. Everything changes when deposit rates reach the zero lower bound (i.e. there is no negative nominal rate on deposits), which occurs before the BoE rate reaches it. From this point on, the bank’s interest income decreases despite its funding cost unable to go any lower. This is the margin compression effect that I described in my first post. In reality, things obviously aren’t that linear but follow the same pattern nevertheless.

Realistic banks are also funded with saving deposits and senior and subordinated debt, on which interest expenses are higher. This is when schemes such as the Funding for Lending Scheme kicks in, by providing cheaper-than-market funding for banks, in order to reduce the margin compression effect. The other way to do it is to reflect a rate rise in borrowers’ cost, while not increasing deposit rates. This is highly likely to happen, although I guess that banks would only partially transfer a rate hike in order not to scare off customers.

Overall, we could say that markets determine mortgage rates to an extent. But this is only due to the fact that banks have natural (short-term) limits under which they cannot go. It would make no sense for banks not to earn a single penny on their loan book (and they would go bust anyway). Beyond those limits, the BoE still determines mortgage rates.

Although I am going to qualify this assertion: the BoE roughly determines the rate and markets determine the margin. At a disaggregated level, banks still compete for funding and lending. They determine the margins above and below the BoE rate in order to maximise profitability. They, for instance, also have to take into account the fact that an increase in the BoE rate might reduce the demand for credit, thereby not reflecting the whole increase/decrease to customers as long as it still boosts their profitability. Those are some of the non-linear factors I mentioned above. But they remain relatively marginal and the aggregate, competitively-determined, near-equilibrium margin remains pretty stable over time as demonstrated with the first chart above.

With this post I hope to have clarified the mechanism I relied on in my previous post, but feel free to send me any question you may have!

Mortgage rates are still determined by the BoE

Ben Southwood from the Adam Smith Institute wrote an interesting piece this week. I have an objection to his title and the conclusion he reached. Ben wrote:

However, it was recently pointed out to me that since a high fraction of UK mortgages track the Bank of England’s base rate, a jump in rates, something we’d expect as soon as UK economic growth is back on track, could make mortgages much less affordable, clamping down on the demand for housing.

This didn’t chime with my instincts—it would be extremely costly for lenders to vary mortgage rates with Bank Rate so exactly while giving few benefits to consumers—so I set out to check the Bank of England’s data to see if it was in fact the case. What I found was illuminating: despite the prevalence of tracker mortgages the spread between the average rate on both new and existing mortgage loans and Bank Rate varies drastically.

Wait. I really don’t reach the same conclusion from the same dataset. This is what I extracted from the BoE website (using the BoE’s old reporting format, as the new one only started in 2011):

Banks and building societies offer two main types of floating rate mortgages: standard variable rate (SVR) and trackers. Trackers usually follow the BoE rate closely. SVR are slightly different: margins above the BoE rate are more flexible. Banks vary them to manage their revenues but usually fix them for an extended period of time before reviewing them again. During the crisis, some banks that had vowed to maintain their SVR at a certain spread angered their customers when this situation became unsustainable due to low base rates. Some banks and building societies made losses on their SVR portfolio as a result and had to break their promise and increase their SVR.

What we can notice from the chart above is clear: since the mid-1990s, it is the BoE that determine both mortgage and deposit rates. Not the market. All rates moved in tandem with the BoE base rate. Still, the linkage was broken when the BoE rate collapsed to the zero lower bound in 2009. And this is probably why Ben declared that

but what is clear is that tracker mortgages be damned, interest rates are set in the marketplace.

I think this is widely exaggerated. Ben missed something crucial here: banks have fixed operational costs. Banks generate income by earning a margin between their interest income (from loans) and interest expense (from deposits and other sources of funding). They usually pay demand deposits below the BoE rate and saving/time deposits at around the BoE rate, and make money by lending at higher rates. From this net interest income, banks have to deduce their fixed costs (salaries and other administrative expenses) and bad debt provisions.

There is a problem though. Setting the BoE rate near zero involves margin compression. Banks’ back books (lending made over the previous years) on variable rates see their interest income collapse. Banks’ deposit base is stickier: many saving accounts are not on variable rates. Therefore, there is a time lag before the deposit base reprice (we can see this on the chart above: whereas lending reprices instantaneously when the BoE rate moves, deposits show a lag). Moreover, near the zero bound, the spread between demand deposit rates and the BoE rates all but disappears. The two following charts clearly illustrate this margin compression phenomenon:

It is clear that banks started to make losses when the BoE rate fell, as the margin on the floating rate back book (stock) became negative. Using the new BoE reporting would make those margins look even worse*. To offset those losses, banks started to increase the spread on new lending, leading to a spike on the interest margin of the front book (green line above). Banks can potentially reprice their whole loan book at a higher margin, but this takes time, especially with 15 to 30-year mortgages. Consequently, banks not only increased the spread on new lending, but also decided to break their SVR promises and increase their back book SVR rates (see black line in charts). This usually did not go down well with their customers, but some banks had no choice, having entered the crisis with too low SVRs.

What happens to a bank whose net interest income is negative (assuming it has no other income source)? It reports net accounting losses as it still has fixed operational expenses… Continuously depressed margins explain why banks’ RoE remains low. For banks to report net profits, their net interest income must cover (at least) both operational expenses and loan impairment charges. What Ben identified as ‘market-defined interest rates’ or the ‘spread over BoE’s rate’ from 2009 onwards is simply the floor representing banks’ operational costs, under which banks cannot go… The only other (and faster) way to rebuild banks’ bottom line would be to increase the BoE rate.

A mystery though: why didn’t banks decrease their time deposit rates further? I am unsure to have an answer to that question. A possibility is that the spread between demand and time deposits remained the same. Another possibility is that banks’ time deposit rates remained historically roughly in line with UK gilts rates. Decreasing time deposit rates much below those of gilts would provide savers with incentives to invest their money in gilts rather than in banks’ saving accounts.

What would a rate hike mean? Ben thinks it would have little impact, probably because the spread over BoE seems to show quite a lot of breathing space before the base rate impacts lending rates. I don’t think this is the case. A rate increase would likely push lending rates upwards on bank’s back book (i.e. banks are not going to reduce the spread in order to maintain stable mortgage rates). Why? Banks’ net interest margin and return on equity are still very depressed. Moreover, new Basel III regulations are forcing banks to hold more equity, further reducing RoE. Consequently, banks will seek to rebuild their margin and profitability, making customers pay higher rates to compensate for years of low rates and newly-introduced regulatory measures.

* I am unsure why the BoE changed its reporting and what the differences are, but reported lending rates are much lower than with the old reporting standards. Tracker mortgage rates even seem to be lower than time deposit rates. See below and compare with my first chart. If anybody has an explanation, please enlighten me:

Update: I replaced ‘ceiling’ with ‘floor’ in the post as it makes a lot more sense!

Update 2: Ben Southwood replies here…

Update 3: …and I replied there!

Recent Comments