Misunderstanding the net interest margin

Lately, there have been a lot of discussions in the media and in the academic sphere surrounding banks’ net interest margin in the low (or negative) interest rate environment. I have explained before how lowering interest rates below a certain threshold led to ‘margin compression’ (see here), which in turned depressed banks’ profitability and hence their internal capital generation, solidity and ability to lend.

The net interest margin (NIM thereafter) is roughly the difference between the average interest rate earned on assets and the average interest rate paid on funding, and is usually defined as

Net interest income / average earning assets, with NII being the difference between interest income (from loans and securities mostly) and interest expense (on deposits and other types of debt/funding instruments)

We now see conflicting articles and research pieces on the effects of low rates on banks’ NIM (see two of the most recent ones by the St Louis Fed here and other Fed researchers here). But, to my knowledge, most, if not all of those pieces make the same fundamental mistake: they do not look at risk-adjusted NIMs.

‘Risk adjustment’ is a critical concept but sadly often overlooked in the literature. I once defined the interest rate on a loan as the following:

LR = RFR + IP + CRP – C,

where LR is the loan rate, RFR is the applicable, same maturity, risk-free rate, IP the expected inflation premium, CRP the credit risk premium that applies to that particular customer and C the protection provided by the collateral (which can be zero).

As I explained elsewhere, margin compression occurs when the risk-free rate declines so much that interest rates banks pay on their funding reaches the zero lower bound while their interest income continues to decline (which led me to hypothesise that the zero-lower bound was actually a ‘2%-lower bound’ in the case of the banking/credit channel of monetary policy). This however assumes no fundamental change in the rest of the economy’s credit (or default) risk.

Indeed, in bad economic times, the CRP usually increases for most borrowers, partially offsetting the effects of the decline in the risk-free rate on new lending. Moreover, bankers can easily boost their NIM by lending relatively more to higher-risk customers or investing in higher-risk projects, even in good economic times. Consequently, it looks like the headline NIM isn’t suffering or declining that much. It can sometimes even improve, in particular when economic conditions are benign. For instance, emerging market banks often boast high NIMs, but also high default rates (and high ‘losses given default’). In such cases, margin compression seems not to be occurring. But this is just an accounting illusion.

See the example in the chart below, which represents the hypothetical evolution of the different components of a given unsecured loan rate throughout a long recession:

Once you adjust the NIM for the loan book’s underlying risk, the story is different. Banks’ interest income can rise but the risk of default on new lending, as well as that of their legacy loan portfolio, also rises. Because the CRP is often fixed at inception, legacy lending now underpays relative to its risk profile, potentially implying economic losses down the line.

Most studies don’t factor this phenomenon in. They look at unadjusted NIMs, which in many cases do not provide any useful information.

A very good and quite recent paper on banking mechanics by Claudio Borio and his team (The influence of monetary policy on bank profitability), which looks at the impact of the shape of the yield curve on margin compression and banks’ profitability, does understand that accounting plays a significant role:

The second form [of dynamic effects in the transmission of the level of interest rates to net interest income], which is more relevant, relates to accounting practices. Any interest margin on new loans also covers expected losses. But provisions in the period we examine follow the “incurred loss model”, so that, in contrast to interest rates, they are not forward-looking. As a result, extending new loans raises profitability temporarily, since losses normally materialise only a few years later at which point loans also become non-performing, eroding the interest margin. This also means that if lower market rates induce more lending, they will temporarily boost net interest margins. The strength of this effect will depend on background economic conditions. For instance, it is likely to be weak precisely when interest rates are unusually low and the demand for loans anaemic.

However, they stop short of providing a solution, or a correction, to this effect. To be fair, risk-adjusted NIMs are not directly observable and very difficult to estimate, given that disclosures about banks’ loan portfolio are very limited and that only some of their customers (i.e. large corporates) have bonds or credit default swaps traded on the secondary market. Therefore, some analysts use the following ex-post adjusted NIM ratio:

(Net interest income – loan impairment charges) / average earning assets

Default risk, expressed in the income statement by loan impairment charges (LICs – also called loan-loss provisions), is directly deducted from net interest income, making the NIM easier to compare across banks or countries. But even this version can be highly inaccurate, as LICs are backward-looking and depend on each bank’s accounting policies. In the short-run, some banks tend to over-provision, others to under-provision.

You’ve reached the end of this post perhaps wondering whether I had a solution to this problem. Unfortunately no, I don’t. But I believed that a clarification was in order. In finance, or economics in general, any decision involves risk-taking, and studies that do not take risk into account must be taken with a pinch of salt.

PS: The inflation premium is stripped out of the risk-free rate in this post, but in practice benchmark market rates such as Treasuries already factor in inflation expectations.

This post was re-published on Alt-M.

On ‘shadow money’

The shadow banking literature has vastly and rapidly expanded since the financial crisis, and has produced some interesting pieces, as well as some exaggerated claims, in my view. While I am not writing today to address those claims, I still wish to question a closely linked concept that has simultaneously sprung up in the literature and in particular in the post-Keynesian one: shadow money.

One of the most elaborated and comprehensive academic research papers on this particular topic is the recently published Gabor’s and Vestergaard’s Towards a theory of shadow money. It’s an interesting and recommended piece. But while I agree with some of their writings, I have to find myself in disagreement with a number of their points and examples* and in particular their central claim: that repurchase agreements (‘repos’ thereafter) are shadow money; that is, a type of monetary instrument used within the shadow banking system.

For some readers that might not know how a repo works, below is a concise definition provided by the IMF:

Repo agreements are contracts in which one party agrees to sell securities to another party and buy them back at a specified date and repurchase price.48 The transaction is effectively a collateralized loan with the difference between the repurchase and sale price representing interest. The borrower typically posts excess collateral (the “haircut”). Dealers use repos to borrow from MMFs and other cash lenders to finance their own securities holdings and to make loans to hedge funds and other clients seeking to leverage their investments. Lenders typically rehypothecate repo collateral, that is, they reuse it in other repo transactions with cash borrowers.

Given repos’ (and their asset counterpart: reverse repos) properties, my view is that repos aren’t shadow money but a shadow funding instrument. While it might not sound such a big issue, I believe the distinction is important from an analytical perspective as well as to avoid confusion. Let me elaborate.

Gabor and Vestergaard define shadow money as “repo liabilities, promises backed by tradable collateral.” According to them, shadow money has four key characteristics:

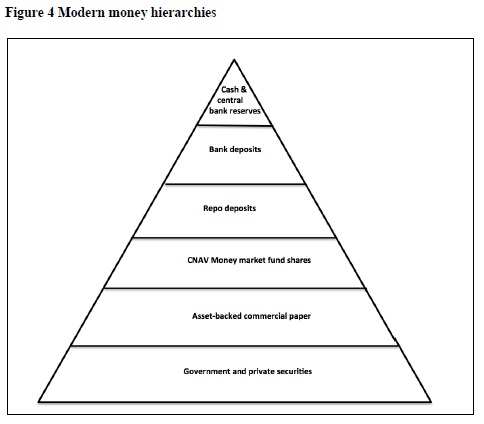

a) In modern money hierarchies, repo claims are nearest to settlement money, stronger in their ‘moneyness’ than ABCPs or MMF shares.

b) Banks issue shadow money. The incentives to issue repos are incentives to economize on bank deposits and bank reserves.

c) Shadow money, like bank money, relies on sovereign structures of authority and creditworthiness. The state offers a tradable claim that constitutes the base asset supporting the issuance of shadow claims.

d) Repos create (and destroy) liquidity at lower levels in the hierarchy of credit claims.

They offer this chart of ‘modern’ money hierarchy:

I have to object to repos being classified as ‘money’.

Money, as typically defined by economists, has three characteristics: it is a medium of exchange, a unit of account and a store of value. High-powered money (the ‘outside money’ of the financial system) currently fits this definition, as a final settlement medium.

The ‘moneyness’ concept, a term now popularised by JP Koning’s excellent blog, asserts that various types of assets have various degrees of money-like properties. In this quite old but classic post, JP argues that anything from beers and cattle to deposits benefits from some degree of moneyness. In another old post, Cullen Roche provided the following good ‘money spectrum’ chart (although I’d disagree with his outside money/deposit ranking):

Therefore, most goods and assets have some monetary properties: some can be used as media of exchange or store of value. All represent a claim of some sort on money proper. As a general (but inaccurate) rule, the more their price in terms of outside money fluctuate, and hence their conversion risk raises, the further away they are on the moneyness scale. But conversion (almost) on demand also implies that, in order to have some money characteristics, a good or asset needs to be tradable.

Now let’s get back to repos as shadow money.

Repos are a liability issued by the debtor in exchange for high-powered money, of which reverse repos are the asset counterpart held by the creditor (and hence the claim on the high-powered money originally transferred, plus interest). The debtor also transfers an extra asset (i.e. the collateral) to the creditor for security purposes at a pre-agreed haircut depending on its credit quality and market risk sensitivity.

We get here to the main point of this post: repos have little money-like property due to their non-tradability and lack of on-demand convertibility.

Indeed, a repo liability is of course non-tradable, in the same way that any debt that one owes cannot be traded for another type of liability. It can only be refinanced and/or extinguished. A reverse repo (or repo claim) however, could potentially have tradable properties, allowing a creditor to exchange his claim almost instantaneously on the market. Problem is: this does not happen. Unlike bonds or other assets, and due to the very specific features of such private agreements, there is no secondary market for repo claims. Once a repo has been agreed upon, the contract is fixed between the two parties until maturity (or default). Consequently, repo claims can effectively be assumed to have no liquidity.

Seen this way, it is hard to classify repos as ‘money’, and they certainly do not deserve their third place in the moneyness hierarchy above. So what are repos? As I previously said, they are a funding instrument. Given that the shadow banking system makes use of repos on a large scale, we can potentially call them a ‘short-term secured shadow funding instrument’. And please note that repo issuance isn’t limited to banks and broker-dealers; other institutions also use them.

You’ll be tempted to reply: “what about deposits? They have no secondary market and are not tradable either.” This isn’t strictly accurate. While they are both promises to pay a certain amount of money proper at a certain date, there is a very specific difference between deposit liabilities (‘on demand’ ones especially) and repo liabilities. Banks themselves are deposits’ secondary market: deposits can be ‘traded’ within the bank’s own balance sheet and swapped for cash on demand. And when dealing with a counterparty that does not hold an account with the same bank, banks take over the responsibility of transferring the underlying funds (i.e. high-powered money).

If repos aren’t ‘money’, what else could be considered ‘shadow money’? Well, assets provided as collateral do have liquidity, tradability, and therefore some ‘moneyness’. Those assets can sometimes be used in further transactions. This is why I am wondering whether or not there isn’t some confusion with ‘shadow money’ proponents’ terminology. While their writings clearly emphasise the ‘shadow money’ nature of repos themselves (and Poszar seems to be using the same definition here), many other academic authors have instead referred to the most commonly-used types of repo collateral (high quality and highly liquid sovereign and corporate bonds) as ‘shadow money’ (which indeed makes more sense to me, although I do not fully adhere to this concept either).

There are plenty of things worth discussing regarding this theory of shadow money and the use of repos in general, but the money-like properties of repurchase agreements isn’t one of them. Let’s focus on their funding properties instead.

*I also believe that their shadow money expansion theory is subject to the same critique as other endogenous outside money theories, such as MMT’s.

PS: the fact that repos are backed by marketable collateral does not confer any specific monetary property to repo claims. Marketable collateral is used in many other types of lending transactions, in particular in private banking-type lending. Also, repos and any other collateralised lending are expected to be repaid at par, independently of the valuation fluctuations of their underlying collateral.

PPS: Baker and Murphy build on Gabor’s and Vestergaard’s piece and just published a blog post that argues for a new ‘investment state’, in a typical post-Keynesian interventionist fashion.

This post was re-published on Alt-M.

What China can teach us about the future of banking

A few weeks ago, Citi published a quite fascinating 100-page report on financial innovations, from blockchain to P2P lending, in various regions of the world. It’s a highly recommended and very comprehensive reading that I won’t be able to summarise in a short blog post.

From this report, it is clear that China’s financial system has adopted innovations at a much faster pace than the Western world. And if there is a defining characteristic of the Chinese system, it is its very erratic and repressive regulatory framework, which made me once call China a ‘spontaneous Frankenstein banking system’:

Financial regulation in China is quite a mess. China seems to be the world testing ground for some of the most ridiculous banking rules. With all their related unexpected consequences.

In an earlier post, I also highlighted that

China is an interesting case. Underneath its very tight government-controlled financial repression hide numerous financial experiments aimed at bypassing those very controls. The Chinese shadow banking system is now a well-known financial Frankenstein, with multiple asset management companies, wealth management products and other off-balance sheet entities providing around half the country’s credit volume. The more the government tries to regulate the system, the more financial innovation finds new workarounds and become increasingly more opaque.

We already knew that the Chinese financial system was completely distorted from years of regulatory repression and crony capitalism, as a whole new report on finance in China by The Economist demonstrates (see the editorial here, and the report starting here). Echoing my worries, The Economist calls for China to ‘free up’ its ‘financial jungle’. Citi’s and The Economist’s reports now allow us to quantify the effects of those distortions. Indeed, China leads the world in fintech and digital disruption in general; it has some of the largest fintech firms and, as Citi said, it is now ‘past the tipping point’.

While its very large e-commerce has been a strong driver of the rise of alternative payment providers in the country, Citi points at a number of other factors that have facilitated the rise of those third-party payment companies, among which an under-developed banking system viewed by the public as quite unreliable (unsurprising given how tightly controlled banking is in China, which has stifled customer-oriented innovation), and ‘relaxed regulation’. Citi points out that Chinese regulators have now proposed new tightened rules for the payment sector, so brace yourself for further innovations in this space. For now, Alipay handles more than three times the volume of transaction that Paypal does, and payment firms have more retail customers than banks have and are now expanding into offline payments.

China also has the largest P2P lending market in the world, four times bigger than that of the US. Citi analysts forecast that P2P loans are going to represent a sizeable 9% of total retail lending in China by 2018.

The driver of this growth is, typically, mostly regulatory constraints on traditional banking that triggered regulatory arbitrage:

P2P lending platforms target segments that are unserved or under-served by existing banking system such as consumer credit and small and micro business lending. Traditional banks are not particularly good at serving this customer segments due to tougher Know Your Client/Anti-Money Laundering (KYC/AML) requirements as well as tightened lending standard post global financial crisis.

And one would add that capital requirements on certain category of customers (such as SMEs) play a large role here too, as I keep pointing out on this blog (see at the end of this post). The same reasons are behind the development of such lending platforms in Europe and the US. And indeed, as Citi writes:

According to China MSME Finance Report 2014 by Mintai Institute of Finance and Banking, almost 80% of SMEs were not served by the banks. The explosive growth in the P2P lending has met the needs of SMEs which cannot get formal financing.

And:

Chinese banks are under tight regulations such as reserve requirement, loan-to-deposit ratios (LDR), KYC, AML, and so on. There was however little regulations for the P2P lending sector. There is also no capital requirement.

Furthermore, Chinese monetary repression is also a driver, as P2P lending allows savers to earn higher returns. Here again, Chinese regulators are looking at ways to scrutinise and more tightly control the sector.

What are the effects of all this? As The Economist points out, China’s shadow banking sector is the largest and possibly the fastest growing in the world:

There is a fundamental difference between the Chinese banking system and the Western one however. Chinese banks, despite being extremely large, have historically had no ability to grow outside of the Communist party’s grip and no ability to adapt to consumer demand as a result. Citi points out that there were only 8.1 bank branches per 100,000 adults in China, vs. around 30 in the Eurozone and the US. With little banking presence, fintech firms have found it easy to rapidly grow.

Yet, developed economies do have a lesson to learn from the Chinese experience. The more regulatory constraints are put in place on banks, the more innovative ways around them will spontaneously emerge and the more complex and opaque (‘Frankenstein-like’) the financial system will become. And sadly, it looks like Europe and the US have decided to follow China’s footsteps.

PS: The following chart is revealing. Most of the financial products that are at most risk of disruption (SME and personal loans, deposits…) are also those that are the most affected by regulatory requirements and low interest rates.

PPS: A very good introduction to the Chinese financial mess is Walter’s and Howie’s Red Capitalism. However the book was ‘only’ updated in 2012, and plenty has happened since then, in particular in the fintech portion of China’s shadow banking sector.

PPPS: Apologies for not posting more regularly at the moment, but I ended up being busier than I thought I would be.

This post was re-published on Alt-M.

Bank regulators are confused by their own mess

Regulators are getting confused by their own reform package. After years of promoting contingent convertible bonds (CoCos) as a good alternative to pure equity capital, and basing a number of their regulatory changes on them, they are now backtracking, as the FT reports (at least in the case of the ECB):

Cocos are a key pillar in the regulatory regime drawn up to strengthen banks’ capital levels and prevent taxpayer bailouts after the financial crisis. But while they are supposed to increase financial stability, concerns about them helped whip up market volatility in February.

Senior executives at several large banks have told officials at the [Single Supervisory Mechanism] that the rules for cocos are too complicated and they could undermine a bank’s financial position rather than strengthen it in a crisis.

CoCos are a form of hybrid debt that converts into equity when a bank’s regulatory capital ratio falls below a certain threshold. They are currently accounted for as ‘Tier 1 capital’. On paper, they sound quite straightforward.

In reality, they are quite opaque. Nobody really knows how to accurately value them. They have both equity and debt-like properties: cash flows are less recurring than debt but more than equity. Nobody really knows how those instruments will fare from a legal point of view when a firm goes into administration. Regulation in some jurisdictions also prevent coupon payments in some unclear cases, even when the bank isn’t about to fall into bankruptcy.

The market has boomed over the past few years as rates on offer looked attractive in a low interest rate environment that pushed many investors to search for yield. CoCos, apparently safer than stocks, seemed to be the easy choice. Some commentators started to worry that interest rates on new issues were way too low for an equity-like instrument (yields fell to about 6% and remained there since 2013, see The Economist chart below, whereas the required return on equity is usually estimated around 11 or 12%). And indeed, CoCos’ valuations suffered during the bank sell-off earlier this year as investors suddenly woke up to the fact that they actually didn’t fully understand those instruments. This CoCo sell-off actually endangered the stability of the banking system, at odds with regulators’ original aim.

Regulators are also backtracking on capital requirements, as they see how damaging they are for smaller banks. Reuters report:

The European Union will propose changing the bloc’s rules on bank capital requirements to ease the burden on smaller lenders in a bid to boost growth, EU financial services chief Jonathan Hill said on Thursday.

In a speech in Amsterdam where EU finance ministers are meeting, Hill said he wants to lighten reporting and disclosure requirements for smaller banks.

“I also want to see whether the intricate calculations banks have to do to comply with prudential rules could be simplified. And whether there is a case for small banks with limited trading activities to be exempt from capital requirements for trading book exposures,” Hill said.

Hill’s speech underscored the willingness of the EU to deviate from globally-agreed capital norms to encourage more banks to lend more.

What the EU is proposing to create is a multi-speed regulatory framework. And we know how damaging multi-speed systems are: firms and individuals engage in regulatory engineering or even stop or reduce their activities in order not to move into the next, more burdensome and constraining, bucket, as this could imply larger additional marginal costs than marginal revenues.

We all know that small banks suffer from those misguided regulatory packages that Basel 3/Dodd-Frank/CRD 4 are, but the best solution is to repeal them for all banks, not create a multi-speed system and introduce further distortions and regime uncertainty that paralyse lending and prevent economic recovery. We’ve had enough of this mess.

PS: Bloomberg reports that Credit Suisse is looking to issue a new type of fixed income instrument that would cover potential operational losses due to rogue trading, fraud or cybercrime, in cooperation with the Zurich Insurance group. As Bloomberg says:

Regulators require banks to hold funds as a safeguard against various kinds of vulnerability, leaving them with less money to build the business.

Here again this potentially difficult to value instrument emerges from the willingness to offset the often unnecessary costs of capital regulation. But it doesn’t take a genius to figure out that those ‘solutions’ create problems of their own.

Update: Regulators are also about to introduce a new capital requirement for interest rate risk, which is likely to seriously weigh on banks’ profitability. It is funny that central bankers, who ow also often are regulators, decide to boost the economy by pushing rates down as much as possible, but then penalise banks for the same reason. Such incoherence is not going to help lending volumes, I’m telling you.

Academics’ unhealthy obsession with bank opacity

I just read a January 2015 paper (not very recent, I know, but my reading list is huge) that was not only curious, but also plain wrong. The paper, titled Understanding the role of debt in the financial system and written by Bengt Holmstrom, illustrates a curious belief among a number of academic economists: that banking, in order to be stable, should be opaque.

The abstract sets the tone:

Money markets are fundamentally different from stock markets. Stock markets are about price discovery for the purpose of allocating risk efficiently. Money markets are about obviating the need for price discovery using over-collateralised debt to reduce the cost of lending.

Later, he adds that

Without the need for price discovery the need for public transparency is much less. Opacity is a natural feature of money markets and can in some instances enhance liquidity

His views about the stock market/money market differences are summarised in the following table:

Now let me say that there is virtually nothing in his arguments that is grounded in reality. This theory is completely disconnected from the day-to-day routine of finance workers.

Let’s start with Holmstrom’s definition of ‘money markets’. Following his paper, money markets only involve repurchase agreements. This cannot be further from the truth. Money markets (which we can also call interbank markets) not only involve repos, but also uncommitted and unsecured interbank placements (which include Fed funds). In fact, for many banks, those placements represent the bulk of their money market exposures. For instance, according to the financial database Bankscope, JPMorgan’s assets comprised $213Bn of reverse repos and $340Bn of interbank placements. Citigroup: $120Bn and $112Bn. Deutsche Bank: EUR107Bn and EUR13Bn. HSBC: $147Bn and $96Bn*. Small banks, that have very limited trading activities, have almost no reverse repo transactions outstanding.

So the unsecured, relatively longer-term, interbank market is at the least a sizeable portion of money markets. And it is completely ignored by Holmstrom’s generalisation. Given that his arguments rest on the ability of the lender to over-collateralise his exposure, they suddenly weaken considerably.

More fundamentally, Holmstrom really misunderstands the differences between stock and money markets. In reality, both markets are very information sensitive and require transparency. Both markets rely on fundamental financial analysis to assess the riskiness of any investment. Equity markets are more liquid because they involve only a single instrument by issuing firm; instrument whose value is highly sensitive to the profitability of the firm because its yield depends on it.

Credit markets are much, much, larger and involve a multitude of instruments by issuing firm, covering a broad spectrum of hybrids from pure credit to almost equity-like debt. Those debt instruments are ranked differently in the hierarchy of creditors. Senior creditors, including unsecured money market placements, have the first claim on a bankrupt firm’s assets. Does this mean they are information insensitive? Certainly not. But the market value of a firm’s assets fluctuates less than the same firm’s profits/cash flows. Price discovery is continuous; either at issuance (the higher the risk, the higher the interest rate), or on the ‘secondary’ market: given that interest rates on issues are usually fixed, a decline or improvement in the risk profile of the issuer triggers a change in the market price of related issues. Therefore information, and indeed transparency, is crucial in this continuous risk assessment process.

So Holmstrom’s generalised arguments about ‘money markets’ are simply wrong. But are secured credit markets, including reverse repos, devoid of the above rules? Does collateral-posting allow the lender to avoid assessing the inherent riskiness of his counterparty?

While it is true that collateral mitigates risk, no serious lender would ever blindly lend merely on the basis of collateral availability. There are a number of reasons for that. First, collateral is also subject to credit risk, and needs separate assessment. Second, collateral is subject to market risk (i.e. market price fluctuations), requiring the application of a haircut. Despite the haircut, when a crisis strikes and markets all fall simultaneously, the value of your collateral can potentially collapse as fast, if not faster, than the amount you lent. Third, legal risk means that there can be a delay between the insolvency event and the moment you can legally take possession of the collateral (depending on the original contract). And fourth, the news that you had exposure to a collapsing firm, even if you were secured, can easily raise risk-aversion towards you and trigger financial difficulties.

In the end, even in the case of secured lending, fundamental analysis, which relies on transparent information, is necessary. Opacity, unlike what our economists believe, is usually ‘credit negative’ and accentuates the compensation and/or the collateralisation that the lender requires. Moreover, how can the collateralisation level of a transaction be determined without some sort of initial price discovery? Holmstrom does not answer this question.

Unfortunately, Holmstrom’s piece is full of facts that are grounded in an imaginary world. For instance, see his claim that

When new bonds are issued, the issue is typically sold in a day or less. Little information is given to the buyers. It is very far from the costly and time-consuming road shows and book-building that new stock issues require in order to convey sufficient information.

Please, I beg you never to say that sort of things at a financial conference if you don’t want to get laughed at. The truth is that specific roadshows targeting fixed income investors are regularly organised by companies. Fixed income managers also employ buy-side analysts who spend their day analysing those firms, as well as reading pieces of financial research published by sell-side analysts. According to Holmstrom, those people do not seem to exist.

He also claims that bond ratings are ‘coarse’, and that this is “another example of what appears to be purposeful opacity.” I find this amazing, given that rating agencies have about 22 different base rating notches, to which a multitude of extra ratings are added in order to provide the information Holmstrom believes is opaque. Now compare this with the usual three-notch stock rating system of Buy/Hold/Sell and you might conclude he got seriously mixed up here.

This tendency to believe that opacity ‘helps’ markets seems to be spreading. In 2014, Gorton et al (which included, unsurprisingly, Holmstrom) published a very weird paper titled Banks as Secret Keepers, which argues precisely that:

Banks are optimally opaque institutions. They produce debt for use as a transaction medium (bank money), which requires that information about the backing assets – loans – not be revealed, so that bank money does not fluctuate in value, reducing the efficiency of trade. This need for opacity conflicts with the production of information about investment projects, needed for allocative efficiency. Intermediaries exist to hide such information, so banks select portfolios of information-insensitive assets. For the economy as a whole, firms endogenously separate into bank finance and capital market/stock market finance depending on the cost of producing information about their projects.

The paper is based on a mathematical model that seems unable to describe what happens in real financial and deposit markets. And indeed they don’t bother providing much empirical evidence of their claims (as I am writing this post, Kadhim Shubber of FT Alphaville quotes the exact same paper rather uncritically).

At the end of the day, Holmstrom’s and Gorton’s theories seem to justify government intervention in deposit and money markets. But as Kevin Dowd just brilliantly reminded us, those ‘opacity’, ‘information asymmetry’ and ‘market failures’ in no way justify banking regulation, unless you disregard all empirical and historical evidences. And, of course, unless you don’t believe in government failure. Sadly, it seems that imagination wins over reality nowadays in academia.

*Moreover, some of the ‘reverse repo’ figures might include collateral posted against other sort of trades, as well as transactions with non-financial counterparties, implying that the ‘pure’ money market reverse repo portion mentioned here is likely smaller.

This post was re-published on Alt-M.

Even central banks suffer from negative rates

The FT reports today that central banks also suffer from negative interest rates. It couldn’t be more ironic.

Investors ranging from small German savers to global life insurers have long complained about central banks’ use of negative interest rates.

Now, however, another group is feeling the pain from negative rates — central banks themselves.

European and Japanese rate cuts are putting pressure on many central banks’ returns — a source of income used to cover running costs and to provide finance ministries with profits on which they have come to rely.

A poll of reserve managers from 77 central banks, entrusted with reserves worth $6tn last August, found a clear majority were changing their portfolio management strategy as a result — including taking steps such as buying riskier assets.

Central banks are indeed big players on the market due to their OMO and related policies that involve purchasing and selling billions of assets in order to influence market prices, aggregate amount of high-powered money and interest rates. They also invest in other currencies and commodities and place cash with other central banks.

Unfortunately, a number of their placements are now generating negative returns and yields on their fixed income investments (often government bonds) are now very low, if not negative.

The irony of the whole situation is that central banks initiated their conventional and unconventional policies partly in order to help (i.e. force) the private sector to take more risks (‘search for yield’). What goes around comes around, and it is now central banks’ turn to follow the same route. In short, they are now turning into vulgar commercial banks that attempt to please their shareholders (i.e. budget-constrained governments who need this cash).

But in doing so, they also potentially endanger their capital base. While it isn’t clear whether or not central banks can fall into bankruptcy and what happens afterwards, I guess we’d all be better off not to reach a point from which we start asking this question.

PS: A French newspaper highlights the very close links between the French government and its domestic financial sector. Many government appointees were formerly financial executives, and many current executives used to work in government. This reminds me of this.

PPS: A few weeks ago, Huw van Steenis, bank analyst at Morgan Stanley, published a good article in the FT about the effects of negative rates on banks. His views are very similar to mine.

April fools and risk-weights

The Basel regulatory framework might look like a bad April fool. On the 1st of April (you couldn’t make that up) the BIS published a document reviewing the practices and average risk-weights applied to various types of assets by large banks. Since the introduction of Basel 2, large banks usually utilise the IRB framework, or ‘Internal-rating based’, which allows them to calculate their own risk-weight, which are then used to compute their regulatory capital ratio. Other banks use risk-weights directly provided by Basel (under Basel 1, all banks used fixed risk-weights).

One could believe that giving banks the ability to define their own risk-weight is a good thing, as it mimics a free market setting (i.e. banks rather than regulatory directives deciding how much capital they need to keep aside). Unfortunately it isn’t. Regulators verify banks’ models and validate them. The consequence of this is that banks attempt to benefit from this by amplifying the differential between what regulators usually view as risky and safe assets.

This is where the BIS paper comes in. It demonstrates the extent of risk-weight gaming among large international banks. The table below shows that median risk-weight on mortgage lending is 17%, whereas median SME corporate lending is 60% and large corporate lending 47%. Given that interest rates on corporate lending is usually not much higher (and sometimes lower, see this earlier analysis on the ECB’s TLTRO) than interest rates charged on mortgage lending, it is not surprising to see banks’ favouring real estate lending: it is much more efficient per unit of capital. Call this capital, or RoE, optimisation.

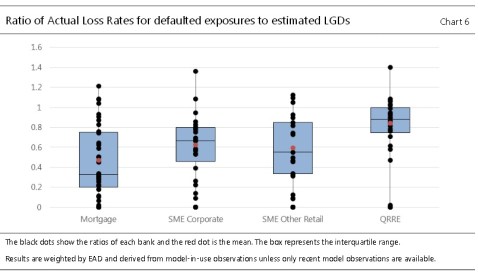

There are quite a few other interesting charts in this publication, see the following one:

This chart shows that actual loss rates on defaulted exposures aren’t much higher for small corporate lending than for mortgage lending. This adds to the increasing amount of evidence that nothing justifies Basel’s and regulators’ much higher capital requirements for corporate exposures. Other charts the paper provides seem to confirm this view.

Finally, the paper also looks at the new Basel 3 leverage ratio, which was supposed to avoid capital gaming by getting rid of risk-weights altogether, hence becoming a ‘backstop’ ratio. Ironically, Basel geniuses reintroduced risk-weights into the leverage ratio, but under another form: credit conversion factors (CCF). CCF essentially provide various risk-weights for various types of off-balance sheet products and commitments (see pages 18 and 19 of this document). Consequently, banks’ lending decisions also become affected by CCF… Here again you couldn’t make it up. The paper provides various implied CCF used by large banks, although by asset class rather than by product type.

PS: I wrote another post on the topic of risk-weight gaming about a year ago here.

PPS: There was a good article on shareholder value in The Economist, reminiscent of some of my own arguments.

Update: SNL reports that the BIS is thinking of preventing large banks to use their own IRB models to calculate risk-weights on loans to other loans and larger corporations. It’s not going to solve anything.

Understanding banking mechanics isn’t sexy; but it is essential

Banking and finance blogging seems to attract a lot fewer readers than economics blogging. This is unfortunate.

It sounds boring and too technical. The terms used to describe banks’ characteristics are mostly ignored by the wider public, and even by many more informed people and economists. Ask the layman what a leverage ratio, a Tier 1 ratio or NPLs are, and you will be met with raised eyebrows. In contrast, GDP, NGDP/aggregate demand, opportunity cost, inflation/CPI, money supply and so forth, are much more wildly known (not enough many would argue, and I’d agree).

Some would reply that economic terms are more ‘important’ in order to understand how the world works. Fair enough. Still, jargons in other industries are also relatively broadly known: horsepower, torque, medical terms, megabyte, dB, resolution, kWh…

Banking seems to be one of the few exceptions. Here again, some would reply that this is not such an issue, as banking is regulated, and supervisors that are more knowledgeable are in charge of monitoring banks. And I would have to strongly disagree.

It is crucial that the public understands at least some basic banking mechanics. Not doing so creates a number of issues. First, moral hazard: it is well-researched that deposit insurance led to banks free riding on depositors’ blind belief that their money was in safe hands. The same reasoning applies to leaving regulators in charge of the monitoring of the financial system. Second, it leaves an open door to politicians and regulators to manipulate the industry through various legislative acts.

And don’t tell me that understanding a leverage ratio or a loan loss coverage ratio is a lot more difficult than understanding broadband speed, computer memory, or fixing a car engine. Moreover, the public can nowadays rely on specialised magazines and websites to test and give awards to the best consumer products. Banks could be reviewed in a similar way and rating agency reports be made much more widely available. Banks could start advertising their strong capital ratios rather than merely their ability to allow you to make cheap payments while travelling abroad.

So banking is viewed as boring. Unsexy. And regulations introduced decade after decade are partly to blame for that as they have shielded the broader public from the need to understand the institutions with which they placed their money.

But understanding banking mechanics and regulation is also crucial. It is crucial because the financial system is the heart of the economic system: it allocates loanable funds to sectors and customers that are likely to generate the most economically efficient outcomes. As such, it is intimately linked to the economic subject as a whole, despite some economists begging us to stop talking about banking. When this mechanic is disrupted by new frameworks of rules, the whole economy is affected and either doesn’t produce optimally, or worse, generate malinvestments by not producing the goods that the public want in the long run. And crises ensue.

Free Banking scholars have demonstrated that many of the 18th and 19th century crises had roots in misguided banking rules. The same applies today. One cannot understand our most recent crisis, and possibly our future crises, without knowledge of the small and dull bits that currently dictate, or at least strongly influence, capital flows. As much as ‘macro’ is sexy, the devil is in the details.

I know my work will remain ‘niche’. It is clear that my most successful blog posts have so far treated relatively non-technical topics or banking framed within a more general economic view. But I’ll keep producing ‘niche’ posts nevertheless; because it is necessary. I’ll keep pushing to make readers understand how much they’ve been scr**d by what seems, at first glance, boring details of financial regulation.

Sadly, those boring details may well trigger the next crisis, and make us lose our job.

Regulatory study says regulators were right

Some regulators seem to be ready to publish the most idiotic arguments to justify their earlier work. A new flawed study about an ill-conceived measure for small firms lending (SME) by the European Banking Authority did just that.

Despite continuously denying that capital requirements have anything to do with SME and other corporate lending, authorities have decided to experiment in 2014 by allowing banks to hold less capital against such lending (a measure called ‘SME Supporting Factor’). In order to find out whether or not this measure had any effect on SME lending, the EBA launched a study that concluded that there was (in the words of Reuters):

“no sufficient evidence” that lower capital charges provided additional stimulus for lending to SMEs compared to large corporates

First, let’s notice the very small timeframe of the study: less than 18 months. Banks are unlikely to be able to grow their loan book by much in a safe fashion in such short timeframe. Second, the demand side seems not to be factored in (but I believe it to be a minor point). Third, SME SF only applied to tiny loans (not more than EUR1.5m, which is too small for medium sized firms). And indeed, the EBA report highlights that “SMEs subject to SF represent 4% of the aggregate corporate portfolios, 11% of the aggregate retail portfolios, and, in case of SA banks only, 6% of the aggregate exposures secured by immovable property.” In other word, they represent a very small share of banks’ loan books.

But the main issue with this measure, and indeed with this study, is that this SME SF has barely tightened the differential between risk-weights applied to SME/corporate exposures and risk-weights applied to real estate/sovereign exposures. SME SF only introduces a 24% capital discount to that form of lending (see table below for Basel’s ‘Standardised Approach’ for SME lending). The result, as the EBA shows, is that total risk-weighted assets (RWA, the denominator used to calculate regulatory capital ratios) only declined by…1.2%. This has effectively zero impact on banks’ RoEs.

Let’s make a quick calculation. A bank has total assets of $2,500 to which an average of risk-weight of 40% is applied, giving $1,000 RWAs. The bank also has $100 in regulatory capital (in order to simplify, let’s assume it only consists of plain vanilla shareholder equity), leading to a 10% regulatory capital ratio. The bank also makes $10 net profit, implying a 10% RoE.

A 1.2% decline in RWAs would lead to RWAs falling by a mere $12, making the capital ratio 10.1%*. Assuming the bank decides to maintain a 10% ratio, the newly-freed capital would allow RoE to improve by…0.1 percentage point. Impressive effect, to say the least.

Irony aside, SME SF was a very ill-conceived measure: its scope was too narrow (targeting firms that are too small), and the incentives it gave banks were very superficial given the remaining differential between the risk-weights applied to SME and other types of exposures (Standardised Approach risk-weight on mortgages remain way below at 35% – and median risk-weight is 17% on an IRB basis** – see upcoming post – UPDATE: here). The mini-gains that banks’ could have expected would have possibly been more than offset by the risk of rapidly growing an SME loan book in an uncertain economic environment.

The study also found that current capital requirements for small and large corporates were adequate, and that applying SME SF would lead to those exposures being undercapitalised. This is in complete opposition with the (mostly independent, that is, not published by EU regulators) papers I reported on a few weeks ago.

In the end, this research undertook by a regulatory body succeeded to prove what it wanted to prove: regulatory measures were right from the start. If only it were not completely wrong.

*This is in line with the EBA’s findings:

**Standardised method refers to a RWA calculation method that applies to relatively small banks, which use fixed risk-weights provided by Basel rules. IRB (Internal Rating Based) refers to more flexible (but validated by regulators) risk-weights calculated internally by large banks using complex models.

My contribution to the Cato Institute/Alt-M

A few weeks ago, George Selgin, director of the Center for Monetary and Financial Alternatives at the Cato Institute, contacted me and kindly suggested that some of my Spontaneous Finance posts be cross-posted on the Cato’s specialised monetary and financial blog, Alt-M. Given that I have a very high estimate of Alt-M’s (as well as its predecessor ‘Free Banking’) and George’s work, I happily accepted to contribute.

An introductory post co-written by George and me was published today on the Alt-M blog. It briefly sums up a number of the ideas I developed on Spontaneous Finance. From now on, I may cross-post on both this blog and Alt-M from time to time.

Recent Comments