A UK housing bubble? Sam Bowman doubts it

On the Adam Smith Institute’s blog, Sam Bowman had a couple of posts (here and a follow-up here, and mentioned by Lars Christensen here) attempting to explain that there might not have been any house price bubble in the UK. He essentially says that there was no oversupply of housing in the 1990s and 2000s. Here’s Sam:

These charts show that housing construction was actually well below historical levels in the 1990s and 2000s, both in absolute terms and relative to population. It is difficult to see how someone could claim that the 2008 bust was caused by too many resources flowing toward housing and subsequently needing time to reallocate if there was no bubble in housing to begin with.

What this suggests is that the Austrian story about the crisis may be wrong in the UK (and, if Nunes’s graphs are right, the US as well). The Hayek-Mises story of boom and bust is not just about rises in the price of housing: it is about malinvestments, or distortions to the structure of production, that come about when relative prices are distorted by credit expansion.

Well, I think this is not that simple. Let me explain.

First, the Hayek/Mises theory does not apply directly to housing. In the UK, there are tons of reasons, both physical and legal, why housing supply is restricted. As a result, increased demand does not automatically translate into increased supply, unlike in Spain, which seems to have lower restrictions as shown by the housing start chart below:

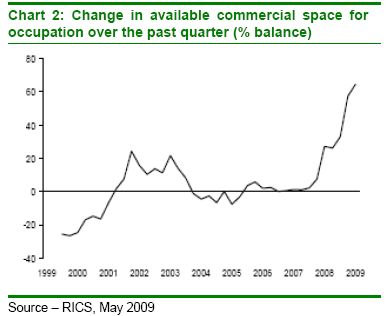

Second, Sam overlooks what happened to commercial real estate. There was indeed a CRE boom in the UK and CRE was the main cause of losses for many banks during the crisis (unlike residential property, whose losses remained relatively limited).

Third, the UK is also characterised by a lot of foreign buyers, who do not live in the UK and hence not included in the population figures. Low rates on mortgages help them purchase properties, pushing up prices, triggering a reinforcing trend while supply in the demanded areas often cannot catch up.

Fourth, the impact of Basel regulations seems to be slightly downplayed. Coincidence or not, the first ‘bubble’ (in the 1980s) appeared right when Basel’s Risk Weighted Assets were introduced. And it is ‘curious’, to say the least, that many countries experienced the same trend at around the same time. Would house lending and house prices have increased that much if those rules had never been implemented? I guess not, as I have explained many times. I have yet to write posts on what happened in several countries. I’ll do it as soon as I find some time.

I recommend you to take a look at my RWA-based Austrian Business Cycle Theory, which seems to show that, while there should indeed be long-term real estate projects started (depending on local constraints of course), there is also an indirect distortion of the capital structure of the non-real estate sector.

While there may well be ‘real’ factors pushing up real estate prices in the UK, there also seems to be regulatory and monetary policy factors exacerbating the rise.

- Chart 1: Spanish Property Insight

- Chart 2: FT Alphaville

- Chart 3: Guardian

2 responses to “A UK housing bubble? Sam Bowman doubts it”

Trackbacks / Pingbacks

- - 6 May, 2014

Leave a comment

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

This is a fascinating alternative! I’ve never heard of this side of the argument but I guess there is some truth to it. After all, hasn’t the population boomed in recent years? It may be that there was a surplus in the past but now it is not enough. The question remains whether this theory will be applied. Even if it is, how do we go about solving our current problem?