NESTA’s alternative finance data goldmine

NESTA, a UK-based charity promoting innovation (and which also organised the annual UK Barcamp Bank), just released its new report on alternative finance trends in the UK. It is a goldmine. The report if full of interesting charts and figures and in many ways tells us a lot about the current state of our traditional financial sector (and possibly of the stance of monetary policy).

Some charts and comments are of particular interest. To my surprise, business lending through P2P platforms was the biggest provider of funds in terms of total amount:

According to the report:

79 per cent of borrowers had attempted to get a bank loan before turning to P2P business lending, with only 22 per cent of borrowers being offered a bank loan. 33 per cent thought it was unlikely or very unlikely that they would have been able to secure funding elsewhere had they not been successful in getting a loan through the P2P business lending platform, whereas 44 per cent of respondents thought they would have been likely or very likely to secure funding from other sources had they not used P2P business lending.

Given bank regulation that penalises banks for lending to small firms, none of this is surprising. As I keep saying, regulation is the primary driver of financial innovation. P2P business lending owes a lot to regulators… until it gets regulated itself?

Another very interesting chart was the following one:

This is crazy. Wealthy people pretty much shun P2P and other alternative finance forms. Why is that? Here’s my theory: wealthy people are usually well advised financially and have access to more investment opportunities than less-wealthy household. Consequently, a low interest environment isn’t that much of a problem (in the short-term): they have the ability to move down the risk scale to look for extra yield. On the other hand, household with more ‘moderate’ incomes do not have access to such investment opportunities: they are the ones hit by low returns on investments. P2P provides them with a unique opportunity to boost the meagre returns on their savings as long as real interest rates remain that low (i.e. lower than inflation):

[The funders] in P2P lending and equity-based crowdfunding were primarily driven by the prospect of financial returns with less concern for backing local businesses or supporting social causes.

Figures concerning P2P consumer lending are similar.

Those figures are both worrying and encouraging. Worrying because the harm that low interest rates and regulation seem to have on the economy and the traditional banking sector. Encouraging because finance is reorganising itself to respond to both borrowers’ and lenders’ demands. This is spontaneous order at work. Let just hope this does not add another layer of complexity and opacity to our already overly-complex financial system.

No, it is low rates that Wall Street ‘hates’

Busy week as I was on the road for business reasons, so no update over the past week.

Noah Smith published an article on Bloomberg arguing that Wall Street doesn’t hate low rates, but hates the Fed. He argues that low rates are beneficial for Wall Street, given that “lower rates mean higher asset values, at least mathematically”. Consequently, he says that the reason why Wall Street doesn’t like low rates is a ‘mystery’. He concludes that:

We may never know exactly why Wall Street hates easy monetary policy with such a violent passion.

I will argue that the only ‘mystery’ here is: why are economists so ignorant about banking and finance?

Unfortunately, and like plenty of central bankers, economists and economic commentators, Noah Smith is guilty of ignoring the margin compression phenomenon. The argument roughly follows those lines: “Why are all those bankers complaining?? Low rates are beneficial! Banks can refinance at lower rates and increase lending volume to boost their profits!” Well, no. I let you refer to my previous posts: under a certain threshold, lowering rates is actually a huge issue for banks, as loan repricing keeps pushing (gross) interest income down while interest expense cannot go down further because deposit funding (and even in certain cases wholesale funding) is stuck at the zero lower bound. Margin falls and net revenues suffer whereas fixed costs remain stable (or even increase due to regulatory and compliance requirements).

What about the buy-side? Surely they must like low rates? Well… to an extent, and more importantly, in the short run, yes. Securities reprice upwards and they make nice mark-to-market gains. Unfortunately for the theory, this is a one-off effect and the portfolio turnover process gets in the way. Fixed income investors, as their securities mature, have to replace them with lower-yielding ones. Investors mostly care about real rates. As their RoI starts trending downward and barely covers inflation, their natural reaction is to go down the rating scale to hunt for yield. This FT article highlights that subprime and leverage loans securitizations have jumped back to pre-crisis highs in the low-interest rate environment. With risk assessment suppressed, asset mispricing is widespread.

In both cases, the key isn’t low rates per se. It is interest rates that fall below a certain threshold.

I’m really wondering whether actual banking experience should become a prerequisite to become a central banker, or whether bank accounting/financial analysis courses shouldn’t be made compulsory for economists and journalists that wish to follow and comment on the banking and financial world…

How short is the economics profession’s memory?

Although prices were not perfectly steady, it is true, they were relatively stable for a period of time longer than any prior period involving comparable conditions. Yet depression ensued, in the face of what the advocates of the older form of monetary theory of the business cycle regarded as the sine qua non of freedom from depression.

It follows particularly from the point of view of the monetary theory of the trade cycle, that it is by no means justifiable to expect the total disappearance of cyclical fluctuations to accompany a stable price-level.

Where do these quotes come from? From any recent critic of inflation targeting, such as David Beckworth, referring to our latest crisis (which followed around two decades of inflation targeting by central banks)?

No. The first one is a 1937 quote from Chester Arthur Phillips, in his Banking and the Business Cycle. The second one is from F.A. Hayek, in his 1933 Monetary Theory and the Trade Cycle. I am sure it is possible to find tons of similar quotes from the pre-WW2 era.

In his book, Phillips has a sub-chapter called ‘Policy of Stabilization of Price Level Tends Towards its Own Collapse’, which is worth quoting here:

The endeavor has been to show that stabilization of the wholesale price level, or of any one price index, is not a proper objective of banking policy of credit control, because aberrations continue to occur in the case of particular types of prices when any one index is sought to be stabilized. […]

Stability of the price level is no adequate safeguard against depression, it is contended, because any policy aimed at stabilizing a single index is bound to set up countervailing influences elsewhere in the economic system. Although the policy of stabilization may appear to be successful for a time, eventually it will break down, because there is no way of insuring that the agencies of control will be able to make their influence at precisely those “points” of strategic importance. As long as economic progress is maintained, resulting in increasing productivity and an expanding total output, there will be an ever-present force working for lower prices. Any amount of credit expansion which will offset that force will find outlets unevenly in sundry compartments of the economic structure; the new credit will have an effect upon the market rate of interest, upon the prices of capital goods, upon real estate, upon security prices, upon wages, or upon all of these, as happened during the late boom. A policy which seeks to direct credit influences at any single index, whether it be of prices, either wholesale or retail, or production, or incomes, in the interest of stabilization, will result in unexpected and unforeseen repercussions which may be expected to prove disastrous in the long run.

What about the following one?

During recent years a number of pseudo-economists have indulged in much glibness about the passing of the “economy of scarcity” and the arrival of the “economy of abundance.” Sophistry of this sort has claimed the public ear far too long; it is high time that the speciousness of such fantastic views be clearly and definitely exposed.

An angry economist about some FT Alphaville blogger? No. Phillips again, in the same 1937 book.

George Selgin posted an old Keynes’ quote two days ago, which may be relevant for some of today’s theorists. Backhouse and Laidler also published a very good paper describing everything that has been ‘lost’ with the IS-LM framework following the post-war Keynesian revolution.

It is slightly scary to see that economics tends to easily forget more ‘ancient’ theories in favour of recent and trendy ones. The same is true regarding banking history: listening to most policymakers makes it clear that past experiences and knowledge have mostly been lost. With such short memories, it is unsurprising that crises occur.

PS: On a side note, George Soros completely misunderstands Hayek. I cannot even believe he could write this article. No, Hayek wasn’t a member of the Chicago School. No, Hayek never believed in the efficient market hypothesis (Hayek didn’t believe in rational expectations). No, Hayek didn’t believe in equilibrium economics but in dynamic frameworks that completely include uncertainty and perpetually fluctuating conditions and agents’ expectations, as well as entrepreneurial experiments (including failures, which are indeed healthy). So… basically the exact opposite of what Soros claims Hayek believed in.

When regulators become defiant of… regulation

After years of regulatory boom, some politicians, and regulators, seem to be – slowly – waking up. I have already described how UK’s Vince Cable seemed to now partially understand that regulation doesn’t make it easy for banks to lend to small and medium-sized businesses, and how Andrew Bailey, from the Bank of England’s Prudential Regulation Authority, complained about the lack of regulatory coordination across country:

I am trying to build capital in firms, and it is draining out down the other side.

Well, Bailey is at it again. Reuters summarized Bailey’s latest speech as:

The over-zealous application of anti-money laundering rules is hampering British banks abroad and cutting off poorer countries from global financial markets, a top Bank of England regulator said on Tuesday.

He said:

We have no sympathy with money laundering, but we are facing a frankly serious international coordination problem. […] We are seeing clear evidence … of parts of the world and activities that are being cut off from the mainstream banking system. […] It cannot be a good thing for the development of the world economy and the support of emerging countries … that we get into that situation. […] I have to spend a large part of my time dealing with the issues that come up in this field … because some of the consequences of the actions taken are potentially existential.

I find it quite ironic to see a regulator disapproving ‘over-zealous’ regulation. Another regulator, Jon Cunliffe, Deputy Governor of the Bank of England, declared that:

Liquidity and market making does seem to have been reduced. […] We’re not sure how much of it is the result of regulatory action, and how much of it is do with the change in business model for the institutions.

While he believes that some of the pre-crisis liquidity was ‘illusory’, his statement clearly indicates that he knows that regulation might not have had only positive effects. (Four days after I spoke about regulatory effects on market liquidity, Fitch published a press release arguing the exact same thing. I still have to write that post…)

Unfortunately, not all regulators are waking up. Reuters reported that David Rule, also from the BoE, said that:

banks had responded to regulatory incentives and increased their focus on the real economy, rather than financial market trading for its own sake.

Really? With business lending stuck at the bottom and mortgage lending (a very productive form a lending to the real economy) booming again? I see.

Andreas Dombret, of the Bundesbank, recently declared in a relatively reasonable speech* that:

But are we really overregulating? If we look at the benefits to society of a stable banking system and the social costs of a banking crisis, I believe the costs of regulation are justifiable.

Clearly he and Bailey should have a proper conversation…

Others, like Andrea Enria, Chairman of the European Banking Authority, which recently ran the European stress tests, warned that

The story is not over, even for the banks who passed it

I am unsure what the goal of that sort of threatening comment is, but I don’t see how this can reintroduce confidence in the European banking system. It certainly will push bankers to consolidate their balance sheet further rather than to start lending more. Let’s not forget that the EBA and ECB tests have the power to create a panic and destabilise markets when nothing would have occurred. Too soft and nobody would trust the tests. Too tough and a panic might set in (imagine the headlines: “Half of European banks at risk of failure!”). Another risk is that investors and commentators stop relying on their own judgment and analysis and start relying too much on regulators’ assessment. This would be extremely dangerous. Yet this already happens to an extent. Perhaps, as more and more regulators start waking up to the potentially harmful side effects of regulatory measures, they will back off and let the market play its role?

* While the speech is overall reasonable, Dombret still comes up with usual myths such as

Yet a leverage ratio would also create the wrong incentives. If banks had to hold the same percentage of capital against all assets, any institution wanting to maximise its profits would probably invest in high-risk assets, as they produce particularly high returns.

This is not correct.

Funnily, he also kind of admitted that regulators did not always understand how banking works, as I’ve been arguing a few times recently:

Do supervisors have to be the “better bankers”? No, absolutely not. Business decisions must be left to those being paid to make them. However, supervisors have to know – and understand – how banking works. Against this background, I personally would very much welcome an increase in the migration of staff between the banking industry and the supervisory agencies.

Still, many regulators influence business decisions…

Martin Wolf’s not so shocking shocks

Martin Wolf, FT’s chief economist, recently published a new book, The Shifts and the Shocks. The book reads like a massive Financial Times article. The style is quite ‘heavy’ and not always easy to read: Wolf throws at us numbers and numbers within sentences rather than displaying them in tables. This format is more adapted to newspaper articles.

Overall, it’s typical Martin Wolf, and FT readers surely already know most of the content of the book. I won’t come back to his economic policy advices here, as I wish to focus on a topic more adapted to my blog: his views on banking.

And unfortunately his arguments in this area are rather poor. And poorly researched.

Wolf is a fervent admirer of Hyman Minsky. As a result, he believes that the financial system is inherently unstable and that financial imbalances are endogenously generated. In Minsky’s opinion, crises happen. It’s just the way it is. There is no underlying factor/trigger. This belief is both cynical and wrong, as proved by the stability of both the numerous periods of free banking throughout history (see the track record here) and of the least regulated modern banking systems (which don’t even have lenders of last resort or deposit insurance). But it doesn’t fit Wolf’s story so let’s just forget about it: banking systems are unstable; it’s just the way it is.

Wolf identifies several points that led to the 2000s banking failure. In particular, liberalisation stands out (as you would have guessed) as the main culprit. According to him “by the 1980s and 1990s, a veritable bonfire of regulations was under way, along with a general culture of laissez-faire.” What’s interesting is that Wolf never ever bothers actually providing any evidence of his claims throughout the book (which is surprising given the number of figures included in the 350+ pages). What/how many regulations were scrapped and where? He merely repeats the convenient myth that the banking system was liberalised since the 1980s. We know this is wrong as, while high profile and almost useless rules like Glass-Steagall or the prohibition of interest payment on demand deposits were repealed in the US, the whole banking sector has been re-regulated since Basel 1 by numerous much more subtle and insidious rules, which now govern most banking activities. On a net basis, banking has been more regulated since the 1980s. But it doesn’t fit Wolf’s story so let’s just forget about it: banking systems were liberalised; it’s just the way it is.

Financial innovation was also to blame. Nevermind that those innovations, among them shadow banking, mostly arose from or grew because of Basel incentives. Basel rules provided lower risk-weight on securitized products, helping banks improve their return on regulatory capital. But it doesn’t fit Wolf’s story so let’s just forget about it: greedy bankers always come up with innovations; it’s just the way it is.

The worst is: Wolf does come close to understanding the issue. He rightly blames Basel risk-weights for underweighting sovereign debt. He also rightly blames banks’ risk management models (which are based on Basel guidance and validated by regulators). Still, he never makes the link between real estate booms throughout the world and low RE lending/RE securitized risk-weights (and US housing agencies)*. Housing booms happened as a consequence of inequality and savings gluts; it’s just the way it is.

All this leads Wolf to attack the new classical assumptions of efficient (and self-correcting) markets and rational expectations. While he may have a point, the reasoning that led to this conclusion couldn’t be further from the truth: markets have never been free in the pre-crisis era. Rational expectations indeed deserve to be questioned, but in no way does this cast doubt on the free market dynamic price-researching process. He also rightly criticises inflation targeting, but his remedy, higher inflation targets and government deficits financed through money printing, entirely miss the point.

What are Wolf other solutions? He first discusses alternative economic theoretical frameworks. He discusses the view of Austrians and agrees with them about banking but dismisses them outright as ‘liquidationists’ (the usual straw man argument being something like ‘look what happened when Hoover’s Treasury Secretary Mellon recommended liquidations during the Depression: a catastrophe’; sorry Martin, but Hoover never implemented Mellon’s measures…). He also only relies on a certain Rothbardian view of the Austrian tradition and quotes Jesus Huerta de Soto. It would have been interesting to discuss other Austrian schools of thought and writers, such as Selgin, White and Horwitz, who have an entirely different perception of what to do during a crisis. But he probably has never heard of them. He once again completely misunderstands Austrian arguments when he wonders how business people could so easily be misled by wrong monetary policy (and he, incredibly, believes this questions the very Austrian belief in laissez-faire), and when he cannot see that Austrians’ goals is to prevent the boom phase of the cycle, not ‘liquidate’ once the bust strikes…

Unsurprisingly, post-Keynesian Minsky is his school of choice. But he also partly endorses Modern Monetary Theory, and in particular its banking view:

banks do not lend out their reserves at the central bank. Banks create loans on their own, as already explained above. They do not need reserves to do so and, indeed, in most periods, their holdings of reserves are negligible.

I have already written at length why this view (the ‘endogenous money’ theory) is inaccurate (see here, here, here, here and here).

He then takes on finance and banking reform. He doubts of the effectiveness of Basel 3 (which he judges ‘astonishingly complex’) and macro-prudential measures, and I won’t disagree with him. But what he proposes is unclear. He seems to endorse a form of 100% reserve banking (the so-called Chicago Plan). As I have written on this blog before, I am really unsure that such form of banking, which cannot respond to fluctuations in the demand for money and potentially create monetary disequilibrium, would work well. Alternatively, he suggests almost getting rid of risk-weighted assets and hybrid capital instruments (he doesn’t understand their use… shareholder dilution anyone?) and force banks to build thicker equity buffers and report a simple leverage ratio. He dismisses the fact that higher capital requirements would impact economic activity by saying:

Nobody knows whether higher equity would mean a (or even any) significant loss of economic opportunities, though lobbyists for banks suggest that much higher equity ratios would mean the end of our economy. This is widely exaggerated. After all, banks are for the most part not funding new business activities, but rather the purchase of existing assets. The economic value of that is open to question.

Apart from the fact that he exaggerates banking lobbyists’ claims to in turn accuse them of… exaggerating, he here again demonstrates his ignorance of banking history. Before Basel rules, banks’ lending flows were mostly oriented towards productive commercial activities (strikingly, real estate lending only represented 3 to 8% of US banks’ balance sheets before the Great Depression). ‘Unproductive’ real estate lending only took over after the Basel ruleset was passed.

The case for higher capital requirements is not very convincing and primarily depends on the way rules are enforced. Moreover, there is too much focus on ‘equity’. Wolf got part of his inspiration from Admati and Hellwig’s book, The Bankers’ New Clothes. But after a rather awkward exchange I had with Admati on Twitter, I question their actual understanding of bank accounting:

While his discussion of the Eurozone problems is quite interesting, his description of the Eurozone crisis still partly rests on false assumptions about the banking system. Unfortunately, it is sad to see that an experienced economist such as Martin Wolf can write a whole book attacking a straw man.

* In a rather comical moment, Wolf finds ‘unconvincing’ that US government housing policy could seriously inflate a housing bubble. To justify his opinion, he quotes three US Republican politicians who said that this view “largely ignores the credit bubble beyond housing. Credit spreads declined not just for housing, but also for other asset classes like commercial real estate.” Let’s just not tell them that ‘Real Estate’ comprises both residential housing and CRE…

Frances Coppola on regulatory arbitrage

Frances Coppola recently wrote an interesting article on the origins of the financial crisis, which reflects several of the points that I have made on this blog time and time again: the crisis is the resulting product of the combination of regulatory arbitrage and interest rates below their natural level (as well as a few other things). I encourage you to read her article (which is at least necessary to follow my own post).

Yet I believe her story isn’t fully accurate. While US banks were subject to a leverage ratio, they were also subject to Basel 1 rules. As I have demonstrated, Basel 1 caused a surge in real estate and sovereign lending, and boosted the use of securitization, through regulatory arbitrage as Basel applied low risk-weights to those asset classes (for the most recent evidence, see here). Unlike what Hyun Song Shin believes, banks were already circumventing the ‘spirit’ of Basel 1 as soon as it was published in 1988… Basel 2 didn’t change much, and its implementation in Europe was anyway too late to have much of an influence on the crisis storyline (which had been building up since the late 1980s).

As a result, I don’t believe that, if European banks had been subject to a leverage ratio, they would not have been able to invest in American securitized products. They would still have done it, and perhaps sacrificed other type of lending or investments in other securities instead. Why? Because RMBSs and other CDOs offered higher yields for lower capital requirements, ceteris paribus. Risk-adjusted profit-maximising banks quickly figure it out.

She concludes:

The story of the financial crisis is a story of the failure of safe assets. That is why it was so traumatic. People expect to take losses on risky investments. They don’t expect to take losses on safe ones. Yet we are still trying to make the financial system “safer” and encourage investors to invest in “safe” assets. When will we learn that the safest investment is a risky one, and the most dangerous investments are those that are believed to be completely safe?

And it is also a warning of the consequences of regulatory arbitrage. The fact that the US and European banks had different regulatory regimes created a golden opportunity for unregulated institutions to exploit, with catastrophic consequences. Yet the US, the UK and the EU are still devising their own systems of regulation with scant regard for international consistency. When will we learn that an international industry requires international regulation?

I would say that the crisis wasn’t a failure of safe assets per se. It was a failure of regulation that wanted us (or actually, forced us) to believe that some assets were safe, creating a vicious spiral as banks piled into those asset classes to maximise their return on regulatory capital.

Moreover, regulatory arbitrage isn’t a cross-border issue. Most countries experienced the same symptoms: increasing real estate prices and securitization-issuance volumes, and lower sovereign debt yields. This points to intra-Basel distortions within countries, not to extra-Basel arbitrage across countries. Regulatory arbitrage-driven financial imbalances are endogenous to Basel regulations. Cross-border arbitrage, the Euro, populist politics (which never dies, as US politicians – incredibly – want to revive Fannie and Freddie…), also played a secondary (and surely exacerbating) role, but they were not at the very root of the crisis.

PS: Frances just published a new article on the ECB stress tests. I don’t disagree with her, but I believe that it is easy to criticise the test in hindsight, once we found out the number of banks that failed: she could have attacked the methodology at the time it was published. She also missed that, if banks don’t increase lending post-result announcements, it isn’t necessarily because they are zombies (some may well be). But the test was run on phased-in Basel 3 CET1 figures, not fully-loaded ones. Many banks still have large capital adjustments/deleveraging to make before complying with fully-loaded Basel 3 requirements, which isn’t going to help lending growth, especially given that banks currently don’t cover their cost of capital. (Another inconsistency of the test is that some banks were tested against fully-loaded ratios, and in the end obviously appeared uglier than if they had been tested against the same standards as other banks. If all banks had been tested against fully-loaded capital ratios, 36 would have failed)

The Economist on mobile payments and market liquidity

The Economist recently published an article on mobile payment, which is suspicious of its success to say the least:

The fragmentation [of mobile payment systems] confuses merchants and consumers, who have yet to see what is in it for them. From their perspective, the current system works well. Swiping a credit card is not much harder than tapping a phone. Nor is it too risky, especially in America, since credit cards are protected against fraud. Upgrading to a new system is a hassle. Merchants have to install new terminals. Consumers need to store their card details on their phones, but still carry their cards around, since most stores are not yet properly equipped.

I believe the newspaper is too pessimistic. Yes, swapping credit cards is easy. But then it involves signing a bill (not the fastest and most modern system ever) and the card can be replicated. Hence why most of the rest of the developed world has moved to a ‘chip and pin’ form of card payment, which is only slightly more burdensome (and not very fast either). The US is also taking the same direction.

Most people who have recently swapped their ‘chip and pin’ card for a contactless one can witness how convenient and quick the new system is. Yet, they also believed that the previous system “worked well”. Following the same argument, it would have been hard to convince people to switch to cards since carrying cash also “worked well” (ok, it’s not as strong an argument). Switching to smartphone-based contactless payment would make the system as fast, yet reduce the number of cards and devices one carries.

The Economist continues:

But even Apple’s magic may not be enough to make mobile payments fly. It is not clear how merchants will benefit from Apple’s new ecosystem: it does not offer them lower fees for processing payments or useful data about their customers, as CurrentC does. As a result, they may refuse to sign up for Apple Pay or discourage its use.

Yet, as described above, speed is mobile payment’s major asset. Any retailer regularly experiencing long queues is likely to lose customers. Contactless cards already speed up the checkout process considerably. Unfortunately, they are usually capped to pay small amounts (GBP20 in the UK). Contactless mobile payment/NFC systems would remove that cap.

In another article, The Economist once again highlights its ambivalent stance towards regulation:

But the illiquidity problem will still be there when the next crisis occurs. In a sense, it is a problem caused by regulators; they wanted banks to be less exposed to the vicissitudes of markets. But you cannot make risk disappear altogether; you can only shift it to another place. Get ready for more moments of sheer market terror.

The article refers to the recent market turbulence and points to regulatory requirements that have made lack of liquidity a rather new problem:

Due to new regulatory restrictions and capital rules that make bond-trading less profitable, banks have cut back their inventories to the level of 2002, even though the value of bonds outstanding has doubled since then (see chart).

That is a problem when trading surges, as it did between October 10th and 16th, when volumes rose by 67%. “Credit is not a continuously priced market,” says Richard Ryan of M&G Investments, a fund manager. “When a bond price falls from 100 to 90, it won’t do so smoothly, but in big drops.”

This is correct. Market-making (mostly fixed income) is becoming trickier because harsher capital requirements make it more expensive to carry a large inventory of bonds through three channels: 1. deleveraging, as banks are pushed towards higher regulatory capital ratios (and as the new leverage ratio is introduced), 2. credit risk, as credit risk-weights are on upward trend, 3. market risk, as holding larger inventories penalise banks through higher market RWAs than before. I may write a whole post on this topic soon.

But the newspaper forgets liquidity requirements: banks are required to hold enough very liquid assets on their balance sheet (‘liquidity coverage ratio’). Given the combination of leverage and liquidity constraints, banks have to sacrifice other asset classes: the riskier bonds. This leads to the following very good chart, from a Citigroup report and reported by Felix Salmon at Reuters:

This has been an issue with The Economist since the start of the crisis: the same newspaper declares that banks needs to be regulated and safer and complains about the negative effects of regulation at the same time. Perhaps time to be less contradictory?

PS: The ECB published its stress test results yesterday. I won’t comment on them. I just thought the AQR was an interesting exercise, but its consequences must be carefully weighted and it is crucial not to over-interpret them (I’ve already written about the danger of ‘harmonizing’ assessments across multiple jurisdictions and cultures).

Blurry banks’ future is

A lot of articles on financial innovation and disruption in the FT over the last few days. Here, John Gapper argues that tech firms aim at using the existing financial system rather than challenge it. Here, Martin Arnold argues that banks shouldn’t forget their traditional branch network as this is how they make money through their oldest and wealthiest clients. Here, Luke Johnson argues that crowdfunding is riskier but also more exciting and, in a way, is the future.

John Gapper is right to point out that the regulatory and capital costs of setting up new bank-alike lending entities are very high. Yet he probably overstates his case. P2P lenders do not provide bank-type services: technology has enabled disintermediation by allowing investors to lend money (almost) directly to borrowers, but the money invested is stuck and does not represent a means of payment, unlike bank deposits. P2P lenders have the ability to take over a large market share of the lending market; and their business model does not require a high operating, regulatory and capital costs base (at least for now…). This is where the traditional intermediated lending channel could effectively approach death. On the other hand, P2P lender cannot handle deposits and banks still have a near-monopoly in this area.

Of course, we could imagine a 100%-reserve banking world in which the lending channel has moved entirely to P2P lenders, mutual and hedge funds and equivalent, whereas the deposit and payment system has moved entirely to Paypal-like payment firms. And this excludes alternative options offered by cryptocurrencies. In this world, banks are effectively dead.

Still, I am far from sure this would be the best solution: banks provide an elastic supply of currency (fractional reserve banking) that can adapt to the demand for money. (We could imagine a world without banks but still an elastic currency supply, if for instance the whole money supply only comprised competing cryptocurrencies. Let’s say this is highly unlikely to happen in the foreseeable future)

Banks can also survive by benefiting from those technologies (if ever they dare touching their antique IT systems…). As I’ve been saying for a while, banks can leverage their huge customer base to set up their own P2P/crowdfunding platform. This has already started to happen: RBS just announced the creation of its own P2P lending platform, Santander announced a partnership with Funding Circle, Lending Club is developing partnerships with many US banks. Banks could earn a fee from referring customers to their own (or third-party) platform, while deleveraging and reducing their on-balance sheet credit risk. Investors would earn more on those investments than on time deposits, but bear some risk.

Whatever they decide to do, banks will have to adapt. But timing is key. Gapper referred to this recent, excellent, Deloitte report. They explain the margin compression effect (due to low base rates)*, which depresses banks’ profitability and adds another challenge on top of those that tech-enabled competitors and regulation already represent. According to them, closing down branches and moving online does not sufficiently slash cost to offset the decrease in net interest income. Closing down branches too quickly could also hurt banks by alienating the part of their client base born before the internet age. Deloitte provides evidence that a radical restructuring of IT systems could significantly improve returns, but this requires investments, which banks aren’t necessarily willing to undertake in a period of below-cost of capital RoE.

As the internet makes it easier for customers to compare pricing through aggregators and hence more difficult for banks to ‘extract value’ from them (what they call ’privileged access’), they recommend banks enhance ‘customer proposition’ (i.e. use ‘big data’) and focus on SME lending. As I’ve argued on this blog, capital regulation makes this difficult. They also indeed support the idea of in-house P2P platform, mostly to focus on local SMEs. This would help with capital requirements by maintaining SME exposures off-balance sheet, the risk borne by customers. Banks could effectively become risk assessment providers: rating lending opportunities to help customers (which include investment funds that don’t have such in-house capabilities) make their investment choices.

At the end of the day, banks are indeed likely to die if they don’t adapt. But also if they adapt too quickly. We could however see in the future surviving banks increasingly becoming like non-banks and non-banks increasingly providing banking services. The distinction between both types of institutions is likely to get very blurry. (That is, if regulation doesn’t kill non-banks first)

* Ben Southwood reiterated that interest rates are determined by markets and not by central banks. I already wrote responses to those claims here and here. Scott Sumner just mentioned his latest post, so I thought it would be a good idea to share Deloitte’s insight and own explanation of the margin compression effect and why “the spreads between Bank Rate and market rates seem to be narrow and fairly consistent—until they’re not.” In reality, lending spreads fluctuate only slightly when rates are above a certain threshold (i.e. banks’ risk-adjusted operating costs) and widen when they drop below it (explaining the “until they’re not”; see my previous posts). The fact that the “until they’re not” occurs does not imply that lending rates are “determined by the market”.

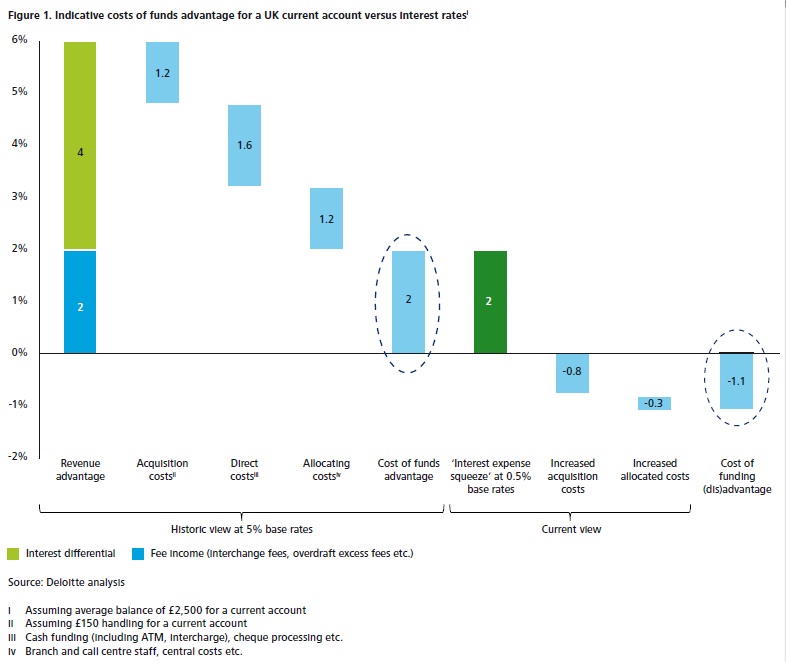

Here’s Deloitte own version:

The interest rate paid by banks on current accounts is typically lower than those paid for lump sum deposits (and the rates paid to borrow in the wholesale markets). However, this interest rate does not reflect the full cost of acquiring and servicing these current accounts. In the past, these acquisitions and servicing costs were offset by the fact that banks did not have to pay very high interest rates on current accounts.

Until the financial crisis, central bank interest rates (the ‘base rate’) were traditionally much higher. This meant that current account rates could easily be 500 or more basis points (hundredths of a percentage point) below lump-sum deposit rates.

Because base rates are at unprecedented lows, that maths does not work. Base rates have been low since 2009, and central bankers have signalled that they are likely to stay that way for some time yet. Figure 1 shows the economics of current accounts in the UK, where banks typically do not charge for them. A 200 basis point margin generated by current accounts when base rates are at 5 per cent turns into a 110 basis point loss at a 0.5 per cent base rate.

New research confirms the role of regulation and housing in modern business cycles

I think readers will find it hard to imagine how excited I was yesterday when I discovered (through an Amir Sufi piece in the FT) a brand new piece of research called: The Great Mortgaging: Housing Finance, Crises, and Business Cycles

(The authors, Jordà, Schularick and Taylor (JST), also published a free version here, and a summary on VOX)

I wish the authors had read my blog before writing their paper as it confirms many of my theses (unless they had?). It’s so interesting that I could almost quote two thirds of the paper here. I obviously encourage you to read it all and I will selectively copy and paste a few pieces below.

In my recent piece on updating the Austrian business cycle theory (ABCT), I pointed out that the nature of lending (and banks’ balance sheets) had changed over time since the 19th century (and particularly post-WW2), mainly due to banking regulation and government schemes. I had already provided a revealing post-WW2 chart for the US to demonstrate the effects of Basel 1 on business and real estate lending volumes.

JST went further. They went further back in time and gathered a dataset of disaggregated lending figures covering 17 developed countries over close to 140 years. Their conclusions confirm my views. Regulations – and in particular Basel – changed everything.

Here is their aggregate credit to GDP chart across all covered countries, to which I added the introduction of Basel 1 as well as pre-Basel trends:

I don’t think there is anything clearer than this chart (I’m not sure that securitized mortgages are included, in which case those figures are understated). Since the 1870s, non-mortgage lending had been the main vector of credit and money supply growth, and mortgage lending represented a relatively modest share of banks’ balance sheet. Basel turned this logic upside-down. How? I have already described the process countless times (risk-weights and capital regulation), so let see what JST say about it:

Over a period of 140 years the level of non-mortgage lending to GDP has risen by a factor of about 3, while mortgage lending to GDP has risen by a factor of 8, with a big surge in the last 40 years. Virtually the entire increase in the bank lending to GDP ratios in our sample of 17 advanced economies has been driven by the rapid rise in mortgage lending relative to output since the 1970s. […]

In addition to country-specific housing policies, international banking regulation also contributed to the growing attractiveness of mortgage lending from the perspective of the banks. The Basel Committee on Bank Supervision (BCBS) was founded in 1974 in reaction to the collapse of Herstatt Bank in Germany. The Committee served as a forum to discuss international harmonization of international banking regulation. Its work led to the 1988 Basle Accord (Basel I) that introduced minimum capital requirements and, importantly, different risk weights for assets on banks’ balance sheets. Loans secured by mortgages on residential properties only carried half the risk weight of loans to companies. This provided another incentive for banks to expand their mortgage business which could be run with higher leverage. As Figure 1 shows, a significant share of the global growth of mortgage lending occurred in recent years following the first Basel Accord.

I wish they had expanded on this topic and made the logical next step: Basel helped set up the largest financial crisis in our lifetime through regulatory arbitrage. Nevertheless, the implications are crystal clear.

To JST, this growth in real estate lending is the reason underlying our most recent financial crises:

We document the rising share of real estate lending (i.e., bank loans secured against real estate) in total bank credit and the declining share of unsecured credit to businesses and households. We also document long-run sectoral trends in lending to companies and households (albeit for a somewhat shorter time span), which suggest that the growth of finance has been closely linked to an explosion of mortgage lending to households in the last quarter of the 20th century. […]

Since WWII, it is only the aftermaths of mortgage booms that are marked by deeper recessions and slower recoveries. This is true both in normal cycles and those associated with financial crises. […]

The type of credit does seem to matter, and we find evidence that the changing nature of financial intermediation has shifted the locus of crisis risks increasingly toward real estate lending cycles. Whereas in the pre-WWII period mortgage lending is not statistically significant, either individually or when used jointly with unsecured credit, it becomes highly significant as a crisis predictor in the post-WWII period.

JST confirm what I was describing in my post on updating the ABCT: that is, that banks don’t play the same role as in early 20th century, when the theory was first outlined:

The intermediation of household savings for productive investment in the business sector—the standard textbook role of the financial sector—constitutes only a minor share of the business of banking today, even though it was a central part of that business in the 19th and early 20th centuries.

JST describe the post-WW2 changes in mortgage lending originally as a result of government schemes to favour home building and ownership, followed by international regulatory arrangements (Basel) from the 1980s onward. Those measures and rules led to a massive restructuring of banks’ balance sheet, as demonstrated by this chart:

While the empirical findings of this paper will be of no surprise to readers of this blog, this research paper deserves praise: its data gathering and empirical analysis are simply brilliant, and it at last offers us the opportunity to make other mainstream academics and regulators aware of the damages their ideas and policies have made to our economy over the past decades. It also puts the idea of ‘secular stagnation’ into perspective: our societies are condemned to stagnate if regulatory arbitrage starve our productive businesses of funds and the only way to generate wealth is through housing bubbles.

While the empirical findings of this paper will be of no surprise to readers of this blog, this research paper deserves praise: its data gathering and empirical analysis are simply brilliant, and it at last offers us the opportunity to make other mainstream academics and regulators aware of the damages their ideas and policies have made to our economy over the past decades. It also puts the idea of ‘secular stagnation’ into perspective: our societies are condemned to stagnate if regulatory arbitrage starve our productive businesses of funds and the only way to generate wealth is through housing bubbles.

China’s Frankenstein banking system keeps growing

Financial regulation in China is quite a mess. China seems to be the world testing ground for some of the most ridiculous banking rules. With all their related unexpected consequences.

Take this recent story: some time ago, Chinese regulators found it clever to cap Chinese banks’ loans/deposits ratios at 75% by the end of each quarter (it isn’t). The goal was to ensure that banks have enough liquidity to face large cash withdrawals. Nevermind that loans/deposits only take into account loans from the asset side of the balance sheet and that banks can use depositors cash to invest in many different sorts of assets (from liquid sovereign bonds and short-term repos to very illiquid securities). Perhaps Chinese banking rules forbid some of those investments (I am not an expert on the Chinese banking system). The fact that the rule was only enforced at quarter-end seemed not to be a problem either (arbitrage anyone?), or that the news that a bank hadn’t complied with the rule could trigger a panic.

Nevertheless, as usual with China, the spontaneous financial order reacts. As the FT reports:

In recent years, the final few days of each quarter have become a nervous time for banks. As liquidity has tightened and many depositors have shifted their savings into higher-yielding substitutes such as Alibaba’s online money-market fund, Yu’E Bao, many lenders have struggled to attract enough traditional deposits to stay below the maximum 75 per cent loan-to-deposit ratio.

That regulation, intended to ensure banks keep enough cash on hand to meet withdrawal demand, is enforced at the end of each quarter – providing an incentive to window-dress deposit totals. This was exacerbated by the desire to prettify quarterly reports to shareholders.

To meet the deposit challenge, many banks resorted to an all-hands-on-deck approach, requiring employees to meet a deposit target. That meant urging clients – and even family and friends – to transfer funds into the bank, typically only for a few days covering the quarter-end period.

Typical example of a rule that, not only introduces opacity, but also creates unintended consequences.

But the story isn’t over.

Chinese regulators didn’t really appreciate that bankers were trying to bypass their well-thought-out rule. They came up with another very ‘clever’ rule to fix the flawed rule:

Regulators will suspend business approvals to banks whose month-end deposit total deviates by more than 3 per cent from the daily average over the previous month.

Problem solved. Not.

To the uncertainty and unintended consequences of the previous rule, they added further uncertainty and unintended consequences. Nevermind that such a rule would limit competition for deposits (Chinese banks are for now forbidden to compete on price – this is about to change –, but can well use other means and advantages). A larger deposit inflow could well happen for any reason (run on a competitor, or simply good news about the financial strength of a bank leading to an inflow of new customers). Penalising banks for such reason sounds rather dubious to say the least.

One of the consequences is that banks now turn away deposits…

The rule can also easily trigger instability, as the FT adds:

A light-hearted commentary circulated among bankers on social media on Wednesday, carrying the headline “If there’s a bank you hate, send them all your money before 12 tonight”.

I’m sure Chinese people, with their usual banking rule-avoiding ingenuity, will soon enough find a way to use all the loopholes created by this combination of definitely very clever regulations. And that regulators, in turn, will come up with another rule to patch the rule that patched the rule. The Frankenstein experiment continues.

Recent Comments