More on the natural rate of interest

Since my recent post on Wicksell, a number of famous economists have also blogged on the Wicksellian ‘natural’ rate of interest.

Tyler Cowen asked ‘what’s the natural rate of interest?’ and has a few interesting points. Paul Krugman responds to Cowen by making the usual mistake (albeit shared by most mainstream academics) of defining the natural Wicksellian rate as the “the rate of interest at which the economy would be more or less at full employment, which in turn implies that inflation will be more or less stable.” He adds that there is no reasonable case that interest rates are kept artificially low. Meanwhile, on Econlog, Scott Sumner added that there was “nothing natural about the natural rate of interest” and added some comments and charts on his own blog, declaring that the natural rate is surely negative.

Cowen in turn responded to Krugman, highlighting that risk was not a good reason to justify low risk-free natural rates. He elaborates on a few points, but one in particular was, I believe, spot on: what he calls “growing legal and institutional requirements for T-Bills as collateral”. While he believes that this hypothesis still has to be demonstrated empirically, he linked to a 2-year old post of his I had missed in which he discusses this theory in more detail.

Here are his first few points:

1. Imagine that financial institutions and traders have to hold large quantities of T-Bills (and similar assets) to participate in financial markets. That may be to satisfy collateral requirements, to meet government regulations, to be credible in private market transactions, and so on.

2. The demand for these assets is now so high and so persistent that the assets have persistently low nominal returns and often negative real returns.

3. The holders of these assets do not however receive negative returns on their portfolio as a whole, when deciding to hold these T-Bills. Holding the T-Bills is like paying an entry fee into financial markets. And once they are in financial markets of the right kind, these market players can earn high returns by possessing special trading technologies (the technology may vary across market participants, but think HFT, hedge funds, prop trading, employing quants, and so on).

4. Let’s say you are not a major financial institution. Then you really will earn negative returns on your safe saving. You might try holding equities, but a) you are not wealthy and thus you are fairly risk averse, and b) as a small player you do not have access to these special trading technologies and indeed you must trade against those who do. You thus will often earn negative or low returns on your portfolio no matter what.

5. The implied prediction is that differential rates of wealth accumulation will be a driver of inequality over time. This seems to be the case.

It is sad that Cowen is not an expert in banking and financial regulation, because he had a remarkable insight there.

US Treasury yields (as well as most government-issued securities and a number of highly-rated corporate ones) do not reflect the ‘natural’ supply and demand of the market. Instead, demand is artificially raised by financial regulation, as I have explained in a number of posts (see this previous blog post on the BIS, which explained how its recent financial reforms will impact a number of reference rates, and also this post for instance). This is where Krugman is wrong when he says that interest rates are not kept artificially low. While we can argue whether or not the Fed and other central banks manipulate rates downward, there is no argument here: regulation does push a number of reference interest rates down.

This was also the case (to a lesser extent) in the post-war era, making Scott Sumner’s reasoning inaccurate, as pointed out by one his commenters. Remarkably, Scott seemed to agree that this might indeed be a good point. Over the past three decades, regulation has fundamentally influenced the demand for a number of assets, modifying their market prices/yields in the process. Any comprehensive analysis, from the causes of the crisis to secular stagnation, should take those microeconomic changes into account. I have read countless academic papers over the past few years, and almost none did. They seemed to consider that banking behaviour and incentives were (mostly) constant over time. They weren’t.

So a number of economists might be slowly waking up to the fact that financial market prices are not freely determined, which seriously constrains our ability to reach conclusions based on market trends. There are many other underlying drivers (the ‘microeconomics of banking’ that I keep mentioning) that are at play.

PS: Marcus Nunes has an interesting post on determining (or not) the natural rate of interest. I agree that there is no point trying to determine the rate to target it.

Wicksell is hiding; the real estate boom isn’t

The Wicksellian natural rate of interest remains an economic mystery. No one knows what its level is. That wouldn’t be a problem if no one tried to emulate (or voluntarily tried to manipulate it downward or upward), that is, if we had a free market for money. But we don’t and a number of central banks attempt to estimate what this interest rate is so they can play with their own monetary policy tools.

Problem is, no one has a proper definition, and we often hear about a ‘neutral’ rate of interest, or a ‘natural’ rate that would maintain CPI stable or on a stable growth trend, and/or a rate that would be consistent with ‘full employment’ or that would allow GDP growth in line with an often ill-defined ‘potential output’. This is all very confusing, and doesn’t seem to accurately represent what Wicksell originally called the ‘natural rate of interest’, that is, the rate whose level would not affect ‘commodity prices’ and is similar to the rate of interest of a money free world (see Interest and Prices). Some believe the natural rate to be relatively stable; others believe it to fluctuate in line with business cycles. This Bruegel post sums up quite well the differing views that a number of current economists hold.

A common view today is that the natural rate has turned negative in most of the Western world since the financial crisis. It’s a view held by a wide range of economists, from Keynesians to Market Monetarists. Scott Sumner believes that the rate is firmly negative (David Beckworth too, and he denies that central banks affect interest rates – see also my response to Ben Southwood on the same topic) because

Since 2008, the inflation rate has usually been below the Fed’s 2% target, and if you add in employment (part of their dual mandate) they’ve consistently fallen short. This means that money has been too tight, i.e. the actual interest rate has clearly been above the Wicksellian equilibrium rate.

He is therefore surprised by a new piece of research by two Richmond Fed economists, who came up with very different conclusions.

First, they remind us of an estimate of the natural rate made by Laubach and Williams, which shows the nominal rate to have fallen into negative territory since the crisis, but also that the real rate is too loose:

Using a different methodology, which they believe more accurately reflects Wicksell’s original vision, the authors estimate the natural rate of interest to be higher than that estimated by LW. They also point out that it never turns negative.

This demonstrates how tricky it can be to estimate this rate (see their lower/upper bound estimates…), and how easily central bankers could make policy mistakes as a result. (See also estimates from Thomas Aubrey’s methodology, i.e. ‘Wicksellian differential’)

Interestingly, all Fed economists above estimate the natural rate to be below the real money rate of interest from around 1994 to 2002, that is, money was too tight during the period. Thomas Aubrey, by contrast, finds the opposite result, with a positive Wicksellian differential over the period, meaning that money was too loose. Similarly, Anthony Evans writes on Kaleidic Economics that his own estimate of the UK natural rate is 2.3%; much higher than the current BoE rate.

If the Fed economists are right, it means that the classic Austrian Business Cycle theory (i.e. malinvestments originating in economic discoordination due to money rate of interest below the natural rate) cannot apply to most of the two decades preceding the crisis (it can in the case of Aubrey’s theory however).

As some readers already know, malinvestments and economic discoordination can still happen independently of the level of the risk-free natural rate of interest. This is what I theorised in my RWA-based ABCT: Basel banking regulations add another layer of distortion to the credit allocation process.

Where it gets scary is that, according to the same Fed economists, the current monetary policy stance is too loose. I find it hard to understand the outright dismissal of those estimates by a number of economic commentators and professors. Some commenters on Sumner’s post don’t even try to discuss the theoretical basis of this Richmond Fed paper. They see some sort of conspiracy or whatever. Not really the highest sort of intellectual debate to say the least. When some ‘evidence’ seems to challenge your theoretical framework, don’t dismiss it outright. Address it.

Personally, I have repeated a number of times that I find it hard to believe that our recent economic woes were so severe that they led to a market clearing, natural, Wicksellian rate below zero for the first time in the history of mankind. I have also tried to show elsewhere that a free banking system would be highly unlikely to drop rates below the zero-lower bound.

Now, if the estimates highlighted above are right, I fear possibly huge distortions in the real estate market. Let’s define a simplified free-market mortgage interest rate as

MR = RFR + IP + CRP – C,

where MR is the mortgage rate, RFR is the applicable, same maturity, risk-free rate, IP the expected inflation premium, CRP the credit risk premium that applies to that particular customer and C the protection provided by the collateral (that is, house value, with lower LTV loans leading to higher C).

Ceteris paribus, if the RFR is pushed downward, MR goes down, likely stimulating the demand for real estate credit. But this can also apply to all sort of lending. Enter Basel.

In a Basel world, the favourable capital treatment of such loans increases the supply of loanable funds towards the real estate sector. MR is pushed down even further, leading to an increase in demand for mortgages, in turn pushing house prices up, which raises the value of collateral C, which lowers MR further. It’s a virtuous (or rather vicious) circle. On the other hand, the stimulating effect of the lower RFR applied to SME lending gets ‘suppressed’ by the reduced supply of loanable funds for that type of credit. (and there are many other impacts on the RFR emanating from Basel)

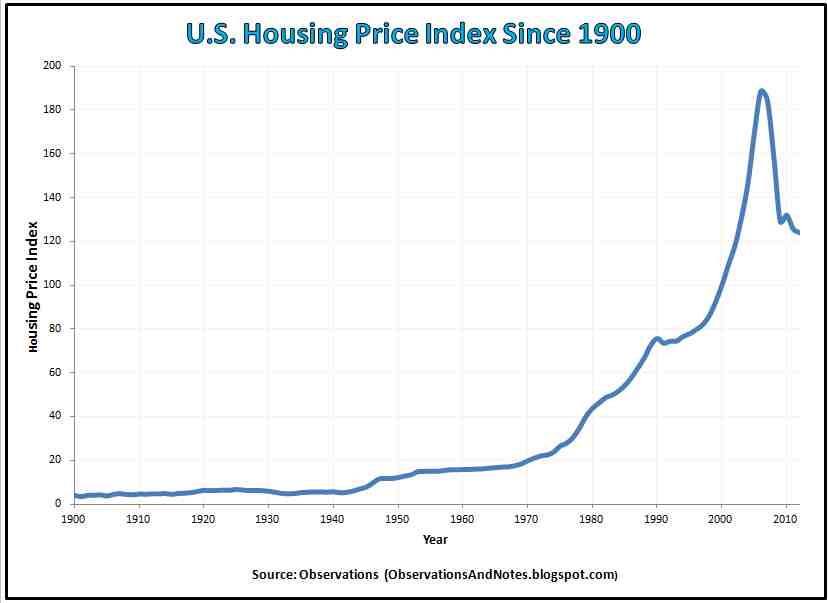

I warned more than two years ago that this situation would continue. And this is precisely what has been happening. While the media complain on a weekly basis that SMEs are starved of bank credit and turn to alternative lenders (while regulators attempt to revive the market for securitised corporate loans), the Economist reports that housing markets are either strongly recovering or even way overvalued in most advanced economies. This sort of continuous and rapid house prices booms and busts was unknown in history before the 80s/90s (see also here).

It is unclear what the exact contribution of low risk-free rates is, relative to Basel’s. What is certain is that, if Richmond Fed economists are right, we’re in for another housing disaster as Basel’s effects get amplified by monetary policy (which doesn’t necessarily imply that the effects would be similar to those of the 2008/9 crisis, although historical evidence shows that housing bubble are the most damaging types of ‘bubbles’).

Natural interest rates are dead, the BIS (indirectly) says

In May (I only found out a couple of weeks ago), the BIS released a big report titled Regulatory change and monetary policy, in which it investigates the effects of the new banking regulatory framework on market interest rates and the implied consequences for the conduct of monetary policy. By the BIS’ own admission, the whole yield curve has nothing ‘natural’ left.

The report is an interesting, though pretty technical read. It is also scary. Scary to see how much banking regulation is affecting interest rates all along the yield curve across most banking products. Scary to see that the suggested remediation by the BIS is more central bank involvement to counteract the effects of those regulations.

Of course, the Basel framework originates from… Basel in Switzerland, where the BIS is located, and where BIS experts have spent years drafting apparently clever rules to make our banking system apparently safer, in spite of all historical evidences and what we’ve learned about the spontaneous order of free markets (remember: “banking is different” they say). So I wasn’t expecting this BIS report to declare that the very rules it put in place was endangering the economy. And indeed it doesn’t. But it does admit that there will be ‘impacts’, which of course will be ‘limited’ and ‘manageable’. They always are.

I won’t replicate here everything that’s in that report. It’s way too long and I’ll let you take a look at it if you’re interested. There is a quite detailed description of the potential effects of the Liquidity Coverage Ratio, the Net Stable Funding Ratio, the Leverage Ratio and the Large Exposure Limits on banks’ product pricing and volume and the impact on central bank’s monetary policy operations. And despite its 30+ pages, the report isn’t even comprehensive. It forgets to look at the large distortive effects of risk-weighted assets and credit conversation factors.

What I’m going to show you below is merely the BIS researchers’ own conclusions, which they neatly summarised in handy tables. This is what they view as the potential changes in money market interest rates:

By their own admission, the cumulative effect of those new rules is unclear. And even when they believe they know which way the interest rate will move, it remains a best guess. To this table you can add the hugely distortive effects of RWAs and CCFs, which I have described on this blog a number of times.

The only conclusion is that there is no free market-defined Wicksellian ‘natural’ interest rate anymore in the marketplace. As interest rates are manipulated by regulatory measures in myriads of ways, entire yield curves across the whole spectrum of banking products and asset classes stop reflecting the pricings that market actors would normally agree on in an unhampered market. The result is a large shift in the structure of relative prices in the economy.

The economic consequences are likely to be damaging (and it is clear, at least to me, that RWAs have already done a lot of damages, i.e. the financial crisis), even though the BIS reckons that central banks could potentially offset some of those interest rates movements:

More central bank intermediation: Many of the new regulations will increase the tendency of banks to take recourse to the central bank as an intermediary in financial markets – a trend that the central bank can either accommodate or resist. Weakened incentives for arbitrage and greater difficulty of forecasting the level of reserve balances, for example, may lead central banks to decide to interact with a wider set of counterparties or in a wider set of markets.

In addition, in a number of instances, the regulations treat transactions with the central bank more favourably than those with private counterparties. For example, Liquidity Coverage Ratio rollover rates on a maturing loan from a central bank, depending on the collateral provided, can be much higher than those for loans from private counterparties.

Problem is (and the BIS also admits it): there is no way non-omniscient central bankers know by how much and in what direction rates should be offset. We here get back again to the knowledge problem. There is no way the central bank can act in a timely manner. It is also unlikely that central bankers could act free from any political interference. Finally, even if central banks managed to figure out what the ‘natural’ rate is for a given asset at a given maturity, central banks’ policies are likely to have unintended consequences by altering the rates of other products and maturities.

The effectiveness of the transmission mechanism (banking channel) of monetary policy is more than ever questioned. Rates will move in unexpected ways. And, as the BIS describes, banks could simply opt out of monetary programmes altogether:

The question is whether there are exceptional situations in which banks would refrain from subscribing to fund-supplying operations because concerns over the LR impact of the reserves that would be added to the banking system in aggregate outweigh the financial benefits accrued by participating in the operations. If so, this lack of participation could prevent a central bank whose operating framework entailed increasing the quantity of reserves from meeting its operating target.

The BIS believes that “the changing regulatory environment will, by design, affect banks’ relative demand across various types of assets and liabilities”. It summarises the potential changes in the demand for central bank tools below:

Here again, a lot of uncertainties remain.

Something looks certain however. The involvement of central banks in the financial and economic system is likely to become more intense. As regulations bound banks’ behaviour and prevent an effective allocation of capital, central banks are increasingly going to step in to boost or restrict the supply of credit to certain market actors and asset classes. See what happened with SMEs, starved of credit as Basel makes it too expensive to extend credit to such customers, while central banks attempted to offset this effect by starting specific lending programmes (such as the Funding for Lending scheme in the UK). We are here again back to Jeff Hummel’s arguments of the central bank as central planner.

Nonetheless, I am certain that capitalism and free markets will get blamed for the next round of crisis. It is becoming urgent that we replicate the achievement of academics such as Friedman and Hayek, who managed to overturn the nonsense post-War Keynesian consensus. Sadly, free markets academics seem to have virtually disappeared nowadays or at least cut off from most policymaking positions and public debate.

Modeling a Free Banking economy and NGDP: a Wicksellian portfolio approach (guest post by Justin Merrill)

My friend Alex Salter and his coauthor, Andrew Young, have an interesting new paper called “Would a Free Banking System Target NGDP Growth?” that I believe was presented at a symposium on monetary policy and NGDP targeting.

I too have wondered the same question. I believe there are real reasons why a dynamic economy might not have stable NGDP. One reason is demographic changes (maybe target NGDP per capita?). Another reason is problems with GDP accounting in general such as the underground economy, changes in workforce participation of women and the vertical integration of firms. Another micro-founded effect might be the income elasticity of demand and substitution effects. But even abstracting from these problems, it is still a worthy question to ask if monetary equilibrium is synonymous with stable NGDP and its relationship to free banking. If they are synonymous, we might expect stable NGDP from free banking. In my paper on a theoretical digital currency called “Wixle” I outline a currency that automatically adjusts its supply to respond to demand by arbitraging away the liquidity premium over a specified set of securities. This is a way to ensure monetary equilibrium without regard for aggregate spending, which is particularly useful if the currency is internationally used.

A small criticism I have of my free banking and Market Monetarist friends is that they often assert that monetary equilibrium and stable NGDP are the same thing, usually by applying the equation of exchange. As useful as the equation of exchange is, it is tautologically true as an accounting identity. But just as we know from C+I+G=Y, accounting identities’ predictive powers are limited when thinking about component variables. I have argued for the conceptual disaggregation of the money supply and money demand, because the motives for holding currency and deposits are different and the classification of money is more of a spectrum. So I was pleased to see that Salter and Young did this in their paper and added the transaction demand for money into their model. This leads them to conclude that a free banking system will respond to a positive supply shock, which results in an increased transaction demand for money, by stabilizing the price level rather than NGDP. This might be true, and whether this is good or bad is another question. Would this increase in currency lead to a credit fueled boom, or is this a feature and not a bug?

I have long been upset with the way that economists overly focus on reserve ratios and net clearings from a quantity perspective. This abstracts away from the micro-foundations of the banking system and ignores the mechanics of banking. This is the point I made at the Mises Institute when I rebutted Bagus and Howden. My moment of clarity for the theory of free banking actually came from reading the works of James Tobin and Gurley & Shaw, as well as Knut Wicksell. The determination of the money supply is the public’s willingness to hold inside money, and this willingness creates the profit opportunity for the financial sector to intermediate by borrowing short and lending long. I believe the case for free banking can be made more robust by adding the portfolio approach, as well as the transactions approach. I will outline here what that would look like without sketching a formal model.

The Model is a three sector economy: households, corporations and banks. Households hold savings in the form of corporate and bank liabilities and have bank loans as liabilities. Corporations hold real capital, bank notes and deposits as assets and bank loans, stocks and bonds as liabilities. Banks hold reserves, securities and loans as assets and net borrowed reserves, notes, deposits and equity as liabilities.

Households can hold their wealth in risky securities or safe, but lower yielding interest paying deposits that pay the risk-free rate in the economy or non-interest paying notes used for transactions. The model could include interest-free checking accounts, but these are economically the same as notes in my model.

Banks can then choose to invest in loans, securities or lending reserves. They fund investments largely by borrowing at the risk-free rate and borrowing reserves at the margin. Logically then, the cost of borrowed reserves will be higher than deposits but lower than that of loans and securities and arbitraging ensures this. If the cost of reserves goes above the return on securities, banks will sell bonds to households and lend reserves to each other. If the cost of reserves goes below the rate on deposits, banks will borrow reserves and deposit with each other. The return on loans and securities (adjusted for risk) will tend towards uniformity because they are close substitutes. Also, as Wicksell pointed out, if loan rates are below the return on securities or the return on real capital, households and firms would borrow from banks and invest.

Empirical evidence for the interest rate channels is provided here. Interestingly, the rules set out above were only violated in times of monetary disequilibrium, such as the Volcker contraction:

http://research.stlouisfed.org/fred2/graph/?g=1aRY

The natural rate of interest is equal to the return on assets for corporations. Most economists that try to model the natural rate mistakenly do it as the risk free rate or the policy rate. This is a misreading of Wicksell since he identified the “market rate” as the rate which banks charge for loans, and the important thing was the difference between the market rate and the natural rate. If the market rate is too low, people will borrow from banks and invest, increasing the money supply.

We can now apply the framework to the CAPM model and conceptualize the returns on various assets:

The slope of the securities market line (SML) is determined by the risk aversion/liquidity preference of the public. Should the public become more risk averse and demand a larger share of their wealth be in the form of money, they will sell securities in favor of deposits. If in aggregate, the household sector is a net seller, the only buyers are banks (ignoring corporate buybacks since this doesn’t change the results since corporations would end up needing to finance the repurchases with bank loans). So the banking sector would purchase the securities (at a bargain price) from households, crediting their accounts and simultaneously increasing the inside money supply. This becomes more lucrative as the yield curve steepens or other kinds of risk premia widen, increasing the net interest margins (NIMs). As the banking sector responds to changes in demand it equilibrates asset prices.

This is another way of coming to the same conclusion: that a free banking system would tend to stabilize NGDP in response to endogenous demand shocks. But how about supply shocks? We know that when the spread between the banks’ return on assets and costs of funding widens, the balance sheet will increase. An increase in productivity will raise both the return on new investments and the rate the banks have pay on deposits. We can assume for now these cancel out. But the public will have a higher demand for notes, and since notes pay no interest, they are a very cheap source of funding. This lowers the average cost of funding overall. However, more gross clearings will increase the demand for reserves and their cost of borrowing relative to the yield on other assets. This would put a check on overexpansion and excess maturity transformation. The net effect on the total inside money supply is uncertain, but probably positive assuming the amount of currency held by the public is larger than borrowed reserves by banks.

Another thing to consider about supply shocks: despite the lower funding costs of increased note issuance, an increase in the natural rate of interest will decrease banks’ net interest margins because their loan book will be locked in at the old, lower rate, but the rate on deposits will have to go up. This is a counter-cyclical effect (in both directions) that may outweigh the transaction demand effect. Another possible counter-cyclical effect is the psychological liquidity preference effect that accompanies optimism associated with supply shocks. So in a strong economy individuals will be more willing to hold the market portfolio directly, which flattens the SML. Depending on the strength of these effects, it may lead to different results than Salter and Young.

Why the Austrian business cycle theory needs an update

I have been thinking about this topic for a little while, even though it might be controversial in some circles. By providing me with a recent paper empirically testing the ABCT, Ben Southwood, from ASI, unconsciously forced my hand.

I really do believe that a lot more work must be done on the ABCT to convince the broader public of its validity. This does not necessarily mean proving it empirically, which is always going to be hard given the lack of appropriate disaggregated data and the difficulty of disentangling other variables.

However, what it does mean is that the theoretical foundations of the ABCT must be complemented. The ABCT is an old theory, originally devised by Mises a century ago and to which Hayek provided a major update around two decades later. The ABCT explains how an ‘unnatural’ expansion of credit (and hence the money supply) by the banking system brings about unsustainable distortions in the intertemporal structure of production by lowering the interest rate below its Wicksellian natural level. As a result, the theory is fully reliant on the mechanics of the banking sector.

The theory is fundamentally sound, but its current narrative describes what would happen in a relatively free market with a relatively free banking system. At the time of Mises and Hayek, the banking system indeed was subject to much lighter regulations than it is now and operated differently: banks’ primary credit channel was commercial loans to corporations. The Mises/Hayek narrative of the ABCT perfectly illustrates what happens to the economy in such circumstances. Following WW2, the channel changed: initiative to encourage home building and ownership resulted in banks’ lending approximately split between retail/mortgage lending and commercial lending. Over time, retail lending developed further to include an increasingly larger share of consumer and credit card loans.

Then came Basel. When Basel 1 banking regulations were passed in 1988, lending channels completely changed (see the chart below, which I have now used several times given its significance). Basel encouraged banks’ real estate lending activities and discouraged banks’ commercial lending ones. This has obvious impacts on the flow of loanable funds and on the interest rate charged to various types of customers.

In the meantime, banking regulations have multiplied, affecting almost all sort of banking activities, sometimes fundamentally altering banks’ behaviour. Yet the ABCT narrative has roughly remained the same. Some economists, such as Garrison, have come up with extra details on the traditional ABCT story. Others, such as Horwitz, have mixed the ABCT with Yeager’s monetary disequilibrium theory (which is rejected by some other Austrian economists).

While those pieces of academic work, which make the ABCT a more comprehensive theory, are welcome, I argue here that this is not enough, and that, if the ABCT is to convince outside of Austrian circles, it also needs more practical, down to Earth-type descriptions. Indeed, what happens to the distortions in the structures of production when lending channels are influenced by regulations? This requires one to get their hands dirty in order to tweak the original narrative of the theory to apply it to temporary conditions. Yet this is necessary.

Take the paper mentioned at the beginning of this post. The authors find “little empirical support for the Austrian business cycle theory.” The paper is interesting but misguided and doesn’t disprove anything. Putting aside its other weaknesses (see a critique at the bottom of this post*), the paper observes changes in prices and industrial production following changes in the differential between the market rate of interest and their estimate of the natural rate. The authors find no statistically significant relationship.

Wait a minute. What did we just describe above? That lending channels had been altered by regulation and political incentives over the past decades. What data does the paper rely on? 1972 to 2011 aggregate data. As a result, the paper applies the wrong ABCT narrative to its dataset. Given that lending to corporations has been depressed since the introduction of Basel, it is evident that widening Wicksellian differentials won’t affect industrial structures of production that much. Since regulation favour a mortgage channel of credit and money creation, this is where they should have looked.

But if they did use the traditional ABCT narrative, it is because no real alternative was available. I have tried to introduce an RWA-based ABCT to account for the effects of regulatory capital regulation on the economy. My approach might be flawed or incomplete, but I think it goes in the right direction. Now that the ABCT benefits from a solid story in a mostly unhampered market, one of the current challenges for Austrian academics is to tweak it to account for temporary regulatory-incentivised banking behaviour, from capital and liquidity regulations to collateral rules. This is dirty work. But imperative.

Major update here: new research seems to confirm much of what I’ve been saying about RWAs and the changing nature of financial intermediation.

* I have already described above the issue with the traditional description of the ABCT in this paper, as well as the dataset used. But there are other mistakes (which also concern the paper they rely on, available here):

– It still uses aggregate prices and production data (albeit more granular): the ABCT talks about malinvestments, not necessarily of overinvestment. The (traditional) ABCT does not imply a general increase in demand across all sectors and products. Meaning some lines of production could see demand surge whereas other could see demand fall. Those movements can offset each other and are not necessarily reflected in the data used by this study.

– It seems to consider that aggregate price increases are a necessary feature of the ABCT. But inflation can be hidden. The ABCT relies on changes in relative prices. Moreover, as the structure of production becomes more productive, price per unit should fall, not increase.

Is the BIS on the Dark Side of macroeconomics?

The BIS has got a hobby: to annoy other economists and central bankers. It’s a good thing. It published its annual report about two weeks ago, and the least we can say is that it didn’t please many.

Gavin Davies wrote a very good piece in the FT last week, summarising current opposite views: “Keynesian Yellen versus Wicksellian BIS”. What’s interesting is that Davies views the BIS as representing the ‘Wicksellian’ view of interest rates: that current interest rates are lower than their natural level (i.e. monetary policy is ‘loose’ or ‘easy’). On the other hand, Scott Sumner and Ryan Avent seem to precisely believe the opposite: that current rates are higher than their natural level and that the BIS is mistaken in believing that low nominal rates mean easy money. This is hard to reconcile both views.

Neither is the BIS particularly explicit. Why does it believe that interest rates are low? Because their headline nominal level is low? Because their real level is low? Or because its own natural rates estimates show that central banks’ rates are low?

It is hard to estimate the Wicksellian ‘natural rate’ of interest. Some people, such as Thomas Aubrey, attempt to estimate the natural rate using the marginal product of capital theory. There are many theories of the rate of interest. Fisher (described by Milton Friedman as America’s best ever economist), Bohm-Bawerk, and Mises would argue that the natural interest rate is defined by time preference (even though they differ on details), and Keynes liquidity preference. Some economists, such as Miles Kimball, currently argue that the natural rate of interest is negative. This view is hard to reconcile with any of the theories listed above. Fisher himself declared in The Rate of Interest that interest rates in money terms cannot be negative (they can in commodity terms).

Unfortunately, and as I have been witnessing for a while now, Wicksell is very often misinterpreted, even by senior economists. The latest example is Paul Krugman, evidently not a BIS fan. Apart from his misinterpretation of Wicksell (see below), he shot himself in the foot by declaring (my emphasis):

Now, what about the BIS? It is arguing that central banks have consistently kept rates too low for the past couple of decades. But this is not a statement about the Wicksellian natural rate. After all, inflation is lower now than it was 20 years ago.

Given that we indeed got two decades of asset bubbles and crashes, it looks to me that the BIS view was vindicated…

Furthermore, in a very good post, Thomas Aubrey corrects some of those misconceptions:

The second issue to note is that when the natural rate is higher than the money rate there is no necessary impact on the general price level. As the Swedish economist Bertie Ohlin pointed in the 1930s, excess liquidity created during a Wicksellian cumulative process can flow into financial assets instead of the real economy. Hence a Wicksellian cumulative process can have almost no discernible impact on the general price level as was seen during the 1920s in the US, the 1980s in Japan and more recently in the credit bubble between 2002-2007.

(Bob Murphy also wrote a very good post here on Krugman vs. Wicksell)

But there are other problematic issues. First, inflation (as defined by CPI/RPI/general increase in the price level) itself is hard to measure, and can be misleading. Second, as I highlighted in an earlier post, wealthy people, who are the ones who own most investible assets, experience higher inflation rates. In order to protect their wealth from declining through negative real returns (what Keynes called the ‘euthanasia of the rentiers’), they have to invest it in higher-yielding (and higher-risk) assets, causing bubbles is some asset classes (while expectations that central bank support to asset prices will remain and allow them to earn a free lunch, effectively suppressing risk-aversion).

If natural rates were negative – or at least very low – and the environment deflationary, it is unlikely that we would witness such hunt for yield: people care about real rates, not nominal ones (though in the short-run, money illusion can indeed prevail). But this is not only an ultra-rich problem: there are plenty of stories of less well-off savers complaining of reduced purchasing power.

Meanwhile, the rest of the population and overleveraged companies, supposedly helped by lower interest rates, seem not to deleverage much: overall debt levels either stagnate or even increase in most economies, as the BIS pointed out.

Banks also suffer from the combination of low rates* and higher regulatory requirements that continue to pressurise their bottom line, and have ceased to pass lower rates on to their customers.

In this context, the BIS seems to have a point: rates may well be too low. Current interest rate levels seem to only prevent the reallocation of capital towards more economically efficient uses, while struggling banks are not able to channel funds to productive companies.

Critics of the BIS point to their call to rise rates to counter inflation back in 2011. Inflation, as conventionally measured, indeed hasn’t stricken in many countries. In the UK and some other European countries though, complaints about quickly rising prices and falling purchasing power have been more than common (and I’m not even referring to house price inflation). This mismatch between aggregate inflation indicators and widespread perception is a big issue, which underlies financial risk-taking.

In the end, Keynes’ euthanasia of the rentiers only seem to prop up dying overleveraged businesses and promote asset bubbles (and financial instability) as those rentiers pile in the same asset classes. I side with the BIS in believing this is not a good and sustainable policy.

I also side with the BIS and with Mohamed El-Erian in believing in the poor forecasting ability of most central bankers, who seem to constantly display a dovish view of the economy, which apparently experiences never-ending ‘slack’, as well as the very uncertain effect of macro-prudential policies, which cannot and will not get in all the cracks. Nevertheless, many mainstream economists and economic publications seem to be overconfident in the effectiveness of macro-prudential policies (see The Economist here, Yellen here, Haldane here, who calls macropru policies “targeted lightning strikes”…).

While central banks’ rates should probably already have risen in several countries (and remain low in others, hence the absurdity of having a single monetary policy for the whole Eurozone), everybody should keep the BIS warnings in mind: after all, they were already warning us before the financial crisis, yet few people listened and many laughed at them.

Unfortunately, politicians and regulators have repeated some of the mistakes made during the Great Depression: they increased regulation of business and banking while the economy was struggling. I have many times referred to the concept of regulatory uncertainty, as well as the over-regulation that most businesses are now subject to (in the US at least, though this is also valid in most European countries). Businesses complaints have been increasing and The Economist reported on that issue last week.

In the meantime, while monetary policy has done (almost) everything it could to boost credit growth and to prevent the money supply from collapsing, harsher banking regulation has been telling banks to do the exact opposite: raise capital, deleverage, and don’t take too much risk.

In the end, monetary policy cannot fix those micro-level issues. It is time to admit that we do not live in the same microeconomic environment as before the crisis. What about cutting red tape to unleash growth rather than risk another financial crisis?

* Yes, for banks, rates are low, whichever way you look at them. Banks can simply not function by earning zero income on their interest-earning assets (loan book and securities portfolio).

PS: Noah Smith, another member of the anti-BIS crowd, has a nonsense ‘let’s keep interest rate low forever’-type article here: raising interest rates would lead to an asset price crash, so we should keep them low to have a crash later. Thanks Noah. The way he describes a speculative bubble is also wrong (my emphasis):

The theory of speculation tells us that bubbles form when people think they can find some greater fool to sell to. But when practically everyone is convinced that asset prices are relatively high, like now, it’s pretty obvious that there aren’t many greater fools out there.

Really? No, speculation involved buying as long as you believe you can get the right timing to exit the position. Even if everyone believed that asset prices were overvalued, as long as investors expect prices to continue to increase, speculation would continue: profits can still be made by exiting on time, even if you join the party late.

PPS: A particularly interesting chart from the BIS report was the one below:

It is interesting to see how coordinated financial cycles have become. Yet the BIS seems not to be able to figure out that its own work (i.e. Basel banking rules) could well be the common denominator of those cycles (which were rarely that synchronised in the past).

It is interesting to see how coordinated financial cycles have become. Yet the BIS seems not to be able to figure out that its own work (i.e. Basel banking rules) could well be the common denominator of those cycles (which were rarely that synchronised in the past).

Blame the rich for the next asset bubble. Or not.

First of all, happy new year to all of you! Fingers crossed we don’t witness another market crash this year! 🙂

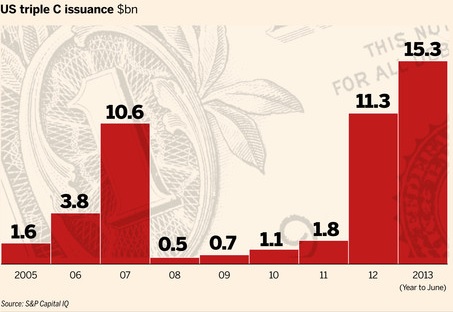

Indeed, credit markets are hot. Equity markets are also hot. The FT published an article yesterday with some striking facts about the ‘improvements’ in credit markets over the past couple of years. Some would say that it’s encouraging. I am not convinced…

Most credit indicators are close to or above their pre-credit crisis high. Sales of leveraged loans and high-yield bonds are above their pre-crisis peak. The average leverage level of US LBOs is back to 2006 level. Issuance of collateralised loan obligations is close to its pre-crisis peak. Even CCC-rated junk bonds are way above their previous peak. I’ve already mentioned some of those facts a few months ago.

In a relatively recent presentation, Citi’s strategist Hans Lorenzen confirmed the trend: central banks are indirectly suppressing most risky investments’ risk premia. Most investors expect junk bonds’ spreads to tighten further or at least to stabilise at those narrow levels and emerging markets bonds and equities, as well as junk bonds are now among investors’ top asset classes .

My ‘theory’ at the time was that (see also here), if investors were piling in increasingly riskier asset classes, bringing their yield down to record low levels in the process, and nonetheless accepting this level of risk for such low returns, it was because current central bank-defined nominal interest rates were below the Wicksellian natural rate of interest. Inflation, as felt by investors rather than the one reported by national statistics agencies, was higher than most real rates of return on relatively safe assets. In order to see their capital growing (or at least to prevent it from declining), they were forced to pick riskier assets, such as high-yield bonds, which were not really high-yield anymore as a result but remained junk nonetheless. This would result in capital misallocation as, under ‘natural’ interest rate conditions, those investments would have never taken place. Thomas Aubrey’s Wicksellian differential, an indicator of the likely gap between the nominal and the natural rates of interest, was, in line with credit markets, reaching its pre-crisis high and seemed to confirm that ‘theory’.

Well, I now think that not all investors are responsible for what we are witnessing today. The (very) rich are.

This came to my mind some time ago while reading that FT piece by John Authers. This was revealing.

“Their wealth gives them scope to try imaginative investments, but they are terrified of inflation, even as deflation is emerging as a greater risk. That is in part because inflation for the goods and services bought by the very rich is running about 2 percentage points faster than retail inflation as a whole in the UK.” (my emphasis)

In the UK, real gilts’ yields were already in negative territory: adjusted by the (potentially underestimated) consumer price index, gilts were yielding around -1% early 2013. Savers were effectively losing money by investing in those bonds. Now think about the rich: by investing in such bonds, they would get a real return of around -3% instead.

Moreover, “71 per cent of respondents said they were more worried now about a steep rise in inflation than they were five years ago.”

Does it start to make sense? The cost of living I was mentioning earlier is increasing particularly quickly for the rich. And… they are the ones who own most financial assets. In order to offset those rising living costs, they naturally look for higher-yielding investments. And it is exactly what the FT reports:

“Their favourite asset classes for the next three decades are emerging markets equities, developed equities and agricultural land, in that order. Private equity comes close after farmland, while art and collectables were also a more popular asset class than any kind of bonds. […]

Hedge funds, as a group, have not fared well since the crisis. But wealthy investors preoccupied by inflation, and robbed of the easy option of bonds, are evidently disposed to give them a try, with an average projected allocation for the next three decades of 25 per cent. Meanwhile, the chance of a bubble in agricultural land prices, or in art, looks very real.”

Are the rich responsible for our current frothy markets then? Obviously not. They are acting rationally in response to central banks’ policies. Nonetheless, this raises an interesting question. Mainstream economics only considers a high aggregate inflation rate as dangerous. What about ‘class warfare’-type inflation? It does look like inflation experienced by one socioeconomic class could inadvertently lead to asset bubbles and bursts, despite aggregate inflation remaining subdued. This may be another destabilising effect of monetary injections on relative prices.

Granted, central banks possibly are on a Keynesian’s ‘euthanasia of the rentier’-type scheme in order to try to alleviate the pain of over-indebted borrowers (and/or to encourage further lending). But financial repression avoidance might well end-up coming back with a vengeance if savers’ reactions, and in particular, rich savers’, make financial markets bubble and crash.

Charts: FT (link above), Citi and Societé Générale

Banks’ risk-weighted assets as a source of malinvestments, booms and busts

Here I’m going to argue that Basel-defined risk-weighted assets, a key component of banking regulation, may be partly responsible for recent business cycles.

Readers might have already noticed my aversion to risk-weighted assets (RWAs), which I view as abominations for various reasons. They are defined by Basel accords and used in regulatory capital ratios. Basel I (published in 1988 and enforced from 1992) had fixed weights by asset class. For example, corporate loans and mortgages would be weighted respectively 100% and 50%, whereas OECD sovereign debt would be weighted 0%. If a bank had USD100bn of total assets, applying risk-weights could, depending on the lending mix of the bank, lead to total RWAs of anything between USD20bn to USD90bn. Regulators would then take the capital of the bank as defined by Basel (‘Tier 1’ capital, total capital…) and calculate the regulatory capital ratio of the bank: Tier 1 capital/RWAs. Basel regulation required this ratio to be above 4%.

Basel II (published in 2004 and progressively implemented afterwards) introduced some flexibility: the ‘Standardised method’ was similar to Basel I’s fixed weights with more granularity (due to the reliance on external credit ratings), while the various ‘Internal Ratings Based’ methods allowed banks to calculate their own risk-weight based on their internal risk management models (‘certified’ by regulators…).

This system is perverse. Banks are profit-maximising institutions that answer to their shareholders. Shareholders on the other hand have a minimal threshold under which they would not invest in a company: the cost of capital, or required return on capital. As a result, return on equity (ROE) has to at least cover the cost of capital. If it doesn’t, economic losses ensue and investors would have been better off investing in lower yielding but lower risk assets in the first place. But Basel accords basically dictate banks how much capital they need to hold. Therefore banks have an incentive in trying to ‘manage’ capital in order to boost ROE. Under Basel, this means pilling in some particular asset classes.

Let’s make very rough calculations to illustrate the point under a Basel II Standardised approach: a pure commercial bank (i.e. no trading activity) has a choice between lending to SMEs (option 1) or to individuals purchasing homes (option 2). The bank has EUR1bn in Tier 1 capital available and wishes to maximise returns while keeping to the minimum of 4% Tier 1 ratio. We also assume that external funding (deposits, wholesale…) is available and that the marginal increase in interest expense is always lower than the marginal increase in interest income.

- Option 1: Given the 100% risk-weight on SME lending, the bank could lend EUR25bn (25bn x 100% x 4% = 1bn), at an interest rate of 7% (say), equalling EUR1.75bn in interest income.

- Option 2: Mortgage lending, at a 35% risk-weight, allows the same bank to lend a total of EUR71.4bn (71.4bn x 35% x 4% = 1bn) for EUR1bn in capital, at an interest rate of 3% (say), equalling EUR2.14bn in interest income.

The bank is clearly incentivised to invest its funding base in mortgages to maximise returns. In practice, large banks that are under the IRB method can push mortgage risk-weights to as low as barely above 10%, and corporate risk-weights to below 50%. As a result, banks are involuntarily pushed by regulators to game RWAs. The lower RWAs, the lower capital the bank needs, the higher its ROE and the happier the regulators. Banks call this ‘capital optimisation’.

Consequently, does it come as a surprise that low-risk weighted asset classes were exactly the ones experiencing bubbles in pre-crisis years? Oh sorry, you don’t know which asset classes were lowly rated… Here they are: real estate, securitisation, OECD sovereign debt. Yep, that’s right. Regulatory incentives that create crises. And the new Basel III regime does pretty much nothing to change the incentivised economic distortions introduced by its predecessors.

Yesterday, Fitch, the rating agency, published a study of lending and RWAs among Europe’s largest banks (press release is available here, full report here but requires free subscription). And, what a surprise, corporate lending is going…down, while mortgage lending and credit exposures to sovereigns are going…up (see charts below). The trend is even exacerbated as banks are under pressure from regulators to boost regulatory capitalisation and from shareholders to improve ROE. And this study only covers IRB banks. My guess is that the situation is even more extreme for Standardised method banks that cannot lower their RWAs.

The ‘funny’ thing is: not a single regulator or central banker seems to get it. As a result, we keep seeing ill-founded central banks schemes aiming at giving SME lending a boost, like the Funding for Lending Scheme launched by the Bank of England in 2012, which provided banks with cheap funding. Yes, you guessed it: SME lending continued its downward trend and the scheme provided mortgage lending a boost.

Should the situation ‘only’ prevent corporates to borrow funds, bad economic consequences would follow but remain limited. Economic growth would suffer but no particular crisis would ensue. The problem is: Basel and RWAs force a massive misallocation of capital towards a few asset classes, resulting in bubbles and large economic crises when the crash occurs.

The Mises and Hayek Austrian business cycle theory emphasises the distortion in the structure of relative prices that emanates from central banks lowering the nominal interest rate below the natural rate of interest as represented by economic agents’ intertemporal preferences, resulting in monetary disequilibrium (excess supply of money). The consequent increase in money supply flows in the economy through one (or a few) entry points, increasing the demand in those sectors, pushing up their prices and artificially (and unsustainably) increasing their return on investment.

I argue here that due to Basel’s RWAs distortions, central banks could even be excluded from the picture altogether: banks are naturally incentivised to channel funds towards particular sectors at the expense of others. Correspondingly, the supply of loanable funds increases above equilibrium in the favoured sectors (hence lowering the nominal interest rate and bringing about an unsustainable boom) but reduces in the disfavoured ones. There can be no aggregate overinvestment during the process, but bad investments (i.e. malinvestments) are undertaken: the investment mix changes as a result of an incentivised flow of lending, rather than as a result of economic agents’ present and future demand. Eventually, the mismatch between expected demand and actual demand appears, malinvestments are revealed, losses materialise and the economy crashes. Central banks inflation worsen the process through the mechanism described by the Austrians.

I am not sure that regulators had in mind a process to facilitate boom and bust cycles when they designed Basel rules. The result is quite ‘ironic’ though: regulations developed to enhance the stability of the financial sector end up being one of the very sources of its instability.

RWA-based ABCT Series:

- Banks’ risk-weighted assets as a source of malinvestments, booms and busts

- Banks’ RWAs as a source of malinvestments – Update

- Banks’ RWAs as a source of malinvestments – A graphical experiment

- Banks’ RWAs as a source of malinvestments – Some recent empirical evidence

- A new regulatory-driven housing bubble?

The Economist struggles with Wicksell

Looks like Wicksell is back in fashion. After years (decades?) with barely any mention of this distinguished Swedish economist outside of work from some heterodox economic schools academics (like the Austrians), he is now everywhere and has unleashed a great debate among academics and financial practitioners. This is the outcome of both the financial crisis (preceded by interest rates that were below their ‘natural’ level according to Wicksellian-based theories) and the current unconventional policies undertaken by central banks all over the world (that risk repeating the same mistakes according to those same theories).

This week’s Economist’s column Free Exchange tries to identify whether or not current interest rates are too low based on a Wicksellian framework (A natural long-term rate). The article is complemented by a Free Exchange blog post on the newspaper’s website.

I won’t get back to the definitions of Wicksell’s money and natural rates of interest as I’ve done it in two recent posts (here and here). I only wish today to comment on The Economist’s interpretation (and misconceptions) of the Wicksellian rate.

A few of things shocked me in this week’s column. First, the assertions that “the natural rate prevails when the economy is at full employment” and that “the natural interest rate is often assumed to be constant.” I’m sorry…what? Putting aside the fact that ‘full employment’ is hard to define, there can be full employment with interest rates below or above their natural level, and interest rates can be at their natural level with the economy not at full employment. Many other ‘real’ factors have effects on ‘full employment’. Using full employment as a basis for spotting the equilibrium rate is dangerous.

Second, where did they get that the natural interest rate was constant? This doesn’t make sense. The natural interest rate rises and decreases following a few variables (various economic schools of thought will have differing opinions) such as time preference (i.e. whether or not people prefer to use income for immediate or future consumption), marginal product of capital (demand for loanable funds by entrepreneurs would increase as long as they can make a profit on the marginal increase in capital stock, driving up the interest rate in the process), liquidity preference (i.e. whether or not people desire to hold money as cash rather than some other less liquid form of wealth – pretty much the only important factor driving the interest rate for Keynesians –)… As you can imagine, all those factors vary constantly, impacting the demand for money and the demand for credit and in turn the rate of interest. It clearly does not remain constant…

The Economist also dismisses the possibility that real interest rates are too low by the fact that sovereign bonds’ yields are low, not only in the US (where the Fed is engaged in massive bonds purchases), but also in other economies whose central banks are less active in purchasing sovereign debt. But it overlooks the fact that natural rates aren’t uniform and may well be lower in other countries (for example, the natural rate was probably lower in Germany than in Spain and Ireland before the crisis, despite having a common central bank). It also overlooks that ‘risk-free’ rates used as a basis of most financial calculations internationally are US Treasuries, not sovereign bonds of other countries.

Finally, in support of its point, the column argues that expected future low rates could also reflect investors’ expectations of sluggish future growth and that “despite profit margins near record levels and rock-bottom interest rates, business investment has been sluggish, recently peaking at just above 12% of GDP; it topped 14% in the late 1990s.” Once again, this is misinterpreting the natural rate: the level of the natural rate of interest does not necessarily depend on expected future economic growth as I described above. Sluggish business investments also are more likely to reflect current regulatory ‘regime uncertainty’ than entrepreneurs’ doubts about the future state of the economy. On top of that, using the dotcom bubble as a reference for business investment is intellectually dishonest. Moreover, the article contradicts itself starting with “central banks ignore this century-old observation at their peril” only to conclude that “all this suggests that policy rates, low as they seem, are not out of line with their natural level.” Hhhmmm, ok.

The Free Exchange blog post by Greg Ip is a little better but still overall quite confused and confusing. Interestingly, it cites a paper by Bill White (http://dallasfed.org/assets/documents/institute/wpapers/2012/0126.pdf) who argues that the sort of yield-chasing that we can witness in financial markets today is a symptom of nominal rates being lower than natural rates. Doesn’t this remind you of anything? That’s right; it was exactly my point in this post. But it then cites Brad de Long, who can be added to the list of people who don’t understand what regulatory uncertainty is, and who tries as a result to convince us that the natural rate is below zero. Theoretically, a below zero natural rate if possible in period of deflation. But it does not make much sense to have a natural rate below zero when inflation is above zero.

It is definitely a hard task to identify the natural rate of interest. Nonetheless, a few rules of thumb are sometimes better than overly-complex reasoning. Investors would be perfectly happy with negative nominal yields if cost of life was declining even faster. This is obviously not the case at the moment.

The ‘great search for yield’ update, Taleb on bank disintermediation and Coeuré on Wicksell

This is a quick update on my post of last week on the rush for yield among private investors and what it meant in terms of interest rate disequilibrium.

Following my post, Thomas Aubrey from Credit Capital Advisory kindly provided me with an update of his ‘Wicksellian differential’ chart. You can also find it here.

As you can see the differential between the estimated natural rate and the money rate of interest in the US have kept increasing and almost reached pre-crisis peak. According to his calculation, the potential differential now reaches………10%. It’s indeed huge. Try for a second to imagine the Fed all of a sudden increasing their target interest rate by 10%…… No you’re right, we just can’t imagine it. Frankly, I hope his calculation is wrong but…I wouldn’t bet my life on it. Consequently, Thomas Aubrey believes that it backs up my claim about malinvestments.

As you can see the differential between the estimated natural rate and the money rate of interest in the US have kept increasing and almost reached pre-crisis peak. According to his calculation, the potential differential now reaches………10%. It’s indeed huge. Try for a second to imagine the Fed all of a sudden increasing their target interest rate by 10%…… No you’re right, we just can’t imagine it. Frankly, I hope his calculation is wrong but…I wouldn’t bet my life on it. Consequently, Thomas Aubrey believes that it backs up my claim about malinvestments.

Meanwhile, in a speech called ‘The economic consequences of low interest rates’ at the International Center for Monetary and Banking Studies on the 9 October, Benoit Coeuré, member of the Executive Board of the European Central Bank, misunderstood Wicksell and inflation, justifying very low interest rates. Not only Mr Coeuré seems to believe that CPI adequately reflects inflation, but also, according to him, inflation is always zero when the money rate of interest equals the natural rate. This is not true: real shocks can temporarily push inflation one way or another, but over the longer term productivity becomes the main driver behind inflation and deflation. In a world of productivity increases (and increasing output), deflation should be the norm (as it was the case at the end of the 19th century and early 20th). A zero level of inflation in this context would actually mean that there is hidden inflation. George Selgin has written a lot on this. See his Less than Zero book or this video.

Last Friday, FT’s Henny Sender discussed the Fed’s impact on markets. According to a Hong Kong-based hedge fund “the Fed is always there. It is clear that it will not tolerate a decline in asset values. If you sell in the face of QE, you look like an idiot.” Sounds like the best way to completely distort markets. Free markets you said?

Today, John Authers, in another FT piece, says that “Western economy is overcentralised, creating extra risk”. I obviously won’t disagree with him. He cites Nicholas Taleb (reminding me of Larry White). But one thing particularly struck me: Taleb seems to think that hedge funds “are developing strategies that aim to disintermediate the banks, such as loan funds.” This is very, very close to my own opinion, which I haven’t mentioned yet on this blog: technological developments will enable shadow banking to grow under one form or another to desintermediate credit creation. This is something big, and it will require many blog posts and possibly a research paper…and some time.

{kind=link}

{kind=link}

Recent Comments