China’s Frankenstein banking system keeps growing

Financial regulation in China is quite a mess. China seems to be the world testing ground for some of the most ridiculous banking rules. With all their related unexpected consequences.

Take this recent story: some time ago, Chinese regulators found it clever to cap Chinese banks’ loans/deposits ratios at 75% by the end of each quarter (it isn’t). The goal was to ensure that banks have enough liquidity to face large cash withdrawals. Nevermind that loans/deposits only take into account loans from the asset side of the balance sheet and that banks can use depositors cash to invest in many different sorts of assets (from liquid sovereign bonds and short-term repos to very illiquid securities). Perhaps Chinese banking rules forbid some of those investments (I am not an expert on the Chinese banking system). The fact that the rule was only enforced at quarter-end seemed not to be a problem either (arbitrage anyone?), or that the news that a bank hadn’t complied with the rule could trigger a panic.

Nevertheless, as usual with China, the spontaneous financial order reacts. As the FT reports:

In recent years, the final few days of each quarter have become a nervous time for banks. As liquidity has tightened and many depositors have shifted their savings into higher-yielding substitutes such as Alibaba’s online money-market fund, Yu’E Bao, many lenders have struggled to attract enough traditional deposits to stay below the maximum 75 per cent loan-to-deposit ratio.

That regulation, intended to ensure banks keep enough cash on hand to meet withdrawal demand, is enforced at the end of each quarter – providing an incentive to window-dress deposit totals. This was exacerbated by the desire to prettify quarterly reports to shareholders.

To meet the deposit challenge, many banks resorted to an all-hands-on-deck approach, requiring employees to meet a deposit target. That meant urging clients – and even family and friends – to transfer funds into the bank, typically only for a few days covering the quarter-end period.

Typical example of a rule that, not only introduces opacity, but also creates unintended consequences.

But the story isn’t over.

Chinese regulators didn’t really appreciate that bankers were trying to bypass their well-thought-out rule. They came up with another very ‘clever’ rule to fix the flawed rule:

Regulators will suspend business approvals to banks whose month-end deposit total deviates by more than 3 per cent from the daily average over the previous month.

Problem solved. Not.

To the uncertainty and unintended consequences of the previous rule, they added further uncertainty and unintended consequences. Nevermind that such a rule would limit competition for deposits (Chinese banks are for now forbidden to compete on price – this is about to change –, but can well use other means and advantages). A larger deposit inflow could well happen for any reason (run on a competitor, or simply good news about the financial strength of a bank leading to an inflow of new customers). Penalising banks for such reason sounds rather dubious to say the least.

One of the consequences is that banks now turn away deposits…

The rule can also easily trigger instability, as the FT adds:

A light-hearted commentary circulated among bankers on social media on Wednesday, carrying the headline “If there’s a bank you hate, send them all your money before 12 tonight”.

I’m sure Chinese people, with their usual banking rule-avoiding ingenuity, will soon enough find a way to use all the loopholes created by this combination of definitely very clever regulations. And that regulators, in turn, will come up with another rule to patch the rule that patched the rule. The Frankenstein experiment continues.

Why the Austrian business cycle theory needs an update

I have been thinking about this topic for a little while, even though it might be controversial in some circles. By providing me with a recent paper empirically testing the ABCT, Ben Southwood, from ASI, unconsciously forced my hand.

I really do believe that a lot more work must be done on the ABCT to convince the broader public of its validity. This does not necessarily mean proving it empirically, which is always going to be hard given the lack of appropriate disaggregated data and the difficulty of disentangling other variables.

However, what it does mean is that the theoretical foundations of the ABCT must be complemented. The ABCT is an old theory, originally devised by Mises a century ago and to which Hayek provided a major update around two decades later. The ABCT explains how an ‘unnatural’ expansion of credit (and hence the money supply) by the banking system brings about unsustainable distortions in the intertemporal structure of production by lowering the interest rate below its Wicksellian natural level. As a result, the theory is fully reliant on the mechanics of the banking sector.

The theory is fundamentally sound, but its current narrative describes what would happen in a relatively free market with a relatively free banking system. At the time of Mises and Hayek, the banking system indeed was subject to much lighter regulations than it is now and operated differently: banks’ primary credit channel was commercial loans to corporations. The Mises/Hayek narrative of the ABCT perfectly illustrates what happens to the economy in such circumstances. Following WW2, the channel changed: initiative to encourage home building and ownership resulted in banks’ lending approximately split between retail/mortgage lending and commercial lending. Over time, retail lending developed further to include an increasingly larger share of consumer and credit card loans.

Then came Basel. When Basel 1 banking regulations were passed in 1988, lending channels completely changed (see the chart below, which I have now used several times given its significance). Basel encouraged banks’ real estate lending activities and discouraged banks’ commercial lending ones. This has obvious impacts on the flow of loanable funds and on the interest rate charged to various types of customers.

In the meantime, banking regulations have multiplied, affecting almost all sort of banking activities, sometimes fundamentally altering banks’ behaviour. Yet the ABCT narrative has roughly remained the same. Some economists, such as Garrison, have come up with extra details on the traditional ABCT story. Others, such as Horwitz, have mixed the ABCT with Yeager’s monetary disequilibrium theory (which is rejected by some other Austrian economists).

While those pieces of academic work, which make the ABCT a more comprehensive theory, are welcome, I argue here that this is not enough, and that, if the ABCT is to convince outside of Austrian circles, it also needs more practical, down to Earth-type descriptions. Indeed, what happens to the distortions in the structures of production when lending channels are influenced by regulations? This requires one to get their hands dirty in order to tweak the original narrative of the theory to apply it to temporary conditions. Yet this is necessary.

Take the paper mentioned at the beginning of this post. The authors find “little empirical support for the Austrian business cycle theory.” The paper is interesting but misguided and doesn’t disprove anything. Putting aside its other weaknesses (see a critique at the bottom of this post*), the paper observes changes in prices and industrial production following changes in the differential between the market rate of interest and their estimate of the natural rate. The authors find no statistically significant relationship.

Wait a minute. What did we just describe above? That lending channels had been altered by regulation and political incentives over the past decades. What data does the paper rely on? 1972 to 2011 aggregate data. As a result, the paper applies the wrong ABCT narrative to its dataset. Given that lending to corporations has been depressed since the introduction of Basel, it is evident that widening Wicksellian differentials won’t affect industrial structures of production that much. Since regulation favour a mortgage channel of credit and money creation, this is where they should have looked.

But if they did use the traditional ABCT narrative, it is because no real alternative was available. I have tried to introduce an RWA-based ABCT to account for the effects of regulatory capital regulation on the economy. My approach might be flawed or incomplete, but I think it goes in the right direction. Now that the ABCT benefits from a solid story in a mostly unhampered market, one of the current challenges for Austrian academics is to tweak it to account for temporary regulatory-incentivised banking behaviour, from capital and liquidity regulations to collateral rules. This is dirty work. But imperative.

Major update here: new research seems to confirm much of what I’ve been saying about RWAs and the changing nature of financial intermediation.

* I have already described above the issue with the traditional description of the ABCT in this paper, as well as the dataset used. But there are other mistakes (which also concern the paper they rely on, available here):

– It still uses aggregate prices and production data (albeit more granular): the ABCT talks about malinvestments, not necessarily of overinvestment. The (traditional) ABCT does not imply a general increase in demand across all sectors and products. Meaning some lines of production could see demand surge whereas other could see demand fall. Those movements can offset each other and are not necessarily reflected in the data used by this study.

– It seems to consider that aggregate price increases are a necessary feature of the ABCT. But inflation can be hidden. The ABCT relies on changes in relative prices. Moreover, as the structure of production becomes more productive, price per unit should fall, not increase.

Kupiec on central banking/planning

In the WSJ a couple of days ago, Paul Kupiec wrote an article that looks so similar to my blog that I had to quote it here.

Macroprudential regulation, macro-pru for short, is the newest regulatory fad. It refers to policies that raise and lower regulatory requirements for financial institutions in an attempt to control their lending to prevent financial bubbles. […]

There is also the very real risk that macroprudential regulators will misjudge the market. Banks must cover their costs to stay in business, and in the end bank customers will pay the cost banks incur to comply with regulatory adjustments, regardless of their merit. By the way, when was the last time regulators correctly saw a coming crisis?

He concludes with:

With Mr. Fischer now heading the Fed’s new financial stability committee, might we soon see regulations requiring product-specific minimum interest rates? Or maybe rules that single out new loan products and set maximum loan maturities and debt-to-income limits to stop banks from lending on activities the Fed decides are too “risky”? None of these worries is an unimaginable stretch.

Since the 2008 financial crisis, U.S. bank regulators have put in place new supervisory rules that limit banks’ ability to make specific types of loans in the so-called leverage-lending market—loans to lower-rated corporations—and for home mortgages. Since there is no scientific means to definitively identify bubbles before they break, the list of specific lending activities that could be construed as “potentially systemic” is only limited by the imagination of financial regulators.

Few if any centrally planned economies have provided their citizens with a standard of living equal to the standard achieved in market economies. Unfortunately the financial crisis has shaken belief in the benefits of allowing markets to work. Instead we seem to have adopted a blind faith in the risk-management and credit-allocation skills of a few central bank officials.

Government regulators are no better than private investors at predicting which individual investments are justified and which are folly. The cost of macroprudential regulation in the name of financial stability is almost certainly even slower economic growth than the anemic recovery has so far yielded.

This is very good, and I can’t agree more.

He points to his own research on macro-prudential policies. In a paper published in June 2014, Kupiec, Lee and Rosenfeld declare that

Compared to the magnitude of loan growth effects attributable to [increase in supervisory scrutiny or losses on loan/securities], the strength of macroprudential capital and liquidity effects are weak. This data suggest that traditional monetary policy (lowering banks’ cost of funding) is likely to be a much more potent tool for stimulating bank loan growth following widespread bank losses than modifying regulatory capital or liquidity requirements.

(note: they also say that the opposite logic applies)

While it doesn’t mean that they are wrong, I am not fully convinced by their arguments, especially given the dataset they base their analysis on (an economic and credit boom period, with less than tight monetary policy and many variables that could have been distorted as a result). In another paper, Aiyar, Calomiris and Wieladek point to the fact that macro-prudential policy can be effective at reducing banks’ lending, but that alternative sources of credit (i.e. shadow banking) grow as a result (they say that macro-prudential policies ‘leak’).

What is clear is that the effects of macro-prudential policies are unclear. What is also clear is that, whatever the effects of those policies, none are necessarily desirable. If macropru is indeed effective, then the resulting distorted capital allocation may be harmful. If macropru isn’t effective, then it may lead central bankers to (wrongly) believe they can maintain interest rates below/above their natural level while controlling the collateral damages this creates. In both cases the economy ends up suffering.

Two kinds of financial innovation

Paul Volcker famously said that the only meaningful financial innovation of the past decades was the ATM. Not only do I believe that his comment was strongly misguided, but he also seemed to misunderstand the very essence of innovation in the financial services sector.

Financial innovations are essentially driven by:

- Technological shocks: new technologies (information-based mostly) allow banks to adapt existing financial products and risk management techniques to new technological paradigms. Without tech shocks, innovations in banking and finance are relatively slow to appear.

- Regulatory arbitrage: financiers develop financial products and techniques that bypass or use loopholes in existing regulations. Some of those regulatory-driven innovations also benefit from the appearance of new technological and theoretical paradigms. Those innovations are typically quick to appear.

I usually view regulatory-driven innovations as the ‘bad’ ones. Those are the ones that add extra layers of complexity and opacity to the financial system, hiding risks and misleading investors in the process.

It took a little while, but financial innovations are currently catching up with the IT revolution. Expect to change the way you make or receive payments or even invest in the near future.

See below some of the examples of financial innovation in recent news. Can you spot the one(s) that is(are) the most likely to lead to a crisis, and its underlying driver?

- Bank branches: I have several times written about this, but a new report by CACI and estimates by Deutsche Bank forecasted that between 50% and 75% of all UK branches will have disappeared over the next decade. Following the growing branch networks of the 19th and 20th centuries, which were seen as compulsory to develop a retail banking presence, this looks like a major step back. Except that this is actually now a good thing as the IT and mobile revolution is enabling such a restructuring of the banking sector. SNL lists 10,000 branches for the top 6 UK bank and 16,000 in Italy. Cutting half of that would sharply improve banks’ cost efficiency (it would, however, also be painful for banks’ employees). It is widely reported that banks’ branches use has plunged over the past three years due to the introduction of digital and mobile banking.

- In China, regulators have introduced new rules to try to make it harder for mainstream banks to deal with shadow banks in order to slow the growth of the Chinese shadow banking system, which has grown to USD4.9 trillion from almost nothing just a few years ago. The Economist reports that, by using a simple accounting trick, banks got around the new rules. Moreover, while Chinese regulators are attempting to constrain investments in so-called trust and asset management companies, investors and banks have now simply moved the new funds to new products in securities brokerage companies.

- In London, underground travellers can now pay for their journey by simply using their contactless bank card. No need of a specific underground card anymore. NFC-enabled smartphones will be able to do the same in the near future.

- Barclays is experimenting contactless wristband that would effectively replace your contactless card for payments (or, for Londoners, your underground Oyster Card).

- Apple announced Apple Pay, a contactless payment system managed by Apple through its new iPhones and Watch devices. Apple will store your bank card details and charge your account later on. This allows users to bypass banks’ contactless payments devices entirely. Vodafone also just released a similar IT wallet-contactless chip system (why not using the phone’s NFC system though? I don’t know. Perhaps they were also targeting customers that did not own NFC-enabled devices).

- Lending Club, the large US-based P2P lending firm, has announced its IPO. This is a signal that such firms are now becoming mainstream, as well as growing competitors to banks.

Of course, a lot more is going on in the financial innovation area at the moment, and I only highlighted the most recent news. Identifying the regulatory arbitrage-driven innovations will help us find out where the next crisis is most likely to appear.

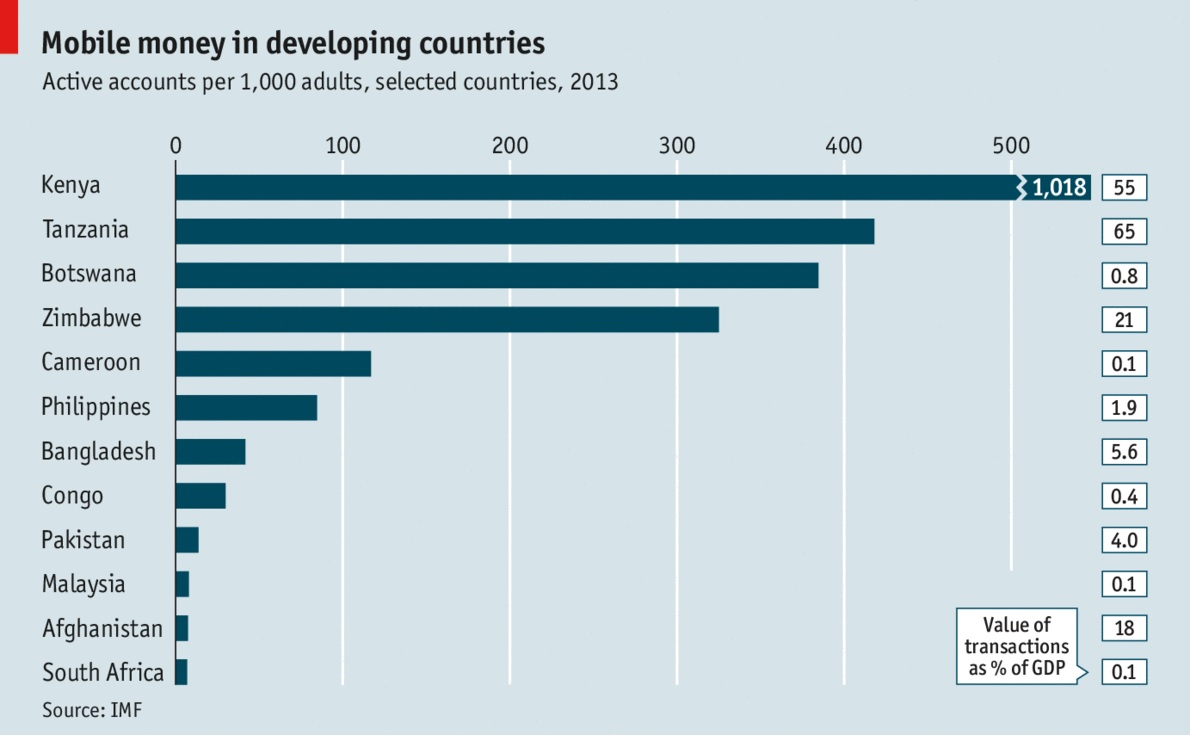

PS: the growth of cashless IT wallets has interesting repercussions on banks’ liquidity management and ability to extend credit (endogenous inside money creation), by reducing the drain of physical cash on the whole banking system’s reserves (outside money). If African economies are any guide to the future (see below, from The Economist), cash will progressively disappear from circulation without governments even outlawing it.

Secular stagnation: factoring in banking regulation

David Beckworth wrote a good post on the secular stagnation hypothesis, highlighting the problem with the interpretation of the natural rate by secular stagnation theorists. This is Beckworth:

First, real interest rates adjusted for the risk premium have not been in a secular decline. Everyone from Larry Summers to Paul Krugman to Olivier Blanchard ignore this point in the book. They all claim that real interest rates have been trending down for decades. The editors of the book, Coen Teulings and Richard Baldwin, even claim that this development is the ‘prima facie’ evidence for secular stagnation. What they are doing wrong is only subtracting expected inflation from the observed nominal interest rate. They also need to subtract the risk premium to get the natural interest rate, the interest rate at the heart of the story. For it is the natural interest rate that is affected by expected growth of technology and the labor force.

He is right. But I believe there is more to the story.

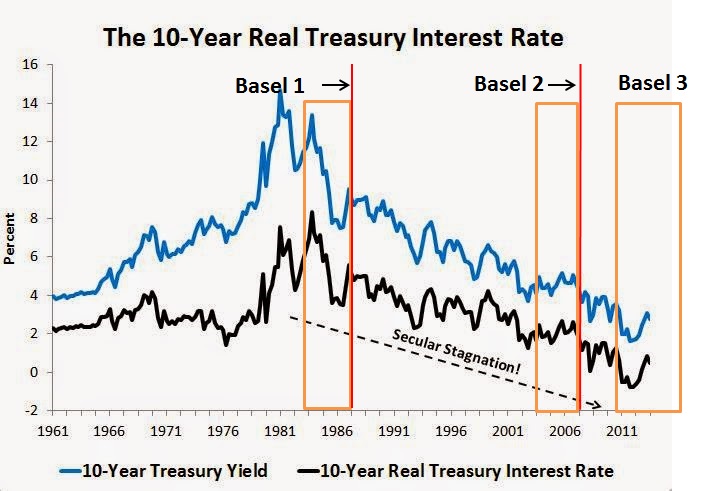

This is Beckworth’s chart highlighting the apparent secular decline in interest rates as believed by secular stagnation adherents. I added to it Basel 1, Basel 2 and Basel 3 introductions (red lines) and discussions (orange area) (unlike in Europe, only a few US banks had implemented Basel 2 when the crisis started):

What is striking is the fact that Treasury yields started declining exactly when Basel 1 was being discussed and implemented. There is a clear reason for this: Basel introduced risk-weighted assets, and government securities were awarded a 0% risk-weight, meaning banks could purchase them and hold no capital against them. As I have described before, banks were then incentivised to pile in such assets to maximise RoE, as a quick risk-adjusted return on capital calculation demonstrates. Basel 1 also introduced risk-weights for other asset classes such as business and mortgage lending. Structural changes in lending* and government securities markets occurred directly post-Basel. I believe this is no coincidence.

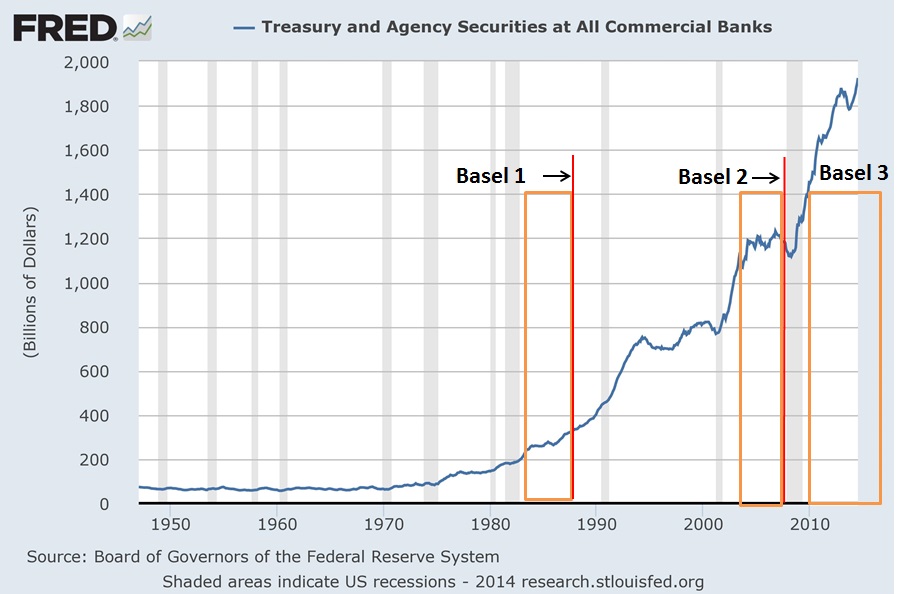

Take a look at the following chart. Until the 1980s, the volume of US government securities on US banks’ balance sheet was pretty much constant. Everything changed from the 1980s onward:

As a share of banks’ total assets (see chart below), US government securities literally spiked after Basel 1 was introduced, only to decline (as a share of total assets) as banks started piling in other assets that benefited from generous capital treatments such as securitisations and insured mortgages (though this doesn’t mean demand faded as banks balance sheets grew quickly over the period, just that demand for other assets was even stronger). Post-crisis, Basel 3 renewed the demand for US sovereign debt as it 1. modified the capital treatment of some previously lowly-weighted assets and 2. introduced minimum liquidity requirements (LCR) as well as margins and collateral requirements that require the use of high-quality liquid assets such as Treasuries.

We identify the same pattern as a share of total securities on US banks’ balance sheet**:

The demand for Treasuries also boomed throughout the financial sector due to those margin/collateral/liquidity requirements that apply (mostly post-Basel 3), not only to commercial banks, but also to broker dealers and investment managers:

All those regulations evidently artificially increase demand for US government-linked securities, pushing their yields down.

But I guess you’re going to tell me that Beckworth’s adjusted risk-free Treasury yield was actually stable over the whole period (chart below). Actually, unlike what Beckworth claims, it does look like there is a slight decline since the end of the 1980s. Moreover, ups and downs almost exactly coincide with banks decreasing/increasing their relative holdings of Treasuries (see above, third chart). Finally, there is also another option: that the natural (risk-free) rate of interest’s trajectory was in fact upward, which would be hidden by financial regulations’ artificially-created demand…

However, this analysis is incomplete: it does not account for foreign banks’ demand for Treasuries, which is also a widely-held asset as part of banks’ liquidity buffers (and in particular when their own sovereign fails…). I unfortunately don’t have access to such data.

In the end, the use of Treasury yield (even adjusted) as an estimate of the natural rate of interest is unreliable given the numerous microeconomic variables that distort its level.

* See this chart from one of my previous posts:

** Post-WW2’s very high figures (close to 100%) reflect the low level of corporate securities issued following the Great Depression and WW2, the high issuance volume of US sovereign debt to fund the war, as well as restrictions on banks’ securities holding to facilitate such wartime issuances.

Macroprudential policy tools: a primer (guest post by Justin Merrill)

In case you hadn’t heard, there’s a new fad in central banking called “macroprudential regulation.” During the Great Moderation there was a belief that low and stable inflation would be sufficient to stabilize financial markets and the economy. When the Great Moderation turned into the Great Recession, this paradigm shifted, but I’m afraid that the wrong conclusions are being drawn. In a series of posts, I shall explain what macroprudential policies are, who some popular people making the arguments for them are and what the risks of the policies are.

Most places I’ve read about macroprudential policies are vague in their description and only list a couple of the tools that central bankers/regulators can use. The policies are intended to prevent systemic risk by preventing/diffusing concentrations of risk. I hope to provide here a nearly comprehensive list of the tools. Conceptually, the tools can be categorized into four categories and theoretically all of the following risks may contribute to asset bubbles or financial instability:

- Leverage/Market Risk

- Reducing leverage is intended to reduce the risk of insolvency in case of a fall in asset prices.

- Liquidity

- Increasing liquidity reduces the risk that payments won’t be made to creditors and may curb fire-sales from credit crunches.

- Credit Quality

- Controlling credit quality intends to prevent future non-performing loans from debtors that would be most susceptible to economic shocks.

- FX/Capital Controls

- FX/Capital controls attempt to prevent hot money from pushing up asset prices and prevents firms from being over-exposed to FX risk from unhedged positions.

Also note that time-varying/dynamic/counter-cyclical rules are a popular concept and can be applied to possibly all of the following tools.

Leverage/Market Risk

- Debt/equity ratios: Also commonly referred to as “capital” in the banking sector. Requiring more funding from equity reduces the risk of insolvency.

- Margin requirements: Determines how much investment can be made with borrowed money. There is a high correlation between margin debt and asset prices.

- Provisioning: Banks account for loss provisions in their financial statements. If they expect losses or are required to hold higher provisions, they will hold a higher equity buffer to offset the losses. If actual losses are less than expected, the bank records a profit.

- Restrictions on profit distribution: If debt/equity ratios are above what regulators want, they may require the firm to retain earnings instead of pay dividends.

- Collateral, hypothecation and haircuts: Regulators may determine which assets may be used as collateral, how much collateral is required for lending, and how much of a haircut is applied to the asset in the repo market. If market prices fall below the repo price the seller may not buy it back. Haircuts (over-collateralization) and margin calls are used to mitigate this risk. Repos and reverse-repos are being increasingly used by central banks as a new tool for an exit strategy from QE and since QE has drained the private markets of credit-worthy assets. Repos also can have broader participation than open market operations (OMOs), the Fed Funds market or deposits at the central banks. OMOs are restricted to primary dealers and deposits at the Fed are restricted to members of the Federal Reserve System and membership is restricted to qualifying commercial banks.

- Too Big To Fail (TBTF) taxes: TBTF taxes have been proposed to reduce the concentration of risk or political power of a single firm as a sort of Pigouvian tax to offset externalities. The taxes could be an assessment on firms whose assets are above an arbitrary cutoff (such as $1 trillion), on firms whose assets exceed a percentage of GDP, or on firms that own above a certain percent of market share.

Liquidity

- Reserve requirements: Reserve requirements are a unique item on this list since they are considered a traditional monetary policy tool. Even though use of changing reserve requirements fell out of favor as a traditional tool, it has gained renewed interest in conjunction with QE, especially in countries with pegged currencies, such as China. This allows the central bank to increase the monetary base without creating price or asset inflation.

- Limits on maturity mismatch: Financial intermediaries such as banks generally engage in maturity transformation by borrowing short and lending long. This can create a funding risk if they are unable to roll over their debts at a reasonable rate. Also, the long dated assets they hold will have more convexity, which means they will be more sensitive to changes in interest rates.

- Liquidity Coverage Ratios (LCR): Basel regulations require financial institutions to hold a level of highly liquid assets to cover their net outflows over a period of time.

Credit Quality

- Caps on the loan-to-value (LTV) ratio: Requiring a larger down payment reduces the risk that the borrower will walk away in case of a decline in property value. It also helps the bank profitably resell the property in case of foreclosure.

- Caps on the debt-to-income (DTI) ratio: DTIs help gauge the borrower’s ability to repay the loan.

- Lending Policies- “No second homes” and risk weighting: Lending policies can target specific sectors of the economy or have specific goals. These can include requiring a larger down payment on second homes, increased risk weightings for real estate, discouraging foreign buyers, and discouraging house flipping by having higher taxes on short term sales.

FX/Capital Controls

- Caps on foreign currency lending: Foreign currency lending that is unhedged exposes the borrower to FX risk.

- Limits on net open currency positions/currency mismatch: Borrowing and investing in different currencies exposes FX risk.

- Capital controls: Capital controls are used to prevent hot money flows in and out of a country that could fuel a boom and bust. Controls are also used for financial repression and increasing domestic investment. Additionally, capital controls are often used in conjunction with a fixed exchange rate, like in China. This is due to the Trilemma. If China wants to peg its currency to the USD and control its domestic interest rate for monetary policy, it must have capital controls. Otherwise, the higher interest rate in China would attract hot money deposits from abroad and there would be an asset boom. The alternatives to a pegged currency with capital controls are a floating exchange rate with free capital or a currency board with free capital.

Links

http://www.imf.org/external/pubs/ft/fandd/basics/macropru.htm

Central banks: an expanding regulatory toolkit

Following my latest post on central banks as the new central planners, a very recent New York Fed Staff Report by Adrian, Covitz and Liang demonstrates the extent of possible central banks’/regulators’ involvement in financial markets, and therefore in what ways they can control, or attempt to control, the allocation of resources within the financial system. Here is a summary of various classes of tools (most of them discretionary) that monetary and financial authorities can play with:

– Monetary policy: the authors classify monetary policy as a “broader tool” that “would affect the rates for all financial institutions”. Indeed, central banks not only set the short-term refinancing rates and reserve requirements and run open market operations, but now also have in place interest rates paid on excess reserves, fixed-rate full allotment reverse repos, as well as various temporary long-term lending facilities such as the BoE’s Funding for Lending Scheme or the ECB’s LTRO and TLTRO, and temporary liquidity facilities such as the ABCP MMF liquidity facility, and can decide what collateral to accept and what securities to purchase, way beyond the traditional Treasury-based OMO.

– Asset markets: central banks can regulate what they view as ‘imbalances’ in the valuation of some asset markets by tightening underwriting standards as well as “through regulated banks and broker-dealers by tightening standards on implicit leverage through securitization or other risk transformations, or by limiting the debt they provide to investors in either unsecured or secured funding markets, if the asset prices are being fuelled by leverage.” In the case of real estate markets and household burdens, central bankers can impose LTV restrictions* and other similar macro-prudential policies.

– Banking policies: central banks have under their control all traditional micro-prudential regulatory tools. In addition, Basel 3 provide them with some flexibility in setting macro-prudential regulatory tools that apply specifically to the banking system, such as counter-cyclical capital requirements (capital conservation buffer, equity systemic surcharge…). Other ad-hoc tools include: sectoral capital requirements (higher/lower capital charges/RWAs for specific asset classes), dynamic provisioning, stress tests…

– Shadow banking policies: harder to regulate, central banks could “address pro-cyclical incentives in secured funding markets, such as repo and sec lending, […] propose minimum standards for haircut practices, to limit the extent to which haircuts would be reduced in benign markets. Other elements of this proposal include consideration of the use of central clearing for sec lending and repo markets, limiting liquidity risks associated with cash collateral reinvestment, addressing risks associated with re-hypothecation of client assets, strengthening collateral valuation and management practices, and improving report, disclosures, and transparency.” Other direct tools include “the explicit regulation of margins and haircuts for macroprudential purposes.”

– Nonfinancial sector: “Tools to address emerging imbalances in asset valuations likely would also address building vulnerabilities in the nonfinancial sector. For example, increasing* [sic] LTVs or DTIs on mortgages, which could reduce a leverage-induced rise in prices, could also limit an increase in exposures of households and businesses to a collapse in prices, thereby bolstering their resilience.”

Given the increased scope of central banks’ operations, it is clear that market prices can be manipulated and distorted in all sort of ways. To be fair however, not all those powers are currently concentrated in the central bankers’ hands. In many countries, there are still a few different institutions that perform those tasks. Nevertheless, the trend is clear: most of those powers are increasingly taken over by and aggregated at central banks.

While this new paper advocates the use of such tools, it admits that their effectiveness and effects on the financial system and the broader economy remains untested and uncertain:

New government backstops to address the risks arising from shadow banking, of course, can be costly. First, an expansion along these lines would require a new regulatory structure to prevent moral hazard, which can be expensive and difficult to implement effectively. Second, an expansion of regulations does not reduce the incentives for regulatory arbitrage, but just pushes it beyond the beyond the existing perimeter. Third, there is a limited understanding of the impact that such a fundamental change would have on the efficiency and dynamism of the financial system.

In a subsequent guest post, Justin Merrill will investigate macro-prudential policy tools more in depth.

* The paper mistakenly describes those potential measures as “increasing” LTV ratios to mitigate house price and household indebtedness increases. I believe this is a typo, even though the same claim reappears several times throughout the paper (if not a typo then the authors have no clue how LTVs work…).

Hummel vs. Haldane: the central bank as central planner

Recent speeches and articles from most central bankers are increasingly leaving a bad aftertaste. Take this latest article by Andrew Haldane, Executive Director at the BoE, published in Central Banking. Haldane describes (not entirely accurately…) the history and evolution of central banking since the 19th century and discusses two possible paths for the next 25 years.

His first scenario is that central banks and regulation will step backward and get back to their former, ‘business as usual’, stance, focusing on targeting inflation and leaving most of the capital allocation work to financial markets. He views this scenario as unlikely. He believes that the central banks will more tightly regulate and intervene in all types of asset markets (my emphasis):

In this world, it would be very difficult for monetary, regulatory and operational policy to beat an orderly retreat. It is likely that regulatory policy would need to be in a constant state of alert for risks emerging in the financial shadows, which could trip up regulators and the financial system. In other words, regulatory fine-tuning could become the rule, not the exception.

In this world, macro-prudential policy to lean against the financial cycle could become more, not less, important over time. With more risk residing on non-bank balance sheets that are marked-to-market, it is possible that cycles in financial assets would be amplified, not dampened, relative to the old world. Their transmission to the wider economy may also be more potent and frequent. The demands on macro-prudential policy, to stabilise these financial fluctuations and hence the macro-economy, could thereby grow.

In this world, central banks’ operational policies would be likely to remain expansive. Non-bank counterparties would grow in importance, not shrink. So too, potentially, would more exotic forms of collateral taken in central banks’ operations. Market-making, in a wider class of financial instruments, could become a more standard part of the central bank toolkit, to mitigate the effects of temporary market illiquidity droughts in the non-bank sector.

In this world, central banks’ words and actions would be unlikely to diminish in importance. Their role in shaping the fortunes of financial markets and financial firms more likely would rise. Central banks’ every word would remain forensically scrutinised. And there would be an accompanying demand for ever-greater amounts of central bank transparency. Central banks would rarely be far from the front pages.

He acknowledged that central banks’ actions have already considerably influenced (distorted?…) financial markets over the past few years, though he views it as a relatively good thing (my emphasis):

With monetary, regulatory and operational policies all working in overdrive, central banks have had plenty of explaining to do. During the crisis, their actions have shaped the behaviour of pretty much every financial market and institution on the planet. So central banks’ words resonate as never previously. Rarely a day passes without a forensic media and market dissection of some central bank comment. […]

Where does this leave central banks today? We are not in Kansas any more. On monetary policy, we have gone from setting short safe rates to shaping rates of return on longer-term and wider classes of assets. On regulation, central banks have gone from spectator to player, with some granted micro-prudential as well as macro-prudential regulatory responsibilities. On operational matters, central banks have gone from market-watcher to market-shaper and market-maker across a broad class of assets and counterparties. On transparency, we have gone from blushing introvert to blooming extrovert. In short, central banks are essentially unrecognisable from a quarter of a century ago.

This makes me feel slightly unconfortable and instantly remind me of the – now classic – 2010 article by Jeff Hummel: Ben Bernanke vs. Milton Friedman: The Federal Reserve’s Emergence as the U.S. Economy’s Central Planner. While I believe there are a few inaccuracies and omissions in Hummel’s description of the financial crisis, his article is really good and his conclusion even more valid today than at the time of his writing:

In the final analysis, central banking has become the new central planning. Under the old central planning—which performed so poorly in the Soviet Union, Communist China, and other command economies—the government attempted to manage production and the supply of goods and services. Under the new central planning, the Fed attempts to manage the financial system as well as the supply and allocation of credit. Contrast present-day attitudes with the Keynesian dark ages of the 1950s and 1960s, when almost no one paid much attention to the Fed, whose activities were fairly limited by today’s standard. […]

As the prolonged and incomplete recovery from the recent recession suggests, however, the Fed’s new central planning, like the old central planning, will ultimately prove an unfortunate and possibly disastrous failure.

The contrast between central bankers’ (including Haldane’s) beliefs of a tightly controlled financial sector to those of Hummel couldn’t be starker.

Where it indeed becomes really worrying is that Hummel was only referring to Bernanke’s decision to allocate credit and liquidity facilities to some particular institutions, as well as to the multiplicity of interest rates and tools implemented within the usual central banking framework. At the time of his writing, macro-prudential policies were not as discussed as they are now. Nevertheless, they considerably amplify the central banks’ central planner role: thanks to them, central bankers can decide to reduce or increase the allocation of loanable funds to one particular sector of the economy to correct what they view as financial imbalances.

Moreover, central banks are also increasingly taking over the role of banking regulator. In the UK, for instance, the two new regulatory agencies (FCA and PRA) are now departments of the Bank of England. Consequently, central banks are in charge of monetary policy (through an increasing number of tools), macro-prudential regulation, micro-prudential regulation, and financial conduct and competition. Absolutely all aspects of banking will be defined and shaped at the central bank level. Central banks can decide to ‘increase’ competition in the banking sector as well as favour or bail-out targeted firms. And it doesn’t stop here. Tighter regulatory oversight is also now being considered for insurance firms, investment managers, various shadow banking entities and… crowdfunding and peer-to-peer lending.

Hummel was right: there are strong similarities between today’s financial sector planning and post-WW2 economic planning. It remains to be seen how everything will unravel. Given that history seems to point to exogenous origins of financial imbalances (whereas central bankers, on the other hand, believe in endogenous explanations, motivating their policies), this might not end well… Perhaps this is the only solution though: once the whole financial system is under the tight grip of some supposedly-effective central planner, the blame for the next financial crisis cannot fall on laissez-faire…

Raising capital requirements? Not that useful

The recent news of the near-bankruptcy of UK-based Cooperative Bank and Portugal-based Banco Espirito Santo made me question the utility of regulatory capital requirements. What are they for? Is raising them actually that useful? It looks to me that the current conventional view of minimum capital requirements is flawed.

In the pre-crisis era, banks were required to comply with a minimum Tier 1 capital ratio of 4% (i.e. Tier 1 capital/risk-weighted assets >= 4%). Most banks boasted ratios of 2 to 5 percentage points above that level. Basel 3 decided to increase the Tier 1 minimum to 6%, and banks are currently harshly judged if they do not maintain at least a 4% buffer above that level.

Indeed, given the possible sanctions arising from breaching those capital requirements, bankers usually thrive to maintain a healthy enough buffer above the required minimum. Sanctions for breaching those requirements include in most countries: revoking the banking licence, forcing the bank into a state of bankruptcy and/or forcing a restructuring/break-up/deleveraging of the balance sheet. Hence the question: what is the actual effective capital ratio of the banking system?

Companies – as well as banks in the past – are usually deemed insolvent (or bankrupt) once their equity reaches negative territory. At that point, selling all the assets of the company/bank would not generate enough money to pay off all creditors (while shareholders are wiped out).

Let’s assume a world with no Tier 1 capital but only straightforward equity, and without regulatory capital requirements. Following the basic rule outlined above, a bank with a 10% capital ratio can experience a 10% reduction in the value of its assets before it reaches insolvency. Let’s now introduce a minimum capital requirement of 6%. The same bank can now only experience a 4% reduction in the value of its assets before breaching the minimum and be considered good for resolving/restructuring/breaking-up by regulators.

For sure, higher minimum requirements have one advantage: depositors are less likely to experience losses. The larger the equity buffer, the stronger the protection.

However, there are also several significant disadvantages.

Given regulators’ current interpretation of the rules, higher minimum requirements also imply a higher sanction trigger. This creates a few problems:

- Raising the minimum threshold does little to protect taxpayers if regulators believe that a bank should be recapitalised, not when its Tier 1 gets close to or below 0%, but when it simply breaches the 6% level. In such case, it might have been possible for the bank’s capital buffer to absorb further losses without erasing its whole capital base and calling for help. For instance, Espirito Santo’s regulators said that its recapitalisation was compulsory: it reported a 5% equity Tier 1 ratio, below the 7% domestic minimum. And the state (i.e. taxpayers) obliged. But… It still had a 5% equity buffer to absorb further losses. Perhaps this would have been sufficient to absorb all losses and spare the taxpayers (perhaps not, but we may never find out).

- When approaching the minimum requirement, bankers are incentivised to start deleveraging in order to avoid breaching. Alternatively, they can be forced by regulators to do so. This has negative consequences on the availability of credit and on the money supply, possibly worsening a crisis through a debt deflation-type bust in order to comply with an artificially-defined 6% level.

- While depositors’ protection can be improved, it isn’t necessarily the case of other creditors, especially in light of the new bail-in rules that make them share the pain (so-called ‘burden-sharing’). Those rules kick in, not when the bank reaches a 0% capital ratio, but when it breaches the regulatory minimum (see here).

- Reaching the minimum requirement can also be self-defeating and self-fulfilling: fearing a bankruptcy event and the loss of their investments, shareholders run to the exit, pushing the share price down to zero and… effectively bringing about the insolvency of the bank. This doesn’t make much sense when a bank still has a 6% capital buffer. Espirito Santo suffered this fate until trading was suspended (see below).

So what’s the ‘effective’ Tier 1 capital ratio? Well, it is the spread between the reported Tier 1 and the minimum regulatory level. A bank that has an 8% Tier 1 under a 4% requirement, and a bank that has a 10% Tier 1 under a 6% requirement have virtually* the same effective capital ratio: 4%.

Regulatory insolvency events also cause operational problems. Espirito Santo was declared insolvent by its regulators but… not by the ISDA association! Setting regulatory minimums at 5% or 25% would have no impact on the issues listed above, as long as this logic is applied. To make regulatory requirements more effective, sanctions in case of breach should be minimal or non-existent in the short-term but should kick in in the long-term if banks’ capitalisation remains too low after a given period of time.

Regulatory minimums exemplify what Bagehot already tried to warn against already at his time: they are bound to create unnecessary panics. Speaking of liquidity reserves (the same reasoning as above applies), he said in Lombard Street:

[Minimums are bad] when legally and compulsorily imposed. In a sensitive state of the English money market the near approach to the legal limit of reserve would be a sure incentive to panic; if one-third were fixed by law, the moment the banks were close to one-third, alarm would begin, and would run like magic. And the fear would be worse because it would not be unfounded—at least, not wholly. If you say that the Bank shall always hold one-third of its liabilities as a reserve, you say in fact that this one-third shall always be useless, for out of it the Bank cannot make advances, cannot give extra help, cannot do what we have seen the holders of the ultimate reserve ought to do and must do.

* ‘virtually’ as, as described above, depositors protection is nonetheless enhanced, though even this is arguable given what happened in Cyprus

Continuously ignoring and misinterpreting history

This recent speech by the Vice President of the ECB, Vítor Constâncio, is in my opinion one of the foremost examples of how a partial reading or misinterpretation of history that becomes accepted as mainstream can lead to bad policy-making.

This speech is typical. Constâncio argues that

the build-up of systemic risk over the financial cycle is an endogenous outcome – a man-made construct – and the job of macro-prudential policy is to try to smoothen this cycle as much as possible. […]

The […] most important source of systemic risk is the risk of the unravelling of financial imbalances. These imbalances may build up gradually, mostly endogenously, and can then unravel abruptly. They form part of the inherent pro-cyclicality of the financial system.

It is crucial to recognise that the financial cycle has an important endogenous component which arises because banks take too much solvency and liquidity risk. The aim of macro-prudential policy should be to temper the financial cycle rather than to merely enhance the resilience of the financial sector ahead of crises.

While Constâncio is right that there is some truth in the pro-cyclicality of financial systems as a long economic boom impairs risk perception, risk assessment and risk premiums, he never highlights why such booms and busts occur in the first place. Outside of negative supply shocks, are they a ‘natural’ consequence of the activity of the economic system? Or are they exogenously triggered by bad government or monetary policies?

Several economic schools of thought have different explanations and theories. Yet, there is one thing that cannot be denied: historical experiences of financial stability.

This is where the flaw of Constâncio’s (and of most central bankers’ and mainstream economists’) thinking resides: history proves that, when the banking sector is left to itself, systemic endogenous accumulation of financial imbalances is minimal, if not non-existent…

According to Larry White in a recent article summing up the history of thought and historical occurrences of free banking, Kurt Schuler identified sixty banking episodes to some extent akin to free banking. White’s paper describes 11 of them, many of which had very few institutional and regulatory restrictions on banking. He quotes Kevin Dowd:

As Kevin Dowd fairly summarizes the record of these historical free banking systems, “most if not all can be considered as reasonably successful, sometimes quite remarkably so.” In particular, he notes that they “were not prone to inflation,” did not show signs of natural monopoly, and boosted economic growth by delivering efficiency in payment practices and in intermediation between savers and borrowers. Those systems of plural note-issue that were panic-prone, like the pre-1913 United States and pre-1832 England, were not so because of competition but because of legal restrictions that significantly weakened banks.

Yet, there is no trace of such events in conventional/mainstream financial history. Central bankers seem to be completely oblivious to those facts (this is surely self-serving) and economists only partially aware of the causes of financial crises. Moreover, free banking episodes also proved that banks were not inherently prone to take “too much solvency and liquidity risk”: indeed, historical records show that banks in such periods were actually well capitalised and rarely suffered liquidity crises. In short, laissez-faire banking’s robustness was far superior to our overly-designed ones’. Consequently we keep making the same mistakes over and over again in believing that a crisis occurred because the previous round of regulation was inadequate…

What we end up with is a banking system shaped by layers and layers of regulations and central banks’ policies. Every financial product, every financial activity, was awarded its own regulation as well as multiple ‘corrective’ rules and patches, was influenced by regulators’ ‘recommendations’, was limited by macro-prudential tools and manipulated through various interest rates under the control by a small central authority. On top of such regulatory intervention, short-term political interference compounds the problem by purposely designing and adjusting financial systems for short-term electoral gains. Markets are distorted in all possible ways as the price system ceases to work adequately, defeating their capital allocation purposes and creating bubbles after bubbles.

Studying banking and financial history demonstrates that it is quite ludicrous to pretend that banking systems are inherently subject to failure through endogenous accumulation of risk. In the quest for an explanation of the crisis, better look at the intersection of moral hazard, political incentives, and the regulatory-originated risk opacity. It might turn out that imbalances are, well, mostly… exogenous.

Please let finance organise itself spontaneously.

Photo: José Carlos Pratas

Recent Comments