What’s wrong with Bloomberg?

Bloomberg was created to report financial and economic events to financiers. Yet it seems that it has drawn the wrong conclusions from the crisis and fallen into the interventionist trap. Repeating usual basic statist/interventionist misconceptions isn’t what we expect from such a respectable company. The editorial line of the Financial Times or The Economist seems to be much more balanced in comparison, even if I don’t agree with everything they say.

Last week, Bloomberg reported that:

Four years after President Barack Obama signed the Dodd-Frank Wall Street Reform and Consumer Protection Act into law, polling suggests that most Americans think it hasn’t done enough to protect them from a repeat of the 2008 financial crisis, a disaster from which the global economy has yet to fully recover.

Unfortunately, they’re right.

According to Bloomberg, Dodd-Frank is the ultimate tool that regulators need to make the system ‘safe’:

Dodd-Frank provides regulators with all the powers they need to prevent the financial sector from leaning on taxpayers and putting the economy in danger. All that’s wanting, four years on, is the will to use them.

This goes against all evidences so far. Dodd-Frank has many issues (too many links to provide… I let you google it). Just don’t tell Bloomberg.

Today, Bloomberg announced its support of tighter regulatory oversight for insurers and… Berkshire Hathaway:

Could Warren Buffett’s Berkshire Hathaway Inc. threaten the stability of the financial system? The U.S.’s top regulators are asking themselves this question as they consider whether Berkshire and other large insurers should come under Federal Reserve oversight.

The answer is yes.

While many of Bloomberg’s contributors publish interesting and intellectually-stimulating articles, and many of its financial facts-reporting articles are useful sources of information, Bloomberg ‘Editors’ have taken a very narrow view of what happened during the crisis based on platitudes, partial understandings and other misconceptions, and keep lamenting about the lack of regulatory pressure/intrusion/control. According to the website, it looks like regulation is the alpha and the omega: if only regulators and politicians were more tightly controlling the financial system, there would be no crisis. Criticisms and challenges (or at least discussions) of regulatory failures and regulatory distortions seem to be pretty much non-existent in editorials. Is this really the type of balanced reporting we expect from such a serious financial publication?

Sovereign debt crisis: another Basel creature?

I often refer to the distortive effects of RWA on the housing and business/SME lending channels. What I don’t say that often is that Basel’s regulations have also other distortive effects, perhaps slightly less obvious at first sight.

Basel is highly likely to be partially responsible for sovereign states’ over-indebtedness, by artificially maintaining interest rates paid by governments below their ‘natural’ level.

How? Through one particular mechanism historically, that you probably start knowing quite well: risk-weighted assets (RWA). Basel 1 indeed applied a 0% risk-weight on OECD countries’ sovereign debt*, meaning banks could load up their balance sheet with such instruments without negatively impacting their regulatory capital ratios at all. Interest income earned on sovereign debt was thus almost ‘free’: banks were incentivised to accumulate them to maximise capital-efficiency and RoE.

This extra demand is likely to have had the effect of pushing interest rates down for a number of countries, whose governments found it therefore much easier to fund their electoral promises. In the end, the financial and economic crisis was triggered by the over-issuance of very specific types of debt: housing/mortgage, sovereign and some structured products. All those asset classes had one thing in common: a preferential capital treatment under Basel’s banking regulations.

Basel 2 introduced some granularity but fundamentally didn’t change anything. Basel 3 doesn’t really help either, although local and Basel regulators have recently announced possible alterations to this latest set of rules in order to force banks to apply risk-weights to sovereign bonds (one option is to introduce a floor). Some banks have already implemented such changes (which cost billions in extra capital requirements).

While those measures go in the right direction, Basel 3 has also introduced a regulatory tool that goes precisely the opposite way: the liquidity coverage ratio (LCR). The LCR requires banks to maintain a large enough liquidity buffer (made of highly-liquid and high quality assets) to cover a 30-day cash outflow. As you may have already guessed, eligible assets include mostly… government securities**.

Here again, Basel artificially elevates the demand for sovereign debt in order to comply with regulatory requirements, pushing yields down in the process. This has two consequences: 1. governments could find a lot easier to raise cash than in free market conditions (with all the perverse incentives this has on a democratic process unconstrained by economic reality) and 2. as sovereign yields are used as risk-free rate benchmarks in the valuation of all other asset classes, the fall in yield due to the artificially-increased demand could well play the role of a mini-QE, boosting asset prices across the board ceteris paribus.

We end up with a policy mix that contaminates both central banks’ monetary policies and domestic political debates. But, worst of all, it is a real malinvestment engine, which trades short-term financial solidity for long-term instability.

* Some non-OECD regions of the world also allow their domestic banks to use 0% risk-weight on domestic sovereign debt. For instance, many African countries are allowed to apply 0% weighing on the sovereign debt of their local governments despite the obvious credit risk it represents as well as its poor marketability (this is partly mitigated as this debt is often repoable at the regional central bank). Moreover, the same regulators prevent their domestic banks from investing their liquidity in Treasuries or European debt, with the obvious goal of benefiting those African states. Consequently, illiquid and risky sovereign bonds comprise most of those banks’ “liquidity” buffers, evidently not making those banking systems much safer…

** The LCR is partly responsible for the ‘shortage of safe assets’ story.

A tale of two US lending curves

I was a little bit intrigued by my previous chart and decided to take a second look at it. Here it is, using a log scale (as this is a chart covering 47 years, please keep in mind that what looks like small temporary fluctuations actually represent large ones…):

The two dotted lines represent the 1950-1980 trend for each curve. Why did I pick 1980? As it takes many years to develop new international Basel regulations, numerous drafts and proposals are circulated over a few years. This raises expectations of what future regulatory requirements will look like and banks progressively adapt the shape of their balance sheet to be in compliance once the rules effectively kick in. For instance, current Basel 3 regulations consultations started in 2009, with almost final proposals published between 2010 and 2011, and planned to be enforced by 2019, although most banks already comply with many of its features.

A draft of Basel 1 rules was published in 1987, following years of consultations (I am unsure exactly when those started, hence the choice of 1980), followed by a final agreement in 1988 and an official enforcement from 1992 onwards. In the US, Basel 1 was in place until well into the 2000s, and only a few banks had started applying Basel 2 before the crisis.

The first shocking feature of this chart is the differential between trend and actual business lending volume. Business lending completely collapsed relative to trend from the end of the 1980s, coinciding pretty much exactly with the implementation of Basel 1, and despite real interest rates falling (see chart below). Can any other (macro or micro) economic event explain this very sudden change? Did we overnight move into a low-growth/secular stagnation/economic ‘abundance’ paradigm? This looks highly unlikely.

The second remarkable feature is that real estate lending volume did not offset the fall in business lending. For a long period, real estate lending seemed to be above pre-1980 trend, before getting back to trend level and then departing from it again from the early 2000s. Never real estate lending fell below trend following the introduction of Basel 1, except during the Great Recession.

Now, this chart is very hard to interpret by itself, and it will take much more analysis to come to any meaningful conclusion. Pre-1980 lending trend perhaps was too rapid (remember post-WW2 boom and stagflation)? This would have two possible consequences: 1. real estate lending growth would therefore have been way too fast post-1980 and 2. business lending was perhaps in line with the actual trend?

My guess is that the truth lies in between: pre-1980 trend was perhaps too rapid, but post-1980 business lending growth was too low. Remember that household debt to income kept increasing over the period, signalling that real estate lending growth was surely too fast.

There is another possible explanation: that my chart does not cover all possible lending instruments. We know that Basel rules strongly encouraged the use of securitised products (which benefited from better capital treatment), in particular securitised mortgage instruments such as CMBS and RMBS. Banks that originate those mortgages originally reported them on their balance sheet, before taking them off-balance sheet. Does the FRED real estate lending data include those products (off-balance sheet or purchased by other institutional investors)? I have no idea and will have to do a lot more research on the FRED database before coming up with a satisfying description of the chain of events.

Is the US dissociating from Basel banking rules?

I was left a little bewildered by this recent FT article:

US lending to businesses is reaching record levels but banks are privately warning that the activity should not be seen as evidence of an economic recovery.

Despite Basel rules that favour mortgage lending over business lending, and business lending struggling in Europe and the UK as a result, have US banks found the trick to bypass those rules or decided not to maximise their profitability? Is the US special?

First, let’s look at the data:

The first thing that comes out of this chart is the massive trend change from the end of the 1980s onwards. What happened at that time? Basel 1 rules were introduced, making it more expensive in terms of capital utilisation to lend to corporates than for real estate-related purposes. Basel is the turning point. Ex-ante, corporate lending volume used to be slightly larger than mortgage lending for decades. Ex-post, house lending became the primary channel of credit growth, by far.

The first thing that comes out of this chart is the massive trend change from the end of the 1980s onwards. What happened at that time? Basel 1 rules were introduced, making it more expensive in terms of capital utilisation to lend to corporates than for real estate-related purposes. Basel is the turning point. Ex-ante, corporate lending volume used to be slightly larger than mortgage lending for decades. Ex-post, house lending became the primary channel of credit growth, by far.

Something happened during the crisis: from end-2010 until now, the differential between the total volume of mortgage lending and the total volume of corporate lending tightened to USD1.9Tr. Surely this doesn’t fit my story that Basel rules introduce massive distortions of the lending channel. I have to admit that my knowledge of the US market is limited. Nevertheless, there is a possible explanation.

First, the tightening remains moderate: ‘only’ USD200Bn, or 9.5% of the original differential. The tightening arose from a strong recovery of business lending from early-2011 onwards (following a sharp fall during which the differential actually widened), whereas mortgage lending remained flat.

Second, risk-weights on residential and commercial real estate lending actually increase when the sector suffers and property prices collapse. The US experienced a large fall in both residential and commercial real estate prices. As defaults on those mortgages and foreclosures soared, risk-weights increased.

It is then very likely that, from a capital utilisation point of view, lending to businesses was as profit-maximising – if not more – as extending credit for real estate purposes. Indeed, daily corporate bankruptcies started normalising from early 2010, whereas house prices continued declining until mid-2012.

It also looks like much of this new corporate lending has been driven by large corporations (for acquisitions and share buybacks), which are less capital intensive for banks (especially at the moment, as many of them are sitting on large piles of cash, USD1.6Tr according to Moody’s, and growing at rapid pace – 12% p.a.). Moreover, the latest data seems to indicate that real estate lending is making a comeback.

At the end of the day, it looks a little premature to say that US banks have found the way to bypass Basel to fund industrial companies and SMEs…

Nevertheless, there is some glitter of hope. The UK regulator PRA warned banks that they may have to increase risk-weights on mortgage lending, hence increasing the amount of capital necessary to fund those loans and making them slightly less attractive to maximise profitability, relatively to other asset classes. This is ironic though. Risk-weights have been introduced and encouraged by regulators over the last twenty years, and still very few of them seem to understand the inherent capital allocation distortion they lead to…

I had a dream: that RWAs and Basel’s economically distortive rules were abolished and we were going back to the pre-1988 consensus of similar industrial and mortgage lending volume. Perhaps we would witness fewer housing bubbles and more economic growth*… But that’s just a dream.

* And be spared of ignorant ‘secular stagnation’ ideas that ignore the economic dynamics at the micro level…

PS: reduced blogging activity over the past 10 days due to work and travel… I’ll try to catch up soon.

A brief comment on Piketty

Thomas Piketty’s new book, Capital in the 21st Century, is both controversial and a great success. Despite its flaws, its success reflects growing concerns that need to be addressed. I finished reading the book a few weeks ago and actually found it quite interesting (apart from its nonsensical last section) and easy to read. I am not going to review it here: there are already possibly 1,000 reviews available online, focusing on the underlying economic theory or on the data-picking of the book.

One thing struck me though: the lack of explanation as to why the data evolves the way it does. Piketty seems to believe that this is the result of a ‘fundamental and inherent’ characteristic of capitalism (‘r > g’). Fair enough, but despite all his expertise in the unequality area, Prof Piketty seems to lack the necessary knowledge in other economic and finance areas to reach the right conclusions.

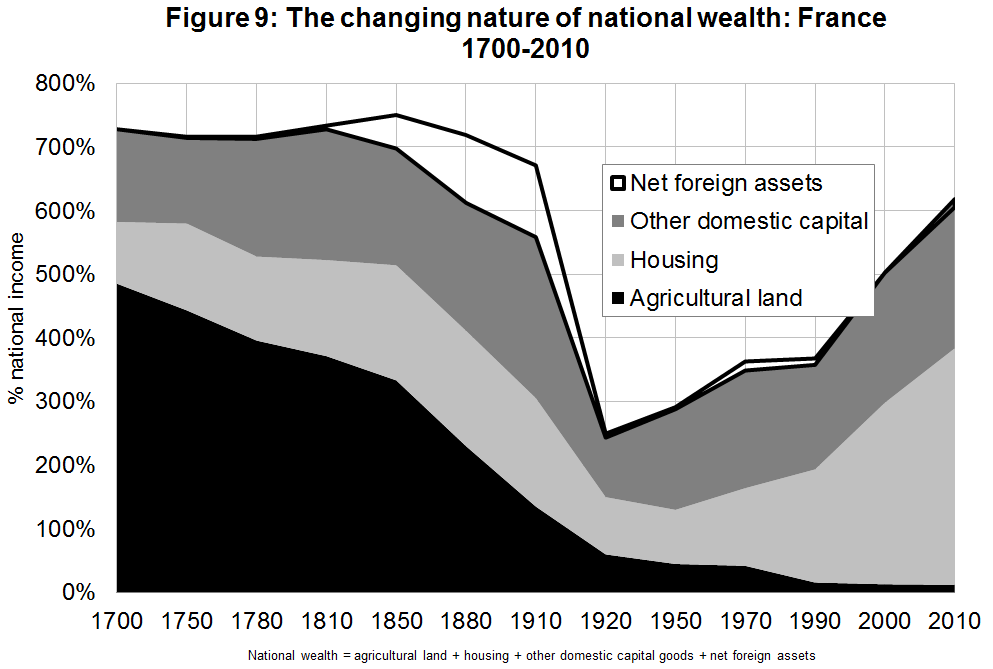

He uses the three following charts to demonstrate the evolution of wealth as a share of national income throughout the last few centuries.

In the US:

In Britain:

In France:

Now compare with the following charts:

A lot of people have already pointed out that most of what Piketty sees as ‘rise’ in inequality in fact emanates almost entirely from housing bubbles… This is obvious for Britain and France, though I am surprised by Piketty’s US chart as the US clearly experienced a housing bubble as well, which seems not to be reflected in in his wealth data: US housing roughly represented the same share of wealth in 2010 as in 1990. This may be due to the fact that, in 2010, US housing prices had collapsed, which is not captured by Piketty’s chart (which isn’t smooth enough, i.e. one data point every 20 years).

Piketty admits several times in his book that ‘bubbles’ were partly the underlying cause of those rises. Yet, to him, those bubbles seem to be fundamental features of capitalism and government must intervene by redistributing the increased capital stock. As I mentioned a couple of weeks ago, I encourage him to dig into Basel banking regulations, which distort lending by benefiting housing and were implemented almost exactly when housing wealth started rising. He would probably notice that a large part of the increase in pre-crisis wealth inequality was due to a combination of banking regulation and interest rates below their ‘natural’ level*, both creatures of government intervention, not of free market capitalism…

* Planning restrictions in places like London and Paris also are to blame, I know, though they can’t explain everything. And, anyway, they also reflect government measures…

Unintended (intended?) consequences

In my previous post, I described how politicians (in this case, Vince Cable) were confused by the impacts of banking regulations. The large amount of new and modified rules that have been striking the financial sector over the past few years are bringing their lot of unintended consequences. Unless some of those consequences were actually perfectly intended…

About a week ago, The Economist reported the collapsing global financial links:

One of the main casualties of the cringe is the very institution of correspondent banking. This is the informal mesh of arrangements allowing the customer of a bank in one country to send money to someone in another country, even if the bank in question does not have a branch there. The system is as old as international finance itself, dating back to the earliest promissory notes and letters of credit written by banks in classical times. Yet it is now being threatened by an overzealous interpretation and enforcement of rules aimed at preventing money-laundering and starving terrorists of funds. […]

The exact size of the retreat is difficult to gauge because of a dearth of recent global data, but executives at such firms say they are dropping as many as a third of their correspondent relationships. One big firm says it is cutting or scaling back about 1,000 linkages; another, 1,800. Such ruthlessness will have a dramatic impact because these institutions are the main nodes through which the world’s banks link up with one another. […]

It is not just in distant and benighted places that the consequences of this severity are being felt. In Britain students from Iran, Sudan and Syria cannot open bank accounts. In America, foreign diplomats and embassies complain that they too are being denied access to banking.

Do-gooders are being caught in the net, too. Charities such as Save the Children, the Red Cross and Christian Aid have struggled to transfer funds to places like Syria due to sanctions. Even after obtaining explicit approval from American regulators, some have found it difficult to convince banks to send money.

We’re indeed on our way to the de-globalisation of banking, with all the systemic risks this involves. Whether or not the outcome of this particular policy was intended by regulators is something I cannot answer. But in general, regulators have been actively working on the fragmentation of the global banking system, as we’ve recently seen.

The research paper from the London School of Economics found the daily changes in the valuation of margin, which traders are required to post, may rise tenfold by using central clearing houses. That compared to banks being allowed to clear the same deals between themselves.

The paper’s conclusion that banks may face greater operational risks and more demands on their liquidity underlines regulators’ and market participants’ concerns that a post-crisis global political accord designed to strengthen the financial system may only succeed in shifting risk.

I haven’t read the study yet (and actually couldn’t even find it on the LSE SRC website), but it does look like the outcome of those new rules is going to be reduced interlinks (through derivative contracts) between banks.

Let’s sum up. New rules that favour a fragmented banking system are:

- Ringfencing different parts within individual banks/legal entities

- Asking for separate capital and funding structures between subsidiaries of a same group

- Reducing the ability of various entities of a same banking group to transfer liquidity and capital

- Reducing interconnectivity and financial agreements between banks of different countries

- Making derivative trading and settlements more expensive

- I’m surely forgetting a lot of other things

My guess is that it will take a few years (possibly early 2020s) to find out what kind of monster this magic regulatory potion really created.

Vince Cable realises too late what banking regulation involves

Back from holidays, and a lot of things to cover…

Let’s start with Vince Cable, Britain’s Secretary of State for Business, who is making a U-turn, though not yet quite finished, as he progressively realises how much he ignored about the pernicious effects of banking regulation.

The way the regulatory system operates has undoubtedly had a suffocating effect on business lending and particularly on our exporters.

Not surprisingly, the result is that banks pump out lending in the mortgage market, while lending to small businesses is restricted. This directly stems from the rules on which the regulatory model is based and has had a very damaging impact.

You may well recognise that he is referring to risk-weighted assets (RWAs), which have been a recurrent theme of this blog (and the focus of my three latest posts). Vince Cable had already sparked controversy pretty much exactly a year ago, when he first attacked the BoE for being a ‘capital Taliban’:

One of the anxieties in the business community is that the so called ‘capital Taliban’ in the Bank of England are imposing restrictions which at this delicate stage of recovery actually make it more difficult for companies to operate and expand.

This is a welcome reaction by one of the country’s top politician. However, let’s go back a few years to find the same Mr Cable vehemently supporting the exact same reforms he now criticises, while fully rejecting bankers’ claims that increased capital requirements would allocate funding away from SMEs (see here, here, here, here and here):

Banks and industry groups have argued more regulation could force institutions to curb lending to small- and medium-sized businesses at a time when the economy is slowing.

Prediction which turned out to be correct.

Mr Cable’s went from blaming banks for the crisis and justifying stronger regulatory requirements to blaming those same requirements for the weak level of business lending in the UK. Unfortunately, his U-turn isn’t fully completed and Mr Cable attacks the wrong target. Capital requirements are defined in Basel, the Swiss city. And he supported them in the first place, without evidently knowing what those rules involved. He also seemingly showed a poor understanding of banking history as his support for banking insulation through ring-fencing demonstrated (though most regulators are to blame as well).

Better late than never? Perhaps, but probably too late to have any effect going forward… Politicians’ and regulators’ rush to design banking rules in order to please the public opinion is making everyone worse off in the end.

Photo: Rex Features

The era of the neverending bubble?

The IMF got the timing right. It published last week a new ‘Global Housing Watch‘, and warned that house prices were way above trend in a lot of different countries all around the world. The FT also reports here:

The world must act to contain the risk of another devastating housing crash, the International Monetary Fund warned on Wednesday, as it published new data showing house prices are well above their historical average in many countries.

As I said, perfect timing, as this announcement follows my previous post on the influence of Basel’s RWAs on mortgage lending.

As long as international banking authorities don’t get rid of this mechanism, we are likely to experience reoccuring housing bubbles with their devastating economic effects (hint for Piketty: and investors/speculators will have an easy life making capital gains).

PS: I am on holidays until the end of the week, so probably not many updates over the next few days.

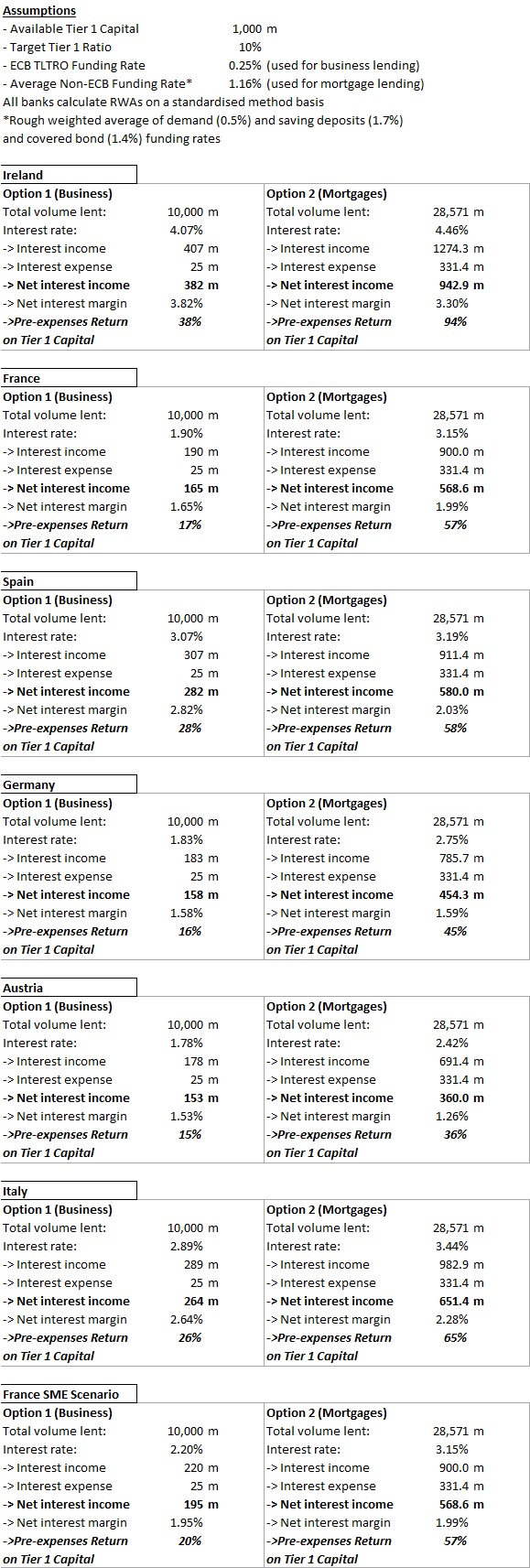

Basel vs. ECB’s TLTRO: The fight

(and vs. BoE’s FLS)

Following my previous post on the mechanics of ECB negative deposit rates, I wanted to back my claims about the likely poor effect of the central bank TLTRO measure on lending.

I argued that despite the cheap funds provided by the ECB to lend to corporate clients (particularly SMEs), Basel’s risk-weighted assets would stand in the way of the scheme as they keep distorting banks’ lending incentives (same is true regarding the BoE and the second version of its Funding for Lending Scheme).

I extracted all the most recent new business and mortgage lending rates from the central banks’ websites of several European countries. Unfortunately, business lending rates are most of the time aggregates of rates charged to large multinational companies, SMEs, and micro-enterprises. Only the Banque of France seemed to provide a breakdown. So most business lending rates below are slightly skewed downward (but not by much as you can see with the French case).

Using this dataset, I built a similar scenario to the one I described in my first RWAs and malinvestments post (as it turned out, I massively overestimated business lending rates in that post…). I wanted to find out what would be the most profitable option for a bank: business lending or mortgage lending, given RWA and capital constraints (banks target a 10% regulatory Tier 1 capital ratio). The results speak for themselves:

Despite the cheap ECB loans, and given a fixed amount of capital, banks are way more profitable raising funding from traditional sources to lend to households for house purchase purposes…

Admittedly, the exercise isn’t perfect. But the difference in net interest income and return on capital is so huge that tweaking it a little wouldn’t change much the results:

- I assume that all business lending is weighted 100%. In reality, apart from the French SME scenario, large corporates (often rated by rating agencies) benefit from lower RWA-density under a standardised method. This would actually raise the profitability of business lending through higher volume (and increased leverage), though not by much. Mortgages are weighted at 35% under that method.

- I assume that all banks use the standardised method to calculate RWAs. In reality, only small and medium-sized banks do. Large banks use the ‘internal rating based’ method, which allows them to risk-weight customers following their own internal models. Here again, most corporates can benefit from lower RWAs. But mortgages also do (RWA-density often decreases to the 10-15% range).

- Cross-selling is often higher with corporates, which desire to hedge and insure their financial or non-financial business positions. Corporates also use banks’ international payment solutions. This adds to revenues.

- Business lending is often less cost-intensive than retail lending. Retail lending indeed traditionally requires a large branch network, which is less the case when dealing with corporates (often grouped within regional corporate centres, though not always for tiny enterprises). However, retail banking is progressively moving online, providing opportunities to banks to cut costs and improve their profitability.

- The lower RWA-density on mortgages allows banks to increase lending volume and leverage. However, this also requires higher funding volumes. In turn, this should increase the rate paid on the marginal increase in funding, raising interest expense somewhat in the case of mortgages.

In the end, even if the adjustments described above reduce the profitability spread by 10 percentage points, the conclusion stands: banks are hugely incentivised to avoid business lending, facilitating misallocation of capital on a massive scale, in particular in a period of raising capital requirements… Moreover, banks also benefit from favourable RWAs for securitised products based on mortgages (CMBS, RMBS…), compounding the effects.

To tell you the truth, I wasn’t expecting such frightening results when I started writing that post… Please someone tell me that I made a mistake somewhere…

Central banks, regulators and politicians will find it hard to prop up business lending with regulations designed to prevent it.

In case anybody still doubted that RWAs affect banks’ lending allocation…

Just a very very quick post tonight.

Our business is constrained by the capital we have available to cover risk-weighted assets (RWA) resulting from the risks in our business, by the size of our on- and off-balance sheet assets through their contribution to leverage ratio requirements and regulatory liquidity ratios, and by our risk appetite. Together, these constraints create a close link between our strategy, the risks that our businesses take and the balance sheet and capital resources that we have available to absorb those risks. As described in “Equity attribution framework” in the “Capital management” section of this report, our equity attribution framework reflects our objectives of maintaining a strong capital base and guiding businesses towards activities that appropriately balance profit potential, risk, balance sheet and capital usage.

Where does this come from? The 2013 annual report of UBS, the largest Swiss bank (page 150).

How banks are incentivised by Basel’s risk-weighted assets is clear. What provides has a low capital treatment (= low RWA), has relatively low default risk, is highly collateralised, even though it doesn’t bring in much interest income? Yep, mortgages (as well as some tranches of securitised products such as RMBSs, and sovereign debt).

Recent Comments